Imagine you're the CEO of a major pharmaceutical company. You've got blockbuster drugs that are raking in billions, a cushy corner office, and a corporate jet at your disposal. Life is good.

But then, you look at the calendar and realize that your patents are about to expire. Suddenly, that jet feels more like a crop duster, and your corner office starts to feel like a broom closet.

That's the reality facing Big Pharma right now. These pharma big shots are sweating bullets over losing their golden geese like AbbVie's (ABBV) Humira and Merck's (MRK) Keytruda.

That’s roughly $300 billion in products about to get kicked to the curb.

But these guys didn't get to the top by sitting on their hands. They've got a war chest of $1 trillion, and they're not afraid to use it.

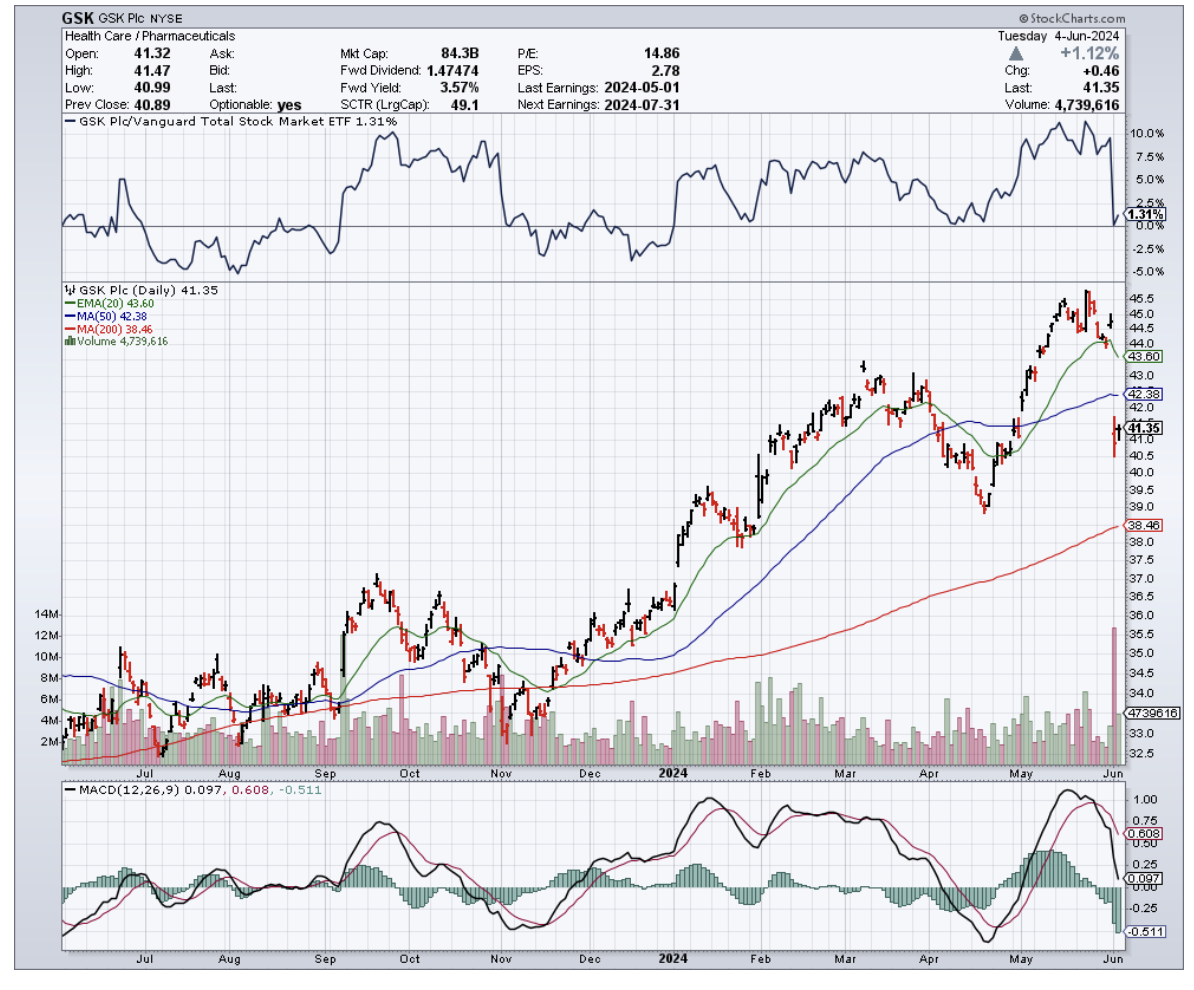

Major pharmaceutical giants like Pfizer (PFE), Roche (RHHBY), Johnson & Johnson (JNJ), AstraZeneca (AZN), and GlaxoSmithKline (GSK) are about to go on the mother of all shopping sprees.

Why the rush? Because they're staring down the barrel of a patent cliff that's going to make the Grand Canyon look like a pothole.

We're talking $198 billion worth of branded drugs going off the patent cliff between 2021 and 2025. That's a gut-wrenching 56% jump from the last five years.

But don't think for a second that they're just going to sit back and watch their profits go up in smoke. No sir, they're on the hunt for the next big thing, and they've got their sights set on some juicy targets – and biotech is at the top of their list.

Leading the biotech charge are mRNA pioneers Moderna (MRNA) and BioNTech (BNTX), each sitting on a gold mine of potential blockbusters taking on everything from flu to cancer vaccines.

Underdogs like CRISPR (CRSP) biotech stars Intellia (NTLA) and Beam Therapeutics (BEAM) are also squarely in Big Pharma's acquisition crosshairs for their cutting-edge work in genetic disease treatments.

But beyond the headliners, don't overlook the sleeper hits that could catalyze the next big boom.

Oncology, in particular, is a prime hunting ground, accounting for 37% of pharma M&A deal value in 2023 as the $392 billion global cancer drug market continues to boom.

Companies like Turning Point Therapeutics (TPTX) and Zentalis Pharmaceuticals (ZNTL), with their promising targeted therapies for various solid tumors, are particularly attractive prospects.

Mirati Therapeutics (MRTX), focused on KRAS inhibitors, and Blueprint Medicines (BPMC), specializing in precision therapies, have also caught the eye of big pharma with their innovative approaches.

Additionally, companies with late-stage assets like MacroGenics (MGNX), Mereo BioPharma (MREO), and Tyra Biosciences (TYRA) could offer promising near-term revenue opportunities for acquiring companies looking to bolster their oncology portfolios.

Close behind are rare disease treatments, snagging 16% of new drug approvals and 9 of the top 100 deals last year in this $262 billion market ripe for more growth.

This lucrative sector has captivated pharma giants, who see potential in companies like Sarepta Therapeutics (SRPT) and Vertex Pharmaceuticals (VRTX), leaders in rare disease therapies with strong financial performance and consistent growth.

Aside from these, smaller biotechs like Amicus Therapeutics (FOLD) and Ultragenyx Pharmaceutical (RARE), focused on developing innovative therapies for a range of rare diseases, are attracting attention for their potential to address unmet medical needs and deliver substantial returns on investment.

But the real wild card everyone wants a piece of is cell and gene therapies. This medical Wild West is projected to explode to $66.8 billion by 2030, with the FDA already greenlighting 6 cutting-edge therapies like next-gen CAR-T treatments from Caribou Biosciences (CRBU) in 2023 alone.

Notably, the buying frenzy is very much already underway. In fact, 2023 saw the biggest biotech M&A spree in a decade, with a staggering $122.2 billion changing hands as the FDA approved 50% more new therapies.

Pharma mega-mergers also hit $135.5 billion as firms raced to reload pipelines.

Interestingly, these deals are only the tip of the iceberg. As Wall Street predicts, with record-smashing deals, sky-high demand, and new approvals surging, "biotech's got plenty of reasons to be cautiously optimistic."

Especially if interest rates finally cooperate, throwing gasoline on the M&A bonfire and making biotech the belle of the ball as soon as late 2024.

So keep your eyes peeled and your powder dry. I suggest you add these innovative biotech names to your watchlist, and you might just discover the next blockbuster drug or breakthrough therapy that could reshape medicine – and deliver explosive returns in the process.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-06-11 12:00:012024-06-11 12:03:04The Capital Cure

I once scaled a mountain everyone swore was cursed after a landslide. They missed out on stunning vistas and the thrill of conquering a challenge. Turns out, the best views often come after a little rock bottoming.

That brings to mind Bristol-Myers Squibb (BMY), the pharma giant fresh off a stock price landslide of its own.

Bristol-Myers Squibb shares have been in a freefall lately, plunging to nearly half their 2022 peak of $80. The culprit? You guessed it: those dreaded patent expirations and a whole lot of hand-wringing about future growth.

However, as a contrarian investor, I see this doom-and-gloom scenario as an opportunity rather than a setback.

Remember those times when the market turned its back on the likes of Meta Platforms (META) and NVIDIA (NVDA)? They were trading for peanuts not so long ago and look at them now.

Now, you might be thinking, "So, BMY's taken a hit. Is it really that undervalued?"

Well, I've been digging through the stock's history, all the way back to 2012, and something interesting popped up: since 2013, BMY has rarely dipped below its 200-week simple moving average (that fancy brown line on your charts). It just recently broke through that floor, which could mean we're looking at a once-in-a-decade buying opportunity.

Every time this stock has even gotten close to that 200-week line, it's been a signal to buy, and the stock has always bounced back.

Let's not forget that just a couple of years ago, this stock was cruising at over $80 a share. Now it's practically a penny stock compared to that. Has the company really lost half its value?

Bristol-Myers Squibb's been facing some headwinds, no doubt about it. Revlimid, their blockbuster cancer treatment, lost patent protection in 2022, and Eliquis, their anti-stroke champ, is set to follow suit in 2026.

But don't count them out just yet. The company still has plenty of promising drugs in its arsenal that aren't facing patent cliffs anytime soon.

Plus, they've been on a shopping spree, snatching up high-potential companies like Karuna, RayzeBio, and Mirati in 2023. These acquisitions could be just the ticket to reignite growth and fill the void left by those expiring patents.

In a strategic move to streamline operations and boost future earnings, Bristol-Myers Squibb also announced a $1.5 billion plan to cut expenses, including eliminating around 2,200 jobs.

Sure, 2024 might be a bit of a transition year with some one-time charges, but this bold move could pave the way for a leaner, meaner, and ultimately more profitable company in the years to come.

Turning to the financials, analysts are forecasting a bit of a slow year for Bristol-Myers Squibb in 2024, with earnings per share of $0.56 on about $46 billion in revenue.

But they're expecting a major rebound in 2025, with earnings soaring to $6.94 per share on similar revenue.

And even though 2026 projections show a slight dip to $6.30 EPS on $43.85 billion revenue, this isn't a company you're buying for explosive growth.

The current stock price is roughly seven times the 2025 earnings estimate. That's a steal, my friends. Sure, they've got a bit of debt on the books – $57.46 billion to be exact, with $9.67 billion in cash. But hey, they still earned a respectable "A2" credit rating, so they're not exactly teetering on the brink.

Now, let's talk about another star of BMY’s show: that sweet, sweet dividend.

Bristol-Myers Squibb is dishing out $0.60 per share each quarter, which adds up to a juicy 5.5% yield. Think about that for a second.

That's more than most money market funds are offering right now, and with the Fed likely to slash interest rates in the near future, those yields are only going to shrink.

Remember that "Fed dot plot" they released earlier this year? It's hinting at a 2.25-point drop in the Fed Funds rate by the end of 2026. That could take us from the current 5.25% to 5.5% range all the way down to 3% to 3.25%.

Imagine how much more tempting that 5.5% dividend yield from Bristol-Myers Squibb will look when money market rates are potentially 40% lower.

That makes Bristol-Myers Squibb's current situation practically irresistible to a contrarian investor like me. We're talking about a stock trading at a price we haven't seen in over a decade, relative to the 200-week simple moving average. That's the kind of bargain that makes my palms sweat.

And that's not all. With a valuation hovering around seven times the 2025 earnings estimate and a dividend yield that makes money market funds look like pocket change, this could be a recipe for serious upside.

Sure, patent expirations are a pain in the you-know-what for every pharma company. But let's not forget those initial years of patent protection are like a golden ticket. Plus, Bristol-Myers Squibb has a proven track record of developing and acquiring blockbuster drugs.

Of course, there's no sugarcoating the challenges and risks, but when a stock's 5.5% yield and a rock-bottom P/E ratio are staring you in the face, it's hard to ignore the potential upside. That's why I'm dipping my toes in with a small initial position, gradually building it up over time.

I'm playing the long game here, folks. I believe that eventually, just like with other beaten-down stocks, investors will wake up and realize the incredible value this historically successful company offers.

In the meantime, that generous dividend will keep those money market-like payouts rolling in while we wait for the share price to rebound.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-06-06 12:00:282024-06-06 12:26:55Is This The Comeback Trail After A Cliffhanger?

Remember the last time you had to pop a pill that felt like a one-size-fits-all solution? I sure do. It was for a nagging cough, and while it did the trick, the side effects left me feeling like I'd been hit by a truck.

Turns out, Big Pharma is facing its own kind of side effects. They spend an average of $2.6 billion and over a decade to bring a new drug to market. That's like betting on a long shot at the Kentucky Derby, but with way worse odds.

But what if we could change the game entirely? What if drug discovery wouldn’t solely be about blindly mixing chemicals and hoping for the best.

Instead, picture a super-smart robot scientist, capable of reading millions of pages of medical research in seconds, understanding how different molecules interact, and even predicting which ones might be effective against a disease.

This AI-powered scientist could then design experiments to test those molecules, analyze the results, and even create new molecules from scratch, tailored to specific diseases and individual patients.

That's the promise of autonomous drug discovery.

While we've already seen robots and miniaturization speed up the drug discovery process, AI is taking it to the next level. I’m talking about AI agents running the entire show, from brainstorming biological theories to designing and running experiments, all with barely a human finger lift.

This isn't just about efficiency. It's a veritable gold mine of benefits: costs slashed, development times cut down, success rates skyrocketing, and a productivity boost that could revolutionize personalized medicine. And why does that matter?

Because it means treatments that are more effective, safer, and tailored to your unique genetic makeup, medical history, and lifestyle. Imagine popping a pill that's not just designed to treat your disease, but designed specifically for you. That's the kind of future autonomous drug discovery could deliver.

Imagine a world where your next prescription is fine-tuned to your genetic makeup, your medical history, your lifestyle. Sounds like bespoke tailoring, but for your health.

And this isn't just hype – it's backed by hard numbers. A recent study by McKinsey & Company found that AI-enabled drug discovery could potentially generate up to $50 billion in annual value by 2026.

The study also highlighted that AI could reduce the time required for drug discovery by up to 50%, while also improving the success rate of clinical trials.

These aren’t merely some abstract predictions either. In fact, some companies are already making waves in this new world of drug discovery.

Recursion Pharmaceuticals (RXRX), for example, is at the forefront of these innovations. They've developed a radical new drug discovery platform that combines advanced robotics, experimental biology, and machine learning to rapidly identify potential new treatments for a wide range of diseases.

Forget dusty labs and slow, painstaking research. Recursion's approach is like giving Sherlock Holmes a supercomputer to solve medical mysteries, and the results speak for themselves: over 2,000 novel biological relationships discovered and a mind-boggling 150 terabytes of relatable biological data generated.

That's the equivalent of roughly 30 million songs, all focused on cracking the code of human biology and disease.

Recursion isn't the only player here. A slew of innovative companies are riding the AI wave, reimagining the drug discovery landscape.

Schrödinger (SDGR) is turbocharging the process with AI and computational wizardry, using algorithms to predict how potential drugs will behave in the body before even stepping foot in a lab.

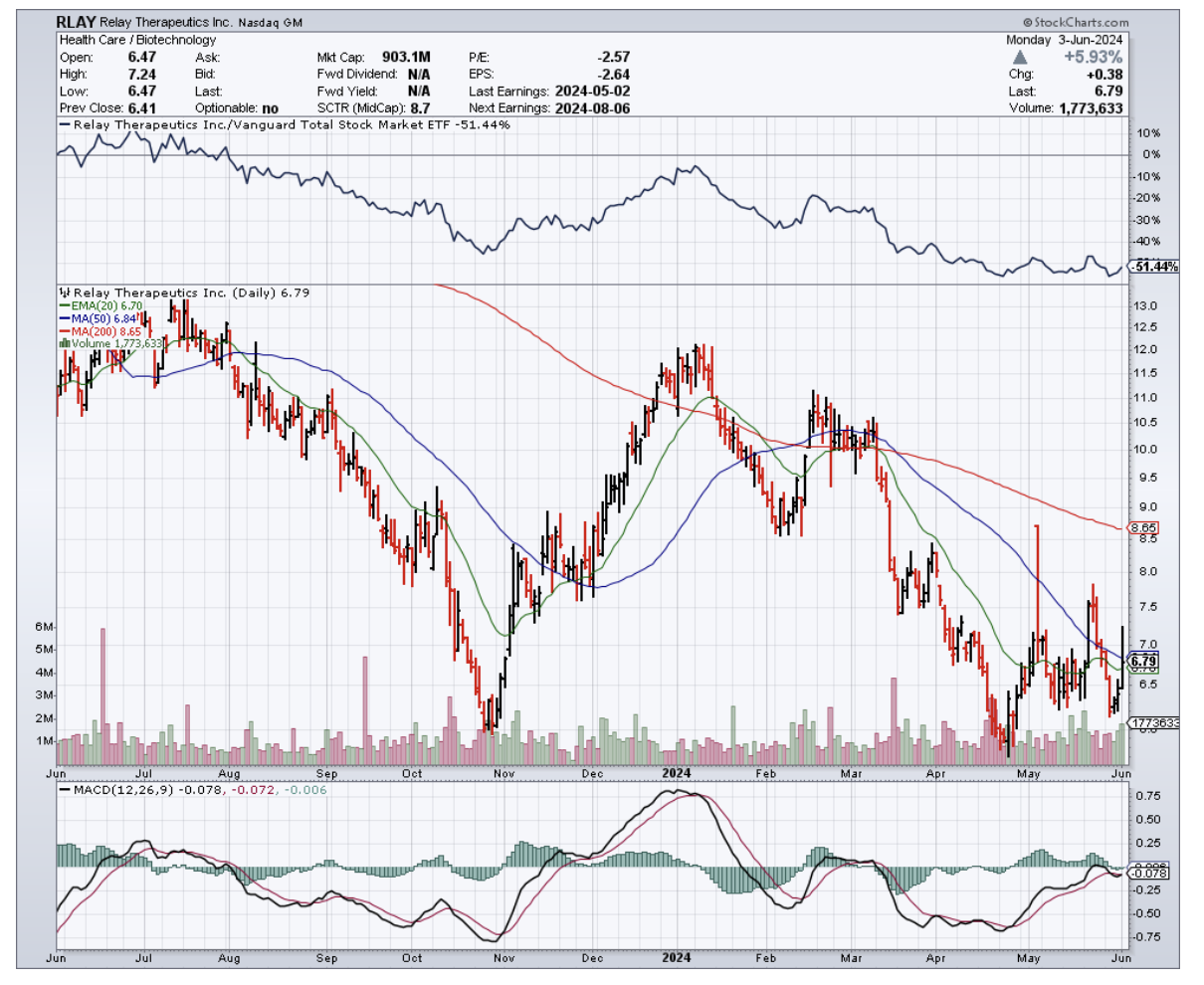

Relay Therapeutics (RLAY) is forging new paths by marrying cutting-edge computation with experimental techniques, focusing on how cancer cells move and change shape to develop targeted therapies.

Exscientia (EXAI), the AI-driven pharmatech company, is designing and discovering new drugs with unprecedented speed, while AbCellera Biologics (ABCL) is harnessing the power of AI and machine learning to decode the secrets of our immune systems, hunting for antibodies that could be developed into life-saving drugs. It’s basically like having a crack team of digital detectives scouring your immune system for clues to fight off diseases.

Meanwhile, BenevolentAI (AMS: BAI) is the top name when it comes to clinical-stage AI drug discovery, using a potent combination of AI, machine learning, and cutting-edge science to unravel the complexities of disease biology and unearth novel treatments. They're not simply content with throwing darts at a target. This company is using AI to pinpoint the bullseye.

But, this AI-powered revolution of the healthcare world isn't happening in a vacuum. It's being supercharged by a tag team of tech titans who are bringing their AI firepower to the table.

Think of it as the Avengers assembling to fight disease, but instead of superpowers, they're armed with algorithms and cloud computing.

Nvidia Corporation (NVDA), IBM Corporation (IBM), and Microsoft Corporation (MSFT) are leading the charge, providing the AI muscle needed to accelerate drug discovery.

Nvidia's Clara Discovery platform, IBM Watson Health, and Microsoft Azure's AI and machine learning services are all being harnessed to build, train, and deploy AI models for a wide range of applications in the biotech and healthcare sectors. It's like having Tony Stark, Bruce Banner, and Thor all working together to create the next medical breakthrough.

And this isn't some wishful thinking. The use of AI in biopharma R&D is projected to skyrocket, growing at a compound annual growth rate of 30% to 40% over the next five years.

Plus, the impact could be huge: AI could potentially boost clinical trial efficiency by 15% to 20% and slash the overall cost of drug development by 10% to 15%. Talk about a win-win situation.

All in all, it’s clear that this AI drug discovery thing isn't just a fad. It's a full-blown revolution that's shaking up the healthcare world as we know it. And while it's still in the early innings, it would be wise to keep a close eye on it. I'm not saying you should throw all your money in right this second, but seriously, put the companies above on your radar.

These are the trailblazers leading the charge into the future of personalized medicine. Who knows, they might just be the ticket to a healthier portfolio—and a healthier you.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-06-04 12:00:562024-06-04 12:21:21From Petri Dish To Personalized Prescriptions

Bob Dylan was right: "The times they are a-changin'". And for Pfizer (PFE), those changing times mean navigating a post-pandemic world and a looming patent cliff. Can they rise to the challenge, or will they be singing the blues?

Pfizer hardly needs an introduction. Founded 175 years ago in 1849 and publicly listed in 1942, Pfizer boasts a market cap of over $160 billion, with highly liquid options trading against its equity.

However, this stock has been on a bit of a rollercoaster lately.

With revenues exceeding $240 billion between 2021 and 2023, largely from vaccines and cancer treatments sold in over 200 countries, Pfizer's reach is undeniable.

But after hitting a record high of $61.71 a share in December 2021, it's taken a nosedive – more than a 50% drop.

So, what gives? Well, it's mostly a combo of waning demand for their Covid-19 products and the dreaded patent cliff looming over some of their top-selling drugs.

At the moment, Pfizer's portfolio paints a mixed picture, with some drugs shining brightly and others facing a cloudier future.

Their pneumonia vaccine duo, Prevnar 13 and 20, remains a reliable workhorse, raking in $6.4 billion in FY23, a 3% increase. With Prevnar 20's patent secure until 2033, it's a safe bet for continued success.

Eliquis, the blood thinner co-marketed with Bristol-Myers Squibb (BMY), is also holding its own, bringing in a respectable $6.7 billion in FY23, up 5%. However, the looming threat of generic competition in 2028 could put a damper on its future prospects.

On the other hand, Vyndaqel, a combination heart and nerve drug, has been a true standout, boasting a remarkable 36% jump in revenue to $3.3 billion in FY23.

Doctors have embraced it for treating a heart condition called ATTR-CM, but its patent situation remains uncertain with a potential expiration in 2024, unless Pfizer's extension to 2028 is approved.

Not all is rosy in Pfizer's garden though.

Comirnaty, their COVID-19 vaccine, may still be pulling in a hefty $11.2 billion in FY23, but it's a far cry from its FY22 peak. Sales have plummeted 70%, and those booster shots aren't exactly flying off the shelves anymore.

As for Paxlovid, the once-promising COVID-19 treatment, this drug has suffered an even more dramatic fall from grace, with revenue crashing 92% to $1.3 billion in FY23. To add insult to injury, Uncle Sam returned a staggering 6.5 million treatment courses.

Meanwhile, Ibrance, their breast cancer treatment, is also feeling the heat, with sales down 6% to $4.8 billion in FY23. It's facing tough competition overseas and its patent is set to expire in 2027, adding further pressure on its future performance.

To make matters worse, several other Pfizer blockbusters – Inlyta, Xeljanz, and Xtandi – are also staring down the barrel of patent expiration in the next few years.

This looming patent cliff poses a significant challenge for Pfizer, as these drugs have been major contributors to their revenue stream.

The company will need to rely on its pipeline of new drugs and strategic acquisitions to offset the potential losses and maintain its position as a leading player in the pharmaceutical industry.

Does that mean, then, that the $43 billion Seagen acquisition in December 2023 could become a lifeline for Pfizer?

Facing a double whammy of declining blockbuster sales and the looming patent cliff, Pfizer isn't sitting idly by. Seagen brings a fresh arsenal of patent-protected cancer-fighting drugs to the table, including three promising antibody-drug conjugates (ADCs).

Two of these, Adcetris for Hodgkin lymphoma and Padcev for urothelial cancer are already showing blockbuster potential, having raked in $751 million and $479 million, respectively, in the first nine months of 2023, despite the acquisition's timing.

But Pfizer's ambition doesn't stop there.

With five new therapies and six label expansions slated for oncology alone by 2026, they're banking on biologics like ADCs to fuel their growth.

They predict these cutting-edge treatments will surge from 6% to 60% of their cancer revenues by 2030, potentially yielding eight new blockbusters.

For now, Seagen's arrival is a much-needed boost to their oncology sales, which dipped 4% to $11.6 billion in FY23, even with Seagen's $120 million contribution in the final weeks of the year.

While the Seagen acquisition helps Pfizer tackle its goals of dominating oncology and fueling pipeline innovation, it's not the whole picture.

Pfizer's got a few other tricks up its sleeve: maximizing new product performance, trimming costs, and playing the capital allocation game to keep shareholders happy.

They're even planning a $3 billion spending spree from late 2023 through 2024, aiming for a cool $4 billion in annual cost savings. Talk about tightening the belt while expanding the empire.

Speaking of empires, Pfizer's 4Q23 results were a bit of a wake-up call.

Earnings per share (EPS) tanked to $0.10 (non-GAAP) on revenue of $14.2 billion, a far cry from the $1.14 EPS and $24.3 billion revenue of the previous year.

For the full year, EPS dropped a whopping 72% to $1.84 (non-GAAP), with revenue down 42% to $58.5 billion.

But, if you ignore those pesky Covid-19 products (Comirnaty and Paxlovid), the top line actually grew a bit – 8% in Q4 and 7% for the whole year.

Just remember, that Paxlovid revenue reversal in Q4 wasn't pretty, slashing both GAAP and non-GAAP EPS by $0.54.

Fast forward to Q1 2024, and Pfizer's numbers were a bit more cheerful, at least compared to what the analysts expected.

Non-GAAP EPS came in at 82 cents, a solid 30 cents above the consensus.

Revenue did fall 19.5% year-over-year to $14.9 billion, but even that beat estimates by $900 million.

Management's still sticking to their FY2024 guidance of $58.5 billion to $61.5 billion in revenue and $2.15 to $2.35 in non-GAAP EPS. We'll see if they can deliver.

That Seagen deal wasn't cheap, though, adding a hefty $31 billion to Pfizer's debt pile. As of March, they had about $12 billion in cash and marketable securities against over $61 billion in long-term debt. Yikes.

Still, management's determined to keep raising those quarterly dividends, now up to $0.42 a share in early 2024. That's a lot, considering it ate up 91% of their non-GAAP earnings in FY23 and is projected to gobble 78% in FY24.

With all that debt, don't expect any more stock buybacks in 2024. Pfizer's taking a break from that game, just like they did last year.

Despite Wall Street's lukewarm reception to Pfizer's patent cliff strategy, it's important to remember that this pharmaceutical giant is far from down for the count.

So, sure, Pfizer's 2023 revenue took a 42% nosedive compared to 2022, but let's not forget: over 620 million people worldwide still rely on their meds.

They actually scored nine FDA approvals, sold more pharmaceuticals than anyone else on the planet, and they're not sitting idly by while their product sales decline. Clearly, they're making moves.

The current bargain-basement price of Pfizer's stock, trading at a P/E of 10.4 on FY25E EPS, coupled with a juicy 5.9% yield, might just be the cherry on top for savvy investors willing to bet on the company's ability to navigate these turbulent times. Whether they can pull it off is anyone's guess, but at this price, it might be worth a gamble.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-05-30 12:00:302024-05-30 11:33:31Scaling The Cliff

Hang on to your Geiger counters because we're about to dive deep into the world of radiopharmaceutical therapy. I bet even Marie Curie would be impressed by the mind-blowing leaps we've made since her ground-shattering discoveries a century ago.

Now, don't get me wrong, she's a tough act to follow. But the big guns in pharma have taken up the challenge, piling up billions on the roulette table of targeted radiopharmaceutical therapy.

And from where I'm sitting, the odds are looking pretty darn exciting.

Just picture the scene: Radiation that directly takes the fight to those nasty tumor cells, like a microscopic missile strike that zaps cancer cells while ignoring the innocent bystanders.

How? By hitching a radioactive particle to a targeting molecule - think Uber, but for cancer therapy.

This healthcare game-changer, dubbed radiopharmaceutical therapy is projected to become a whopping $25 billion goldmine.

Forget the clunky radiation therapy your grandparents endured – this is precision, it's innovation, and it could potentially enrich your investment portfolio.

Actually, everyone seems to be piling into the radiopharma race. Experts say we're merely at the start line and these next-gen technologies could bring a windfall.

Evidence? The recent flurry of acquisitions, with no less than four deals being sealed just these past months.

Now, let's put some names to this game.

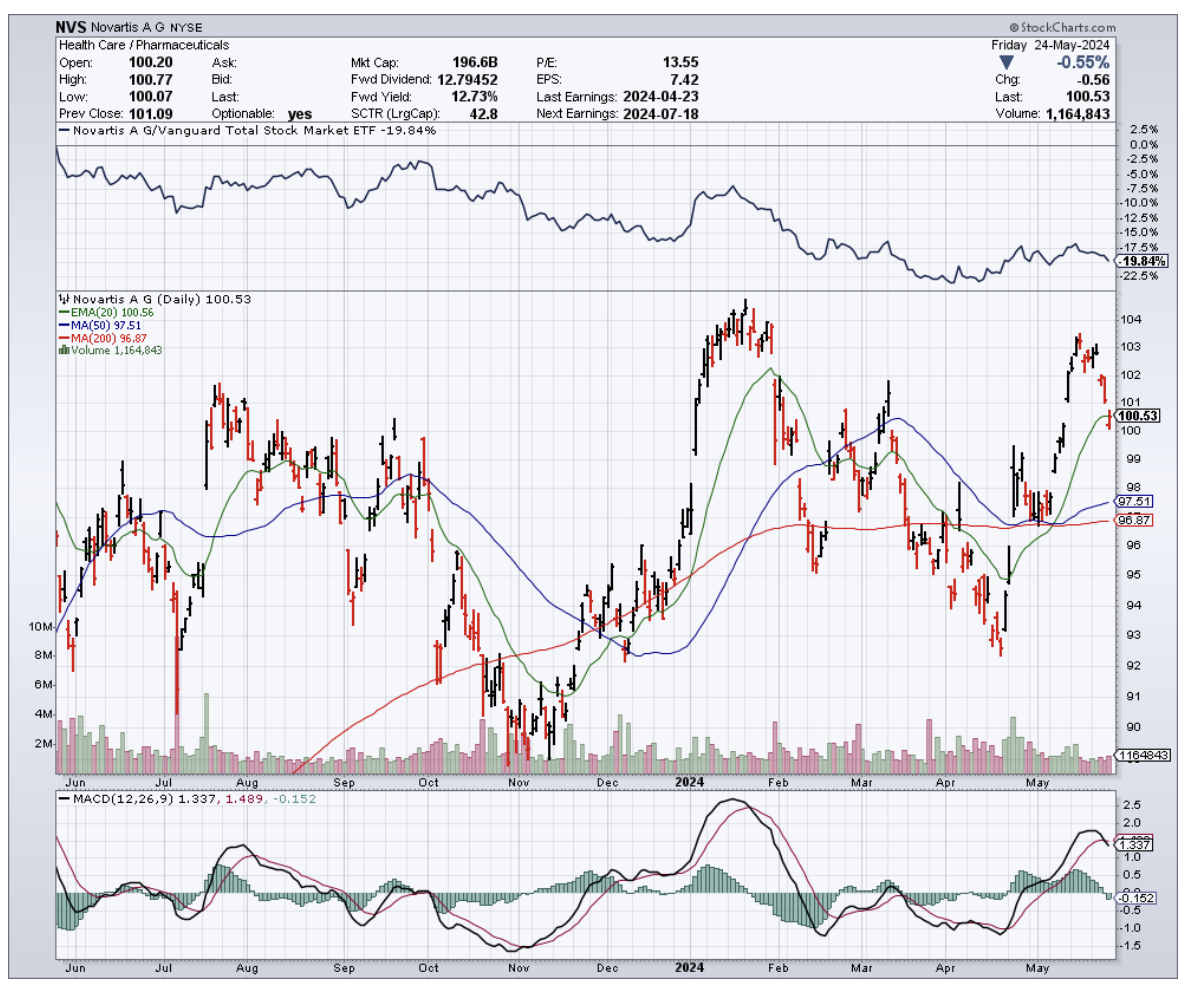

Novartis (NVS) is leading the pack with two radiopharmaceutical showstoppers under its belt. With their drugs Pluvicto and Lutathera, they're forecasted to rake in a whopping $5 billion by 2028 – that's more zeros than I can count on two hands.

Not just resting on their pile of success, they've scooped up Mariana Oncology in a $1 billion deal. This strategic move solidifies Novartis' dominion in the radiopharmaceutical arena – and you can quote me on that.

Inspired by Novartis' success, other pharmaceutical titans are catching the FOMO fever.

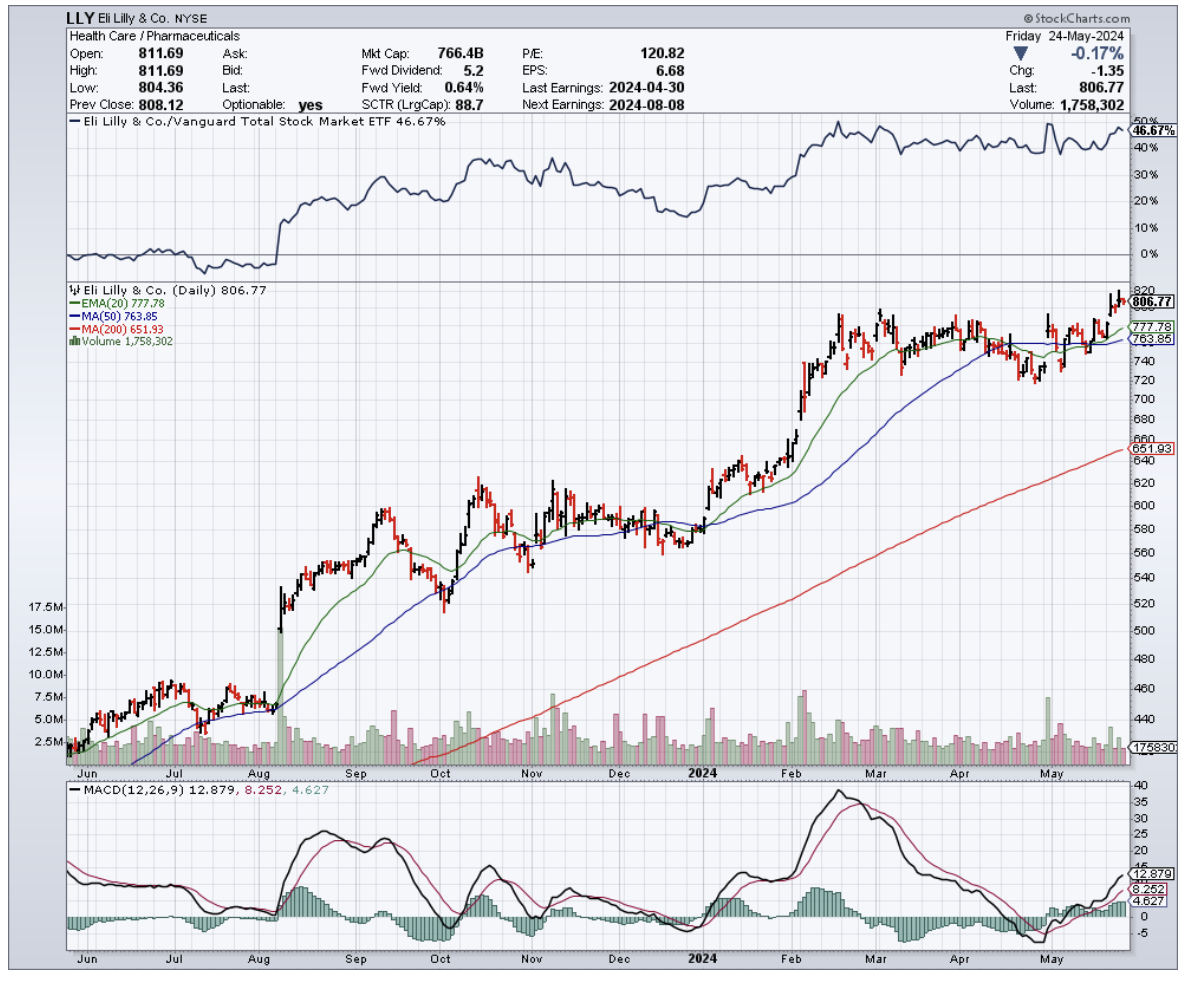

Eli Lilly (LLY), for instance, handed over $1.4 billion to acquire Point Biopharma and its promising radiation drug, PNT2002.

The investors’ darling this year with a near 38% surge in stock price (thanks to the overwhelming success of its obesity drugs), Eli Lilly is set to maintain its upward trajectory by venturing into the radiopharmaceutical space.

Bristol-Myers Squibb (BMY) isn't about to be left out of the radiopharmaceutical race either.

They ponied up a cool $4.1 billion for RayzeBio, snagging a promising pipeline of treatments. One standout is RYZ101, a late-stage targeted radiopharma therapy already making waves in trials for gastroenteropancreatic neuroendocrine tumors and small-cell lung cancer.

This acquisition followed closely on the heels of their $14 billion buyout of schizophrenia drug developer Karuna Therapeutics. Clearly, they’re feeling the heat as patents on some of their older cash cows are set to expire.

So, sure, BMY’s stock has been a bit sluggish lately, but this radiopharmaceutical gamble could be the shot in the arm they need.

And the acquisition spree doesn't stop there. AstraZeneca (AZN) also dove headfirst into the radiopharmaceutical pool, shelling out $2.4 billion for Fusion Pharmaceuticals in March.

Fusion's pipeline, including their Phase 2 candidate FPI-2265 for metastatic castration-resistant prostate cancer, adds another potential blockbuster to the mix.

Meanwhile, several biopharma companies are still standing tall, catching the eye of investors.

In fact, the venture capital poured into radiopharmaceutical drugs surged to $518 million last year, a cool 722% increase from 2017.

The race isn't slowing down anytime soon either. Researchers are exploring the use of radiopharmaceuticals alongside other treatments like immunotherapy, and even envision a future where this technology could be applied to any cancer, including ovarian, breast, or brain tumors.

And with only two products currently in the market, the potential for growth in targeted radiotherapies seems almost infinite.

So, I'll say it one more time – get your Geiger counters ready. The radiopharmaceutical revolution is just getting started, ladies and gentlemen. It’s time to zero in on this hotbed of innovation and watch your investments go nuclear.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-05-28 12:00:522024-05-28 11:59:05Get Your Geiger Counters Ready

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.