Mad Hedge Biotech and Healthcare Letter

April 3, 2025

Fiat Lux

Featured Trade:

(MIND THE GAP)

(DHR)

Mad Hedge Biotech and Healthcare Letter

April 3, 2025

Fiat Lux

Featured Trade:

(MIND THE GAP)

(DHR)

If I had a nickel for every time someone said pharmaceutical manufacturing was boring, I could’ve started bidding against Novo Holdings for Catalent (CTLT) myself.

Sure, I’d still be $16.5 billion short, but you get the point—this deal is huge, and it’s about to make some smart money look even smarter.

Here’s the deal: Novo Holdings is shelling out $16.5 billion to snap up Catalent, a contract development and manufacturing organization (CDMO).

If that acronym sounds like alphabet soup, let me translate: CDMOs are where the real action happens.

These are the guys behind the curtain making sure your miracle drugs and life-saving treatments aren’t just ideas—they’re products hitting the market at scale.

The numbers don’t lie. The CDMO market sits at $146 billion right now.

Fast-forward to next year, and that balloons to $243.3 billion. By 2029, it’s cruising toward a cool $332 billion.

And if you think that’s impressive, just wait: the broader pharmaceutical outsourcing trend is nowhere near slowing down.

In 2014, Big Pharma still clung to in-house production for 66.3% of its output.

Today? That figure’s down to 51%, and dropping fast. Why? Because outsourcing lets the specialists handle the hard stuff—faster, cheaper, and more efficiently.

For investors, Catalent’s immediate upside is a no-brainer. The acquisition premium is pure gravy, but that’s not the whole story.

Rivals like Lonza Group (SWX: LONN) and Samsung Biologics are already feeling the heat.

The biologics CDMO market alone is expected to expand by $10.63 billion between 2024 and 2028, and you better believe those two are scrambling to stay ahead.

If you own shares, keep your seatbelt fastened. If you don’t, well… you might want to rethink that.

And here’s where it gets really interesting: Novo Holdings may be private, but its publicly traded golden child, Novo Nordisk (NVO), is set to ride this wave like a pro surfer.

They’re already a global powerhouse in biologics, and Catalent’s souped-up manufacturing capabilities are going to help them scale production with military-grade efficiency.

Lower costs, tighter operations, bigger margins—it’s like handing a Formula 1 car to an already championship-winning team.

So if you’re not watching Novo Nordisk stock, you’re doing it wrong.

Of course, it’s not just the big CDMO players who stand to win here. Companies like Danaher (DHR), Repligen (RGEN), and Avantor (AVTR) are quietly cashing in on this gold rush.

These firms supply the picks, shovels, and critical bioprocessing tools that CDMOs need to keep production humming.

As Catalent scales under Novo Holdings, demand for these essentials will go through the roof.

Zooming out, the pharma manufacturing landscape is evolving at a breakneck pace.

The CDMO market is expected to hit $530.3 billion by 2033, growing at a steady 7.7% CAGR.

That’s not speculative growth—it’s a structural shift, backed by demand for biologics, gene therapies, and personalized medicine.

In short, we’re entering an era where outsourcing is king, and companies with the infrastructure to capitalize on it are poised to dominate.

Don’t forget about the big dogs in Big Pharma, either.

Pfizer (PFE), Eli Lilly (LLY), and Merck (MRK) aren’t just spectators in this game. They’re snapping up CDMO capacity, investing in biologics, and doubling down on therapies with blockbuster potential.

The Catalent deal is just the latest chess move in a game where the stakes keep getting higher.

So what does this mean for you? If you’re holding Catalent, congratulations—your portfolio is about to get a nice bump.

But the real play here isn’t Catalent alone. It’s understanding that CDMOs, suppliers, and adjacent players are the unsung heroes of this industry transformation.

You want exposure to the companies enabling the next wave of medical innovation? This is where you look.

Novo Holdings just threw down the gauntlet, and the smart money is already moving. The pharmaceutical manufacturing sector isn’t boring—it’s booming.

So, while everyone’s chasing flashy biotech startups and blockbuster drugs, the real smart money is quietly following the companies that make those breakthroughs possible.

Catalent isn’t just a $16.5 billion deal—it’s proof that outsourcing is the new backbone of pharma’s future. Call it “The Big Batch Theory:” scale up, outsource smart, and watch the returns multiply.

Ignore this shift, and you’re leaving money on the table.

Now, if you’ll excuse me, I need to check my CDMO positions. Just like a perfectly run batch, they’re growing fast—and that’s exactly how I like it."

Mad Hedge Biotech and Healthcare Letter

December 5, 2024

Fiat Lux

Featured Trade:

(GRANT EXPECTATIONS)

(TXG), (ILMN), (TMO), (DHR)

Mad Hedge Biotech and Healthcare Letter

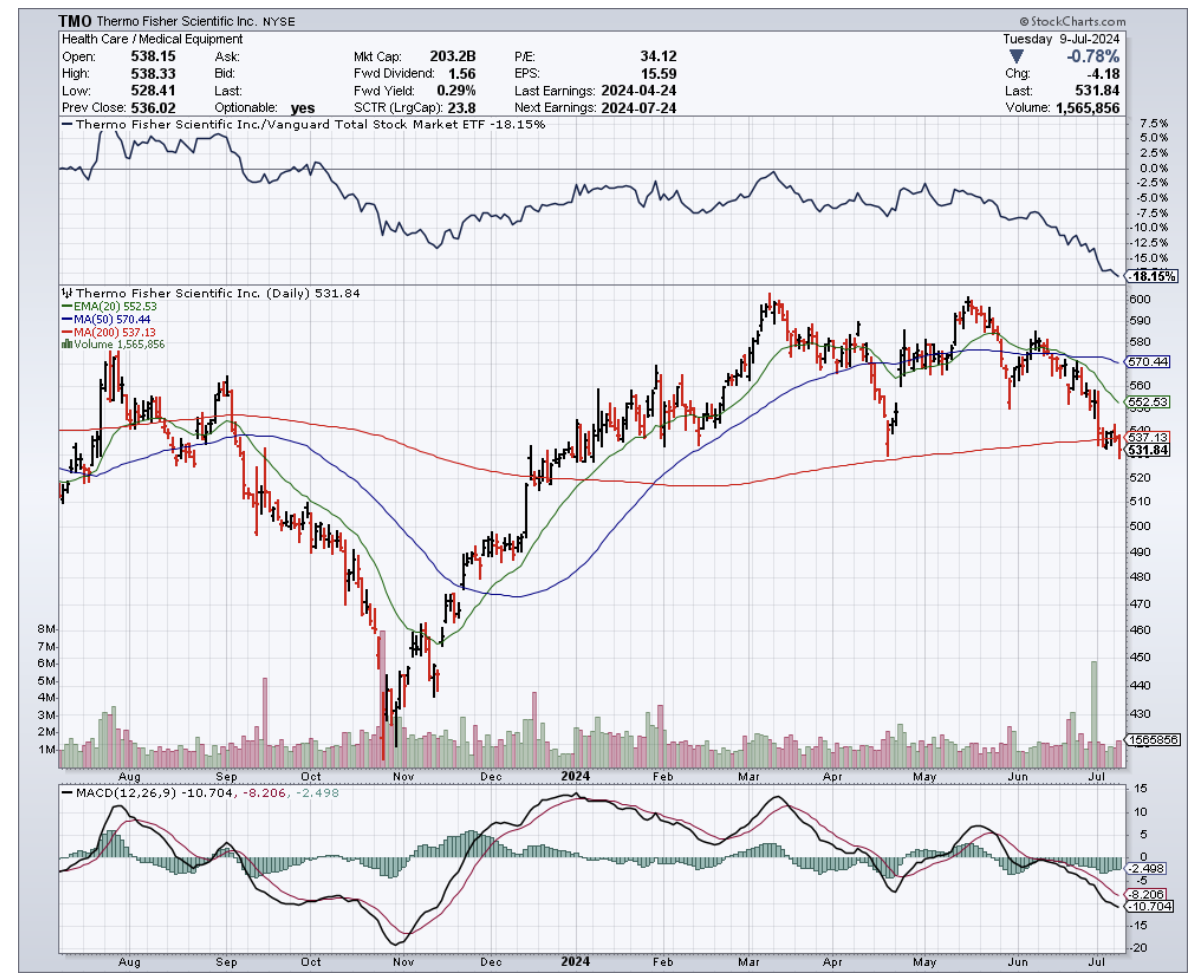

July 11, 2024

Fiat Lux

Featured Trade:

(FORGET THE CASINO, INVEST IN THE HOUSE)

(TMO), (BIO), (DHR), (A)

I've always had a soft spot for healthcare innovation. But let me tell you, picking winners in this sector is trickier than trying to nail jello to a wall. You've got regulatory hurdles, fierce competition, and funding risks that'd make a Vegas bookie sweat.

That's why I'm a big fan of buying the arms dealers in this war on disease. I'm talking about the suppliers. These companies are calmly sitting pretty, ready to cash in on the general need for innovation without getting their hands too dirty.

Enter Thermo Fisher Scientific (TMO), the Waltham, MA-based behemoth that's supplying everyone from big pharma to your local hospital. They're slinging lab equipment faster than a short-order cook at a greasy spoon, and business is booming.

Just look at the numbers. Over the past decade, TMO's delivered a 400% total return. That's not just beating the S&P 500 – it's leaving it in the dust by 170 points.

And recently, Thermo Fisher just got the green light from those sticklers at the UK antitrust office to close a $3.1 billion deal for Olink, a Swedish outfit that's cooking up some serious magic in protein analysis.

We're talking about technology that can analyze hundreds of proteins faster than you can say "proteomics."

Speaking of proteomics, for those of you who slept through biology class, it's the study of proteins in biological systems. These little buggers are the muscle behind everything your body does.

While DNA is the blueprint, proteins are the construction crew that brings that blueprint to life. Figuring out how these microscopic workers operate is the golden ticket to a treasure trove of new drugs and therapies.

It's a growing field, with the global market expected to explode from $32.8 billion in 2023 to a whopping $161.9 billion by 2035. That translates to a compound annual growth rate of 14.2%.

As expected, Thermo Fisher isn't the only player in this game. You've got heavyweights like Bio-Rad Laboratories (BIO), Danaher Corporation (DHR), and Agilent Technologies (A) all jockeying for the top position.

But thanks to this recent Olink acquisition, Thermo Fisher's looking to pull ahead like a thoroughbred at the Kentucky Derby.

For better context, let's break down what this means for TMO's bottom line. Their mass spectrometry business, already a cash cow, could see a 5% bump in market share.

We're talking about an extra $475 million in revenue by 2028, with profit margins that'd make a hedge fund manager blush.

And that's just the tip of the iceberg. Their protein assays and kits business could see a 10% boost in market share, translating to another $450 million in revenue.

Despite these, Thermo Fisher isn't resting on its laurels. They're also partnering up with the likes of Bayer (BAYRY) to develop next-generation sequencing tools.

Next, let's talk dividends. I know, I know, a 0.3% yield isn't going to have you popping champagne. That's barely enough for a value meal at McDonald's. But don't let that fool you.

This company's been growing its dividend faster than a beanstalk on Miracle-Gro, with a five-year CAGR of 15.5%. It's not TMO's fault their stock price keeps outrunning their dividend.

Looking ahead, Thermo Fisher is projected to reach a 12% EPS growth in 2025 and 11% in 2026. It's like watching a rocket take off in slow motion.

Before you jump aboard though, I'll be honest with you.

At a P/E ratio of 26.6x, TMO isn't exactly on the bargain rack. It's priced like a fine wine, not a box of Franzia. But hey, quality costs money, and this is a company that's been delivering returns of 16.7% per year since 2004.

So, what's the takeaway here? Well, it’s clear that Thermo Fisher Scientific is a powerhouse in the healthcare and biotech sectors.

But, it's not going to give you the cheap thrills of a biotech startup that might cure cancer or go belly-up next week.

Instead, it's the steady Eddie that's going to keep chugging along, supplying the tools that make those moonshots possible.

If you're looking for income, well, this ain't your horse. But if you want growth with a side of stability, Thermo Fisher might just be the ticket. It's got more potential than a kid with a 4.0 GPA and a mean fastball.

Mad Hedge Biotech and Healthcare Letter

March 14, 2023

Fiat Lux

Featured Trade:

(A MARKET LEADER SELLING AT A DISCOUNT)

(GE), (GEHC), (MTD), (DHR), (BSX), (TMO)

The spanking new multibillion-dollar healthcare spinoff from General Electric (GE) is gradually turning into a favorite in the industry.

The healthcare company, GE HealthCare (GEHC), was officially spun out of GE last January 4, but its shares began trading around mid-December. To date, GEHC is up about 30%. The stock has been trading for roughly 23 times its projected earnings in 2023.

While that value is already above the market multiple, GEHC is still anticipated to boost its earnings at an average of approximately 15% per year until 2026.

GEHC’s fourth-quarter earnings report was pretty solid. The company recorded $4.94 billion in revenue, rising by 8% year over year compared to the previous $4.59 billion. Most of the growth came from its imaging division, which climbed 11% from $2.44 billion to $2.71 billion thanks to the increasing demand.

For this year, GEHC is projected to generate over $19 billion in sales. This estimate is conservative since the company has yet to gain traction on Wall Street. Given its solid performance thus far, the company is expected to post a higher figure in the coming months.

Not much is known about GEHC yet. Aside from being an Illinois- based healthcare company focusing on medical technology, healthcare software and analytics, patient monitoring systems, and medical equipment maintenance and repair services, the spinoff only describes itself as “a leading global precision care innovator.”

That’s a relatively vague explanation that could cover much ground, but it appears to be focused on artificial intelligence (AI) in healthcare. After all, this is a lucrative and growing market that has sustained the ever-increasing demand.

Based on its records, GEHC generates the majority of its revenue from ultrasound and imaging services and products. These segments comprise about 75% of the company’s overall revenue. The rest are from various services, including clinical networking systems and financial solutions.

At the moment, more than 4 million of GEHC’s products are installed across the globe, lending support to over 2 billion patients since 2022.

Although this sounds less exciting than the other developments in the healthcare industry, the total addressable market for the medical imaging segment is impressively huge.

In 2021, this market was projected to reach $28 billion and will reach $47.4 billion by 2030. This represents a promising compounded annual growth rate of 4.9%. Critical to this growth and expansion is the climbing number of chronic diseases, which triggered earlier and more frequent checkups.

GEHC notably ensures that it sustains its momentum and gains a larger market share. The company has invested aggressively in research and development, allocating $2.7 billion to this effort alone from 2020 to 2022.

In February, the spinoff shelled out $3 billion to acquire Caption Health, a healthcare technology company developing AI software for medical imaging. The company's flagship product, Caption AI, is an FDA-approved medical imaging software that uses AI to guide healthcare professionals in acquiring and interpreting ultrasound images.

Basically, Caption AI is designed to help healthcare professionals who may need more specialized training in medical imaging, such as primary care physicians and nurses, to accurately and confidently perform and interpret ultrasound exams.

Apart from those, Caption Health's AI technology can assist in acquiring cardiac, lung, abdominal, and musculoskeletal images. It is intended to improve patient access to quality care by reducing the need for specialized medical personnel to conduct ultrasound exams.

By leveraging AI, these services could increase the speed and accuracy of diagnoses and treatment, ultimately improving patient outcomes. Needless to say, this deal significantly bolstered GEHC’s lineup and is expected to generate more than enough revenue to cover the price the company paid for the acquisition.

Despite its promising performance, GEHC remains under the radar and underappreciated. Comparing it to its peers, such as Mettler Toledo (MTD), Danaher (DHR), Boston Scientific (BSX), and Thermo Fisher (TMO), the company’s valuation looks discounted. Considering that it has the potential to become a long-term compounder, I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

May 4, 2022

Fiat Lux

Featured Trade:

(A PICK AND SHOVELS BUSINESS POISED TO EXPLODE)

(TMO), (CRSP), (MRNA), (BNTX), (A), (DHR), (ILMN)

There’s never a wrong time to begin investing. In 2021, the markets generated positive buzz when things started to heat up again.

That same optimism has recently transformed into bearishness following the decline in share prices.

Nevertheless, there’s still good news.

Given the lower valuations, investors can now get more bang for their buck.

In the past two years, we’ve experienced so many unprecedented events. Among the most heavily affected by the pandemic is the life sciences sector.

One of the biggest names in this field is Thermo Fisher Scientific (TMO).

With a market capitalization of roughly $200 billion, it’s no longer accurate to describe this as an under-the-radar company. TMO has received minimal fanfare among investors despite its massive size for decades.

A key reason for this is its lowkey steady execution of a well-established or tried-and-tested strategy.

Although it lacks the pizzazz of more exciting companies these days like CRISPR Therapeutics (CRSP), Moderna (MRNA), and BioNTech (BNTX), TMO has rewarded its investors with substantial returns.

Over the last 40 years, TMO has recorded an annual growth rate of 16.5%, hitting a 27,000% return in total by 2021.

In fact, TMO came off a strong 2021.

Its sales grew by 22% from 2020 to report $39.2 billion. While acquisitions played significant roles in the company’s growth, the 17% organic revenue growth of TMO served as its primary growth driver behind its solid numbers in 2021.

Even its COVID-19-related sales, particularly its testing products, contributed to reach $9.2 billion.

Looking at TMO’s business model, it’s evident that the company offers investors great exposure to the entire healthcare field via a single investment only.

That is, TMO is a broad business. It covers practically all life sciences solutions, analytical tools, specialty diagnostics, lab items, and even clinical, biotechnology, and pharmaceutical services.

Spanning the entire industry, such portfolio of products and services allow TMO to confidently go toe-to-toe against industry heavyweights like Agilent Technologies (A), Danaher (DHR), and Illumina (ILMN).

Actually, all of its segments grew last year, with TMO showing off quicker revenue increases than its competitors in the previous five years.

Hence, it is no surprise that TMO expects its numbers to climb in 2022. For this year, the company’s projected revenue is estimated to rise by at least 7% to reach $42 billion.

TMO strategically leveraged more significant acquisitions to build its diverse and deep portfolio today.

In 2011, the company spent $3.5 billion to buy Sweden’s blood-testing firm Phadia and cleverly maneuvered a relatively cheap deal to also grab chromatography company Dionex for only $2.1 billion.

In 2013, TMO bought a fast-growing genetic testing company called Life Tech for $13.6 billion.

At that time, Life Tech was the leader in this field and already possessed the technology to become a front-runner in the personalized medicine space.

In 2016, it shelled out $4.2 billion for electron microscopy company FEI and dropped another $7.2 billion in 2017 to buy pharmaceutical contract manufacturer Patheon.

To date, TMO’s most substantial deal is its $17.4 billion acquisition of contract research business Wilmington’s PPD.

This particular deal created a gateway between the biopharma giant and other drug developers, with TMO boosting its services segment focused on its biotechnology and pharmaceutical clients.

Between 2019 and 2021, the pharmaceutical and biotechnology market has experienced a promising over 20% growth.

This field is expected to grow to an additional $20 billion in 2022, following the growing interest in the industry in this post-pandemic era.

There is another emerging sector within the pharmaceutical and biotechnology market: the precision medicine and gene sequencing field.

Taking into consideration the growing demand for the products and services from this space, this market is estimated to reach roughly $1.6 trillion by 2030.

This makes TMO’s PPD acquisition timely, as it would allow the company to gain a bigger market share and expand its reach across the globe.

Furthermore, the previous acquisitions would bolster the company’s hold on the current market and ensure its position as a first-mover in potential groundbreaking innovations in the biotech and pharma sector.

Considering its expansion strategies and growth history, TMO doesn’t seem to be stopping anytime soon.

While the environment for mergers and acquisitions did become a bit more restrictive these days, there are still several potential buyout targets that could deliver favorable returns. So, we might hear about another TMO-linked acquisition sometime soon.

Overall, TMO is a healthcare stock offering robust and stable growth and a promising future regardless of economic downturns.

Moreover, its pick-and-shovels play makes it an excellent stock that looks poised to sustain its momentum and is well-positioned for global expansion. Hence, it would be wise to buy the dip.