Mad Hedge Biotech and Healthcare Letter

July 30, 2024

Fiat Lux

Featured Trade:

(RETAIL THERAPY, MEET RETAIL RX)

(HUM), (WMT), (WBA), (UNH), (CVS), (TDOC)

Mad Hedge Biotech and Healthcare Letter

July 30, 2024

Fiat Lux

Featured Trade:

(RETAIL THERAPY, MEET RETAIL RX)

(HUM), (WMT), (WBA), (UNH), (CVS), (TDOC)

In my years of covering the markets, from the trading floors of Tokyo to the halls of power in Washington, I've seen my fair share of unexpected partnerships.

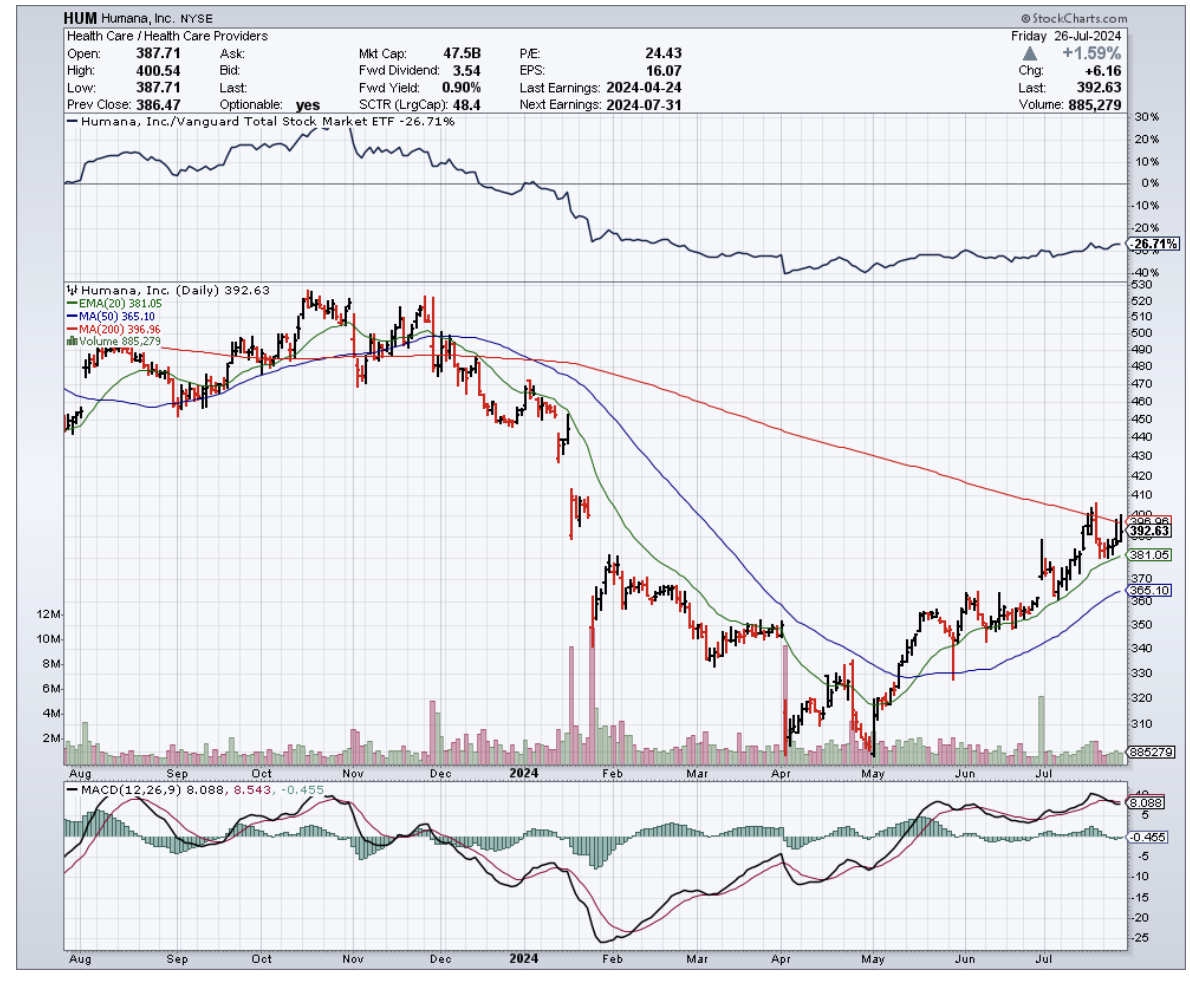

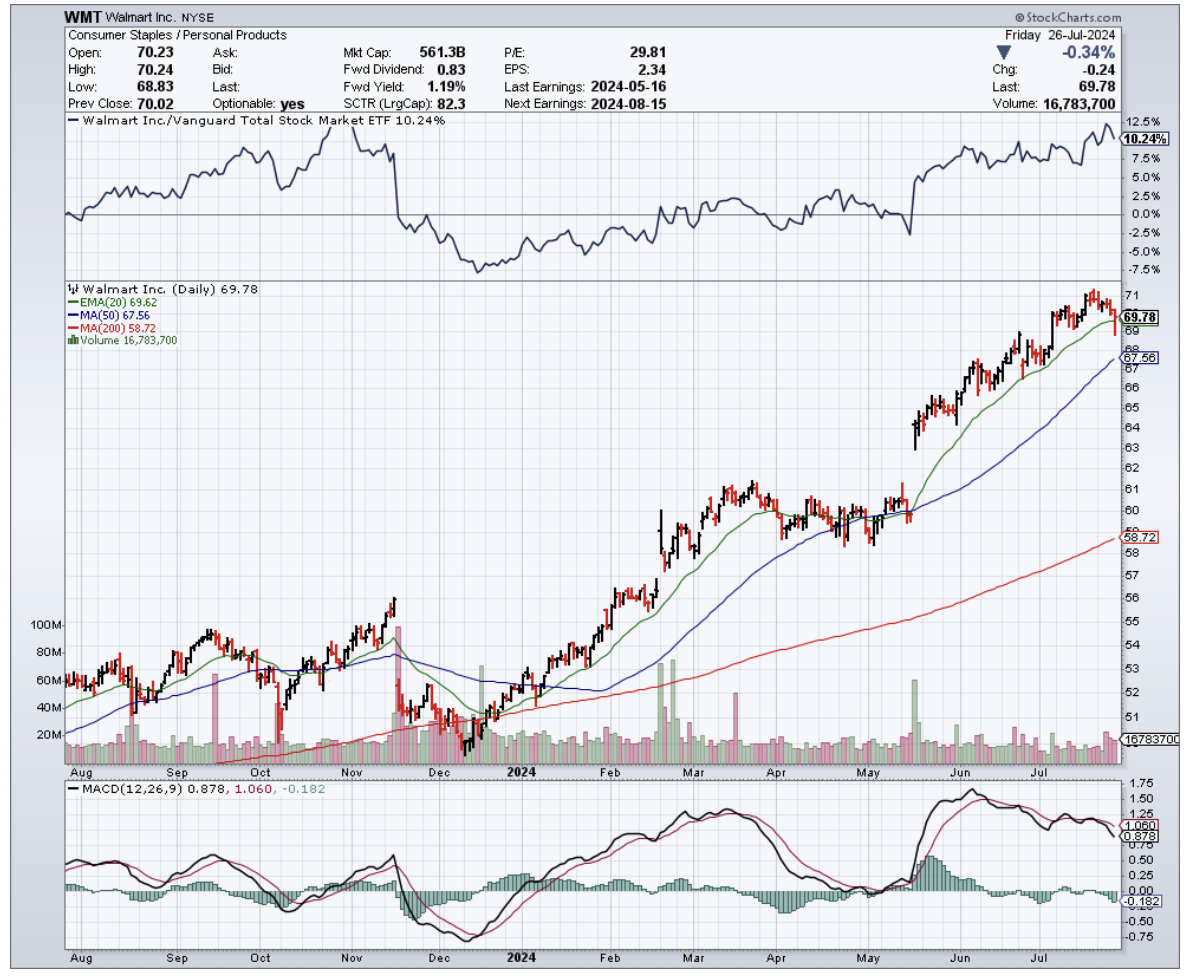

But the recent tie-up between Walmart (WMT) and Humana (HUM) has me sitting up and paying attention.

That’s right. Walmart, the king of rollbacks and home of the $1 hot dog, has found a new tenant for the vacant spaces that used to house its healthcare business: Humana's CenterWell health clinics.

Humana, as you know, is one of the biggest players in the Medicare Advantage game, and is setting up shop in 23 Walmart Supercenters across Florida, Georgia, Missouri, and Texas.

And they're not just dipping their toes in the water – they're diving in headfirst, with plans to have these clinics up and running by the first half of 2025.

Now, I know what you're thinking. "John, why should I care about some dusty old retail giant like Walmart getting into bed with a health insurance company?"

Let me tell you why.

Humana's Q1 2024 earnings were nothing to sneeze at, with revenues growing 11% year-over-year to a whopping $29.6 billion.

And while the company did revise its full-year EPS guidance downward, it maintained its outlook for adjusted EPS and even revised its membership growth in MA plans upward.

This is a big deal, folks. Medicare Advantage plans have been the bread and butter of Humana's business model, underpinning the company's phenomenal share price gains from $25 per share in 2010 to over $550 in late 2022.

With the population aging faster than fine wine, the demand for senior-focused healthcare services will only grow.

But Humana isn't the only one benefiting from this partnership.

For Walmart, renting out these spaces to CenterWell allows them to recoup some of the infrastructure investments they made in building out their 51 Walmart Health clinics, which they recently shut down due to profitability challenges.

It's like finding a roommate to help pay the rent after your startup goes belly up.

But the healthcare industry is like a giant game of Jenga, with players constantly pulling out blocks and hoping the whole thing doesn't come crashing down.

Just look at Walgreens Boots Alliance (WBA), another retail giant that recently announced the closure of 150 of its in-store clinics due to profitability challenges. It's a stark reminder of how difficult it can be to make a buck in this business.

That's why Walmart's pivot to a partnership model with Humana is so intriguing.

By leasing out pre-equipped facilities to CenterWell, Walmart is essentially letting Humana handle the nitty-gritty of patient care while still maintaining a presence in the rapidly growing primary care industry.

It's like having your cake and eating it too, without having to worry about the pesky details of actually baking the cake.

As expected, Walmart and Humana aren't the only ones making moves in the healthcare space.

CVS Health (CVS) and UnitedHealth Group (UNH) are also betting big on primary care, with CVS acquiring Oak Street Health for $10.6 billion and UnitedHealth's Optum division going on an acquisition spree to expand its network of physicians and healthcare providers.

Then, there’s the meteoric rise of telehealth during the pandemic. Companies like Teladoc Health (TDOC) saw their revenues skyrocket as patients turned to virtual care in droves.

While growth has slowed down since the height of the pandemic, telehealth is still a force to be reckoned with and could potentially disrupt traditional brick-and-mortar clinics.

So, what does all this mean for us?

Well, if you're an investor looking to get in on the action, you've got plenty of options. From established players like Humana and UnitedHealth to up-and-comers like Oak Street Health and Teladoc, there's no shortage of companies vying for a piece of the healthcare pie.

With an aging population, rising healthcare costs, and a growing focus on preventative care and chronic disease management, the demand for innovative healthcare solutions is only going to increase in the coming years.

And who knows, maybe one day we'll all be getting our annual check-ups at the local Walmart, with a side of low-priced toilet paper and a jumbo bag of Cheetos.

Stranger things have happened in the wild world of healthcare.

Mad Hedge Biotech and Healthcare Letter

January 25, 2024

Fiat Lux

Featured Trade:

(FROM BIG TO BIGGER)

(UNH), (CI), (ELV), (CVS)

Today, let's talk about where the smart money's at in our whirlwind economy – healthcare and insurance.

And who's the king of the hill in this game? None other than UnitedHealth Group (UNH).

It's not just any old company; it's a health insurance juggernaut that's been on a growth tear, doubling its value in just five years. That's definitely something to write home about.

With a market cap closing in at $500 billion and revenues of $372 billion in 2023, it's a force to be reckoned with. If it doubles again, we're looking at a $1 trillion giant. That's uncharted territory for healthcare stocks.

Before anything else, let's hop in our time machine for a sec.

Around 10 years back, UnitedHealth was a mere $75 billion baby. Fast forward to today, and it's ballooned to around half a trillion. We're talking about top-dog status in the healthcare world.

Now, let's get down to brass tacks. UnitedHealth's bottom line might not be the stuff of legends – a 6% profit margin over the past year.

But hold your horses – with over $300 billion in annual revenue, that 6% turns into a cool $18 billion-plus in profit.

And guess what? They've been raking in even more lately – $21.7 billion over four quarters.

"But will it double in value in a year or two?" you ask. Maybe not that fast, but hey, it's done it in five years before.

So, could UnitedHealth hit that mind-boggling $1 trillion mark by 2030? I wouldn't bet against it.

After all, UnitedHealth isn't just playing in the health insurance sandbox. It's the biggest kid in the playground – the largest health insurer in the United States and the biggest healthcare company globally.

For context, its closest peers are Cigna (CI) with $90.44 billion in market cap, Elevance (ELV) with $111.87 billion, and CVS (CVS) with $95.08 billion. You get the picture.

But here's the juicy part – UnitedHealth loves to shop. It's like the Pac-Man of healthcare, gobbling up companies left and right.

Just last year, it bagged Amedisys for a cool $3.3 billion, hot on the heels of its $5.4 billion acquisition of LHC Group. Talk about making moves.

Now, for my fellow investors, here's the sweetener: UnitedHealth also pays dividends, with a 1.4% yield. It might not sound like much, but this company's got a knack for growing dividends. It's like owning a golden goose that keeps laying more golden eggs.

So, what's the secret sauce for UnitedHealth potentially hitting that $1 trillion valuation? Simple – growth, growth, and more growth. It's not just selling insurance; it's into analytics and isn't shy about snapping up companies to beef up its portfolio.

Let's talk numbers. Management is eyeing an annual earnings growth somewhere between 13% and 16%. If UnitedHealth keeps hitting these home runs, its stock value climbing higher isn't just a possibility – it's a likelihood.

"But is it a good buy?" I hear you ask. Well, trading at around 23 times its earnings, it's a bargain compared to the average healthcare stock at 28 times earnings.

Simply put, this baby's got room to grow, and investors might just be willing to pay a premium for this gem.

So, when will it hit $1 trillion? If UnitedHealth sticks to the S&P 500 index's average 10% annual growth, we're looking at 2030 for that milestone.

But knowing UnitedHealth, which often outperforms the market, it could be sooner if it keeps up its projected annual growth rate.

In a nutshell, UnitedHealth Group isn't just a safe bet – it's a potential goldmine. With its continued growth, strategic acquisitions, and reasonable price tag, it's a shining star in any investment portfolio.

Mark my words – this is one stock that could make its investors very, very happy by 2030.

Mad Hedge Biotech and Healthcare Letter

December 5, 2023

Fiat Lux

Featured Trade:

(A UNION IN THE MAKING?)

(HUM), (CI), (CVS), (AET), (UNH)

The healthcare market was recently abuzz with the news of a potential mega-merger that sent shares of Humana (HUM) and The Cigna Group (CI) into a nosedive - 5.5% and 8.1% respectively. This news, centered around a transaction combining stocks and cash, could significantly reshape the healthcare landscape.

But let's not get ahead of ourselves. After all, in the world of healthcare mergers, certainty is as elusive as a mirage.

Still, if you’re feeling a sense of déjà vu, it’s because this isn’t the first time Humana and Cigna have danced around the idea of a merger.

Recall 2015 when Humana flirted with the idea of a merger with Cigna but ended up cozying up to Aetna (AET) – a union that never saw the light of day, thanks to the US courts.

A similar fate befell an attempted merger in 2017, when Elevance Health (ELV), then known as Anthem, tried to acquire Cigna for $48 billion, only to be blocked by the courts.

Since these previous attempts, both Humana and Cigna have significantly grown.

Prior to this market shake-up, Humana boasted a market capitalization of $62.87 billion, with Cigna commanding a higher ground at $83.77 billion.

But as history shows, regulatory skepticism often casts a long shadow over such ambitious plans, with fears of increased costs for the American public. This skepticism has extended to smaller deals, such as UnitedHealth Group's (UNH), which faced hurdles in their acquisition attempts.

Yet, the potential merger between these healthcare giants teases the possibility of substantial cost savings.

When giants unite, the promise of cost savings looms large. Redundancies in corporate functions like HR, investor relations, and executive positions offer low-hanging fruits for cost-cutting.

But the real cherry on top is the potential for operational synergies – cross-selling opportunities and leveraging infrastructure for efficient service delivery.

Humana's stronghold lies in its Insurance unit and CenterWell, with the latter, including pharmacy, provider services, and home solutions, contributing 16.3% of last year's revenue.

In contrast, Cigna wades into deeper waters, with its substantial revenue streams from pharmacy benefits and home delivery pharmacy businesses.

Now, let’s look at the companies in terms of revenue. A side-by-side of Humana and Cigna's revenues offers an intriguing picture.

Humana's Medicare Advantage revenues soared from $59.47 billion in 2020 to $72.89 billion in 2022.

Cigna, however, has only inched forward in this space. Humana's evident dominance in Medicare Advantage, with a market share of about 18%, contrasts sharply with Cigna's modest 2%.

Despite these differences, a merger isn't outside the realm of possibility.

For example, CVS (CVS) managed to successfully acquire Aetna for $69 billion back in 2018, with the two companies eventually turning into CVS Health.

While that merger proved that big deals could happen, the odds for Humana-Cigna are not exactly in Vegas betting territory.

Speculations about Cigna offloading its Medicare Advantage operations could make this merger more palatable to regulators, but it's far from a sure bet.

Another question to think about amidst these talks is why the market reacted like someone yelled “fire” in a crowded theater.

Well, it all boils down to the fear of overpayment.

Cigna, being larger, could potentially swallow Humana. But Humana, with its stronger financial health and market positioning, is seen as the more desirable entity.

The valuation metrics – price to earnings, price to adjusted operating cash flow, and EV to EBITDA – further complicate this perception, as Humana commands a premium.

With a potential merger announcement might be on the horizon, investors should approach this with a blend of skepticism and intrigue. The market is jittery, perceiving a possible merger as potentially detrimental to shareholder value.

However, should the merger succeed against the odds, the combined prowess of Humana and Cigna could spell a profitable future for investors. Knowing that the healthcare sector is never short of surprises, this potential merger, should it come to pass, could be one for the history books.

Mad Hedge Biotech and Healthcare Letter

October 19, 2023

Fiat Lux

Featured Trade:

(THE UNSUNG HERO OF PHARMA DISTRIBUTION)

(MCK), (CI), (UNH), (PFE), (MRK), (LLY), (NVO), (CAH), (COR)

McKesson (MCK) is the silent behemoth of the U.S. corporate world that's likely slipped under your radar. As the ninth-largest U.S. company by revenue, it doesn’t grab the headlines like some of its pharmaceutical peers. However, with a robust 22% stock gain this year alone, investors might want to sharpen their focus on this quiet achiever.

Now, you might mistake McKesson for a pharmacy benefit manager like Cigna Group's (CI) Express Scripts or UnitedHealth Group’s (UNH) OptumRx. But it doesn't stand shoulder-to-shoulder with pharmaceutical giants such as Pfizer (PFE) or Merck (MRK). Instead, its pivotal role ensures that prescription medications, consumed by a large fraction of Americans, reach their intended destinations.

Their operational model cuts through the noise: acquire medications from manufacturers and deliver them seamlessly to pharmacies. This spans local establishments and major national chains, including stalwarts like Walmart (WMT) and CVS Health (CVS).

Distributing medications is intricate. Not any logistics company can step up to the plate. These drugs, strictly governed by regulations, demand precision in handling and transit. Specific conditions are mandatory to retain their efficacy and, ultimately, their trust with consumers.

Newcomers in the pharmaceutical space, such as Ely Lilly’s (LLY) Mounjaro and Novo Nordisk’s (NVO) Ozempic, are set to further accelerate McKesson's growth trajectory. McKesson's operations, in tandem with Cardinal Health (CAH) and Cencora (COR)—the former AmerisourceBergen—underscore the dominance of this trio in the industry.

Given their consistent performance and notable market share, there's no mistaking their leadership. From an investor's lens, their well-established distribution networks translate to attractive returns.

The narrative enveloping McKesson has matured, particularly in the wake of the pandemic. Pre-COVID-19, the air was thick with concerns – potential drug price regulations, whispers about executive remuneration, and the ever-looming shadow of opioid liabilities.

In recent history, McKesson navigated tumultuous waters. They confronted their role in the opioid saga, culminating in a staggering $7.4 billion settlement spanning two decades. Such a settlement, rooted in claims of McKesson's hand in opioid distribution, marked a challenging chapter in the company's journey. But, like all resilient entities, they emerged with lessons and a sharper focus.

Refocusing on its core competency in drug distribution, the future projections for McKesson radiate optimism. Sales are on track for a 10% rise by fiscal 2024, aiming for the $304 billion mark. On the earnings front, a hike of 4.8% is forecasted, reaching $27.20 a share, followed by a notable ascent to 13.4% in fiscal 2025 – a jump to $30.84 a share.

While profit margins have hovered around the 4.8% range over half a decade, the company's cash flow paints a promising picture. With a robust $5 billion cash flow from the previous fiscal year, the announcement of a $6 billion share repurchase plan indicates a stronger, more liquid financial position.

McKesson’s journey, past and present, casts it as a promising investment, both for its operational prowess and its strategic repurchase blueprint. Examining its financial statements reveals a commendable reduction in net debt over the past triennium.

When McKesson is pitted against the likes of Cardinal and Cencora, optimism for its prospects feels natural. Projections indicate a growth rate between 12-14% in the years on the horizon, potentially crowning it as an industry vanguard. Valued at 15.6 times forward earnings, even if it inches above its five-year mean, the stock's appeal remains intact. Given its robust growth metrics, the stock seems a potential bargain, especially when juxtaposed with fellow S&P 500 members.

And there's more in the mix. With McKesson poised to ride the wave of prescription surges, particularly from premium medications like Ozempic, Wegovy, and Mounjaro, revenue streams seem destined for an upward course. A sentiment echoed by industry comrades, Cardinal and Cencora.

To encapsulate, in the expansive tableau of the pharmaceutical sector, where innovation meets timely delivery, McKesson etches its mark. As the healthcare matrix continues its evolution, especially in a world reshaped by a pandemic, the resilience and growth story of McKesson becomes hard to sidestep for the discerning investor. It's high time investors pivot their gaze towards this under-the-radar giant, poised for more milestones.

Mad Hedge Biotech and Healthcare Letter

August 3, 2023

Fiat Lux

Featured Trade:

(A FUTURE-PROOF INVESTMENT)

(UNH), (CI), (HUM), (CNC)

With a staggering market cap of $472 billion and a network reaching scores of policyholders, UnitedHealth Group (UNH) is an undisputed titan in the health insurance industry.

To put this into perspective, its competitors such as Cigna (CI), Humana (HUM), and Centene (CNC) have market caps of $86.42 billion, $56.64 billion, and $36.32 billion, respectively.

However, the past year witnessed a slight dip in UnitedHealth’s share price by 2%, which noticeably lags the broader market's return of 17%.

This raises a question: Is UnitedHealth’s investment appeal dwindling, or is it merely in a brief pause?

One can't discuss the health insurance sector without addressing the brewing storm of growth in its forecast. This sector is expected to welcome a turbocharged surge fuelled by an escalating burden of maladies and an expanding aging population worldwide.

The global landscape is witnessing a steep rise in various chronic afflictions - from cardiovascular and respiratory conditions to neurological disorders, cancer, musculoskeletal diseases, and diabetes. With the world population growing savvier about the financial cushioning health insurance provides, we're staring at a potential boom in this sector.

Take a gander at the numbers: The global health insurance industry was valued at a hefty USD 2.17 trillion in 2022.

Fast forward to 2032, and we're talking about a market swelling to an eye-watering USD 4.37 trillion. And with a projected CAGR of 7.3% from 2023 to 2032, we can safely say the health insurance express isn't slowing down anytime soon.

With this backdrop, let's dive into the compelling aspects of investing in UnitedHealth.

First, let's delve into the favorable aspects of investing in UnitedHealth. The core rationale is simple: healthcare is perennial. As long as human beings exist, healthcare will always be needed.

In the United States, individuals or their employers inevitably need to secure health insurance on a monthly basis. The constant evolution and improvement of healthcare services create a fertile ground for potentially substantial earnings in both the insurance and healthcare delivery sectors.

UnitedHealth, a veritable powerhouse, operates two key divisions - one specializing in health insurance and prescription coverage, and the other focused on healthcare provision. This dual-pronged approach has the potential to create sustained shareholder value.

Finding a flaw in this favorable proposition is challenging, particularly when examining the figures.

The company amassed an impressive $93 billion in revenue in the second quarter of 2023 alone, making it one of the world's largest corporations. It outperformed analysts' predictions of $91 billion, and the earnings per share of $6.14 surpassed Wall Street estimates of $5.99.

Although the company's medical care ratio did increase from 81.5% to 83.2% as expected, this was offset by a robust revenue growth that outpaced the rise in medical and operational costs.

UnitedHealth provides insurance to over 51 million individuals, with an addition of over a million new policyholders in 2023. UnitedHealth's scale allows it to keep costs low, forming a formidable entry barrier for new market contenders.

Moreover, its quarterly revenue experienced a notable 63% increase over the past five years, hinting at significant growth potential. This suggests that UnitedHealth's future growth prospects remain robust.

Straight from the company itself, UnitedHealth anticipates growing its earnings per share (EPS) between 13% and 16% annually. Moreover, the company has shown consistent dividend growth, with an annual increase of 10% since 2010.

This indicates a company that excels in operating its business model over time, suggesting potential stability and growth in both share price and dividends.

One key strategy of UnitedHealth is its diverse portfolio, developed over the years through strategic acquisitions like home health company LHC Group and analytics firm Change Healthcare. This diversity has allowed the company to maintain a growth rate exceeding 10% over the last five years.

UnitedHealth's most significant growth driver remains its premiums, but the company also saw an additional $2 billion in revenue from services and $1.2 billion from product sales last quarter.

Although it faces potential increases in medical costs, the company's diversified portfolio helps it maintain strong profit growth, with adjusted earnings per share rising 10% to $6.14 year-on-year.

Despite the overall positive outlook, it's worth noting that UnitedHealth's shares have decreased by about 4% this year. While the stock is trading at 23 times trailing earnings, slightly below the healthcare industry average of 25, the company's consistent growth could justify a higher valuation.

Overall, UnitedHealth remains a promising investment in the long run despite some short-term volatility, as it offers a blend of stability and growth. It may well be a stock worth considering for those looking for a long-term hold in the healthcare sector. I suggest you buy the dip.