Mad Hedge Biotech & Healthcare Letter

November 3, 2020

Fiat Lux

FEATURED TRADE:

(TESTED AND PROVEN COVID-19 STOCK FOR THESE UNCERTAIN TIMES)

(ABT), (PFE), (AZN), (MRNA)

Mad Hedge Biotech & Healthcare Letter

November 3, 2020

Fiat Lux

FEATURED TRADE:

(TESTED AND PROVEN COVID-19 STOCK FOR THESE UNCERTAIN TIMES)

(ABT), (PFE), (AZN), (MRNA)

As we hold our breath for the results of the presidential election, it’s no surprise that investors are wondering how their portfolios will be impacted.

That’s why now is the right time to pick a stock or two that can thrive regardless of who emerges as the victor.

To do this, it’s wise to look at a company that has already experienced a boost under Trump’s presidency and could continue to enjoy the rewards even with a Joe Biden administration.

The obvious common denominator is Trump and Biden’s goal to be aggressive in COVID-19 testing for as long as the virus is around.

Pfizer (PFE), AstraZeneca (AZN), and Moderna (MRNA) are undoubtedly three of the most widely reported coronavirus stocks in the past months.

These companies were the first to launch their COVID-19 vaccine candidates in human trials and are the leaders in the race towards the finish line.

However, long-term investors may find more value betting on one of my preferred COVID-19 stocks: the $188 billion healthcare behemoth Abbott Laboratories (ABT).

Let me tell you why.

In either Trump’s or Biden’s presidency, Abbott stands to benefit.

Regardless of the winner of the 2020 election, Abbott remains a winner for as long as COVID-19 continues to threaten the world.

While the majority of COVID-19 vaccine companies have yet to generate income from their coronavirus programs due to pending FDA approvals, Abbott has been leveraging its pipeline to boost its growth even with the pandemic.

Since the early days of this health crisis, Abbott has been working to stay ahead of the pack.

To date, the company has at least seven COVID-19 tests with emergency use authorization from the FDA and are available in the market.

These tests, which boosted Abbott’s diagnostics sales by 39% in the third quarter, range from detecting active cases to identifying whether a person has been infected with the virus in the past.

The latest swab test to join Abbott’s growing lineup of COVID-19 products is called the antigen test and is designed to deliver results in as fast as 15 minutes and costs only $5.

To add convenience, this test is connected to a mobile to allow users to access their results right away.

Prior to the antigen test, Abbott launched a rapid detection test called BinaxNOW. This test can also return results on-site within 15 minutes. It has a free digital app, which sends users with negative results a “digital health pass” right on their phones.

When BinaxNOW was launched in August, the Trump administration spent $760 million for 150 million tests.

This company has supplied over 100 million COVID-19 tests and generated roughly $881 million in sales in the third quarter, up from the $615 million it reported in the second quarter.

Abbott is one of the safer stocks to own in the healthcare sector, with sales estimates for this company expected to grow by 14% in 2021 and 2022.

So far, Abbott shares have climbed 22% this year. Even amidst the pandemic, Abbott raised its full-year guidance for its earnings per share from $3.25 to $3.55.

While the company has been focused on its COVID-19 programs, this strategy is not a one-time deal.

On the contrary, the popularity of its COVID-19 testing kits serves as the much-needed door-opener for Abbott to expand its medical venues—an effort that generally takes years to develop.

For instance, its diabetes care segment alone managed to achieve a 26.9% year-over-year jump in sales to reach $843 million in the third quarter.

On top of that, Abbott has an incredibly diverse pipeline with over 100 new products across its different business units.

Abbott is a widely known dividend aristocrat, paying quarterly dividends consistently since 1924. It has a proven track record of solid performance and a carefully curated suite of businesses that promises future rewards.

At the rate the company is growing and the future projects it has in its pipeline, this dividend aristocrat would no doubt continue with this proud tradition of rewarding its investors generously.

Mad Hedge Biotech & Healthcare Letter

October 22, 2020

Fiat Lux

FEATURED TRADE:

(IS THIS COVID-19 VACCINE OUTLIER ON THE FAST LANE?)

(NVAX), (PFE), (AZN), (JNJ), (SNY), (MRNA), (TAK)

It is not at all surprising that the biggest names in the healthcare industry are dominating the COVID-19 vaccine race.

After all, Big Pharmas such as Pfizer (PFE), AstraZeneca (AZN), Johnson & Johnson (JNJ), and Sanofi (SNY) are backed with vast resources that even media favorites like Moderna (MRNA) find challenging to compete against.

For months now though, going head to head with these big-name frontrunners is a clear outlier: Novavax (NVAX).

So far, there are only 10 COVID-19 vaccine candidates that have reached late-stage testing and Novavax’s NVX-CoV2373 has been performing at par (if not better) than its rivals—and the market has definitely noticed.

When 2020 started, Novavax’s market capitalization was less than $130 million and traded at roughly $4 per share.

Ten months into the pandemic, this small biotechnology company’s market cap grew to over $6.5 billion and has been trading at $110 per share—and that is already after a price decrease in the past weeks.

Given the disparity in its size and resources compared to its competitors, it’s safe to say that Novavax has been punching way above its weight class particularly in terms of landing supply agreements for its COVID-19 program.

Novavax first received a CEPI grant in March worth $4 million, which was immediately dwarfed by the $384 million the biotech company got in May.

In a matter of months, Novavax joined the major league players and secured a $1.6 billion funding courtesy of the US government’s Operation Warp Speed program.

In exchange, the biotech company will supply 100 million doses of NVX-CoV2373 to the US upon approval.

Novavax also inked an agreement with the UK for 60 million doses and another with Canada for 76 million doses.

Novavax has also landed deals with Japan through Takeda Pharmaceutical (TAK) and India via the Serum Institute of India.

As expected, the grants and supply agreements were perceived as votes of confidence on Novavax’s work and the company reaped the rewards.

In March, the prices started moving from less than $10 per share to almost $50.

By May, the price moved up to roughly $80 per share.

After its Operation Warp Speed contract in July, Novavax’s price per share soared all the way to $189 before eventually falling to $110 this October.

Novavax has only conducted late-stage testing in the UK. But, Phase 3 is expected to begin in the US soon as well.

Admittedly, a lot is riding on NVX-CoV2373.

However, the company has actually offloaded the majority—if not all—of its financial risks linked to the program.

Riding the momentum of its COVID-19 vaccine candidate, Novavax has been working on a related influenza vaccine called Nanoflu.

Given the market size for this, Nanoflu is estimated to rake in an annual revenue somewhere between $550 million and $1.7 billion.

Another potential blockbuster is respiratory syncytial virus (RSV) vaccine ResVax, which is projected to reach peak sales of $2 billion.

Novavax is also working on a vaccine candidate for the Ebola virus, the Middle East Respiratory Syndrome (MERS-CoV), and Severe Acute Respiratory Syndrome (SARS).

While NVX-CoV2373 is anticipated as Novavax’s moneymaker in the coming years, the biotech company can only realistically expect massive sales from this until 2023.

Looking at the company’s manufacturing partnerships and the aggressive timeline it has taken, Novavax is expected to produce 2 billion doses of its COVID-19 vaccine by mid-2021.

This is great news for its investors because of Novavax’s smaller market capitalization compared to its competitors.

Since the biotech company is projected as one of the first companies—if not the first—to offer a vaccine, then it can cover a substantial market share before its bigger rivals take over the market.

Even if Novavax prices its COVID-19 vaccine cheaply, say, $10 per dose, it can still generate $20 billion in annual sales.

Moreover, the late-stage success of NVX-CoV2373 will definitely cause Novavax’s stock price to skyrocket.

Despite this potential though, it’s important to keep in mind that this biotech company still has a way lower market cap than its rivals.

That means its share price will move a lot higher compared to the stocks of the other vaccine leaders.

Therefore, Novavax’s small size is not a negative for its investors—it is actually an advantage.

So for biotech investors who are searching for a promising COVID-19 vaccine stock, there’s nothing cheaper and more promising than Novavax.

Mad Hedge Biotech & Healthcare Letter

October 20, 2020

Fiat Lux

FEATURED TRADE:

THE MOST FAMOUS CANCER STOCK YOU’VE NEVER HEARD OF

(TRIL), (NVAX), (PFE), (IMMU), (SHOP), (GILD), (ABBV)

Biotechnology stocks have proven time and time again to be excellent growth vehicles for risk-tolerant investors.

Underscoring this claim are companies like COVID-19 vaccine frontrunner Novavax (NVAX), which generated jaw-dropping returns on capital for their investors within an impressively short period.

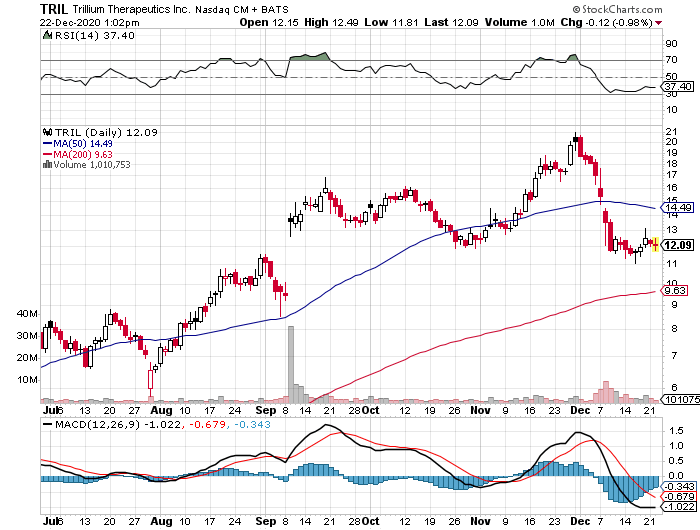

Now, another biotechnology stock is showing telltale signs of following their footsteps: Trillium Therapeutics (TRIL).

Trillium’s story is a familiar one in the biotechnology industry.

Trading only in the penny stock range back in 2019, the company’s share price practically quadrupled since the start of 2020.

Taking into consideration that this meteoric rise actually happened while COVID-19 was blasting the world to smithereens, it’s hardly surprising that this news didn’t receive much media attention.

Trillium’s shares are currently up by an astounding 1,260% -- and the company still has so much room to grow from here.

For context, Trillium had a market capitalization of $7 million in November 2019. This number skyrocketed to $1.3 billion since its shift to cancer technology.

Although a lot of factors came into play, the key turning point for Trillium was when the company decided to go all-in on its cancer programs.

Ultimately, Trillium’s goal is to challenge chemotherapy.

The move to shutter its lead programs on tumor treatments and instead focus on developing cancer-fighting technology was the gamble of a lifetime for the company.

This gutsy move impressed investors, and Trillium was never the same since then.

Today, Trillium is the No. 1 stock on Canada’s S&P/TSX Composite Index, overtaking its previous leader e-commerce giant Shopify (SHOP) by almost 10-fold.

In the US, Trillium shares rank as the No. 4 best-performing company on the Nasdaq Composite Index.

While its epic stock market rally may have some investors feeling left out, all signs point to further gains in the future even for those who missed the initial boom.

Among the major capitalists of this biotechnology company is giant biopharmaceutical company and COVID-19 vaccine leader Pfizer (PFE), which invested $25 million in Trillium’s common stock.

While this equity stake may seem small in relation to Pfizer’s $212.16 billion market capitalization, this initial show of confidence is hailed as a prelude to an even bigger investment in the future.

So far, the most exciting cancer treatments in Trillium’s pipeline are TTI-621 and TTI-622.

These programs are in the same class of emerging cancer technologies, called CD47-based therapies, that prompted Gilead Sciences’ (GILD) $4.9 billion acquisition of Forty Seven, Inc. in April this year.

Aside from Gilead, AbbVie (ABBV) has also been reported to have invested a huge sum in this technology.

In simplest terms, CD47-based therapies can bypass the “don’t eat me signal” put up by some cancer cells in an effort to evade immune detection.

Thus far, both TTI-621 and TTI-622 have been showing promising results. Trillium recently announced that it will increase the dosage in these programs.

While Trillium leaders have not been specific in terms of being open to an acquisition, their recent statements indicate that they are not completely opposed to one.

It’s either that or a partnership with a company as big or even bigger than Pfizer.

As with all the biotechnology stocks, however, there will always be a risk.

For Trillium, the most evident one is competition.

While it’s true that the company has been recognized as the leader in the CD47 arena, more and more competitors are entering the immuno-oncology space.

Right now, the most obvious rival is Gilead, which added Immunomedics (IMMU) to its arsenal via a $21 billion acquisition deal.

Given the sheer amount of money that Gilead has been spending to practically corner the immuno-oncology market, it’s to be expected that more biopharmaceutical titans will enter the fray.

This is one of the reasons Trillium has been tagged as a prime candidate for a massive acquisition deal soon. So far, Pfizer is considered the most probable suitor.

Despite its astonishing performance this year, Trillium’s market capitalization still remains within the small-cap territory. That’s to be expected since its lead assets are still undergoing trials.

Considering that it is an early-stage biotechnology stock, Trillium does not have much in terms of income.

However, the company does have enough cash to last for a while. At the moment, it has $130 million cash.

With its total expenses of $38.8 million in 2019, I say this could offer the company more than three years of breathing room financially.

But it would be shocking if Trillium’s value won’t enter the large-cap territory (higher than $10 billion) if and when the company’s high-value assets reach the late-stage studies.

The fact that it’s also an attractive acquisition candidate offers incredible incentive to its investors.

Simply put, Trillium’s stock could get as much as 1,000% gain over the coming two to three years, making it an ideal investment for risk-tolerant investors.

Mad Hedge Biotech & Healthcare Letter

October 13, 2020

Fiat Lux

FEATURED TRADE:

(THE UNDERDOGS OF THE COVID-19 VACCINE RACE)

(BNTX), (PFE), (CVAC), (PFE), (RHHBY)

It’s about time we talk about the German reinforcements brought in to fight this war against COVID-19.

For all the horror that this health crisis brought us, it’s nearly impossible to believe that there could be an upside to all these.

However, there is a bit of good news here.

Since the pandemic started, efforts to determine its origin, understand how it works, and search for a cure and vaccine have kickstarted innovation across the entire healthcare spectrum – from the familiar pharmaceutical sector to the volatile oft-misunderstood biotechnology field.

In fact, the biotechnology industry has received more attention in the past 10 months than the combined coverage of this sector since it was first introduced in 1919.

Nowadays, companies like Moderna (MRNA) have enjoyed practically round the clock coverage for their work.

So let’s take a look at the other up-and-coming biotechnology companies that have not received enough air time but are just as impressive.

In particular, let’s check out two of the German companies leading the charge in the COVID-19 vaccine race.

One company that isn’t getting enough credit these days is BioNTech (BNTX).

Since this German company paired up with Pfizer (PFE) in its vaccine development program, it rarely gets mentioned in the news.

After all, Pfizer with its $204.99 billion market capitalization makes for a bigger story compared to BioNTech’s $20.95 billion.

Nonetheless, the duo’s COVID-19 vaccine candidate, BNT162b2, is arguably the leading candidate right now – just ask Bill Gates.

If BNT162b2 succeeds, BioNTech stands to enjoy a financial windfall in the coming years.

So far, its vaccine program with Pfizer has secured them deals with the US, Canada, and Japan.

The German biotechnology company has also sealed an agreement with Fosun Pharma to supply 10 million doses to Macau and Hong Kong.

By 2021, BioNTech is expected to produce 250 million doses of the vaccine every six months.

This is enough to cover roughly 125 million people.

At a price of $19.50 for every dose, the company is estimated to earn $9.75 billion in annual revenue—not bad for a biotechnology company of its size.

The success of BNT162b2 could also mean additional leverage to propel the pipeline candidates in BioNTech’snmessenger RNA (mRNA) platform.

BioNTech has been working with Roche (RHHBY) in developing an mRNA therapy, called BNT122, to offer as a first-line treatment for melanoma and other solid tumors.

Apart from that, the company also has six early-stage mRNA candidates that target various types of cancer.

Aside from its mRNA technology-based programs, BioNTech is working with Denmark’s Genmab (CPH: GMAB) on three antibody therapies in early-stage trials for solid tumors and pancreatic cancer.

Another German biotechnology company flying under the radar is CureVac (CVAC).

A possible reason why it has not been generating that much buzz in the US is because it only conducted its initial public offering on the Nasdaq stock exchange in August.

Ever since the pandemic began though, CureVac has been one of the most active vaccine developers.

CureVac’s COVID-19 vaccine candidate uses the same technology as Moderna, which utilizes mRNA to trigger the body’s immune system to generate antibodies.

While Moderna has a huge head start in terms of clinical trials, CureVac may still have an advantage over the more popular biotechnology company.

Based on recent data, CureVac’s vaccine candidate shows more promise because it can take effect at very low doses of 2 to 6 micrograms.

In comparison, Moderna’s mRNA-1273 COVID-19 vaccine candidate requires a 100-microgram dosage.

Like BioNTech, the success of CureVac’s vaccine candidate would also bode well for the rest of the company’s mRNA candidates in its pipeline.

Two of those candidates are for cancer immunotherapies; one targets non-small lung cancer and the other targets a rare kind of cancer called adenoid cystic carcinoma. These therapies are also being studied for advanced melanoma as well as cancers of the head and neck.

Neither BioNTech nor CureVac has been hailed a household name in the US, and they may never reach that status.

Regardless, both companies will become extremely important and relevant for so many American households in the not-too-distant-future.

Due to the money they received to fund their COVID-19 programs, neither are in danger of running out of capital sometime soon or even take dilutive financing options as an alternative recourse. This stability, albeit short term, makes both biotechnology companies worth checking out.

More importantly, the pipeline programs of BioNTech and CureVac look promising despite being in the early stages.

All things considered, BioNTech and CureVac look like risky bets. However, these are risks with the potential to transform into massive rewards.

So, what should you do?

It all boils down to your investing style.

If you are an aggressive investor with high-risk tolerance, buy shares from dynamic biotechnology players that offer promising gains in a relatively short period.

Companies like BioNTech and CureVac, if successful in their COVID-19 vaccine efforts, could extend those gains to the long term and even leverage them to eventually market new products.

If you have lower risk tolerance, you can still make a play on these biotechnology companies. The key is to take a small position. This will limit your losses if things go south, but would also offer you rewards if the candidates work out.

Mad Hedge Biotech & Healthcare Letter

October 6, 2020

Fiat Lux

FEATURED TRADE:

(CAN THIS DIVIDEND KING BE THE NEXT VACCINE KING?)

(JNJ), (MRNA), (PFE), (BNTX), (AZN), (INO), (NVAX), (SNY)

One area that Johnson & Johnson (JNJ) has not been a leader in for the past years is vaccine development.

That could change soon however.

Among the healthcare companies racing to develop a COVID-19 vaccine these days, JNJ has been a heavy favorite to come up with the most potent candidate.

Although the company started its clinical trials two months after Moderna (MRNA) and the partners Pfizer (PFE) and BioNTech (BNTX) started theirs, JNJ might release results even earlier than November.

This is because JNJ’s vaccine candidate, called Ad26.COV2.S, worked quickly on the patients after only a single dose.

In comparison, Moderna and Pfizer’s candidates need a first dose and then, after a month, a second dose or a booster shot.

While it could take a month or two for Moderna and Pfizer’s vaccines to take effect, those given Ad26.COV2.S could be protected after two weeks.

Moderna and Pfizer both use messenger-RNA technology for their vaccines, while JNJ utilizes a hollowed-out virus to deliver the DNA instructions to the relevant cells to trigger a protein spike and provoke an immune response.

This is the same method the company used in its Ebola vaccine, which has been instrumental in the immunization programs in Africa.

Inasmuch as Ad26.COV2.S offers incredible potency compared to other candidates, there is one potential trade-off: our immune system might later on start to resist the drug.

However, JNJ is attempting to resolve this issue by developing a booster shot for future use.

Meanwhile, Moderna and Pfizer’s vaccine candidates could be given as many times as possible without that risk.

JNJ’s vaccine can also be distributed and stored without any special handling unlike its rivals, which require lower temperatures. This means that the vaccine can be delivered to even the less-developed facilities.

Other than eliminating the logistical problem of people failing to get a second shot of the vaccine, JNJ’s one-shot regimen can guarantee that governments can vaccinate 1 billion people annually.

Only a handful of the manufacturers can match that claim, offering JNJ an edge regardless of the seven-month head start of the other developers.

Apart from JNJ, Pfizer, and Moderna, more companies have started their late-stage vaccine trials. The list includes AstraZeneca (AZN), Inovio Pharmaceuticals (INO), Novavax (NVAX), and Sanofi (SNY).

Outside its COVID-19 programs, JNJ has been delivering solid results despite the ongoing crisis.

The company’s pharmaceutical division showed notable growth in the second quarter, with its immunology drugs leading the charge.

In terms of sales in this quarter, rheumatoid arthritis and Crohn’s disease drug Remicade raked in $935 million while severe rheumatoid, psoriatic, and ankylosing spondylitis injection Simponi brought in $526 million.

Meanwhile, psoriasis medicines Stelara and Tremfya generated an impressive $1.7 billion and $342 million, respectively.

JNJ is also expanding its portfolio to cover the biotechnology market. So far, one of its most telling moves is its $6.5 billion all-cash acquisition of Momental Pharmaceuticals.

Buoyed by these promising results, JNJ boosted its full-year revenue guidance for 2020 with operational sales estimated to reach somewhere between $81 billion and $82.5 billion.

JNJ has been widely known for its consumer products, but the truth is that the company’s forte is actually healthcare.

In 2019, JNJ’s pharmaceutical sector comprised nearly 50% while medical devices generated roughly one-third of the company's total sales. These figures may very well be the reason why this stock is gaining traction among retirees.

After all, healthcare is where the money lies – and JNJ is now the biggest healthcare conglomerate in the world.

In fact, the company serves over 1 billion patients on a daily basis and 12 of the products in its portfolio can easily generate $2 billion in sales annually.

The company’s cash flows have also been steadily increasing, setting off an impressive 58-year streak of consistent and consecutive dividend boost every year.

Needless to say, JNJ has been hailed the “Dividend King” in the healthcare sector for decades now.

Simply looking at JNJ profile, track record, and pipeline, it’s clear to see that buying and holding JNJ shares and reinvesting the dividends you receive along the way could give your portfolio a substantial boost.