Mad Hedge Biotech and Healthcare Letter

May 8, 2025

Fiat Lux

Featured Trade:

(A DOUBLE HELIX OF OPPORTUNITY)

(CRSP), (NTLA)

Mad Hedge Biotech and Healthcare Letter

May 8, 2025

Fiat Lux

Featured Trade:

(A DOUBLE HELIX OF OPPORTUNITY)

(CRSP), (NTLA)

I never fully appreciated the potential of gene therapy until last fall when my college friend Eric called with surprising news. His 14-year-old daughter Sophie, who'd struggled with sickle cell disease her whole life, had undergone treatment with Casgevy, a CRISPR-based gene therapy developed by CRISPR Therapeutics (CRSP) and Vertex (VRTX). Six months later, she hasn't needed a single blood transfusion or hospitalization—a transformative outcome for a girl accustomed to spending more weeks in hospital rooms than classrooms.

"The doctors keep using phrases like 'functionally cured,'" Eric told me. "I just know she's planning her first summer camp experience. That's miracle enough for me."

Eric's story prompted me to dive deeper into gene-editing therapies and the companies working on them. What struck me the most is that despite groundbreaking science, market volatility has created a disconnect between technological progress and stock valuations.

Gene therapy stocks like CRISPR Therapeutics and Intellia Therapeutics (NTLA) had a rocky first quarter of 2025, with shares dropping 2.82% and 24.19%, respectively. The broader market mirrored this instability, with the S&P 500 down nearly 3%. Yet, beneath these headline fluctuations lies an intriguing opportunity for patient long-term investors.

CRISPR is particularly interesting. It's sitting pretty with $1.9 billion in cash and equivalents as of the end of 2024. That's enough runway to keep the scientists doing what they do best for years without financial pressure.

More importantly, they're expecting their flagship product Casgevy to be accretive from late 2025, meaning actual revenue is on the horizon – not just the promise of future miracles.

Casgevy's approval for sickle cell disease and beta-thalassemia underscores CRISPR Therapeutics' tangible progress. With a cost of $2.2 million per patient, the price seems steep until compared against lifetime management costs of these conditions. Additionally, their pipeline extends beyond blood disorders into cardiovascular treatments like CTX-310 and CTX-320. These therapies aim to permanently eliminate the need for daily medications—a seismic shift in a market projected to grow from $156 billion in 2025 to nearly $215 billion by 2034.

CRISPR Therapeutics' strategic advantage is further enhanced by their U.S.-based manufacturing facility, strategically positioned to mitigate risks from reshoring trends and global supply chain disruptions.

On the other hand, Intellia faces a tighter financial outlook. With $861.73 million in cash and equivalents, they project operations funding through the first half of 2027. However, this timeline feels restrictive, especially since their first products aren't anticipated until at least 2027.

Although their financial runway is limited, Intellia's therapeutic breakthroughs still command attention. Their treatments NTLA-2002 for hereditary angioedema and Nex-z for transthyretin amyloidosis have shown extraordinary results. I remember a conversation with a trial participant who shared, "I went from planning my life around my disease to barely remembering I have it." Such transformative experiences underline the real-world potential of Intellia's science.

However, Intellia must dramatically reduce its annual cash burn from $592 million to around $345 million to ensure survival until commercialization. This aggressive belt-tightening could jeopardize their momentum.

Both companies currently trade at attractive valuations given their prospects. CRISPR Therapeutics holds a price-to-book ratio below the sector median, with cash comprising 57% of its market cap. Intellia's cash reserves represent an astounding 94% of its market cap, suggesting significant market undervaluation of its intellectual property and promising pipeline.

For investors able to tolerate short-term volatility, this disconnect offers a potentially lucrative entry point, particularly with CRISPR Therapeutics’ imminent commercial revenue.

As I told Eric, the market currently undervalues these revolutionary companies despite proven science. Eventually, stock prices will reflect this reality. I'm cautiously building positions during these dips, anticipating the long-term transformative impact of these therapies.

Just ask Sophie, who’s packing for summer camp instead of preparing for another hospital stay.

Mad Hedge Biotech and Healthcare Letter

June 11, 2024

Fiat Lux

Featured Trade:

(THE CAPITAL CURE)

(ABBV), (MRK), (PFE), (RHHBY), (JNJ), (AZN), (GSK), (MRNA), (BNTX), (CRSP), (NTLA), (BEAM), (TPTX), (ZNTL), (MRTX), (BPMC), (MGNX), (TYRA), (SPRT), (VRTX), (FOLD), (RARE), (CRBU)

Imagine you're the CEO of a major pharmaceutical company. You've got blockbuster drugs that are raking in billions, a cushy corner office, and a corporate jet at your disposal. Life is good.

But then, you look at the calendar and realize that your patents are about to expire. Suddenly, that jet feels more like a crop duster, and your corner office starts to feel like a broom closet.

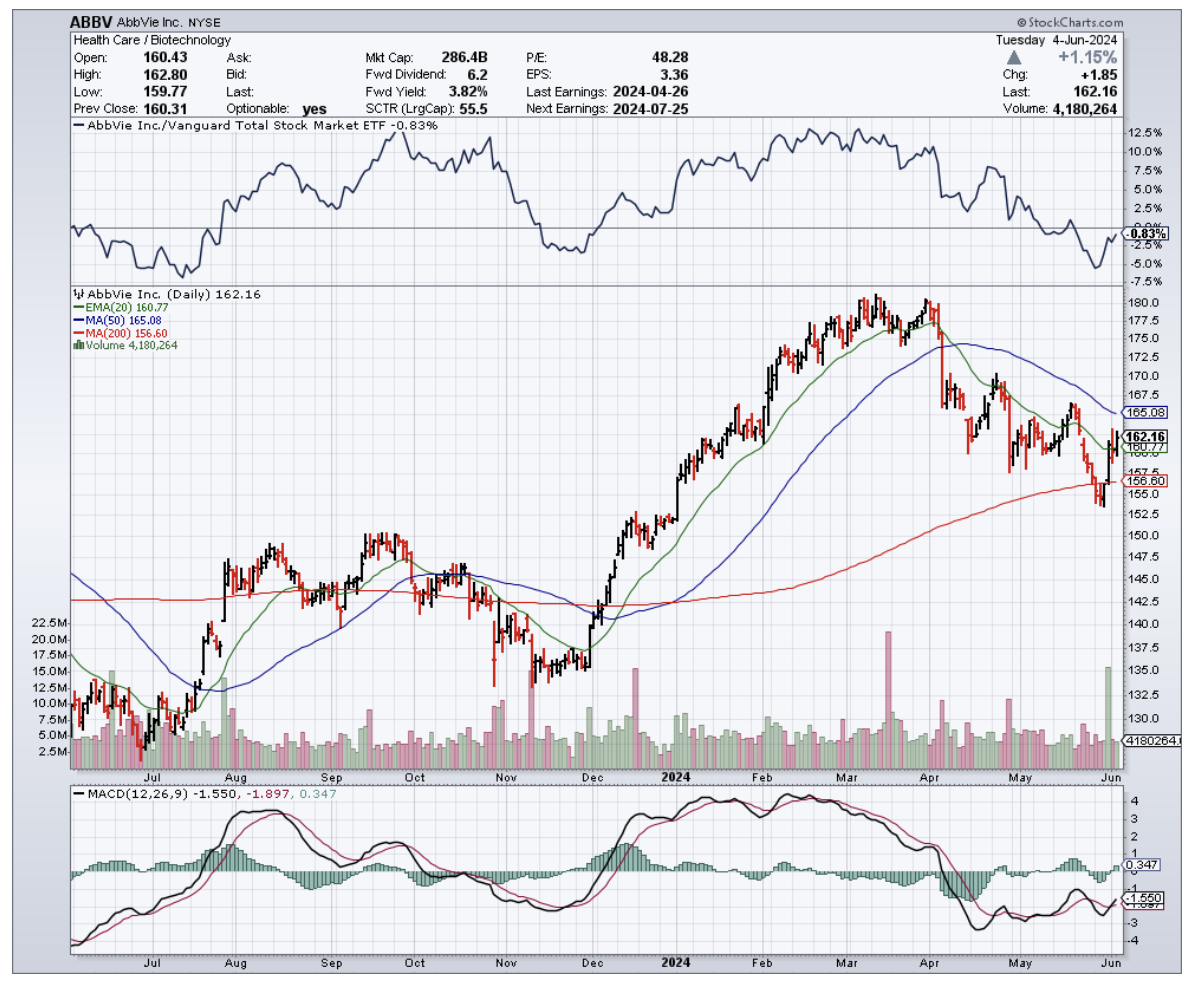

That's the reality facing Big Pharma right now. These pharma big shots are sweating bullets over losing their golden geese like AbbVie's (ABBV) Humira and Merck's (MRK) Keytruda.

That’s roughly $300 billion in products about to get kicked to the curb.

But these guys didn't get to the top by sitting on their hands. They've got a war chest of $1 trillion, and they're not afraid to use it.

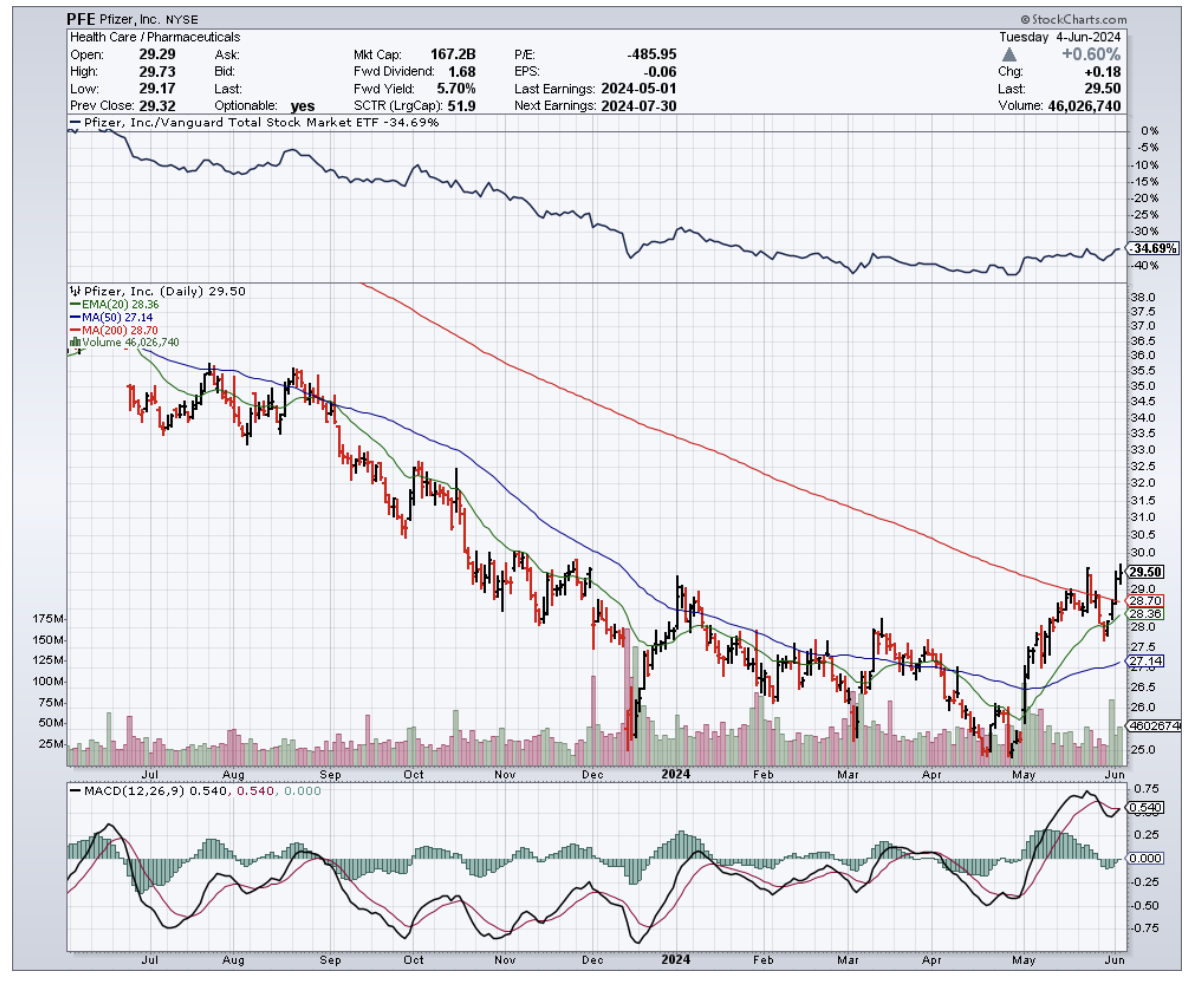

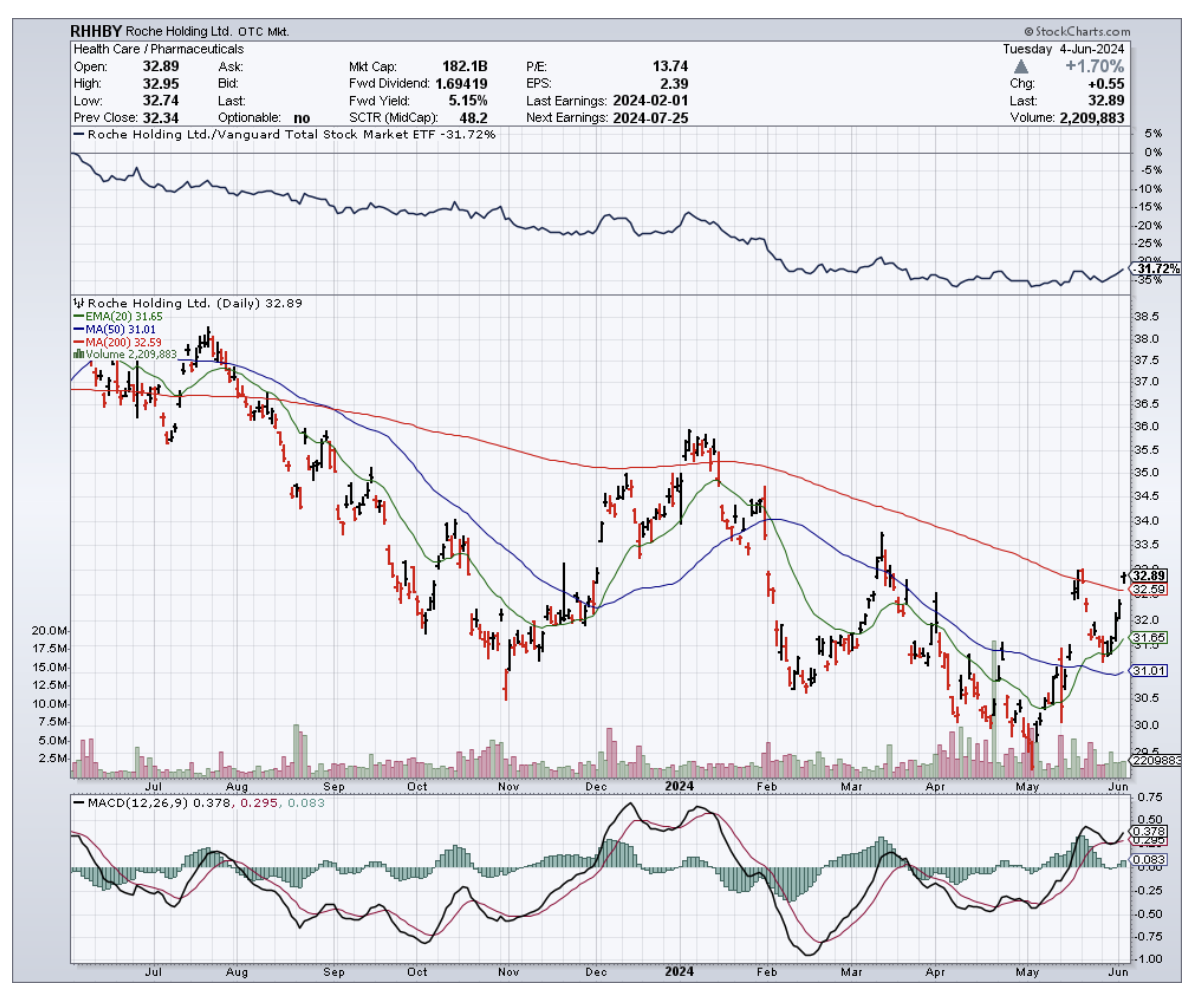

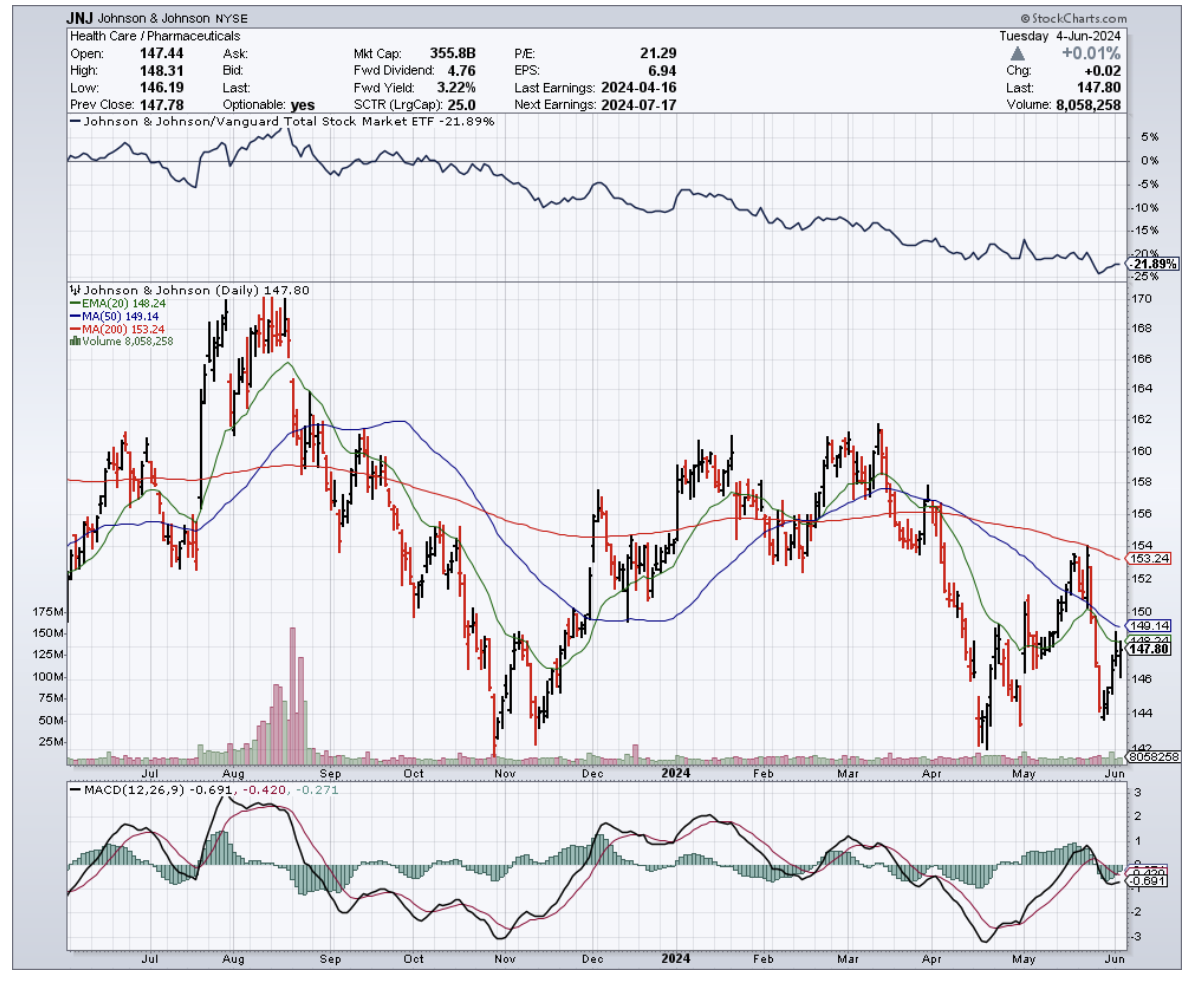

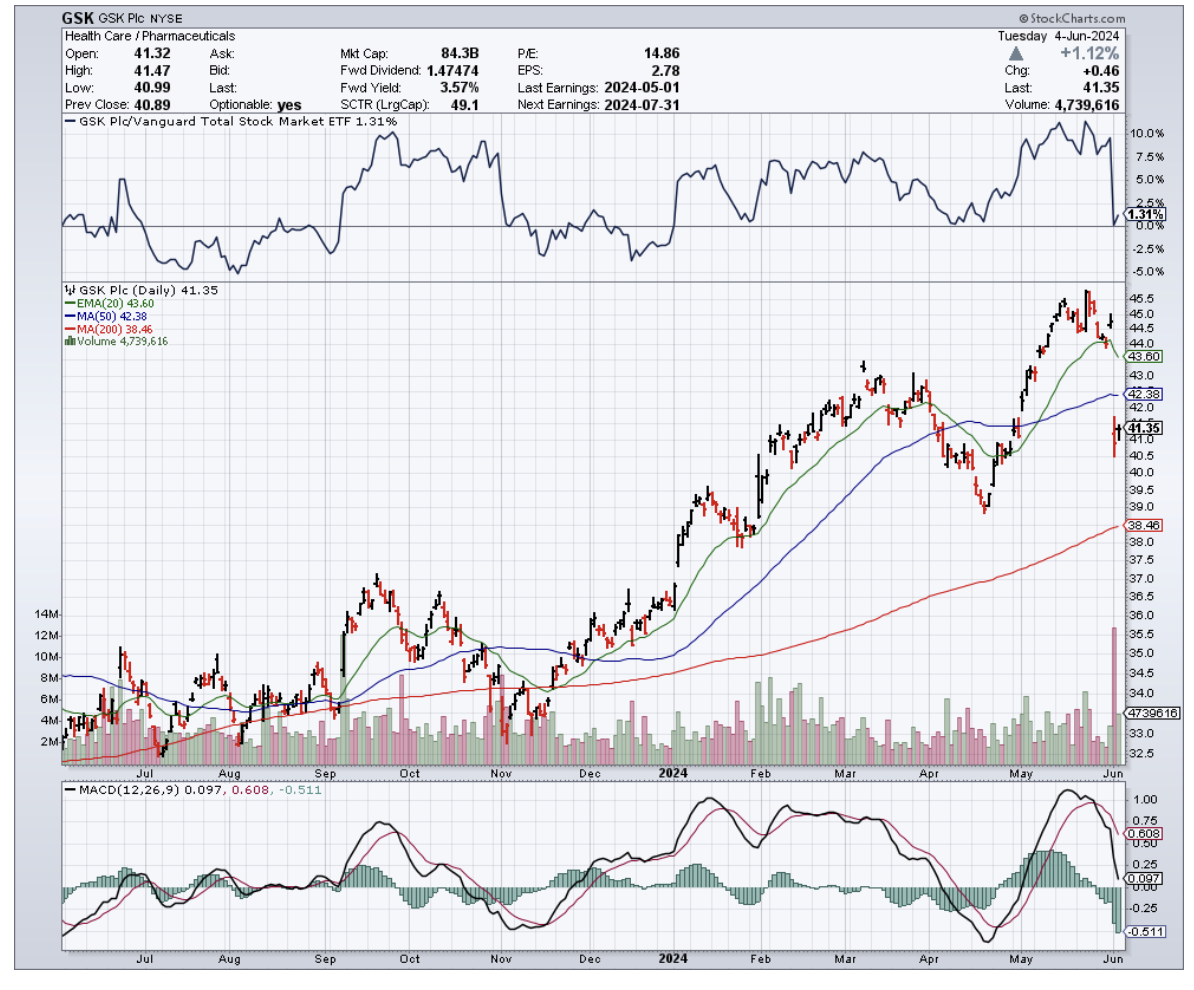

Major pharmaceutical giants like Pfizer (PFE), Roche (RHHBY), Johnson & Johnson (JNJ), AstraZeneca (AZN), and GlaxoSmithKline (GSK) are about to go on the mother of all shopping sprees.

Why the rush? Because they're staring down the barrel of a patent cliff that's going to make the Grand Canyon look like a pothole.

We're talking $198 billion worth of branded drugs going off the patent cliff between 2021 and 2025. That's a gut-wrenching 56% jump from the last five years.

But don't think for a second that they're just going to sit back and watch their profits go up in smoke. No sir, they're on the hunt for the next big thing, and they've got their sights set on some juicy targets – and biotech is at the top of their list.

Leading the biotech charge are mRNA pioneers Moderna (MRNA) and BioNTech (BNTX), each sitting on a gold mine of potential blockbusters taking on everything from flu to cancer vaccines.

Underdogs like CRISPR (CRSP) biotech stars Intellia (NTLA) and Beam Therapeutics (BEAM) are also squarely in Big Pharma's acquisition crosshairs for their cutting-edge work in genetic disease treatments.

But beyond the headliners, don't overlook the sleeper hits that could catalyze the next big boom.

Oncology, in particular, is a prime hunting ground, accounting for 37% of pharma M&A deal value in 2023 as the $392 billion global cancer drug market continues to boom.

Companies like Turning Point Therapeutics (TPTX) and Zentalis Pharmaceuticals (ZNTL), with their promising targeted therapies for various solid tumors, are particularly attractive prospects.

Mirati Therapeutics (MRTX), focused on KRAS inhibitors, and Blueprint Medicines (BPMC), specializing in precision therapies, have also caught the eye of big pharma with their innovative approaches.

Additionally, companies with late-stage assets like MacroGenics (MGNX), Mereo BioPharma (MREO), and Tyra Biosciences (TYRA) could offer promising near-term revenue opportunities for acquiring companies looking to bolster their oncology portfolios.

Close behind are rare disease treatments, snagging 16% of new drug approvals and 9 of the top 100 deals last year in this $262 billion market ripe for more growth.

This lucrative sector has captivated pharma giants, who see potential in companies like Sarepta Therapeutics (SRPT) and Vertex Pharmaceuticals (VRTX), leaders in rare disease therapies with strong financial performance and consistent growth.

Aside from these, smaller biotechs like Amicus Therapeutics (FOLD) and Ultragenyx Pharmaceutical (RARE), focused on developing innovative therapies for a range of rare diseases, are attracting attention for their potential to address unmet medical needs and deliver substantial returns on investment.

But the real wild card everyone wants a piece of is cell and gene therapies. This medical Wild West is projected to explode to $66.8 billion by 2030, with the FDA already greenlighting 6 cutting-edge therapies like next-gen CAR-T treatments from Caribou Biosciences (CRBU) in 2023 alone.

Notably, the buying frenzy is very much already underway. In fact, 2023 saw the biggest biotech M&A spree in a decade, with a staggering $122.2 billion changing hands as the FDA approved 50% more new therapies.

Pharma mega-mergers also hit $135.5 billion as firms raced to reload pipelines.

Interestingly, these deals are only the tip of the iceberg. As Wall Street predicts, with record-smashing deals, sky-high demand, and new approvals surging, "biotech's got plenty of reasons to be cautiously optimistic."

Especially if interest rates finally cooperate, throwing gasoline on the M&A bonfire and making biotech the belle of the ball as soon as late 2024.

So keep your eyes peeled and your powder dry. I suggest you add these innovative biotech names to your watchlist, and you might just discover the next blockbuster drug or breakthrough therapy that could reshape medicine – and deliver explosive returns in the process.

Mad Hedge Biotech and Healthcare Letter

January 2, 2024

Fiat Lux

Featured Trade:

(FROM LIMPING TO LEAPING)

(LLY), (NVO), (PFE), (AMGN), (VRTX), (BMY), (CRSP), (NTLA)

The year 2023 in the biotechnology and healthcare world has been a rollercoaster with more dips than peaks.

While Eli Lilly (LLY) and Novo Nordisk (NVO) are hitting the jackpot with their new weight loss drugs, the rest of the healthcare sector is limping behind.

By year's end, the S&P 500 Health Care index had slipped by 0.4% since the start of the year, starkly contrasting the broader S&P 500's robust 24% growth.

That’s not just a minor setback; it's the sector's most significant underperformance in 30 years.

Fast forward to 2024. Conventional wisdom suggests healthcare stocks might lag in an election year. Why? Presidential candidates love to shake things up with healthcare reform promises, usually sending investors into a sell-off frenzy.

But this time around, the air is tinged with an unexpected optimism. After a year of hefty sell-offs, healthcare valuations have become irresistibly low, presenting a fertile ground for investment opportunities.

Plus, there's less regulatory uncertainty now, with major acquisitions like Amgen's (AMGN) of Horizon Therapeutics and Pfizer's (PFE) of Seagen sailing through without a hitch. And let's not forget the anticipated interest rate cuts could be a game-changer for the sector.

Interestingly, the typical election-year healthcare jitters might be less intense in 2024. After all, the likely presidential candidates are familiar faces, and the healthcare changes they've made (or not made) are well known.

Trump’s healthcare impact was minimal, and Biden has already pushed through significant drug pricing reform with the Medicare drug price negotiation program. This program, despite legal hurdles, is moving forward and has been priced into the market's expectations.

In a surprising turn of events, the Biden administration's recent move to potentially invalidate patents of some high-priced drugs didn't send investors running for the hills like it might have in previous years. It seems the fear of drug price regulation may be losing its sting.

Now, let's take a closer look at some of the healthcare sectors that are drawing attention.

Biotech has been in a slump since 2020, but things are starting to look up. The sector's last three-year downturn was in 1992, followed by a significant rebound.

Despite challenges like high capital-raising costs and a deluge of IPOs, biotech is showing signs of life. As these pandemic-era companies mature and produce valuable data, they offer both buying and selling opportunities.

M&A activity in biotech is also on the rise, and if interest rates fall, the sector's prospects look even brighter.

Keep an eye on Vertex Pharmaceuticals (VRTX), which is set to reveal more data on its experimental pain drug, and Amgen, which is awaiting data on its new obesity pill. CRISPR Therapeutics (CRSP) and Intellia Therapeutics (NTLA) should be on your watchlist, too.

Over in MedTech, the hype around GLP-1 weight loss drugs led to a sector-wide selloff.

The iShares Medical Devices ETF took a hit, dropping 13.9% by the end of October, but it started to recover in the last two months of the year. The GLP-1 concerns might continue to cast a shadow, but there's a growing sense that their impact might be more long-term, especially if interest rates fall.

In the pharma world, 2023 was a tale of two halves: Eli Lilly and Novo Nordisk on one side, with their successful weight-loss drugs and the rest trailing behind.

While the S&P 500 Pharmaceuticals index slightly declined, Lilly and Novo surged ahead with 56% and over 45% gains, respectively.

But 2024 might bring new challenges, especially for Lilly, as it rolls out Zepbound, its highly anticipated weight-loss drug.

For Novo, the focus will be on how Ozempic fares under Medicare's new drug pricing negotiations set to take effect in 2027.

The key to success in pharma now is finding companies with innovative drugs that promise revenue acceleration without the looming threat of patent cliffs. Pfizer and Bristol Myers Squibb (BMY), for instance, are under the microscope as they navigate impending patent expirations and strive to reassure investors.

In 2023, the healthcare market was a stock picker's paradise, especially given its complexity. The year ahead promises more of the same. Investors should be on the lookout for opportunities among stocks that underperformed last year but have solid fundamentals.

Despite the unpredictability of election years and the bumpy ride of 2023, the healthcare sector, buoyed by low valuations and potential rate cuts, is gearing up for what could be a significant turnaround this 2024. For savvy investors, this could be an opportunity not to be missed.

Mad Hedge Biotech and Healthcare Letter

December 14, 2023

Fiat Lux

Featured Trade:

(EDITING YOUR PORTFOLIO)

(CRSP), (VRTX), (BLUE), (BEAM), (CRBU), (EDIT), (NTLA), (PRME), (VERV), (LLY), (REGN)

In the world of biotechnology, the buzz these days is all about gene editing – a frontier that’s moving at warp speed.

While the journey from sequencing the first human genome took a staggering 13 years, companies like CRISPR Therapeutics (CRSP) have sped up the process, bringing their revolutionary "molecular scissors" concept to market in a mere decade.

It's a thrilling time for investors, with the potential for staggering returns, but the path is littered with clinical and regulatory landmines. This turns choosing the best stocks to put your money into a tricky challenge.

Recently, the FDA gave the green light to two groundbreaking gene therapies for sickle cell disease, developed by Vertex Pharmaceuticals (VRTX) in collaboration with CRISPR Therapeutics and by Bluebird Bio (BLUE).

This disease, predominantly affecting African-American communities in the U.S., has been a target for medical advancement for years.

While the approval is a landmark, it's not without its tremors. Bluebird Bio's stock took a nosedive by 33.9%, triggered by the FDA’s warning label about potential cancer risks linked to their treatment.

In contrast, the treatment by Vertex and CRISPR dodged such warnings, possibly giving it an edge in the eyes of prescribing doctors.

And then there’s the money side of things. Bluebird Bio missed out on a priority review voucher from the FDA, which they were hoping to sell to Novartis for a cool $103 million. That's a tough break.

Meanwhile, the Vertex and CRISPR therapy, now known as Casgevy, boasts the honor of being the first FDA-approved drug using the trailblazing Crispr/Cas9 technology. It's a Nobel Prize-winning innovation that's finally reaching the patients it promises to help.

The approvals of Casgevy and Bluebird Bio’s Lyfgenia, which arrived earlier than expected, mark a significant moment for patients with sickle cell disease.

Although priced in the millions, these treatments offer a potential one-time cure, replacing the traditional, complex regimens. Unfortunately, they are not without their challenges, involving intensive procedures, lengthy hospital stays, and chemotherapy.

This brings us to the investment side of things.

The gene-editing arena is brimming with potential, but it's akin to navigating a labyrinth. With no specific exchange-traded funds (ETFs) focusing solely on gene editing stocks, investors might feel like they're trying to find their way in the dark.

However, a diversified approach could be the lantern in this darkness.

Companies like Beam Therapeutics (BEAM), Caribou Biosciences (CRBU), Editas Medicine (EDIT), Intellia Therapeutics (NTLA), Prime Medicine (PRME), and Verve Therapeutics (VERV) are some of the key players in this space, each with its unique technological platform.

But it's not just the pure-play gene editors that are worth your attention. Giants like Eli Lilly (LLY), Regeneron Pharmaceuticals (REGN), and Vertex Pharmaceuticals have thrown their hats into the ring, making substantial investments in gene editing.

So, how should you play this? If it were my money, I'd spread it around.

Put a chunk in leaders like CRISPR and Intellia. Then, combine these with established players like Eli Lilly, Regeneron, and Vertex to provide a safety net, balancing out the inherent risks of this high-stakes biotech game.

On the other hand, companies like Beam and Verve, representing the next wave of this technology, should not be overlooked, though perhaps with a more conservative stake.

And here's a little hedge for you: keep an eye on smaller players like Caribou Biosciences and Editas Medicine. In this high-stakes game, they could be your ace in the hole.

The gene-editing industry is a roller coaster of innovation, risk, and potential. It's a sector where fortunes can be made and lost in the blink of an eye.

For the savvy investor, a diversified, strategic approach, blending the bold with the stable, could be the key to unlocking the vast potential of this exciting field.

Remember, as with any investment, the key is not just in choosing the right horses but knowing how to spread your bets across the race.

Mad Hedge Biotech and Healthcare Letter

July 11, 2023

Fiat Lux

Featured Trade:

(A CALCULATED GAMBLE)

(PFE), (CRBU), (AAPL), (NTLA), (CRSP)

There has been a lot of chin-wagging about whether we're on a collision course with a recession or on the upswing. I get it. It's as confusing as figuring out why Warren Buffet didn't invest in Apple (AAPL) sooner.

Still, there are stocks that, recession or not, will let you sleep like a baby. In the biotechnology and healthcare sector, Pfizer (PFE) stands out as one of those stocks. In bear markets, it fares well because, well, let's face it, health trumps wealth every time.

Now, you might look at Pfizer's recent earnings and think it's taken a bit of a tumble. No growth in revenue or EPS in the first quarter of 2023? That’s definitely worrisome. But hold your horses. Let's peel back the layers a bit to see the full picture.

Pfizer has been raking in the dough from its COVID-19 potions, especially its vaccine Comirnaty and therapy Paxlovid. With the COVID gold rush subsiding, the company reported a 29% dip in revenue in Q1, clocking in at $18.3 billion.

Remember, context is key. Strip out the COVID-19 products, and revenue has actually nudged up 5% YoY.

It’s the same story with the company's forecast.

Revenues are predicted to be between $67 billion and $71 billion, a drop of 29% to 33%. But subtract the COVID dollars and cents, and Pfizer's set to grow between 7% to 9%.

What's Pfizer doing with its COVID-19 windfall? It's not buying beachfront properties, that's for sure.

Instead, it has a staggering 101 programs in the pipeline, including 38 in phase 3 trials. This year, the company also had four new approvals, from new uses for Paxlovid and Prevnar 20 to a vaccine for older folks and a nasal spray for migraines.

But the market's jittery about the predicted revenue drop, causing the stock to tumble 21% this year. That just makes it a bargain.

Pfizer's trading at less than 8 times earnings makes it the frugal shopper's dream.

To sweeten the pot, Pfizer's upped its quarterly dividend by 2.5% to $0.41 a pop. That gives a yield of about 4%, twice the average of the S&P 500. More impressively, it's been doing this for 14 consecutive years.

However, Pfizer's not resting on its laurels.

Its latest move? A 7% stake in Caribou Biosciences (CRBU), a firm that's pushing the boundaries of gene-editing tech and cell therapies for cancer. It's like investing in a tech startup but with a biological twist.

Caribou's stock has taken a wild ride since it went public in 2021, peaking at over $30 and dipping to a recent low of $4. After Pfizer's buy-in, it jumped 46% to $5.94. A small stake of $25 million, but it's a clear sign that gene editing is back in the spotlight.

Moreover, Caribou's no one-trick pony.

It's testing treatments based on the Nobel Prize-winning CRISPR technology. This precision tool allows doctors to zero in on problematic DNA and tweak it. The potential for treatments for cancer and genetic disorders is mind-boggling.

Caribou currently has a pair of potential game-changers simmering in the preliminary stages.

First up is their experimental treatment, CB-010, aiming a direct hit at blood cancer lymphoma. This therapy manipulates immune cells to lock onto the cancer.

Picture them as bounty hunters of the body, genetically tweaked to bring down the cancerous bad guys.

To date, we've got a trio of these CAR-T therapies courtesy of other pharmaceutical giants in the game, but they all work on modifying the patient's immune cells. Unfortunately, not every patient’s cells are ripe for the CAR-T transformation.

This is where Caribou switches things up.

The biotech’s CAR-T therapy is akin to a supermarket for immune cells – off-the-shelf and ready for action. Through some nifty gene editing, immune cells from healthy volunteers are modified and packed for delivery.

In theory, these should pack more punch. And it seems they do, judging by Caribou's initial guinea pigs – six lymphoma patients who saw their cancer vanish without a trace after a rendezvous with Caribou's CAR-T.

Obviously, they’re not promising an everlasting disappearance, but a couple of these folks kept their cancer at bay for at least a year.

While Caribou isn't alone in the off-the-shelf CAR-T quest, they've put up a stellar performance so far against the likes of Intellia Therapeutics (NTLA) and CRISPR Therapeutics (CRSP).

Caribou’s pipeline also features another off-the-shelf CAR-T contender battling the blood disorder known as multiple myeloma. This therapy, dubbed CB-011, is what specifically caught Pfizer's eye. Basically, Pfizer’s investment has earned it the right to haggle for a license if another suitor comes courting for Caribou's star player.

But Caribou's act doesn't end here.

It has a growing ensemble featuring CB-012, a CAR-T cell therapy focused on recurrent or stubborn acute myeloid leukemia, and CB-020, another CAR-T variant for various stubborn tumors.

Pre-Pfizer deal, Caribou boasted a cash reservoir of $291 million, promising smooth sailing until around 2025.

Caribou promises an action-packed second half of 2023, with an update on CB-010's phase 1 trial safety and efficacy, a dose-escalation report for CB-011's phase 1 trial, and a new drug application for CB-012 targeting relapsed/refractory acute myeloid myeloma.

As with all biotechs in the clinical stage, though, it's a bit of a gamble. With some key milestones expected later this year, investors are watching with bated breath to see if the company can deliver.

If the dice roll the right way, Caribou could be a jackpot for Pfizer – and for savvy investors.

So if you're looking for a stock that has the potential to thrive despite market uncertainties, with a dash of excitement and a sprinkle of future possibilities, Pfizer could be your ticket.

Not only is it a reliable dividend payer, but its recent ventures show it's also not afraid to swing for the fences.