Mad Hedge Biotech and Healthcare Letter

May 20, 2025

Fiat Lux

Featured Trade:

(HEALTHCARE’S FALLING KNIFE)

(UNH), (CI), (CVS), (LLY), (VRTX), (SGRY), (AAPL), (AMZN)

Mad Hedge Biotech and Healthcare Letter

May 20, 2025

Fiat Lux

Featured Trade:

(HEALTHCARE’S FALLING KNIFE)

(UNH), (CI), (CVS), (LLY), (VRTX), (SGRY), (AAPL), (AMZN)

Mad Hedge Biotech and Healthcare Letter

April 8, 2025

Fiat Lux

Featured Trade:

(YOUR ALL-WEATHER HEALTHCARE FORTRESS)

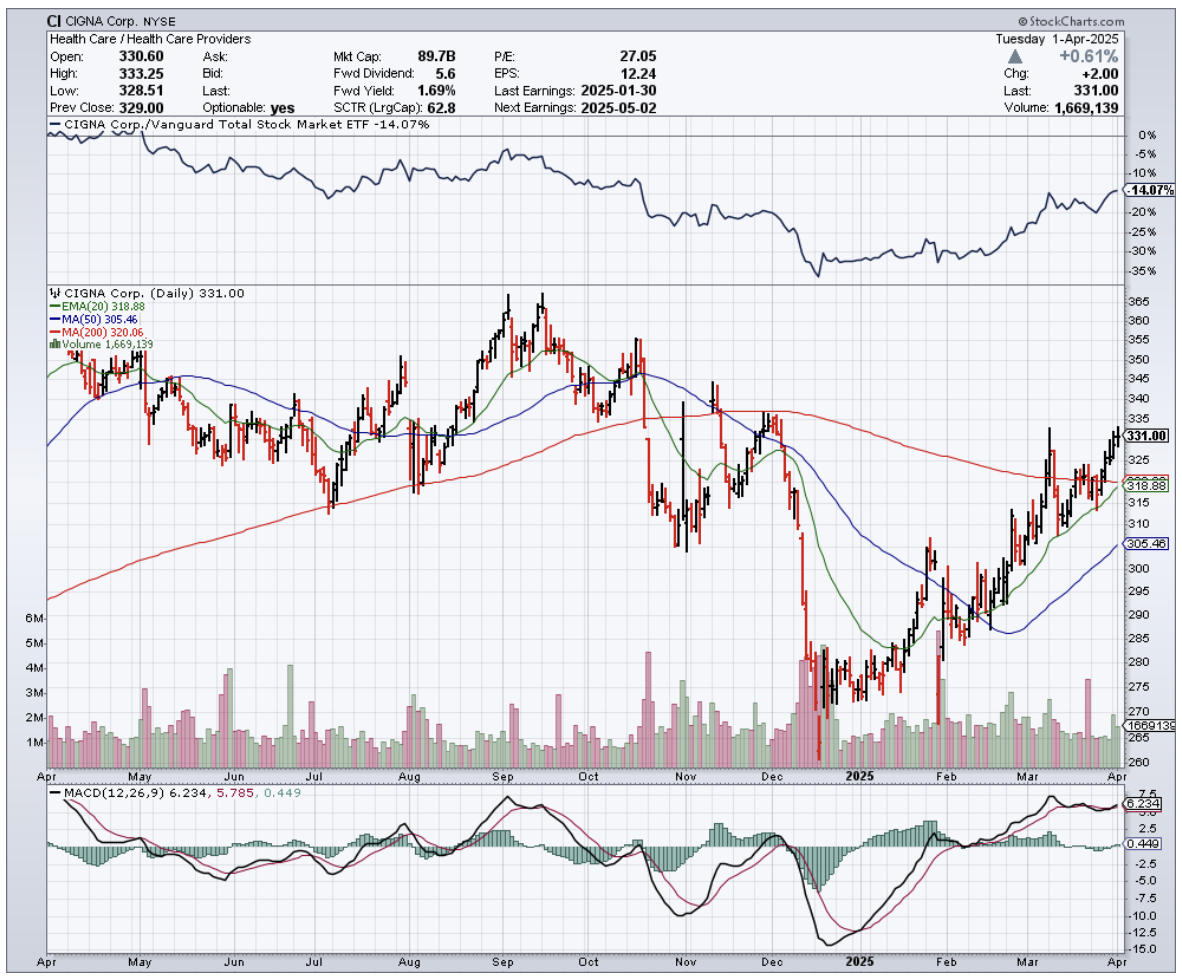

(CI)

I've stared down bears in Yellowstone, MiGs over Moscow, and market crashes that would make your financial advisor need therapy. But nothing gets my pulse racing like finding a massively mispriced asset hiding in plain sight.

Ladies and gentlemen, I give you Cigna (CI) – the financial equivalent of discovering an abandoned Ferrari with the keys still in the ignition.

Two nights ago, at a private dinner with three healthcare CEOs, I heard something that confirmed what my models have been screaming for months: Cigna isn't just surviving healthcare's perfect storm – it's secretly thriving in it.

At $331 per share, we're looking at a rare beast: a value play with growth-stock upside.

I've spent enough time hanging around hospital C-suites to know when something smells like money.

Healthcare has been absolutely battered these past couple of years – staffing shortages, skyrocketing utilization rates, and the mother of all pandemic hangovers. Yet here's Cigna, delivering 8-9% year-over-year earnings growth.

What really gets my investment juices flowing is watching Cigna’s strategy play out beautifully. In fact, they just closed their Medicare business sale to HCSC in Q1, a move so smart it makes me want to applaud slowly from across the room.

I was having dinner with Medicare Advantage executives last month, and these folks were practically in tears over reimbursement rates. "It's like trying to run a restaurant where customers expect filet mignon but only want to pay for ground beef," one said, nursing his third scotch.

By reducing Medicare exposure, Cigna is saying, "We'd rather control our destiny than beg government bureaucrats for pennies." Companies that pivot away from heavily regulated, margin-compressed businesses typically emerge looking like they've been on a financial fitness program.

Here's the cherry on top – practically all proceeds from the Medicare divestiture are funding stock buybacks.

Cigna already has a track record of reducing share count that would make other CEOs jealous. One of my former students who now runs healthcare equity research at a bulge bracket bank messaged me privately that his team is dramatically underestimating the EPS impact – like forecasting a drizzle when there's a monsoon coming.

As both an insurer and pharmacy benefits manager, Cigna occupies rarefied air. Their ability to steer members toward lower-cost biosimilars isn't just smart business – it's practically printing money.

During my last Mad Hedge Fund Trader conference, I arranged a private tour of Cigna's specialty pharmacy operations for some of our Concierge members, and what I saw confirmed my thesis: their integration of medical and pharmacy data gives them insights that would make McKinsey consultants salivate.

And can we talk about prior authorization? If you've dealt with health insurance, you know it's bureaucratic torture that makes the DMV seem like a day spa. Remarkably, Cigna is reducing these requirements.

A Cigna EVP I've known since our Harvard Business School days told me over golf that their internal data shows customer retention improving by double digits from these changes alone.

Let's get down to the numbers. Like I said earlier, even during healthcare's darkest days, Cigna delivered 8-9% EPS growth. Using that as my bear case and applying a conservative 3% terminal growth rate, we're looking at a fair value of $432.79 per share.

But if they execute on their 10-14% EPS growth strategy, the fair value jumps to $508.40. That's 33-53% upside from current levels – the kind of return profile that usually comes with significantly more risk.

In 40 years of trading everything from Japanese derivatives during the Nikkei bubble to Texas fracking plays, I've learned that when everyone panics about an industry, the smart money quietly pounces on the gems.

Cigna isn't just any healthcare company – it's the one with enough foresight to shed Medicare exposure right before what my Washington contacts warn will be a reimbursement bloodbath.

Mark my words: By this time next year, when I'm recounting this trade over sake in Tokyo, Cigna won't be our little secret anymore – and neither will the 33%+ returns sitting on the table right now.

Well, that's enough financial wisdom for one day. My trading screens are flashing, my yacht captain's texting, and somewhere in the Himalayas, a summit is wondering where I've been.

Mad Hedge Biotech and Healthcare Letter

December 10, 2024

Fiat Lux

Featured Trade:

(THE INSURANCE COMPANY ALWAYS RINGS TWICE)

(UNH), (CI), (CVS), (HUM), (AMGN), (BIIB), (GILD)

Got an interesting call yesterday from an old college buddy - let's call him Bob. We go way back to our UCLA days, before I headed to Tokyo and he went into tech.

He was fuming because UnitedHealth (UNH) just denied his family's third claim this year, something about an "experimental treatment" for his daughter's rare condition.

Coming from a guy who just cashed out of his third startup, hearing him rant about insurance bureaucracy was pretty rich.

Still, his situation got me thinking. After hanging up, I dug into what's really happening with insurance stocks, and the picture isn't pretty.

UnitedHealth Group, our nation's biggest health insurer, just had its worst week in years - dropping 9.5% after one of their executives was tragically murdered, which sparked an unexpected spotlight on their claims practices.

Cigna (CI) and CVS Health (CVS) caught the same downdraft, falling 4.5% and 5% respectively.

But here's what really caught my attention: UnitedHealthcare's denial rate for Medicare Advantage claims has more than doubled since 2020, hitting 22.7% last year.

Interestingly, this spike happened right as they rolled out new automation processes. Funny how that works, isn't it?

Experian Health's latest report shows this isn't isolated - 73% of healthcare providers are reporting more denials than ever, with processing times stretching longer and longer.

The cost of this trend? The Council for Affordable Quality Healthcare estimates $31 billion annually in administrative expenses alone.

Meanwhile, biotech companies find themselves in an awkward position. They're developing treatments that cost more than a house in the Hamptons and then need these very same insurers to make them accessible.

Amgen's (AMGN) been crushing it with their human therapeutics portfolio, pulling in $28.2 billion in revenue last year.

Biogen's (BIIB) making serious moves in neurological treatments, though their path has been rockier - just ask anyone who followed the Aduhelm saga.

Gilead Sciences (GILD), our antiviral champions, have managed to stay above the fray, partly because their HIV and hepatitis treatments have become standard of care.

But even these giants must wonder:: as insurers tighten their prior authorization screws, what happens to patient access?

These biotechs spend billions developing breakthrough treatments - Amgen alone dropped $4.4 billion on R&D last year - only to face the insurance industry's equivalent of "computer says no."

The irony isn't lost on anyone: insurers need innovative treatments to justify their premiums, while biotech needs insurance coverage to justify their R&D spending.

It's a delicate dance that's worked reasonably well so far, but these rising denial rates have everyone on edge. Just last quarter, we saw several biotech earnings calls dominated by questions about insurance coverage rather than clinical trials.

So what should we do? Well, I say UnitedHealth and Cigna are "holds" right now - the current turbulence needs time to settle.

CVS Health is showing broader operational challenges that suggest it might be wise to consider selling. But Humana (HUM), with their strong Medicare Advantage presence, looks promising.

On the biotech side, Gilead looks like an excellent stock to buy on the dip. Its leadership in antivirals and solid pipeline make it compelling.

Amgen and Biogen? Keep them on your watch list while they try to find their footing in this situation.

Bob texted me again this morning - turns out he's filing an appeal with help from one of Silicon Valley's top healthcare attorneys. Typical Bob, bringing a cannon to a knife fight.

But maybe that's exactly what this sector needs right now - some heavy artillery to shake up the status quo.

For those willing to dodge the crossfire, there might just be some spoils of war worth picking up. After all, fortune favors the bold—and sometimes, the heavily armed.

Mad Hedge Biotech and Healthcare Letter

January 25, 2024

Fiat Lux

Featured Trade:

(FROM BIG TO BIGGER)

(UNH), (CI), (ELV), (CVS)

Today, let's talk about where the smart money's at in our whirlwind economy – healthcare and insurance.

And who's the king of the hill in this game? None other than UnitedHealth Group (UNH).

It's not just any old company; it's a health insurance juggernaut that's been on a growth tear, doubling its value in just five years. That's definitely something to write home about.

With a market cap closing in at $500 billion and revenues of $372 billion in 2023, it's a force to be reckoned with. If it doubles again, we're looking at a $1 trillion giant. That's uncharted territory for healthcare stocks.

Before anything else, let's hop in our time machine for a sec.

Around 10 years back, UnitedHealth was a mere $75 billion baby. Fast forward to today, and it's ballooned to around half a trillion. We're talking about top-dog status in the healthcare world.

Now, let's get down to brass tacks. UnitedHealth's bottom line might not be the stuff of legends – a 6% profit margin over the past year.

But hold your horses – with over $300 billion in annual revenue, that 6% turns into a cool $18 billion-plus in profit.

And guess what? They've been raking in even more lately – $21.7 billion over four quarters.

"But will it double in value in a year or two?" you ask. Maybe not that fast, but hey, it's done it in five years before.

So, could UnitedHealth hit that mind-boggling $1 trillion mark by 2030? I wouldn't bet against it.

After all, UnitedHealth isn't just playing in the health insurance sandbox. It's the biggest kid in the playground – the largest health insurer in the United States and the biggest healthcare company globally.

For context, its closest peers are Cigna (CI) with $90.44 billion in market cap, Elevance (ELV) with $111.87 billion, and CVS (CVS) with $95.08 billion. You get the picture.

But here's the juicy part – UnitedHealth loves to shop. It's like the Pac-Man of healthcare, gobbling up companies left and right.

Just last year, it bagged Amedisys for a cool $3.3 billion, hot on the heels of its $5.4 billion acquisition of LHC Group. Talk about making moves.

Now, for my fellow investors, here's the sweetener: UnitedHealth also pays dividends, with a 1.4% yield. It might not sound like much, but this company's got a knack for growing dividends. It's like owning a golden goose that keeps laying more golden eggs.

So, what's the secret sauce for UnitedHealth potentially hitting that $1 trillion valuation? Simple – growth, growth, and more growth. It's not just selling insurance; it's into analytics and isn't shy about snapping up companies to beef up its portfolio.

Let's talk numbers. Management is eyeing an annual earnings growth somewhere between 13% and 16%. If UnitedHealth keeps hitting these home runs, its stock value climbing higher isn't just a possibility – it's a likelihood.

"But is it a good buy?" I hear you ask. Well, trading at around 23 times its earnings, it's a bargain compared to the average healthcare stock at 28 times earnings.

Simply put, this baby's got room to grow, and investors might just be willing to pay a premium for this gem.

So, when will it hit $1 trillion? If UnitedHealth sticks to the S&P 500 index's average 10% annual growth, we're looking at 2030 for that milestone.

But knowing UnitedHealth, which often outperforms the market, it could be sooner if it keeps up its projected annual growth rate.

In a nutshell, UnitedHealth Group isn't just a safe bet – it's a potential goldmine. With its continued growth, strategic acquisitions, and reasonable price tag, it's a shining star in any investment portfolio.

Mark my words – this is one stock that could make its investors very, very happy by 2030.

Mad Hedge Biotech and Healthcare Letter

December 5, 2023

Fiat Lux

Featured Trade:

(A UNION IN THE MAKING?)

(HUM), (CI), (CVS), (AET), (UNH)

The healthcare market was recently abuzz with the news of a potential mega-merger that sent shares of Humana (HUM) and The Cigna Group (CI) into a nosedive - 5.5% and 8.1% respectively. This news, centered around a transaction combining stocks and cash, could significantly reshape the healthcare landscape.

But let's not get ahead of ourselves. After all, in the world of healthcare mergers, certainty is as elusive as a mirage.

Still, if you’re feeling a sense of déjà vu, it’s because this isn’t the first time Humana and Cigna have danced around the idea of a merger.

Recall 2015 when Humana flirted with the idea of a merger with Cigna but ended up cozying up to Aetna (AET) – a union that never saw the light of day, thanks to the US courts.

A similar fate befell an attempted merger in 2017, when Elevance Health (ELV), then known as Anthem, tried to acquire Cigna for $48 billion, only to be blocked by the courts.

Since these previous attempts, both Humana and Cigna have significantly grown.

Prior to this market shake-up, Humana boasted a market capitalization of $62.87 billion, with Cigna commanding a higher ground at $83.77 billion.

But as history shows, regulatory skepticism often casts a long shadow over such ambitious plans, with fears of increased costs for the American public. This skepticism has extended to smaller deals, such as UnitedHealth Group's (UNH), which faced hurdles in their acquisition attempts.

Yet, the potential merger between these healthcare giants teases the possibility of substantial cost savings.

When giants unite, the promise of cost savings looms large. Redundancies in corporate functions like HR, investor relations, and executive positions offer low-hanging fruits for cost-cutting.

But the real cherry on top is the potential for operational synergies – cross-selling opportunities and leveraging infrastructure for efficient service delivery.

Humana's stronghold lies in its Insurance unit and CenterWell, with the latter, including pharmacy, provider services, and home solutions, contributing 16.3% of last year's revenue.

In contrast, Cigna wades into deeper waters, with its substantial revenue streams from pharmacy benefits and home delivery pharmacy businesses.

Now, let’s look at the companies in terms of revenue. A side-by-side of Humana and Cigna's revenues offers an intriguing picture.

Humana's Medicare Advantage revenues soared from $59.47 billion in 2020 to $72.89 billion in 2022.

Cigna, however, has only inched forward in this space. Humana's evident dominance in Medicare Advantage, with a market share of about 18%, contrasts sharply with Cigna's modest 2%.

Despite these differences, a merger isn't outside the realm of possibility.

For example, CVS (CVS) managed to successfully acquire Aetna for $69 billion back in 2018, with the two companies eventually turning into CVS Health.

While that merger proved that big deals could happen, the odds for Humana-Cigna are not exactly in Vegas betting territory.

Speculations about Cigna offloading its Medicare Advantage operations could make this merger more palatable to regulators, but it's far from a sure bet.

Another question to think about amidst these talks is why the market reacted like someone yelled “fire” in a crowded theater.

Well, it all boils down to the fear of overpayment.

Cigna, being larger, could potentially swallow Humana. But Humana, with its stronger financial health and market positioning, is seen as the more desirable entity.

The valuation metrics – price to earnings, price to adjusted operating cash flow, and EV to EBITDA – further complicate this perception, as Humana commands a premium.

With a potential merger announcement might be on the horizon, investors should approach this with a blend of skepticism and intrigue. The market is jittery, perceiving a possible merger as potentially detrimental to shareholder value.

However, should the merger succeed against the odds, the combined prowess of Humana and Cigna could spell a profitable future for investors. Knowing that the healthcare sector is never short of surprises, this potential merger, should it come to pass, could be one for the history books.

Mad Hedge Biotech and Healthcare Letter

October 19, 2023

Fiat Lux

Featured Trade:

(THE UNSUNG HERO OF PHARMA DISTRIBUTION)

(MCK), (CI), (UNH), (PFE), (MRK), (LLY), (NVO), (CAH), (COR)