Mad Hedge Biotech and Healthcare Letter

May 23, 2024

Fiat Lux

Featured Trade:

(A DIVIDEND DERBY WINNER)

(ABT)

Mad Hedge Biotech and Healthcare Letter

May 23, 2024

Fiat Lux

Featured Trade:

(A DIVIDEND DERBY WINNER)

(ABT)

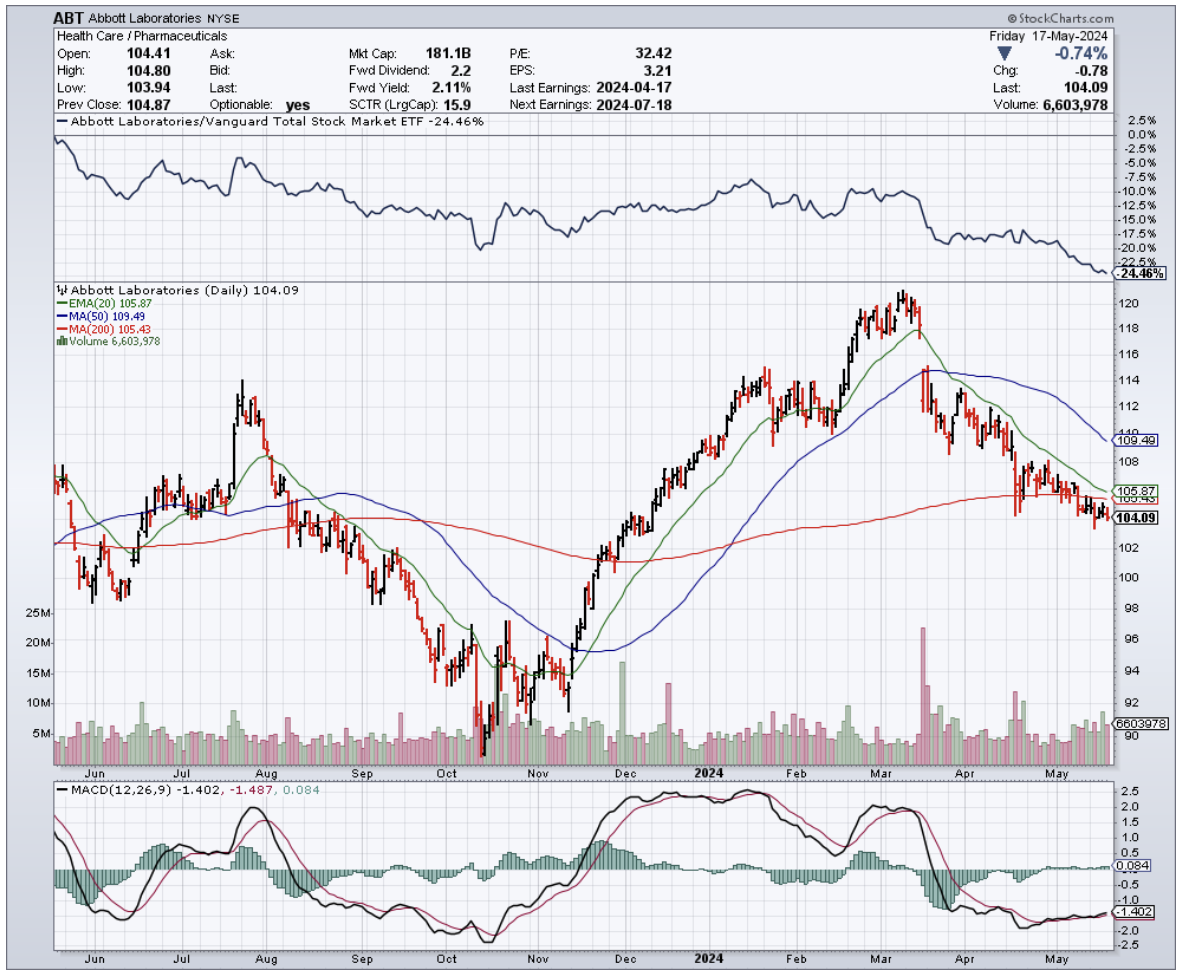

When you're at a racetrack, eyeing the horses before the big race, you're not just looking for a quick win. You want a stallion that'll keep delivering, race after race.

Well, that's exactly what we're hunting for in the stock market – companies that can keep those dividend payouts growing year after year. And if there's one thoroughbred you won't want to miss, it's Abbott Laboratories (ABT).

This biotech and healthcare giant isn't just keeping pace; it's setting the darned pace. Abbott is dominating the medical devices arena, a sector projected to skyrocket from $518.5 billion in 2023 to a whopping $886.8 billion by 2032. That's a steady 6.3% annual growth rate.

However, Abbott's not content with just one race – they've got their fingers in the lucrative pies of diagnostics and nutritional products, too.

But hold your horses, partner. Abbott isn't some one-trick pony. They've got their fingers in the lucrative pies of diagnostics and nutritional products too. Earlier this year, I gave this stock a thumbs-up, and it's only become more of a hot ticket since.

Fresh off their first-quarter reveal in April, Abbott's core business – think medical devices, diagnostics, and even baby formula – grew organically by an impressive 10.8% year-over-year.

This marks the fifth consecutive quarter of double-digit growth, so we're not just talking about a lucky streak here.

From what I can see, their Medical Devices segment is the real workhorse, surging 14.2% over the previous year. Their FreeStyle Libre device isn't just flying off the shelves, it's practically teleporting, with sales up 23% from last year. And with the FDA's recent green light for innovative products like TriClip and Amulet, Abbott isn't just playing in the major leagues, they're calling the shots.

Their Nutrition sector wasn't a slouch either, pulling in $2.1 billion in sales, a 5.1% increase over last year. Abbott's new Protality shake, launched in January, is specifically designed for those on weight loss journeys, adding another feather to their growth cap. Needless

Even their Diagnostics segment, which saw a dip due to the waning of COVID-19 testing, showed underlying strength in non-COVID testing. Their recent clearance for a concussion diagnostic test proves they're not slowing down on the innovation front.

When it comes to financials, Abbott is built like a brick house. With rock-solid interest coverage and debt servicing capacity, it's no wonder analysts are predicting a steady climb in their earnings. They've got a pipeline of new products and a market that's bouncing back from the pandemic, creating a recipe for success.

And don't even get me started on the dividends. Sure, Abbott's 2.1% yield might seem modest, but it's the growth story that's truly captivating.

Over the past decade, they've seen a staggering 11.4% annual growth in dividends. This ain't no stagnant stock, folks; it's a purebred built for speed.

Of course, no investment is without its bucking broncos. Abbott's still wrestling with the drop-off in pandemic-related revenues, and while their R&D spending is admirable, there's no guarantee those investments will always pay off. And let's not forget the ever-present threat of cyberattacks—a risk for any big player in today's world.

Still, while there might be a few hurdles in the race, Abbott Laboratories is a thoroughbred built for the long haul. With a rock-solid balance sheet, a track record of innovation, and a dividend that's been growing faster than a foal in springtime, this is a stock that's hard to beat.

And right now, the odds are in your favor. This company’s shares have been trading at a discount. So if you're ready to saddle up with a dividend growth thoroughbred, it's time to consider adding Abbott Laboratories to your stable. Because when it comes to the dividend derby, this is one horse you'll want to back.

Mad Hedge Biotech and Healthcare Letter

May 21, 2024

Fiat Lux

Featured Trade:

(THE FAT’S IN THE FIRE)

(RHHBY), (LLY), (NVO), (AMGN), (VKTX), (PFE), (MRK), (SNY), (ABT)

Well, well, well, look who's decided to crash the obesity-drug party. Roche (RHHBY), the Swiss pharmaceutical giant, has just unveiled some pretty impressive early-stage results for its weight-loss drug, CT-388. And let me tell you, this could be the start of something big.

Now, I know what you're thinking: "Another weight-loss drug? Yawn." But trust me, this is no ordinary contender.

In a small trial, patients who received CT-388 saw an average placebo-adjusted weight loss of 18.8% after just 24 weeks. That's right, 18.8%.

While it's hard to compare trials, experts are saying these numbers might even give Eli Lilly's (LLY) Zepbound, the current king of the market, a run for its money.

Let's take a step back and look at the bigger picture. The obesity drug market has been on fire lately, with everyone going gaga over these miracle pills.

Lilly and Novo Nordisk (NVO) have been dominating the scene with their drugs, Zepbound and Wegovy, but that hasn't stopped a whole host of other companies from trying to get a piece of the pie.

Merck (MRK), Sanofi (SNY), Abbott Labs (ABT), and Eisai have all tried their hand at weight-loss drugs and ultimately thrown in the towel.

More recently, Pfizer's (PFE) daily oral pill, danuglipron, has faced hurdles due to side effects. Amgen's (AMGN) drug, MariTide, is in Phase 2 studies and showing promise. And let's not forget Viking Therapeutics' (VKTX) VK2735, which has earned the nickname "twincretin" for its dual targeting of GLP-1 and GIP receptors.

So, what makes Roche's CT-388 so special?

Well, for starters, it's a GLP-1/GIP receptor agonist, which is similar to Lilly's Zepbound. In the Phase 1 trial, all participants achieved more than 5% weight loss, with 85% losing more than 10%, 70% shedding more than 15%, and a whopping 45% dropping more than 20% of their body weight. That's some serious weight loss.

Of course, there were some side effects, mainly mild to moderate gastrointestinal issues, but hey, that's the price you pay for looking fabulous, right? Roche is also testing CT-388 in patients with Type 2 diabetes, so stay tuned for updates on that front.

Now, I know you're all dying to know how CT-388 stacks up against the competition.

Notably, the drug's data looks strong compared to earlier studies of Zepbound. In fact, CT-388's efficacy results appeared "numerically higher" than Zepbound's.

But let's not get ahead of ourselves. Lilly still has a multi-year lead on Roche, so CT-388 isn't an immediate threat. However, it does suggest that the future of this rapidly growing market is up for grabs.

Now, let's talk about Roche. It’s the world's seventh-largest pharma company by market cap, sitting at around $205 billion. They pulled in $65 billion in revenue in 2023, second only to Johnson & Johnson (JNJ).

But here's the kicker—they've been struggling with growth, and their share price has taken a hit, down more than 25% over the past three years.

Contrast that with Eli Lilly and Novo Nordisk. Lilly's share price shot up 290% in three years, and Novo's climbed 226%.

Even though their revenues were less than half of Roche's in 2023, their market caps are sky-high. Why? Because of their blockbuster GLP-1 agonist drugs, Zepbound and Wegovy, which have shown jaw-dropping weight-loss results.

But could CT-388 be the underdog story Roche needs?

With the obesity market estimated to reach a staggering $100 billion by 2030, and over 1 billion people worldwide suffering from obesity, the potential is enormous.

Of course, there's still a long way to go for CT-388. Cross-trial comparisons can be tricky, and Roche's Phase 1 trial was much smaller than Lilly's pivotal study of Zepbound.

Plus, we don't have all the juicy details on patient characteristics, dose titration, and long-term weight loss just yet.

But here's the thing: Roche has scale and infrastructure on its side. It could potentially outmuscle smaller players like Viking and Boehringer Ingelheim.

And if CT-388 can match or even surpass the performance of current and future GLP-1 agonists? Well, let's just say those peak revenue forecasts might be in for a surprise.

So, is Roche the dark horse you should bet on in the obesity-drug race? If you're looking to get in on the action without paying the premium commanded by Lilly and Novo, or taking on the higher risk of smaller players, Roche might just be the ticket.

With promising mid-single-digit revenue growth on the horizon and a strong position in other areas like oncology and autoimmune disorders, Roche could be a smart play for anyone keen on the obesity drug market.

As for me? Well, you know I love an underdog story. And CT-388 might just be the Cinderella story of the year. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

February 6, 2024

Fiat Lux

Featured Trade:

(SETTING THE TABLE FOR STEADY GAINS)

(ABBV), (ABT), (PFE), (GILD), (DNA), (MRNA), (AMGN), (LLY)

Here's a nugget of wisdom from someone who's sailed the investment waters more times than I've had hot dinners: diversification is your best friend. Think of it as the Swiss Army knife in your investment toolkit.

Now, if there's one treasure you'd want aboard your investment ship, it's a dividend stock. Not just any old stock, though. I'm talking about AbbVie (ABBV).

Since it waved goodbye to its parent company, Abbott Laboratories (ABT), in 2013, it has boosted its dividend payouts by an eye-popping 290%. With a yield hanging around 4% and delivering a 130% total return over the past 5 years, long-term investors undoubtedly struck gold.

Unfortunately, 2023 has turned into the kind of year we'd rather forget. The end of Humira's patent was looming like a dark cloud, threatening to rain on AbbVie's parade by letting generics flood the market. The horror, right?

But, plot twist: the anticipated disaster was more of a light drizzle. Despite the competition, Humira still brought in a cool $11.1 billion. Sure, it's a dip, but not the plunge we feared.

Meanwhile, AbbVie's been on a shopping spree, snapping up Immunogen and Cerevel for a combined total that's a smidgen under $19 billion. It's like they're collecting Infinity Stones, diversifying beyond Humira into areas ripe with potential.

And let's not forget their foray into the realm of Antibody Drug Conjugates (ADCs) — the hot ticket in oncology.

While AbbVie’s not throwing around cash like confetti, like some of their peers including Pfizer (PFE), Gilead Sciences (GILD), Genentech (DNA), they're making notable moves. It's a bit like betting on the dark horse; if their ADCs and CNS ventures hit their stride, we're all in for a treat.

Amidst all this innovation and expansion, AbbVie hasn't lost sight of what gets investors' hearts racing — a solid dividend. It's the kind of steady reliability that's as comforting as your favorite cozy blanket.

As if those aren’t enough, the company just threw us a curveball that's got Wall Street buzzing more than my neighbor's annoying leaf blower on a peaceful Sunday morning.

In its recent earnings report, AbbVie not only beat the revenue expectations for its fiscal fourth quarter but decided to sweeten the deal by raising its long-term sales outlook.

Despite the concerns about Humira, AbbVie still posted fourth-quarter earnings that had their investors nodding in approval, even if they were a tad lower than previous years’ glory days. With revenue hitting $14.3 billion, surpassing the street's guess of $14 billion, it's clear the company isn't just hanging in there; it's throwing punches back.

The immunology portfolio, while taking a 12% hit, isn't down for the count, thanks to Skyrizi and Rinvoq. These two rising stars, which are quickly becoming the Batman and Robin of the biopharmaceutical world, are not just filling Humira's big shoes; they're sprinting.

With the duo’s sales surging by 52% and 63%, respectively, it's no wonder AbbVie is adjusting its binoculars and raising its long-term guidance for these drugs to a whopping more than $27 billion by 2027.

That's a $6 billion jump from their previous forecast. If that doesn't scream confidence, I don't know what does.

And just for a bit of perspective, while AbbVie was basking in the glow of success, its peers had a mixed day at the market. Pfizer took a slight tumble, Moderna (MRNA) and Amgen (AMGN) dipped their toes into the red, while Eli Lilly (LLY) floated up, riding a wave of optimism.

So, as we move forward this 2024, you might be wondering, "What's next for AbbVie?"

Well, if I were a betting man (and let's be honest, investing is betting with extra steps), I'd say we're not likely to see AbbVie pulling a rabbit out of a hat.

But, and it's a big but, we're talking about a company that's as expertly managed as a Michelin-starred kitchen. They've got a knack for serving up share price growth and dividends that leave investors coming back for seconds.

So while AbbVie might not be dangling the next blockbuster breakthrough in front of us, their steady march forward is as promising as finding a shortcut on your morning commute. We might not see the stock skyrocket overnight, but a climb to around $180 per share? That's not just possible; it's on the menu. And right now, with its recent earnings report, it's as good a time as any to pull up a chair to the AbbVie table. Bon appétit.

Mad Hedge Biotech and Healthcare Letter

November 28, 2023

Fiat Lux

Featured Trade:

(A MILLIONAIRE MAKER IN THE MAKING)

(ABBV), (ABT)

In the high-stakes game of investment, where the dream is to turn a modest sum into a cool million, savvy players are constantly on the hunt for that one stock with the Midas touch.

Enter the scene: AbbVie (ABBV), a heavyweight in the healthcare arena, boasts a revenue growth of over $20 billion since 2019.

Let's cut through the noise and see if AbbVie is the golden goose for your portfolio, capable of outpacing the market and padding your account with those sought-after seven figures.

Since its spinoff from Abbott Labs (ABT) in 2013, AbbVie has been flexing its muscles in the dividend world.

I’m not talking about just keeping up with the Joneses here; AbbVie's dividend payout has skyrocketed by an impressive 270% through late 2023. This isn't just inheritance; it's multiplication.

Now, let's address the elephant in the room: Humira, AbbVie’s blockbuster drug, which is set to lose its patent shield in 2023.

This anti-inflammatory drug has been a cash cow for AbbVie, spanning a wide range of treatments from rheumatoid arthritis to Crohn's disease. But the party can't last forever. As the patent protection fades, so does a chunk of AbbVie’s revenue stream.

However, don't think AbbVie's been caught off guard. They've been prepping for this moment with Rinvoq and Skyrizi, two new immunology drugs poised to pick up the slack and maybe, just maybe, outshine their predecessor by 2027.

Dig into the latest quarter, and you'll find Rinvoq and Skyrizi raking in the cash with double-digit sales growth, eyeing to breach the $11 billion mark in annual revenue.

AbbVie's strategy? Cover all bases Humira did, and then some.

But that's not all in AbbVie's arsenal. With over 50 programs chugging along in development, the odds are in favor of a few big wins that could give the biopharma top and bottom lines a healthy boost.

Besides the promising Rinvoq and Skyrizi, AbbVie has other aces up its sleeve. Take bipolar disorder treatment Vraylar, with its potential to hit $4 billion in peak annual revenue, or acute migraine drug Ubrelvy, eyeing at least $1 billion.

While transition phases are tricky, especially since AbbVie's shift from Humira to the likes of Skyrizi and Rinvoq is no walk in the park, it's the other elements in play that add to AbbVie's potential.

For instance, here's another factor that makes the company attractive for growth investors: AbbVie's stock is currently undervalued, trading at a mere 12 times its estimated future earnings, a bargain compared to the sector's average. This could be your ticket to get on board for the long haul, eyeing those hefty returns down the road.

Now, what about the financials? After all, a company's muscle is measured by its monetary might. Well, AbbVie's operating profit of $15.8 billion on $55.1 billion in revenue in the past 12 months is nothing to sneeze at.

Now, let's talk free cash flow (FCF) – aka the real indicator of financial fitness. AbbVie's sitting pretty with $24.7 billion in FCF over four quarters. That's not pocket change; it's a war chest, part of which is already earmarked for a generous 4.5% dividend yield.

So, is AbbVie the magic bean that grows into a million-dollar beanstalk? Let’s give it more context.

To morph a $30,000 investment into $1 million, AbbVie's market cap would need to balloon over 30 times its current size, a Herculean feat that translates to a market valuation of over $7.3 trillion.

It's a long shot but not beyond the realms of possibility, especially considering the long-run average return of the S&P 500.

Overall, AbbVie is more than just a contender in the investment arena. With its solid track record, robust pipeline, and undervalued stock, it's a heavyweight with a puncher's chance of turning your investment into a million-dollar dream. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

September 21, 2023

Fiat Lux

Featured Trade:

(HEALTH MEETS WEALTH)

(BSX), (ABT), (JNJ), (MDT), (SYK)

In a state-of-the-art medical facility, a surgeon's hands move with precision, guiding a catheter towards the basivertebral nerve. Their mission is clear: to halt the persistent pain signals traveling to the brain, offering relief to those burdened by vertebrogenic pain. This is the real-world application of the Intracept system, a breakthrough in healthcare.

Boston Scientific Corporation (BSX) has recently made headlines by announcing its definitive agreement to acquire Relievant Medsystems, Inc., the very creators of the Intracept Intraosseous Nerve Ablation System. This power move, sealed with a cool $850 million upfront cash payment, also includes some exciting performance-based bonuses over the next three years.

Let's zoom in on the Intracept system for a moment. It's the only kid on the block with a nod from the U.S. Food and Drug Administration, specifically tailored for vertebrogenic pain. This sleek, implant-free outpatient procedure employs radiofrequency energy, acting like a mute button for the pain-causing basivertebral nerve.

And with over 5.3 million Americans wrestling with vertebrogenic pain, the ripple effect of this innovation is monumental. So, mark your calendars: the acquisition is set to be finalized in the first half of 2024 once all the formalities are squared away.

On the financial front, the future's looking bright for Relievant. They're gearing up to clock sales north of $70 million in 2023, with a growth spurt expected to zoom past 50% in 2024. And while the 2024 earnings per share (EPS) might not cause a big splash, 2025 and beyond are looking sunny.

While the acquisition is a major step, Boston Scientific's journey doesn't stop there.

Their Watchman device, which dominates its market segment, is poised to bring transformative changes to atrial fibrillation treatments. Just think of this gadget as a guardian angel for patients with non-valvular atrial fibrillation, shielding them from stroke risks without the ball-and-chain of long-term blood thinners.

Apart from this, Boston Scientific dropped some exciting news earlier this year about their ADVENT Study of the FARAPULSE Pulsed Field Ablation System (PFA). This nifty gadget uses electric fields to treat atrial fibrillation (AF), sidestepping the need to heat up the tissue. The study was a trailblazer, being the first to pit the FARAPULSE system against traditional AF treatments.

However, Boston Scientific's game plan goes beyond just gadgets and gizmos.

Their keen interest in Shockwave (SWAV) and a track record of smart acquisitions hint at a company that's always two steps ahead. This forward-thinking mindset has earned them nods of approval from both the medical community and sharp-eyed investors. The success of its ADVENT study, for instance, has further underscored its growing prominence in the sector.

In today's roller-coaster financial world, with storm clouds of economic downturns gathering, investors are on the hunt for solid ground. This is where Boston Scientific comes through. They're not just a safe harbor; they're also a vessel of growth.

With two solid quarters in the bag and a projected 11% revenue growth on the horizon, they're on a skyward journey. And while there might be some chatter about its share valuation, their blend of innovation and strategy makes every penny worth it.

In a nutshell, Boston Scientific is more than a company name; it's a promise of a brighter, healthier tomorrow. Moreover, the stock has consistently outpaced the broader medical device sector, gaining an edge of about 10% over notable competitors like Abbott (ABT), Johnson & Johnson (JNJ), Medtronic (MDT), and Stryker (SYK). This performance was evident even before the company unveiled the impressive results of its ADVENT study on the Farapulse ablation.

Currently, I remain optimistic about the potential of BSX shares. Granted, a forward revenue multiple of 6.5x isn't exactly modest, and the valuation might appear ambitious when assessed through traditional metrics like discounted free cash flow. However, top-tier growth med-tech stocks rarely come with a discount tag.

Given the prospects of Farapulse, Watchman label extension studies, innovative CRM products, the Agent drug-coated balloon, and growth avenues in peripheral intervention, endoscopy, and urology, Boston Scientific stands out as a unique growth narrative. Historically, investors have shown a willingness to pay premium multiples for such consistent growth in this market segment.