Mad Hedge Biotech and Healthcare Letter

May 8, 2025

Fiat Lux

Featured Trade:

(A DOUBLE HELIX OF OPPORTUNITY)

(CRSP), (NTLA)

Mad Hedge Biotech and Healthcare Letter

May 8, 2025

Fiat Lux

Featured Trade:

(A DOUBLE HELIX OF OPPORTUNITY)

(CRSP), (NTLA)

I never fully appreciated the potential of gene therapy until last fall when my college friend Eric called with surprising news. His 14-year-old daughter Sophie, who'd struggled with sickle cell disease her whole life, had undergone treatment with Casgevy, a CRISPR-based gene therapy developed by CRISPR Therapeutics (CRSP) and Vertex (VRTX). Six months later, she hasn't needed a single blood transfusion or hospitalization—a transformative outcome for a girl accustomed to spending more weeks in hospital rooms than classrooms.

"The doctors keep using phrases like 'functionally cured,'" Eric told me. "I just know she's planning her first summer camp experience. That's miracle enough for me."

Eric's story prompted me to dive deeper into gene-editing therapies and the companies working on them. What struck me the most is that despite groundbreaking science, market volatility has created a disconnect between technological progress and stock valuations.

Gene therapy stocks like CRISPR Therapeutics and Intellia Therapeutics (NTLA) had a rocky first quarter of 2025, with shares dropping 2.82% and 24.19%, respectively. The broader market mirrored this instability, with the S&P 500 down nearly 3%. Yet, beneath these headline fluctuations lies an intriguing opportunity for patient long-term investors.

CRISPR is particularly interesting. It's sitting pretty with $1.9 billion in cash and equivalents as of the end of 2024. That's enough runway to keep the scientists doing what they do best for years without financial pressure.

More importantly, they're expecting their flagship product Casgevy to be accretive from late 2025, meaning actual revenue is on the horizon – not just the promise of future miracles.

Casgevy's approval for sickle cell disease and beta-thalassemia underscores CRISPR Therapeutics' tangible progress. With a cost of $2.2 million per patient, the price seems steep until compared against lifetime management costs of these conditions. Additionally, their pipeline extends beyond blood disorders into cardiovascular treatments like CTX-310 and CTX-320. These therapies aim to permanently eliminate the need for daily medications—a seismic shift in a market projected to grow from $156 billion in 2025 to nearly $215 billion by 2034.

CRISPR Therapeutics' strategic advantage is further enhanced by their U.S.-based manufacturing facility, strategically positioned to mitigate risks from reshoring trends and global supply chain disruptions.

On the other hand, Intellia faces a tighter financial outlook. With $861.73 million in cash and equivalents, they project operations funding through the first half of 2027. However, this timeline feels restrictive, especially since their first products aren't anticipated until at least 2027.

Although their financial runway is limited, Intellia's therapeutic breakthroughs still command attention. Their treatments NTLA-2002 for hereditary angioedema and Nex-z for transthyretin amyloidosis have shown extraordinary results. I remember a conversation with a trial participant who shared, "I went from planning my life around my disease to barely remembering I have it." Such transformative experiences underline the real-world potential of Intellia's science.

However, Intellia must dramatically reduce its annual cash burn from $592 million to around $345 million to ensure survival until commercialization. This aggressive belt-tightening could jeopardize their momentum.

Both companies currently trade at attractive valuations given their prospects. CRISPR Therapeutics holds a price-to-book ratio below the sector median, with cash comprising 57% of its market cap. Intellia's cash reserves represent an astounding 94% of its market cap, suggesting significant market undervaluation of its intellectual property and promising pipeline.

For investors able to tolerate short-term volatility, this disconnect offers a potentially lucrative entry point, particularly with CRISPR Therapeutics’ imminent commercial revenue.

As I told Eric, the market currently undervalues these revolutionary companies despite proven science. Eventually, stock prices will reflect this reality. I'm cautiously building positions during these dips, anticipating the long-term transformative impact of these therapies.

Just ask Sophie, who’s packing for summer camp instead of preparing for another hospital stay.

Mad Hedge Biotech and Healthcare Letter

February 4, 2025

Fiat Lux

Featured Trade:

(TOO RICH TO FAIL, TOO EXPENSIVE TO SUCCEED)

(MRNA), (TSLA), (NVS), (SNY), (JNJ), (BNTX), (RHHBY), (REPL), (CRSP), (ORCL)

Last weekend, while organizing my home office, I stumbled across an old COVID vaccination card. Remember those? It got me thinking about Moderna (MRNA), the biotech darling that went from relatively unknown to household name faster than you can say "messenger RNA."

Now, in early 2025, this once up-and-coming company is already facing what my grandmother would call "champagne problems" - too much cash to be broke, but burning through it faster than a Tesla (TSLA) on Ludicrous mode.

First, let's talk about this biotech's cash burn. In just nine months of 2024, Moderna torched through over $4 billion - that's the same amount they burned in all of 2023, suggesting their cash cremation rate is actually accelerating.

This acceleration in spending wouldn't be as worrying if they had endless reserves, but their current position shows $7 billion in cash and $2 billion in non-current investments.

The math isn't complex: at this burn rate, their runway is shorter than many investors realize.

The recent Health and Human Services (HHS) grant of $176 million in July 2024 for bird flu research barely registers on their financial statements.

While we've seen about 70 bird flu cases in the U.S. with one fatality in an elderly patient with underlying conditions, this isn't going to be another COVID-style revenue stream.

I've analyzed enough pharmaceutical companies to know that betting on another pandemic windfall is like expecting lightning to strike twice in the same spot.

What really interests me is Moderna's position in the competitive landscape. I spent last week analyzing patent data and geographic reach metrics across the industry.

First, you've got the old-guard pharma giants like Novartis (NVS), Sanofi (SNY), and Johnson & Johnson (JNJ), who have been at this game since before mRNA was a gleam in a scientist's eye.

Then, there are companies like BioNTech (BNTX) and Roche (RHHBY) with significantly higher geographic reach, while Replimune Group (REPL) and CRISPR Therapeutics (CRSP) demonstrate superior application diversity.

In comparison, Moderna's position in this landscape shows relatively low scores on both metrics - not exactly what you want to see from a company burning cash at this rate.

Stéphane Bancel, Moderna's CEO, recently outlined their pipeline: 2 approved medicines, 7 Phase 3 trials, and 45 candidates in development. They're also targeting $1.1 billion in annual R&D cost reductions by 2027.

But here's what keeps bothering me: their SG&A expenses have ballooned to nearly 10 times their pre-COVID levels, yet management is focusing on R&D cuts instead of addressing this administrative bloat.

The insider trading patterns since early 2024 haven't exactly inspired confidence either.

When I see heavy selling from insiders while a company is promising future breakthroughs, I can't help but remember all the biotech stories I've covered where the promise didn't match the reality.

Speaking of promises, Oracle's (ORCL) Larry Ellison recently made headlines talking about 48-hour personalized cancer vaccines using AI and robots.

While the technology sounds promising, I'm more interested in the practical path to profitability. Moderna isn't alone in this race, and their well-capitalized competitors have the luxury of funding similar development programs while maintaining positive cash flow.

Given Moderna's cash burn trajectory, their next three quarters will be telling.

I'll be watching that $4 billion nine-month burn rate closely, along with their progress on cost reductions - particularly those inflated SG&A expenses that management seems reluctant to address.

I'm keeping my old vaccination card as a reminder of Moderna's impressive COVID-19 achievement, but I'm not ready to bet on lightning striking twice.

Sometimes the hardest part of investing is knowing when to appreciate history without banking on its repeat performance.

Mad Hedge Biotech and Healthcare Letter

December 24, 2024

Fiat Lux

Featured Trade:

(THE LAB RESULTS ARE IN)

(GILD), (TSLA), (WVE), (EDIT), (CRSP), (LLY), (NVO), (WMT), (CVS), (CCCC), (RHHBY)

I found myself gridlocked in Bay Area traffic a few days ago, inching past Gilead's (GILD) sprawling Foster City headquarters, when my phone lit up with a call from an old friend at Goldman.

“Alright, tell me—what’s the real story with biotech this year?” she asked, her tone hovering somewhere between curiosity and exasperation. “Half my portfolio feels like a masterstroke, the other half... well, let’s just say it’s testing my patience.”

As I watched a Tesla (TSLA) weave through traffic like it was auditioning for a Fast & Furious reboot, I smiled.

Biotech has always been a bit of a high-stakes chess game—brilliance in one corner, chaos in another, and always a few surprises lurking behind the next move.

“Let me break it down for you,” I said, steering the conversation as carefully as I did my car through the bumper-to-bumper maze.

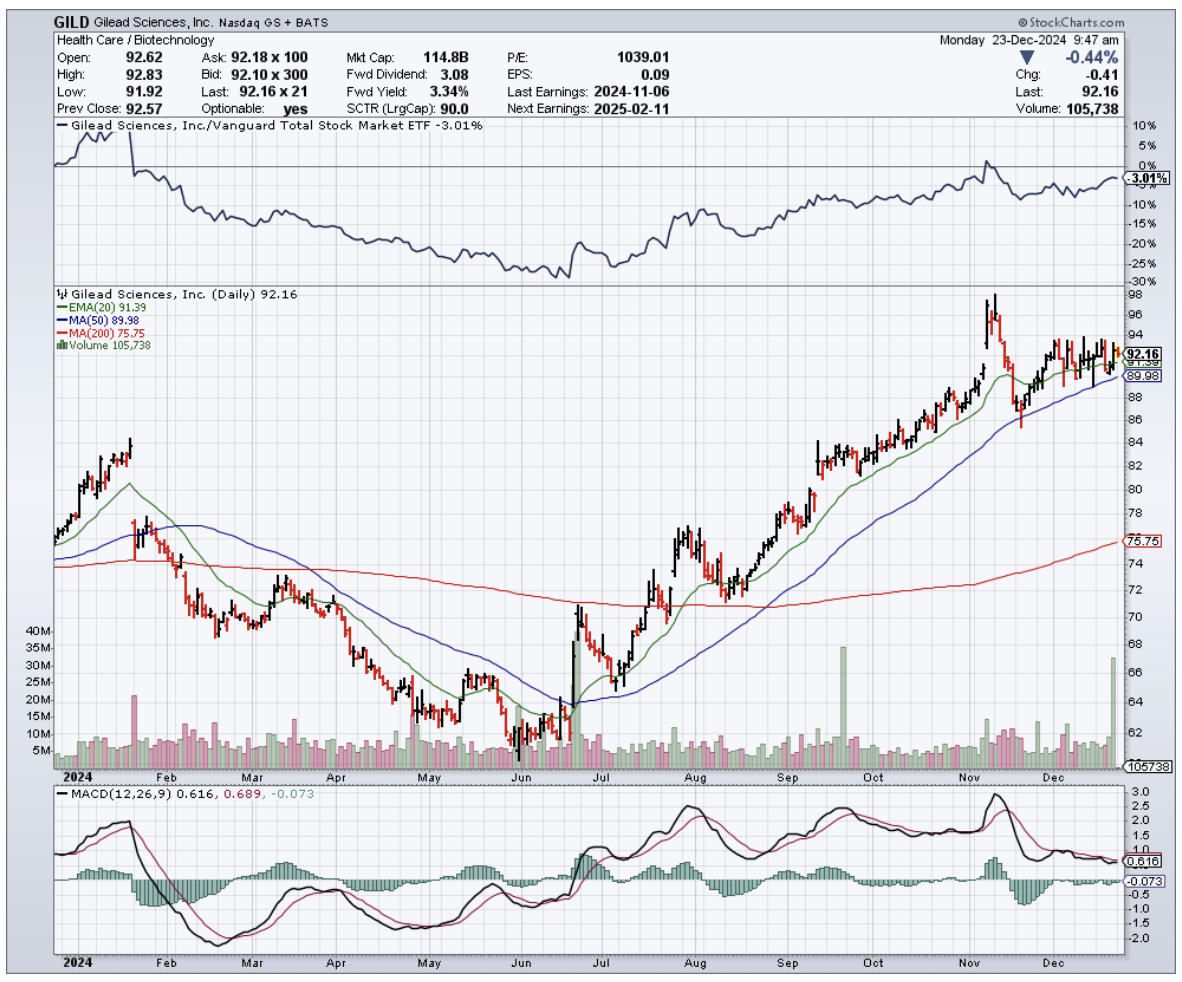

First, the winners are crushing it, and I mean crushing it. Gilead (GILD) finally cracked the code on HIV treatment, developing what's essentially a vaccine that doesn't require popping pills like they're Tic Tacs.

My contacts in clinical development tell me the Phase 3 data in cisgender women is nothing short of spectacular. With a $6 billion annual market potential by 2028, this isn't just another incremental advance - it's the kind of breakthrough that makes everyone in biotech salivate.

Then there's Wave Life Sciences (WVE) and their RNA editing technology. Remember when we thought CRISPR was the only game in town? Well, Wave just showed us there's more than one way to edit a gene.

Their liver-targeting therapy is the first successful RNA editing in humans - think of it as spell-check for your DNA, but reversible. The market's currently at $1.1 billion, but with 35% CAGR through 2030, this train is just leaving the station.

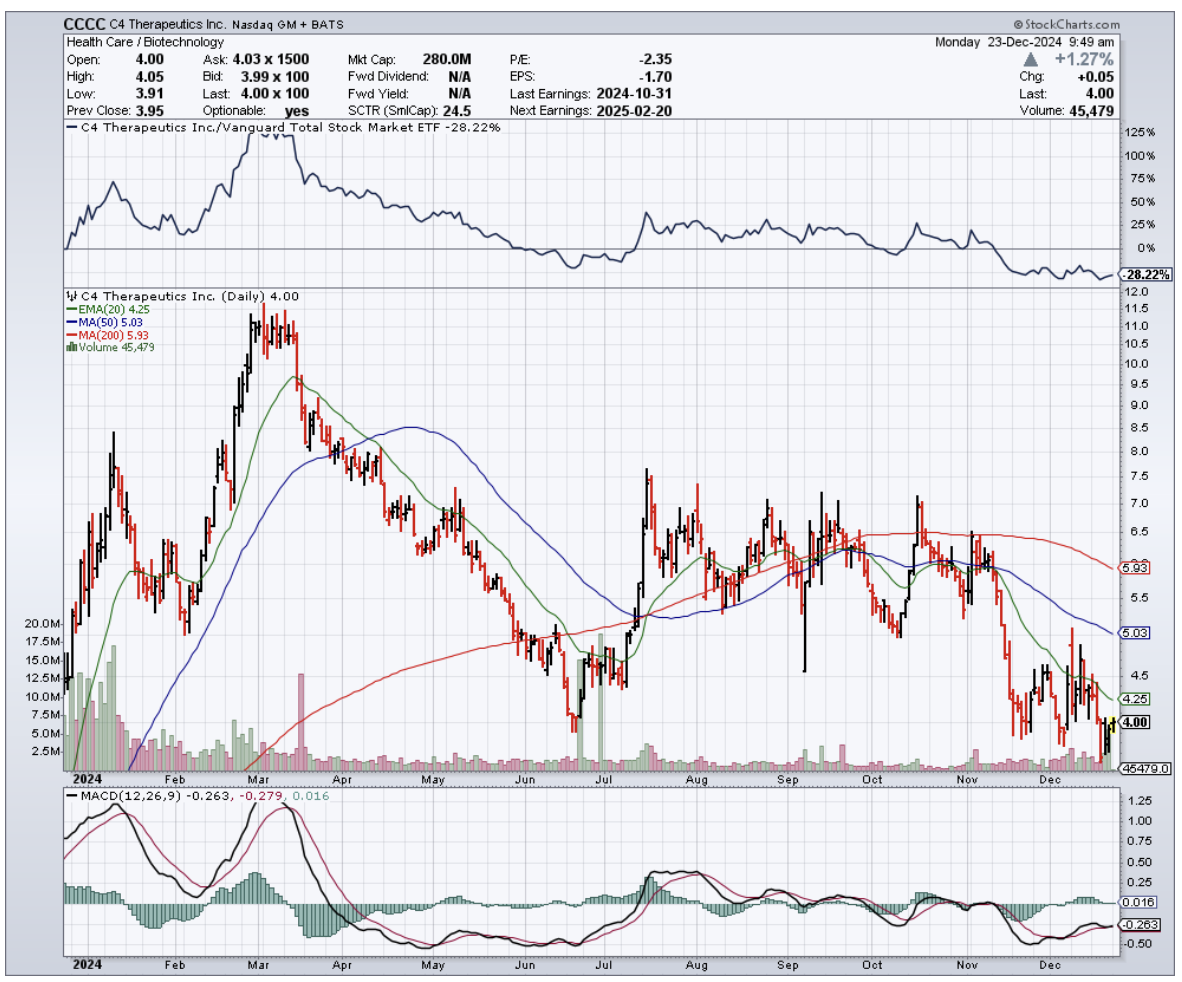

Speaking of trains leaving stations, molecular glue developers like C4 Therapeutics (CCCC) are watching Big Pharma back up the Brink's truck.

We're talking $8 billion in licensing deals this year alone. After all, when Roche (RHHBY) drops $300 million upfront - not milestone payments, mind you, but cold hard cash - you know they've seen something special in the data room.

But here's where it gets interesting, and I had to pull over at this point in the conversation because my friend wasn't going to like what came next.

CRISPR stocks? Down 20%. Editas (EDIT) and CRISPR Therapeutics (CRSP) are learning that revolutionary science doesn't always translate to revolutionary returns.

My friend Janet at the Fed might be talking about higher rates, but these companies are bleeding cash faster than a Silicon Valley startup's WeWork budget.

The obesity market? Unless your name is Eli Lilly (LLY) or Novo Nordisk (NVO), you're probably not having a great time.

Only three startups cleared $100 million in funding this year. In biotech terms, that's like trying to build a house with pocket change.

The global market's sitting at $4.1 billion, but it's more crowded than a San Francisco coffee shop during a tech conference.

And don't get me started on Walmart (WMT) and CVS (CVS) trying to play doctor. They thought they could disrupt traditional healthcare with their “get your physical next to the garden tools” model.

The result? A combined loss of $250 million and a wave of clinic closures.

The lesson here is clear: just because you can sell lightbulbs and Band-Aids in the same aisle doesn’t mean you should try to diagnose strep throat next to the automotive department.

A kid in a modded Subaru WRX cut me off as I wrapped up the call, but I left my friend with this: In biotech, timing is everything.

Gilead and Wave are showing us that patience pays off when the science is solid. Meanwhile, CRISPR stocks remind us that even the most promising technology needs good timing and deep pockets.

So, watch those clinical trial results like a hawk, and keep an eye on where the venture money's flowing.

But most importantly, remember what my old mentor used to say: "In biotech, you're not just betting on the science - you're betting on the scientist, the CFO, and sometimes, just sometimes, on whether people are ready to get their flu shot next to the garden center."

Now, where's that highway patrol when you need them?

Mad Hedge Biotech and Healthcare Letter

August 27, 2024

Fiat Lux

Featured Trade:

(NOT ALL THAT GLITTERS IS LILLY)

(JNJ), (LLY), (CRSP), (ISRG)

I've been so busy chasing after Eli Lilly (LLY) and its trillion-dollar dreams that I nearly overlooked a gem in the making.

While everyone's obsessing over LLY's march towards that coveted $1 trillion market cap, there's another pharma giant that's been quietly chugging along, building value like it has for over a century.

I'm talking about Johnson & Johnson (JNJ). You know, that little company that's only been around for 138 years.

I understand that JNJ isn’t as exciting as the likes of Crispr Therapeutics (CRSP) with their fancy gene editing therapies, or Intuitive Surgical (ISRG) with their robotic surgeons, but, let me tell you, sometimes boring is beautiful – especially when it comes with a 3% dividend yield and a rock-solid business model.

Let's break it down, shall we?

First off, JNJ isn't sitting on its laurels. Just last week, they dropped $1.7 billion to snatch up a private heart-device company. That's not chump change, even for a behemoth like JNJ.

And speaking of big moves, the FDA just gave them the green light for a chemotherapy-free lung cancer treatment.

We're talking about Rybrevant plus Lazcluze, which showed a 30% reduction in the risk of disease progression or death compared to AstraZeneca's (AZN) offering.

That's not just incremental progress – that's potentially life-changing stuff for patients.

But they’re not stopping there. They're also shelling out $600 million upfront (with potential milestone payments up to $1.1 billion) for V-Wave, a company making shunts for heart failure patients.

This deal's expected to close before the year's out, beefing up JNJ's already impressive MedTech division.

Now, let's talk numbers. JNJ's current market cap is sitting pretty at just under $400 billion. Sure, it's not in Lilly's $850 billion stratosphere, but remember – slow and steady wins the race.

And speaking of winning races, JNJ was the global leader in pharmaceutical sales last year, raking in $85 billion. That's a cool 30% higher than their closest competitor, Roche (RHHBY).

But here's where it gets interesting for value hunters. JNJ's currently trading at an enterprise value of 12.8 times forward EBITDA. In English? It's reasonably priced compared to its peers.

Even better, it's trading near the bottom of its five-year range for forward P/E ratio, EV-to-EBITDA, and price-to-free cash flow. Translation: This stock's on sale, folks.

Now, I know what some of you are thinking. "But what about those talcum powder lawsuits?" Fair question.

JNJ's looking at potentially settling around $6.5 billion worth of claims. That's not a small amount, even for these guys.

But here's the kicker – they've got over $25 billion in cash on hand and generated about $19 billion in free cash flow over the last 12 months. They can take the hit and keep on ticking.

Let's talk products. Stelara, Tremfya, Darzalex, Erleada – these aren't just random drug names. They're cash cows for JNJ. And with a diverse portfolio where no single drug accounts for more than 13% of total sales, they're not putting all their eggs in one basket.

Still, I'm not saying JNJ is going to double overnight. This isn't some flashy tech stock riding the AI hype wave.

But for those of us with a long-term horizon and a love for steady income, JNJ looks mighty attractive.

Think about it – they've raised their dividend for over six decades straight. That's longer than some of you reading this have been alive.

And with a 77% payout ratio, they've got room to keep that streak going.

Sure, over the past decade, JNJ's total return of 106% might not set your hair on fire. It lags behind the S&P 500's 234% and even the Health Care Select Sector SPDR Fund ETF's (XLV) 189%.

But remember, past performance doesn't always guarantee future results.

Here's my take: JNJ isn't for the get-rich-quick crowd. It's for investors who appreciate a good night's sleep knowing their money's in a company that's weathered world wars, depressions, and yes, even lawsuits.

Will JNJ hit that trillion-dollar mark? I'd bet my last bottle of Tylenol on it. It might take a decade, but hey, good things come to those who wait.

Mad Hedge Biotech and Healthcare Letter

August 13, 2024

Fiat Lux

Featured Trade:

(THE RISE OF THE STEADY EDDIES)

(CNC), (UNH), (PFE), (JNJ), (ABBV), (LLY), (BIO), (UHS), (WAT), (AMGN), (REGN), (VRTX), (CRSP), (MRNA)

Think of the market as a body fighting off an infection. Tech stocks might be the flashy antibodies, but healthcare is the steady, reliable immune system, keeping things stable when the going gets tough. And right now, that immune system is looking stronger than ever.

Skeptical? I get it. We've heard the hype about healthcare before. But this time, it's different.

The Healthcare Select Sector SPDR ETF (XLV) has been on a tear, up 9.3% this year as of Thursday's close. That's nearly keeping pace with the broader S&P 500's 12% gain - a remarkable feat in a market that's been anything but stable.

But what's even more impressive is the turnaround. Back in mid-July, XLV was lagging behind like a three-legged horse in the Kentucky Derby, up only 8.3% while the S&P 500 was showing off with an 18% gain.

In fact, out of the 63 healthcare stocks in the S&P 500, only a dozen have been slacking off since July. The rest? They've been outperforming like it's going out of style.

So what changed?

Well, it wasn't so much that healthcare stocks suddenly discovered the fountain of youth. No, my friends, it was more like the rest of the market decided to take a swan dive off the high board.

You see, while tech stocks were busy doing their best Icarus impression – flying too close to the sun and then plummeting back to earth – healthcare stocks were steady as she goes. It's like the old tortoise and hare story, except in this version, the hare got distracted by shiny objects and ran off a cliff.

Now, let's shine the spotlight on some of the key players driving this healthcare rally.

Remember those health insurers everyone was worried about back in spring? The ones that had investors biting their nails over the future of Medicare Advantage? Well, they've made a comeback.

The S&P 500 Managed Health Care index was down 12% in mid-April, looking about as healthy as a chain smoker with a Big Mac habit. But now? It's up 4.5% since the start of the year.

Companies like Centene (CNC) and UnitedHealth Group (UNH) have bounced back faster than a rubber band on steroids.

And it's not just the insurers. Big Pharma's been flexing, too.

Pfizer (PFE), the company that became a household name faster than you can say "vaccine," is holding steady. Johnson & Johnson (JNJ) is up 2.2%, probably thanks to all that baby powder they're not selling anymore.

Meanwhile, AbbVie’s (ABBV) up 11% since July. These guys are like the Energizer Bunny of the pharma world – they just keep going and going.

But the real showstopper? Eli Lilly (LLY). This biopharma has been on a tear since the beginning of 2024. Up 45% on the year at one point, they've been climbing faster than a squirrel up a tree with a dog in hot pursuit.

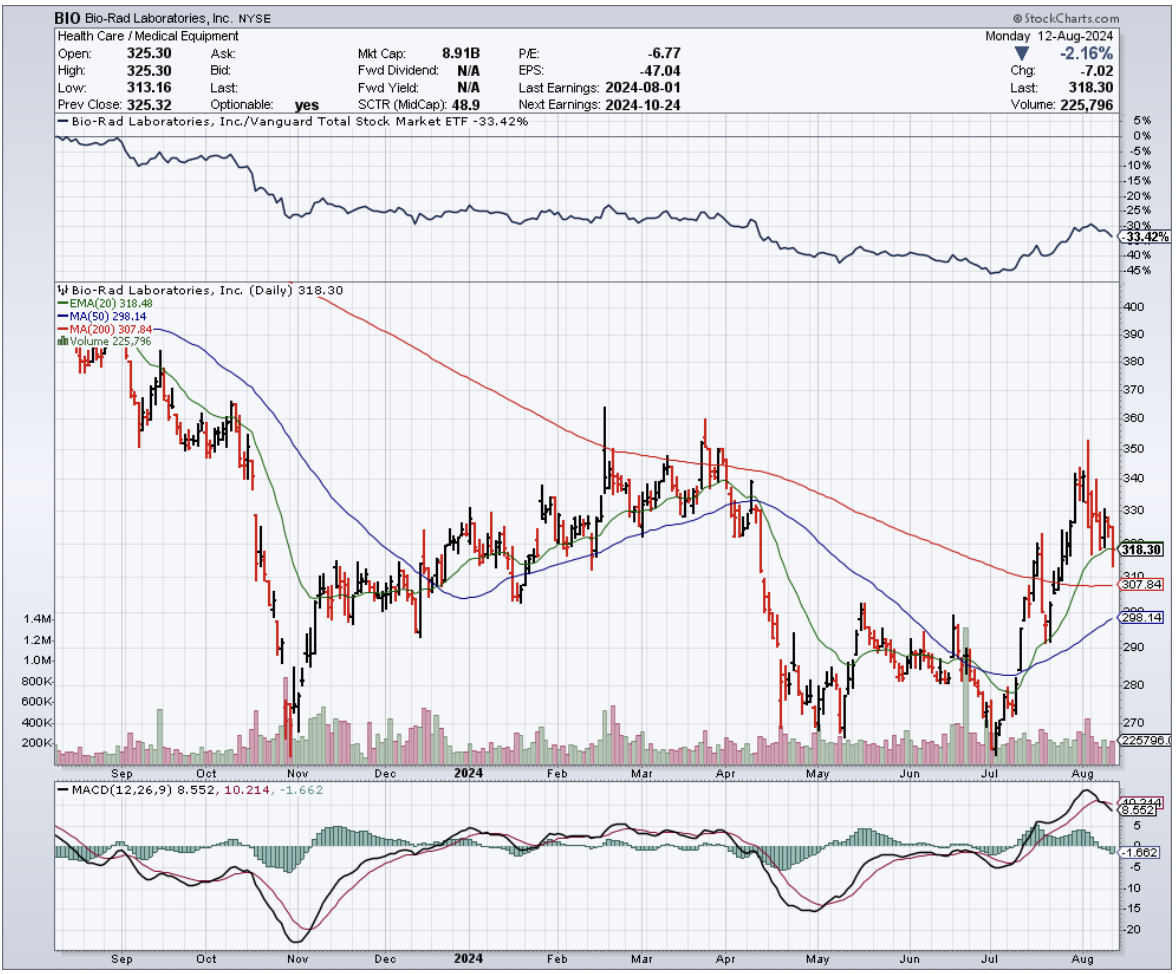

Then, there are companies like Bio-Rad Laboratories (BIO), up 20% since July. Universal Health Services (UHS)? Up 18% since July. Waters (WAT), the life sciences tools folks? Up 15%.

Even the biotechs are out to impress.

Amgen (AMGN), the granddaddy of biotech, is up 10% year-to-date. They're selling drugs like Prolia and Enbrel faster than hotcakes at a lumberjack convention.

And Amgen’s pipeline? It’s packed with potential blockbusters, setting the stage for further expansion in the future.

Gilead Sciences (GILD)? Up 15% year-to-date. Turns out, their COVID-19 treatment, Remdesivir, is back in vogue like bell-bottom jeans. And their HIV and hepatitis C drugs? They're still growing stronger.

But the real rock star of biotech? That'd be Regeneron Pharmaceuticals (REGN). These guys are up over 30% year-to-date. They're treating everything from eye diseases to cancer to inflammation.

Vertex Pharmaceuticals (VRTX) is another one to watch. Up 12% this year, they've got the cystic fibrosis market cornered. And they're not stopping there – they're expanding faster thanks to their collaboration with the likes of Crispr Therapeutics (CRSP).

Now that I’ve mentioned gene therapy, I know you're wondering about Moderna (MRNA). After all, weren’t they the darlings of the COVID era? Well, yes and no.

Their stock's down about 35% year-to-date, but don't count them out just yet. Their mRNA technology is hotter than a jalapeño popper fresh out of the fryer. They might be down, but they're definitely not out.

So, what's the takeaway here? I suggest you keep your eyes peeled on the biotechnology and healthcare sectors. After all, in this market, the best offense might just be a good defense – and what's more defensive than betting on the sector that keeps us all alive and kicking?