Mad Hedge Biotech and Healthcare Letter

January 21, 2025

Fiat Lux

Featured Trade:

(THE ONLY TIME FIGHTING YOURSELF MAKES MONEY)

(ABBV), (AMGN), (SDZNY), (CHRS), (PFE), (JNJ), (ALVO), (TEVA), (SNY), (BMY)

Mad Hedge Biotech and Healthcare Letter

January 21, 2025

Fiat Lux

Featured Trade:

(THE ONLY TIME FIGHTING YOURSELF MAKES MONEY)

(ABBV), (AMGN), (SDZNY), (CHRS), (PFE), (JNJ), (ALVO), (TEVA), (SNY), (BMY)

If I had a dollar for every time someone told me the biotech sector was overvalued, I'd have enough to fund my own drug development program.

Yet here we are, watching the global immunology market rocket from $55 billion to $166 billion in just a decade, with the sector projected to hit $192 billion by 2028.

If you're wondering why big pharma keeps pouring billions into autoimmune research - and believe me, this question came up in every meeting last week - the answer is simple: we've barely scratched the surface.

Despite thousands of PhDs burning midnight oil in labs from Boston to Basel, we still don't have effective treatments for systemic lupus erythematosus, scleroderma, or even something as visible as vitiligo.

Want to see where the smart money is going? Look no further than the biosimilar stampede into AbbVie's (ABBV) Humira territory.

Like bargain hunters at a Black Friday sale, everyone's getting in line: Amgen (AMGN) with Amjevita, Sandoz (SDZNY) with Hyrimoz, Coherus (CHRS) with Yusimry, and Pfizer (PFE) with Abrilada.

And just when you thought the party was over, here comes Amgen's Wezlana challenging Johnson & Johnson's (JNJ) Stelara, followed by Alvotech (ALVO) and Teva's (TEVA) Selarsdi.

But here's where it gets interesting. I've identified four companies that are trading at valuations that would make Benjamin Graham smile.

First up is AbbVie, trading at 15.96x earnings (11.9% below sector median), with projected EPS growth to $15.21 by 2027.

Their dynamic duo of Rinvoq and Skyrizi is performing like a biotech version of Batman and Robin.

Rinvoq sales hit $1.61 billion in Q3 2024, up 45.4% year-over-year, while Skyrizi broke $3 billion, thanks to its mid-2024 FDA approval for ulcerative colitis.

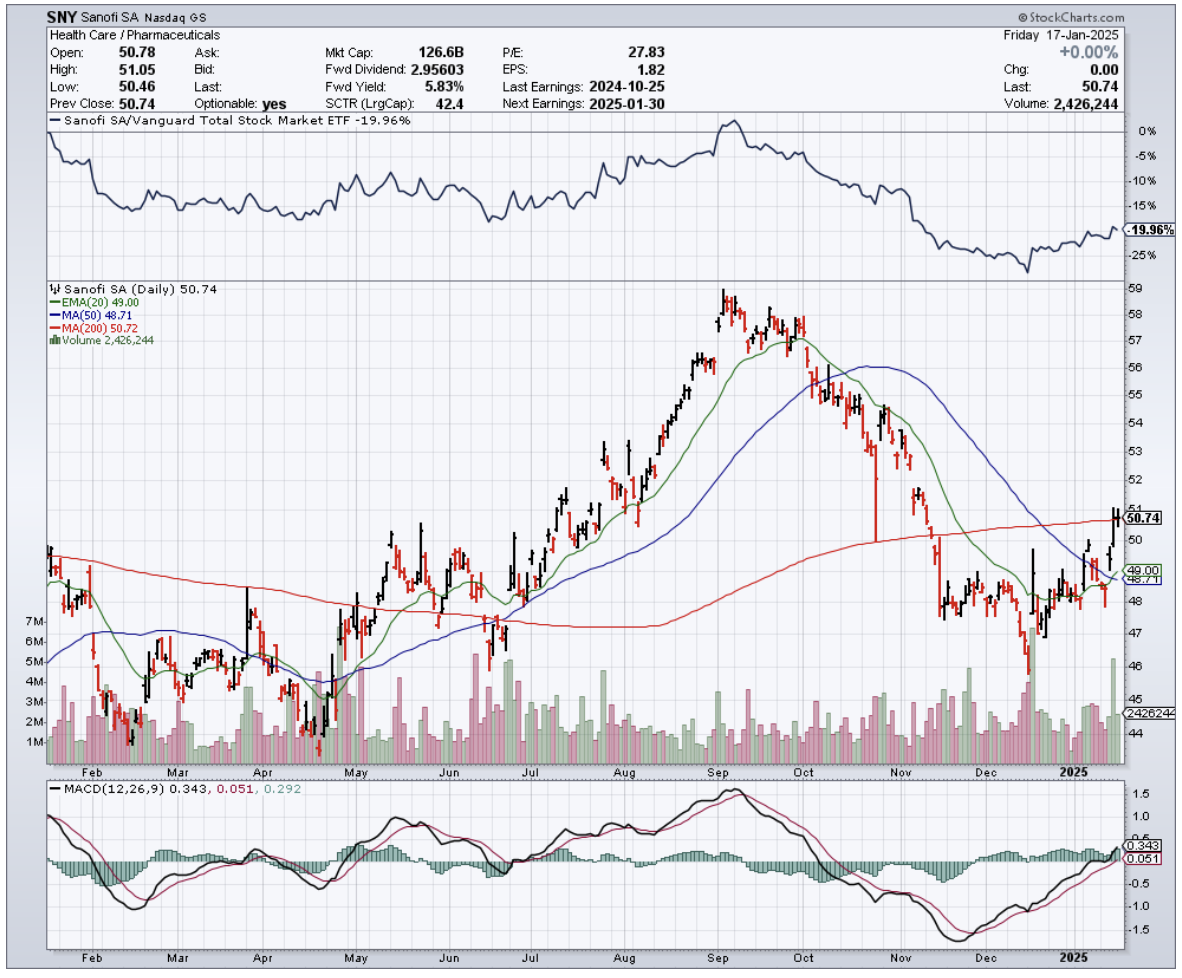

As for Sanofi (SNY)? Now we're talking value. At 11.7x earnings - 35.39% below sector median and 1.3% below its 5-year average - it's like finding a Ferrari priced like a Fiat.

Their star player Dupixent raked in 3.48 billion euros in Q3 2024, up 22.1% year-over-year and 5.2% quarter-over-quarter.

Then, there’s Teva Pharmaceuticals. Trading at a P/E ratio of 7.88x - that's 56.5% below the sector median - while projecting non-GAAP EPS growth to $3.6 by 2028.

But here's the kicker: their clinical trial data reads like a biotech investor's dream. Their new drug duvakitug achieved 47.8% clinical remission in ulcerative colitis patients versus 20.45% for placebo (p=0.003).

In Crohn's disease? Even better - 47.8% endoscopic response compared to 13% for placebo (p<0.001).

Finally, there's Bristol-Myers Squibb (BMY). Yes, it's trading at 47.5x earnings (162.1% above sector median), but here's where patience pays off - their P/E ratio is expected to drop to 8.82x by 2027.

Meanwhile, Zeposia sales jumped 19.5% year-over-year to $147 million in Q3 2024, while Sotyktu showed consecutive quarterly growth.

The cherry on top? These companies are paying you to wait. We're talking dividend yields from 3.8% to 4.41% - try getting that from your savings account.

Looking at these numbers reminds me of the tech sector in the late 1990s, but with one crucial difference - these companies are actually making money, lots of it.

They generate significant cash flow and have strong balance sheets, unlike many of the high-flying tech companies of the dot-com era that were burning through cash with no clear path to profitability.

While others are chasing the next meme stock or crypto moonshot, smart investors are quietly positioning themselves in companies that are literally changing the face of medicine.

Remember, buying umbrellas in the summer heat has always been my style.

Right now, the immunology sector is experiencing its own kind of summer, and these four stocks are your umbrellas.

The forecast? Growth storms ahead.

Mad Hedge Biotech and Healthcare Letter

January 16, 2025

Fiat Lux

Featured Trade:

(THE EYES HAVE IT)

(REGN), (SNY), (PFE), (BMY)

Last week, while waiting for my annual eye exam, I couldn't help but notice the parade of elderly patients shuffling in for their regular Eylea injections. My optometrist tells me these folks show up like clockwork every 4-8 weeks, rain or shine.

That's about to change, and therein lies a multibillion-dollar story.

You see, when Regeneron reported Q3 earnings on Halloween, boy, they sure had some treats for investors. Revenue hit $3.72 billion, up 11% YoY, with EPS coming in at a sweet $11.54.

But here's what really caught my attention: their cost of revenue was $1.762 billion, while R&D and SG&A expenses ran $1.271 billion and $714.4 million respectively.

Net income? A cool $1.34 billion. Not too shabby for a company whose main product is under siege from copycats.

Speaking of copycats, let's talk about Eylea. The original formula saw revenues drop 21% YoY to $1.145 billion – that's what happens when biosimilars crash your party.

This is where it gets interesting though: Eylea HD (think of it as Eylea's muscled-up big brother) jumped from a mere $43 million to $392 million YoY.

Sure, about $40 million of that came from wholesalers stocking up like it's Black Friday at Costco, but still – that's what I call a growth story.

I've been watching Regeneron since they were just a gleam in Wall Street's eye, and they've always had a knack for turning scientific breakthroughs into cold, hard cash.

Take Dupixent, their inflammation blockbuster co-developed with Sanofi (SNY). It just got FDA approval for COPD with an eosinophilic phenotype.

Why does this matter? Because we're talking about a $6 billion market opportunity here, folks.

About 36% of COPD patients have this particular flavor of the disease and trust me, there are more of them than you'd think still wheezing away on their old inhalers.

Want to know what else is cooking in their labs? They're working on antibodies that could make blood clots a thing of the past – think better than Eliquis, which pulls in $10 billion annually for Pfizer (PFE) and Bristol Myers Squibb (BMY). Their secret? Something called Factor XI, which could be a game-changer for the 1 in 5 patients at high risk for bleeding.

And because no self-respecting biotech can resist the siren call of the obesity market, they're also cooking up their own weight loss cocktail. Results won't drop until late 2025, but if they crack the code on keeping weight off AFTER stopping treatment, they'll have something Wegovy and Zepbound can't match.

The financials are rock solid, too: $2.012 billion in cash, $7.785 billion in marketable securities, and current assets of $19.334 billion versus current liabilities of just $3.661 billion.

They've generated $3.158 billion from operations in the first nine months of 2024 alone.

Yes, there's $1.984 billion in long-term debt, but with cash flow like that, it's about as worrying as a paper cut.

I've already started nibbling at Regeneron, and I'm looking to add more if it dips further. After all, this is a company that's proven it can grow revenues at upper single digits year over year while maintaining 25% free cash flow margins - the kind of numbers that make a value investor's heart skip a beat.

Sure, there are risks lurking around every corner – biosimilars nipping at Eylea's heels, Medicare negotiations that could squeeze margins, and clinical trials that might go sideways.

But with multiple growth catalysts and a pipeline that reads like a wish list for modern medicine, Regeneron's got more upside than my daughter's college tuition bills.

As my optometrist likes to say - in the land of the blind, the one-eyed man is king. But in the land of biotech, Regeneron's got a 20/20 vision for what's coming next.

Mad Hedge Biotech and Healthcare Letter

December 17, 2024

Fiat Lux

Featured Trade:

(THE BIG BATCH THEORY)

(CTLT), (DHR), (RGEN), (AVTR), (NVO), (PFE), (LLY), (MRK)

If I had a nickel for every time someone said pharmaceutical manufacturing was boring, I could’ve started bidding against Novo Holdings for Catalent (CTLT) myself.

Sure, I’d still be $16.5 billion short, but you get the point—this deal is huge, and it’s about to make some smart money look even smarter.

Here’s the deal: Novo Holdings is shelling out $16.5 billion to snap up Catalent, a contract development and manufacturing organization (CDMO).

If that acronym sounds like alphabet soup, let me translate: CDMOs are where the real action happens.

These are the guys behind the curtain making sure your miracle drugs and life-saving treatments aren’t just ideas—they’re products hitting the market at scale.

The numbers don’t lie. The CDMO market sits at $146 billion right now.

Fast-forward to next year, and that balloons to $243.3 billion. By 2029, it’s cruising toward a cool $332 billion.

And if you think that’s impressive, just wait: the broader pharmaceutical outsourcing trend is nowhere near slowing down.

In 2014, Big Pharma still clung to in-house production for 66.3% of its output.

Today? That figure’s down to 51%, and dropping fast. Why? Because outsourcing lets the specialists handle the hard stuff—faster, cheaper, and more efficiently.

For investors, Catalent’s immediate upside is a no-brainer. The acquisition premium is pure gravy, but that’s not the whole story.

Rivals like Lonza Group (SWX: LONN) and Samsung Biologics are already feeling the heat.

The biologics CDMO market alone is expected to expand by $10.63 billion between 2024 and 2028, and you better believe those two are scrambling to stay ahead.

If you own shares, keep your seatbelt fastened. If you don’t, well… you might want to rethink that.

And here’s where it gets really interesting: Novo Holdings may be private, but its publicly traded golden child, Novo Nordisk (NVO), is set to ride this wave like a pro surfer.

They’re already a global powerhouse in biologics, and Catalent’s souped-up manufacturing capabilities are going to help them scale production with military-grade efficiency.

Lower costs, tighter operations, bigger margins—it’s like handing a Formula 1 car to an already championship-winning team.

So if you’re not watching Novo Nordisk stock, you’re doing it wrong.

Of course, it’s not just the big CDMO players who stand to win here. Companies like Danaher (DHR), Repligen (RGEN), and Avantor (AVTR) are quietly cashing in on this gold rush.

These firms supply the picks, shovels, and critical bioprocessing tools that CDMOs need to keep production humming.

As Catalent scales under Novo Holdings, demand for these essentials will go through the roof.

Zooming out, the pharma manufacturing landscape is evolving at a breakneck pace.

The CDMO market is expected to hit $530.3 billion by 2033, growing at a steady 7.7% CAGR.

That’s not speculative growth—it’s a structural shift, backed by demand for biologics, gene therapies, and personalized medicine.

In short, we’re entering an era where outsourcing is king, and companies with the infrastructure to capitalize on it are poised to dominate.

Don’t forget about the big dogs in Big Pharma, either.

Pfizer (PFE), Eli Lilly (LLY), and Merck (MRK) aren’t just spectators in this game. They’re snapping up CDMO capacity, investing in biologics, and doubling down on therapies with blockbuster potential.

The Catalent deal is just the latest chess move in a game where the stakes keep getting higher.

So what does this mean for you? If you’re holding Catalent, congratulations—your portfolio is about to get a nice bump.

But the real play here isn’t Catalent alone. It’s understanding that CDMOs, suppliers, and adjacent players are the unsung heroes of this industry transformation.

You want exposure to the companies enabling the next wave of medical innovation? This is where you look.

Novo Holdings just threw down the gauntlet, and the smart money is already moving. The pharmaceutical manufacturing sector isn’t boring—it’s booming.

So, while everyone’s chasing flashy biotech startups and blockbuster drugs, the real smart money is quietly following the companies that make those breakthroughs possible.

Catalent isn’t just a $16.5 billion deal—it’s proof that outsourcing is the new backbone of pharma’s future. Call it “The Big Batch Theory:” scale up, outsource smart, and watch the returns multiply.

Ignore this shift, and you’re leaving money on the table.

Now, if you’ll excuse me, I need to check my CDMO positions. Just like a perfectly run batch, they’re growing fast—and that’s exactly how I like it."

Mad Hedge Biotech and Healthcare Letter

December 12, 2024

Fiat Lux

Featured Trade:

(BREAKING THE MOLD)

(MRK), (PFE), (GILD), (AZN), (DSNKY), (JNJ)

Did you know that in the 1890s, scientists tried to cure cancer by injecting patients with... bread mold? (Spoiler alert: it didn't work.)

Fast forward to 2024, and Merck just announced something that makes moldy bread look like, well, moldy bread: their new cancer drug achieved a 100% complete response rate in its Phase 3 trial.

That's doctor-speak for "the cancer completely disappeared in every single patient." Not 99%. Not 99.9%. One hundred percent.

The drug in question is zilovertamab vedotin, and it belongs to a fascinating family of medications called antibody-drug conjugates, or ADCs.

These drugs are essentially molecular delivery trucks - the antibody part knows exactly where to go, while the drug part carries the cancer-fighting payload.

It's a bit like having a microscopic postal service that only delivers to cancer cells, except instead of Amazon packages, it's delivering something more lethal.

The story of how Merck got their hands on this drug is equally interesting.

In 2020, they wrote a check for $2.75 billion to acquire a company called VelosBio. To put that number in perspective, that's enough money to fund a small space program, or if you're feeling particularly eccentric, to buy 5.5 million laboratory mice (a purchase that would probably raise some eyebrows at the bank).

The global market for ADCs hit $7.72 billion in 2023, and some analysts predict it could reach $44 billion by 2029. I asked three different economists to explain these projections and got four different answers, but they all agreed on one thing: it's a lot of zeros.

And, as expected, the competition in this field is intense. Pfizer (PFE) bought Seagen for $43 billion. AstraZeneca (AZN) and Daiichi Sankyo (DSNKY) partnered up for Enhertu, while Gilead Sciences (GILD) nabbed Immunomedics and their wonderfully named drug Trodelvy.

Even Johnson & Johnson (JNJ), which most people associate with baby shampoo and that bottle of Band-Aids in their medicine cabinet, jumped into the fray by buying Ambrx Biopharma.

Then there's Mersana Therapeutics, partnered with Merck. They're smaller than the pharmaceutical giants, but in biotech, size isn't everything. (I once visited a lab where groundbreaking cancer research was happening in a space roughly the size of my kitchen.)

What makes Merck's achievement particularly remarkable is its rarity. In the world of cancer research, getting a 100% response rate is about as common as finding a unanimous decision on social media. It represents a fundamental shift in how we treat cancer, moving from traditional chemotherapy to these precisely targeted treatments.

For investors wanting a piece of this molecular magic, here's the thing: success in biotech isn't like picking a winning racehorse (though both can make your palms equally sweaty).

It's about finding companies that have mastered the three-ring circus of innovation, partnerships, and research pipelines. And yes, I've spent enough time in research facilities to know that "pipeline" is just a fancy word for "stuff we hope works but haven't broken yet."

Merck's perfect score suggests they've cracked one particular code, but companies like Seagen (now part of Pfizer), AstraZeneca, and Daiichi Sankyo are all pushing boundaries in their own ways.

Despite the competition, Merck's recent achievements still look the most promising. The company's breakthrough with zilovertamab vedotin suggests they're not just throwing darts at a laboratory wall - they're onto something big. So when their stock dips, smart money takes notice.

Similarly, Seagen, now under Pfizer's umbrella, looks particularly promising, especially given their established track record in the ADC space and Pfizer's deep pockets. Add them to your watchlist, too.

AstraZeneca and Pfizer, meanwhile, merit a steady "hold" position in your portfolio - like that reliable sourdough starter that keeps producing even if it's not particularly exciting at the moment.

Both companies have proven ADC programs and the resources to weather market volatility, even if they're not currently serving up the kind of headline-grabbing results that Merck just delivered.

Remember those 19th-century scientists with their bread mold? Turns out, they were onto something, even if their execution was a bit... moldy.

And while I wouldn't recommend their treatment methods today (please don't raid your fridge for experimental purposes), their spirit of innovation lives on in every precisely-targeted ADC molecule. After all these years, I guess you could say cancer treatment has finally risen above its moldy beginnings.

Mad Hedge Biotech and Healthcare Letter

November 26, 2024

Fiat Lux

Featured Trade:

(NO MORE EATING AT YOU)

(PFE), (LLY), (NVO), (AMGN), (RYTM), (ALT)

Who knew the devil could lurk in an Excel spreadsheet? More specifically, in a hidden tab that, until recently, was minding its own business like a shy teenager at a school dance.

That is, until some eagle-eyed analyst at Cantor Fitzgerald decided to right-click their way into a $12 billion nightmare for Amgen.

(If you're wondering how to find these hidden tabs yourself, just right-click on any visible tab in Excel. Though after this debacle, pharmaceutical companies might start password-protecting their spreadsheets like they're nuclear launch codes.)

The data in question concerns MariTide, Amgen's hopeful contestant in the "help-America-lose-weight" sweepstakes.

The hidden tabs revealed what the published paper in Nature Metabolism conspicuously didn't mention: bone density scans that would make an osteoporologist reach for their stress ball.

Patients receiving the 420-milligram dose saw their bone density drop by about 4% over 12 weeks - the kind of number that sends stock traders reaching for their sell buttons faster than you can say "osteoporosis."

Speaking of selling, this discovery sent Amgen's stock tumbling 7%, which in the biotech world is like watching $12 billion vanish faster than free cookies at a Weight Watchers meeting.

Amgen, doing what pharmaceutical companies do best when faced with uncomfortable data, assured everyone that their Phase 1 study doesn't suggest any bone safety concerns. (One imagines their PR team working overtime, possibly sustained by the same stress-eating habits their drug aims to curb.)

Now, let's talk about the increasingly crowded room of companies trying to help elephants become gazelles.

Novo Nordisk (NVO), the current crown prince of weight-loss drugs, is sitting pretty with Wegovy raking in 17.3 billion Danish kroner (about $2.5 billion) in just one quarter.

They're so confident they're throwing $11 billion at Catalent faster than you can say "production scale-up." That's enough kroner to buy every Danish pastry in Copenhagen, though that might defeat the purpose.

Not to be outdone, Eli Lilly's (LLY) Zepbound is showing off with weight loss results that would make Jenny Craig jealous - we're talking 21% body weight reduction.

Together with Novo Nordisk, they're expected to dominate 80% of the market, leaving other companies to fight over the crumbs like desperate dieters at a birthday party.

Still, the supporting cast is equally fascinating.

Pfizer's (PFE) danuglipron and Structure Therapeutics' (GPCR) GSBR-1290 are trying to turn these injectable drugs into pills, because apparently not everyone enjoys playing pin cushion.

Viking Therapeutics (VKTX) is getting creative with VK2735, a dual GLP-1 and glucagon receptor agonist, which is pharmaceutical speak for "two mechanisms of action are better than one."

Meanwhile, AstraZeneca's (AZN) AZD5004 is trying to join the party, though their early Phase I results are about as impressive as a rice cake at a dessert buffet.

Now, let’s take a look at the numbers. The global anti-obesity drugs market is expected to balloon from $6.15 billion in 2024 to an eye-watering $37.94 billion by 2032.

But, that seems to be just the conservative estimate. Some analysts are betting this market could hit $150 billion by the early 2030s.

So, what’s the smart move here?

For those watching this space (while probably patting their own midsections thoughtfully), the message is clear: This market is hotter than a freshman chemistry experiment gone wrong.

But as Amgen's Excel adventure shows, sometimes the devil really is in the details - or in this case, in Tab 9, hidden away like a chocolate bar in a dieter's sock drawer.

And like my old friend Deng Xiaoping used to say, sometimes you have to cross the river by feeling the stones.

Today, those stones are telling me this: hold off on buying Amgen - that bone density data isn't just a minor setback, it's a potential deal-breaker.

If you really want to take part in the action, opt for Novo Nordisk and Eli Lilly for their proven ability to execute and dominate.

And for those of you who, like me, enjoy a bit of calculated risk-taking, consider a speculative position in Structure Therapeutics and Viking Therapeutics.

Before you get too excited, though, I'd suggest limiting these speculative plays to no more than 5% of your portfolio each - promising early-stage biotechs can deliver spectacular returns, but they can also crash faster than a poorly maintained MIG-25.