Mad Hedge Biotech & Healthcare Letter

June 11, 2020

Fiat Lux

Featured Trade:

(THE BIOTECH MERGER BOOM ACCELERATES)

(AZN), (GILD), (BMY), (ABBV), (AGN), (TAK), (CI), (SNY), (JNJ), (UNH), (RHHBY), (LLY)

Mad Hedge Biotech & Healthcare Letter

June 11, 2020

Fiat Lux

Featured Trade:

(THE BIOTECH MERGER BOOM ACCELERATES)

(AZN), (GILD), (BMY), (ABBV), (AGN), (TAK), (CI), (SNY), (JNJ), (UNH), (RHHBY), (LLY)

Nothing can ever be absolutely shocking in the biotechnology and healthcare world.

I’ll admit though that the reports on AstraZeneca’s (AZN) interest in acquiring Gilead Sciences (GILD) surprised me.

The two companies touched base last month on a potential acquisition deal.

If this rumor turns into a reality, then we’re looking at what could be the biggest healthcare deal to date.

That’s saying something considering the massive mergers we’ve seen in the past years.

So far, the biggest biotechnology and healthcare deal is the $87.6 billion acquisition of Celgene (CELG) by Bristol-Myers Squibb (BMY) in 2019.

In the same year, AbbVie (ABBV) acquired Allergan (AGN) for a whopping $83.8 billion, making it the third biggest deal in the healthcare sector to date.

The year 2018 paved the way for two more massive deals in the form of Takeda’s (TAK) $81 billion acquisition of Shire, which ranks fourth overall, and Cigna’s (CI) $68.4 billion deal with Express Scripts (ESRX) in seventh place.

Fifth on the list is by Sanofi’s (SNY) $73.5 billion deal with Aventis in 2004.

Although it has been two decades since it happened, the $72.5 billion merger of Glaxo and SmithKline Beecham in 2000 still counts as one of the biggest deals in the industry. This agreement gave birth to GlaxoSmithKline (GSK).

Prior to Bristol-Myers Squibb and Celgene deal, it was Pfizer’s (PFE) $87.3 billion acquisition of Warner-Lambert in 1999 that topped the list.

AstraZeneca’s current market capitalization is roughly $140 billion. Meanwhile, Gilead Science’s market cap stands at approximately $96 billion.

With all these in mind, the AstraZeneca-Gilead Sciences merger is estimated to reach roughly $250 billion on top of the significant synergies expected throughout the years.

If these two health industry heavyweights merge, then their newly formed company would become the third biggest healthcare company in the world behind Johnson & Johnson (JNJ), which has a market cap of $384.55 billion, and UnitedHealth Group (UNH) with $293.85 billion.

Looking at this potential merger in the context of the coronavirus race, it’s safe to say that the combined efforts of AstraZeneca and Gilead would create a COVID-19 titan.

AstraZeneca’s partnership with the University of Oxford resulted in a COVID-19 vaccine candidate that was recently selected as one of the top five candidates worthy of US government support through Trump’s Operation Warp Speed program.

Meanwhile, Gilead’s antiviral medication Remdesivir has been constantly hailed as the standard of care for COVID-19 treatment since the pandemic broke.

The drug which was previously marketed as an HIV medication is now expected to generate $2 billion in sales as a COVID-19 treatment in 2020 alone.

In 2022, Remdesivir is estimated to rake in roughly $7.7 billion in sales. After that, the antiviral drug is projected to generate annual sales somewhere between $6 billion and $7 billion.

Although everything is hypothetical, let’s take a quick look at where each company stands at the moment outside their COVID-19 efforts.

AstraZeneca has been a consistent strong stock market performer throughout the years.

In the first quarter of 2020, sales improved in practically all of AstraZeneca’s territories. Although it has a diversified portfolio of drugs and a robust pipeline, the company’s hottest segment is its oncology business.

A good example of this is non-small cell lung cancer treatment Tagrisso, which is starting to live up to expectations as the next mega-blockbuster for AstraZeneca.

The cancer drug’s first quarter sales reached an impressive $982 million, showing off a 56% jump year over year.

This is promising considering that its competitors include Roche’s (RHHBY) Tarceva and Eli Lilly’s (LLY) Cyramza.

As for its 2020 revenue forecast, AstraZeneca is reported to rake in $25 billion, from which it will generate approximately $7.5 billion in operating profit.

On the other hand, Gilead also has an impressive portfolio that it can bring to the table.

In the first quarter of 2020, the company earned $5.47 billion in revenue compared to the $5.20 billion it generated in the same period last year.

Despite the decline in its hepatitis products from $790 million in the first quarter of 2019 to $729 in the same period of 2020, Gilead’s HIV line made up for the loss by bringing in over $4 billion in sales compared to the $3.6 billion it earned last year.

Not only that, some of Gilead’s other candidates are exciting.

For example, rheumatoid arthritis drug Filgotinib is expected to become another blockbuster and generate $5 billion in revenue annually.

Meanwhile, the anti-tumor treatment Magrolimab is estimated to rake in $3 billion in peak sales.

With the company’s older drugs still capable of generating strong revenue and its new candidates showing their potential for revenue expansion, Gilead can be assured of a continued cash flow well into the 2030s.

Regardless of whether this rumored mega-merger pushes through, both Gilead and AstraZeneca are attractive stocks worthy of their premium valuations.

Mad Hedge Biotech & Healthcare Letter

April 23, 2020

Fiat Lux

Featured Trade:

(POST-PANDEMIC STOCKS TO DIVERSIFY YOUR PORTFOLIO)

(BPMC), (NVTA)

Mad Hedge Biotech & Healthcare Letter

April 21, 2020

Fiat Lux

Featured Trade:

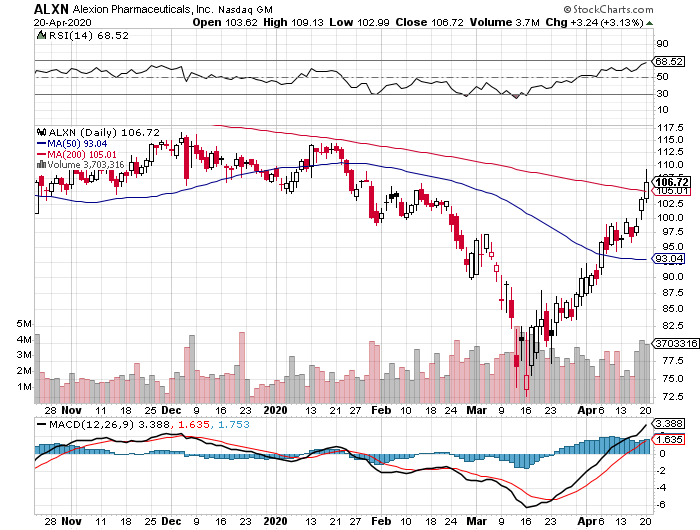

(GETTING YOU BANG PER BUCK WITH ALEXION PHARMACEUTICALS)

(ALXN), (GILD), (RHHBY), (REGN), (SNY)

Since nobody can actually control when to get sick or what type of disease to acquire, it makes absolute sense that biotech stocks remain one of the wisest bets if you want to put your hard-earned cash to work.

The question, therefore, is what are the best biotech stocks to buy now?

Looking at the biotechnology stock prices today, I can say that Alexion Pharmaceuticals (ALXN) will give you the most bang for your buck.

For over a decade, this ultra-rare-disease biotechnology company had been regularly valued at roughly 22 to 67 times its cash flow and frequently well above 30 times forward EPS.

Now, you can buy this top biotech stock for less than eight times its Wall Street profit consensus in 2021 and 10 times its cash flow for next year as well. It definitely doesn’t hurt that its PEG ratio is less than 1, categorizing it as an “undervalued” stock today.

However, its attractive pricing isn’t the only thing that’s putting Alexion in the news these days as this biotech company has been active in the race to find a coronavirus cure since early February.

When news about the pandemic broke, Alexion decided to repurpose its rare chronic blood disease bestseller Soliris as a potential COVID-19 treatment since the drug showed promising results on patients with severe pneumonia or acute respiratory distress syndrome.

Alexion’s efforts have been quite promising so far, with the biotech company targeting to commence a Phase 2 study of Soliris within the month. What we know so far is that this experiment will involve 10 patients as part of the proof-of-concept trial.

Apart from Alexion, other top biotech companies repurposing old drugs in search of a COVID-19 cure are Gilead Sciences (GILD) with Remdesivir, Roche (RHHBY) with Actemra, and Regeneron (REGN) and Sanofi (SNY) with Kevzara.

Outside its coronavirus treatment efforts, Alexion actually prides itself on a promising pipeline. To date, three treatments are projected to turn into blockbusters soon.

The first is Strensiq, which is formulated to treat a rare disease commonly known as hypophosphatasia. Patients with this disorder have an enzyme deficiency, making them unable to properly process calcium and phosphorus. As a result, they end up with malformed bones and teeth.

The second treatment is Kanuma, which is for patients suffering from lysosomal acid lipase (LAP) deficiency. People with this condition lack a key enzyme, preventing them from effectively breaking down fats.

Both conditions are extremely rare. Hypophosphatasia affects only 1 in 100,000 people while LAP is suffered by 1 in 40,000 individuals.

The third treatment is Ultomiris, which is widely regarded as Soliris’ successor.

For years, Soliris has been Alexion’s major moneymaker. However, uncertainties on the company’s hold on its patent exclusivity have started to shake investors’ faith in this stock. With one of Soliris’ key patents set to expire in 2021, the biotech company has to brace itself for the onslaught of generic competition.

This is where Ultomiris comes in.

Alexion has been busy migrating its customers to opt for Ultomiris before Soliris’ key patent expires.

To make this offer enticing, the biotech company has priced the newer drug to be slightly cheaper than the old blockbuster. Ultomiris costs $458,000 while Soliris is priced at $500,000.

To sweeten the deal further, the newer treatment is only required once every eight weeks. In comparison, Soliris’ treatment schedule is bi-monthly.

Basically, it’s as if Alexion has effectively restarted the clock in its patent exclusivity on this ultra-rare disease indication. The company aims to convert at least 70% of its users by mid-2020.

From a financial point of view, Alexion is performing quite well. Its fourth-quarter report showed that the company earned $1.4 billion in revenues, demonstrating a 23% increase from the same quarter in 2018.

Meanwhile, it raked in $5 billion in full-year sales for 2019. This indicated a 21% jump from its relatively paltry sales of $4.1 billion.

Looking at the metrics, Alexion is one of the surprisingly cheap stocks considering its growth. It also has the added bonus of dominating its chosen ultra-rare disease space.

This is typically a good strategy to avoid competition while also being able to seek high price points for its innovative treatments. The fact that insurers generally cover these treatments all but guarantees that Alexion is secure in terms of cash flow predictability.

Despite the panic induced by the coronavirus market, investing opportunities are everywhere --- if you know where to look.

Alexion is a solid company with strong growth prospects and is selling at a reasonable price. Any opportunistic investor worth his salt would know that this is the ideal time to strike.

Mad Hedge Biotech & Healthcare Letter

February 4, 2020

Fiat Lux

Featured Trade:

(ABBVIE’S BIG CORONA VIRUS PLAY)

(ABBV), (RHHBY), (GILD)

Two major issues are in the root of the panic caused by every new infectious disease.

The first is because of the uncontrollable spread of the virus, affecting thousands of people in a short span of time. This consequently pushes the public to question the capacity of their government to provide the proper healthcare to every patient, causing further confusion, alarm, and eventually, economic upheaval.

The second is the overpowering uncertainty that looms over not only the people directly affected by the disease but also the rest of the world as we feel like sitting ducks, wondering who the virus will infect next.

Both effects have become apparent with the news of a new coronavirus, known as 2019-nCoV, which originated in Wuhan, China.

The public’s reaction has come so close to mass hysteria, especially since the virus has already taken over 400 lives and infected more than 20,000 people worldwide.

The speed by which the disease is spreading is also alarming. The 2019-nCoV getting transmitted from one person to another almost as fast as the highly transmissible flu, which was not the case for its slower-moving cousins Severe Acute Respiratory Syndrome (SARS) and Middle East Respiratory Syndrome (MERS).

In response to this alarming situation, the Chinese government along with the medical community has turned to unconventional means to find a cure — and giant biotechnology company AbbVie (ABBV) is at the forefront of these efforts today.

One measure taken by the health experts is using AbbVie’s off-label HIV drug, called Kaletra (aka Aluvia), to treat 2019-nCoV patients.

Kaletra has two components valuable in battling the coronavirus: lopinavir and ritonavir. Both have the capacity to block HIV viral replication.

The twice-a-day Kaletra regimen comprises taking the HIV drug and undergoing infusions of interferon, a protein that triggers the immune system.

Although the AbbVie drug has yet to be officially declared as an approved cure for the 2019-nCoV, more and more health experts in China are already using it.

The belief on this treatment’s efficacy stemmed from the statement of the head at Peking University First Hospital, who shared that he contracted 2019-nCoV but cured himself by taking Kaletra.

This Chinese doctor is currently part of the national team of experts sent by the Chinese government to tend to those in Wuhan. Aside from him, Shanghai authorities disclosed that they have already adopted the HIV treatment in handling their own patients.

However, this isn’t the first time that Kaletra was deployed as a treatment against a coronavirus.

In 2004, Kaletra was used to cure the patients of SARS-CoV. This is promising since SARS, which is also caused by a coronavirus, bears a close resemblance to the 2019-nCoV. Experts tested the drug to help treat MERS patients as well.

A roadblock for the Kaletra cure is the scarcity of the drug in China.

A lot of health professionals disclosed that they have been struggling to get their hands on the AbbVie off-patent product. In response, AbbVie donated approximately $1.5 million worth of Kaletra to help contain the 2019-nCoV.

Other biotechnology behemoths have followed AbbVie’s lead of donating funds to help with the research in China. The list includes Roche Holding (RHHBY) and Gilead Sciences (GILD).

Meanwhile, this piece of promising news is not lost in the market. In fact, AbbVie shares pushed higher the moment Kaletra’s efficacy against the 2019-nCoV was revealed.

Apart from that, this development has reminded investors of AbbVie’s promising growth lately.

Unfortunately, most of the company’s growth came from acquisitions — a path where AbbVie has an abysmal track record. More often than not, investors fear that the company overpays in deals that fail to reap the promised rewards.

Case in point: AbbVie’s hefty $63 billion acquisition of Botox maker Allergan, which is due to be finalized early 2020.

In moving to acquire a company that only has one consistent blockbuster product, experts believe that AbbVie might have pulled the trigger too soon without considering other options.

While this high-profile agreement has been such a hot topic in the investing community, I think it’s a good move towards diversifying AbbVie’s sales and injecting additional growth.

Remember, AbbVie is in desperate need for a new outlet in light of the dwindling Humira sales. Adding a high-selling and established industry leader like Botox to the mix would make AbbVie more diversified than ever, making it safer.

More importantly, AbbVie ensured that the $63 billion acquisition doesn’t run the company to the ground — and its precautionary measures showed.

The company has been consistent in its net income, reporting over $5 billion annually in the past three years. It also raked in $12.8 billion in free cash flow in 2018, proving that AbbVie is well-positioned to acquire more companies and be more creative in looking for growth targets.

Hence, I view this biotechnology stock as an underrated buy that would appeal to bargain hunters willing to hang onto it for the years to come.

Mad Hedge Biotech & Healthcare Letter

January 16, 2020

Fiat Lux

Featured Trade:

(THE FUTURE OF PRECISION MEDICINE),

(ILMN), (PACB), (RHHBY), (TMO), (QGEN)

Hyper-personalized treatments, otherwise known as precision medicine, have been hailed as one the hallmarks of the healthcare revolution in the past decade.

Although a lot of people don’t see the need for such personalized treatments, a 2017 study by Boston medicine professor Jason Vassy indicated otherwise.

In his paper, titled “Annals of Internal Medicine,” Vassy discussed how his team performed whole-genome sequencing to 100 perfectly healthy adults.

To give you a better picture of how big this project was, whole-genome sequencing involves the analysis of the entire body’s DNA -- yes, all 3 billion pairs of letters found in every individual’s body.

So, you can imagine how tedious and complicated Vassy’s process was and why a lot of people found that to be incredibly pointless, especially since the adults in the study are all “healthy.” More importantly, the naysayers believed that this process would only bring unnecessary panic and anxiety to the subjects.

However, the results shocked them as 20% of the people tested positive for rare, life-threatening conditions that required immediate medical attention.

This prompted more experts to delve deeper into gathering genetic data sets in an effort to bolster the preventive power of genomics. This movement was supported by the National Institutes of Health in 2018 via their “All of Us” project, investing $27 million.

Meanwhile, a Harvard geneticist named George Church founded a similar organization called Nebula Genomics.

Basically, the idea behind precision medicine is very simple: Understanding how your genome works means knowing exactly how to “optimize” your body.

That means health professionals will be able to determine the perfect diet, perfect exercise routine, and of course, the perfect drugs for every patient. You’ll even learn the diseases your body is most susceptible to and how to prevent those.

At the moment, the biotechnology world only has a handful of companies focusing on precision medicine.

One of the leading biotechnology companies in this field is Illumina (ILMN), which focuses on DNA sequencing.

Utilizing its advanced machines, Illumina has been designing treatments to target specific cells in the human body -- and its efforts have been rewarded in recent years.

So far, Illumina stock has been up by 5,791% since its initial public offering back in 2000.

At the moment, Illumina practically controls approximately 80% of the next-generation sequencing space geared towards human genome analysis.

The key to its success is the company’s move to zero in on short-read data sequencing, which has been known as the cheapest, quickest, and most accurate service available in the market.

Since Illumina is one of the top movers in this field, it has easily become the top dog with a long waiting list of clients willing to pay tons of cash for the biotechnology firm’s machines.

While the machines definitely cost a lot upon purchase, Illumina actually earns more from the follow-up revenues generated from all the instances that a biotechnology or research laboratory uses the company’s technology to sequence a genome.

In 2019, Illumina earned $390 million in instrument revenue and $1.73 billion in consumables profit in the first three quarters alone.

Unfortunately, one of Illumina’s efforts to broaden its hold of the market failed.

The company opened 2020 to bad news as regulatory pressures pushed Illumina to shut down its plan to acquire its rival, Pacific Biosciences (PACB), for $1.2 billion.

While no particular reason was officially given by the reviewing bodies, reports indicate that the merger had been delayed due to fears of creating a monopoly.

Nonetheless, many consider this an odd excuse considering that Illumina’s supposed “monopoly” would actually compete directly with Roche (RHHBY).

For comparison, Roche’s market capitalization is $275 billion while Illumina is at $49 billion. In terms of revenue, Illumina earns $3.5 billion annually while Roche rakes in $56.8 billion.

Nevertheless, Illumina has decided to shrug off the rejection and move on to another potentially lucrative deal -- a 15-year partnership with another up and coming next-generation sequencing company: Qiagen (QGEN).

Initially thought to be a surefire acquisition candidate by Thermo Fisher Scientific (TMO) to the tune of $8 billion, Qiagen opted to reject the offer.

Instead, the smaller biotechnology firm has decided to focus on expanding its product portfolio. In the next five years, Qiagen estimates an earnings growth rate of roughly 9.1%.

Between Qiagen and Illumina, the former focuses more on individually customized treatments or “N-of-1 medicine.”

This has become even more pronounced following Qiagen’s acquisition of N-of-One, which raised $12.4 million in funding at the time, in January 2019.

N-of-One provides precision cancer care services. It offers clinical solutions like molecular interpretation to doctors and other healthcare professionals.

Apart from its partnership with Illumina, Qiagen also collaborates closely with NeoGenomics for cancer genetic testing services and DiaSorin for automated TB testing.

We’re in an era of remarkably personalized medical care.

With more and more genetic data made available for analysis, the rare diseases that boggled the minds of the healthcare industry are gradually becoming a thing of the past.

Now, we have access to tools that help with preventive measures to save us from the rare conditions that plagued our predecessors. If you really stop to think about it, targeted medicine just might be the key to immortality -- or at least to a significantly less disease-laden life.

If you’re looking to invest in Illumina or Qiagen stock (or both), the best thing to do is to take advantage of the next price drop.

Mad Hedge Biotech & Healthcare Letter

January 14, 2020

Fiat Lux

Featured Trade:

(CALIFORNIA JUMPS INTO THE DRUG BUSINESS)

(MYL), (TEVA), (RHHBY)