The Troll Under The Data Center

The company now known as MARA Holdings (MARA) started life as Marathon Patent Group, a firm whose primary business was buying up patents and suing technology companies for infringement.

The polite term for this is "non-practicing entity." The impolite term, the one critics used loudly and in public filings, is patent troll.

When that model fizzled around 2018, management pivoted to Bitcoin (BTC) mining. When crypto went mainstream, they rebranded again. Now they're pivoting to AI infrastructure.

Three corporate identities in 15 years. The market has every right to be skeptical, and I understand the instinct completely.

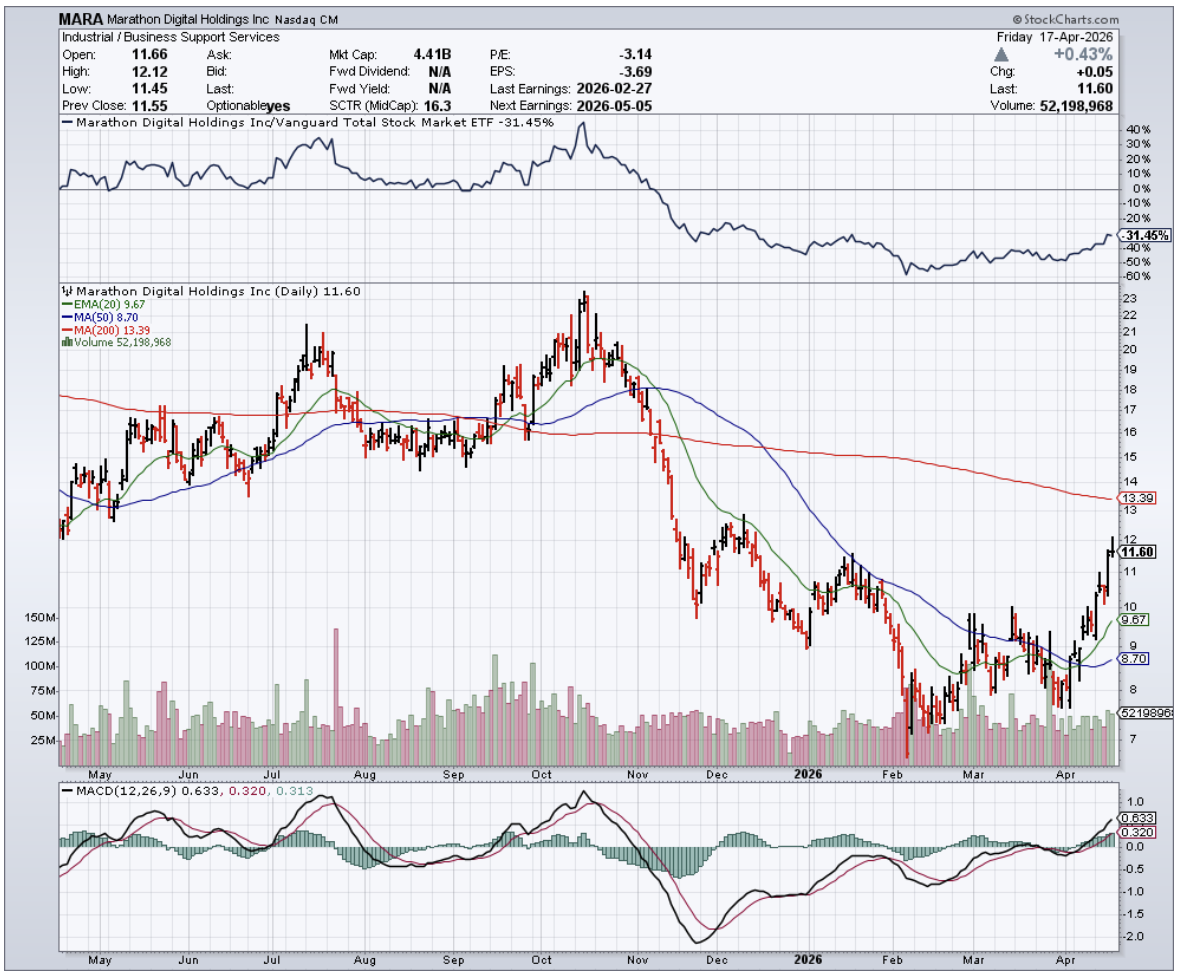

The near-term numbers won't talk you out of that skepticism. Q4 2025 revenue came in at approximately $202 million, down 6%, missing analyst expectations by nearly $50 million.

Daily Bitcoin production fell from 27.1 coins to 21.9, which stings when you consider that the company simultaneously spent money growing its computing power by 25%. More muscle, fewer results.

This is the permanent condition of post-halving Bitcoin mining. Every four years, the block reward gets cut in half, the whole industry keeps piling in anyway, and everyone produces less for more.

G&A expenses ballooned from approximately $19 million to $57 million in a single year, and the company swung from earnings of $1.24 per diluted share to a loss of $4.52.

None of this is a mystery. It's the math of a business model with a structural ceiling.

Which brings us to why the AI pivot is worth taking seriously, even coming from a company with this particular résumé.

Last August, MARA paid approximately $168 million for a 64% stake in Exaion, a computing infrastructure operator that was originally built inside Électricité de France, the French state utility with roughly $122 billion in annual revenues.

EDF didn't sell because it needed the money. It retained a minority stake, stayed on as a paying customer, and sat through a French government regulatory review that scrutinized the deal on national sovereignty grounds. It cleared.

Xavier Niel's NJJ Capital, a name that commands genuine respect in European technology circles, simultaneously took a stake in MARA France as part of the broader arrangement. These are not investors who chase press releases.

The strategic logic is straightforward once you strip away the crypto branding.

MARA already controls the two things AI infrastructure desperately needs and can't conjure overnight: cheap power and physical data center capacity.

Through a separate joint venture with Starwood Capital Group's SDV, it's building toward hyperscale cloud customers using a modular approach that deploys capital in stages rather than in the single massive bets that hyperscalers make.

Faster time to revenue, less capital sitting idle. The company is targeting 1 gigawatt of IT capacity in the near term and says early tenant demand has been strong.

The valuation makes the case on its own.

The forward P/E sits at a multiyear low of 17.77, priced as if the mining business is the whole story. The BTC treasury currently holds approximately 38,689 coins worth roughly $2.9 billion, against a market cap that has been trading in the same neighborhood.

At that math, the Exaion stake, the Starwood joint venture, and 66 exahashes of operating infrastructure are effectively priced at zero.

Obviously, there are risks. BTC sensitivity hasn't gone away, cost discipline is still wanting, and management has a habit of reinventing itself faster than it delivers.

But EDF, Starwood, Niel, and French regulators, who could have simply said no, have all looked at this company and decided to stay in the room.

For a firm that once made its living filing lawsuits, that may be the most valuable intellectual property it has ever produced.