Whale, Whale, Whale.....What Do We Have Here?

I remember watching Tokyo whales quietly accumulate positions in beaten-down industrials in late 1992 while every gaijin investor was sprinting for the exits.

The Nikkei had already cratered 60%, and the newspapers were full of obituaries for the Japanese miracle.

Three years later, those patient accumulators had doubled their money. The lesson wasn't specific to Japan. It never is.

Which brings me to Ethereum (ETH).

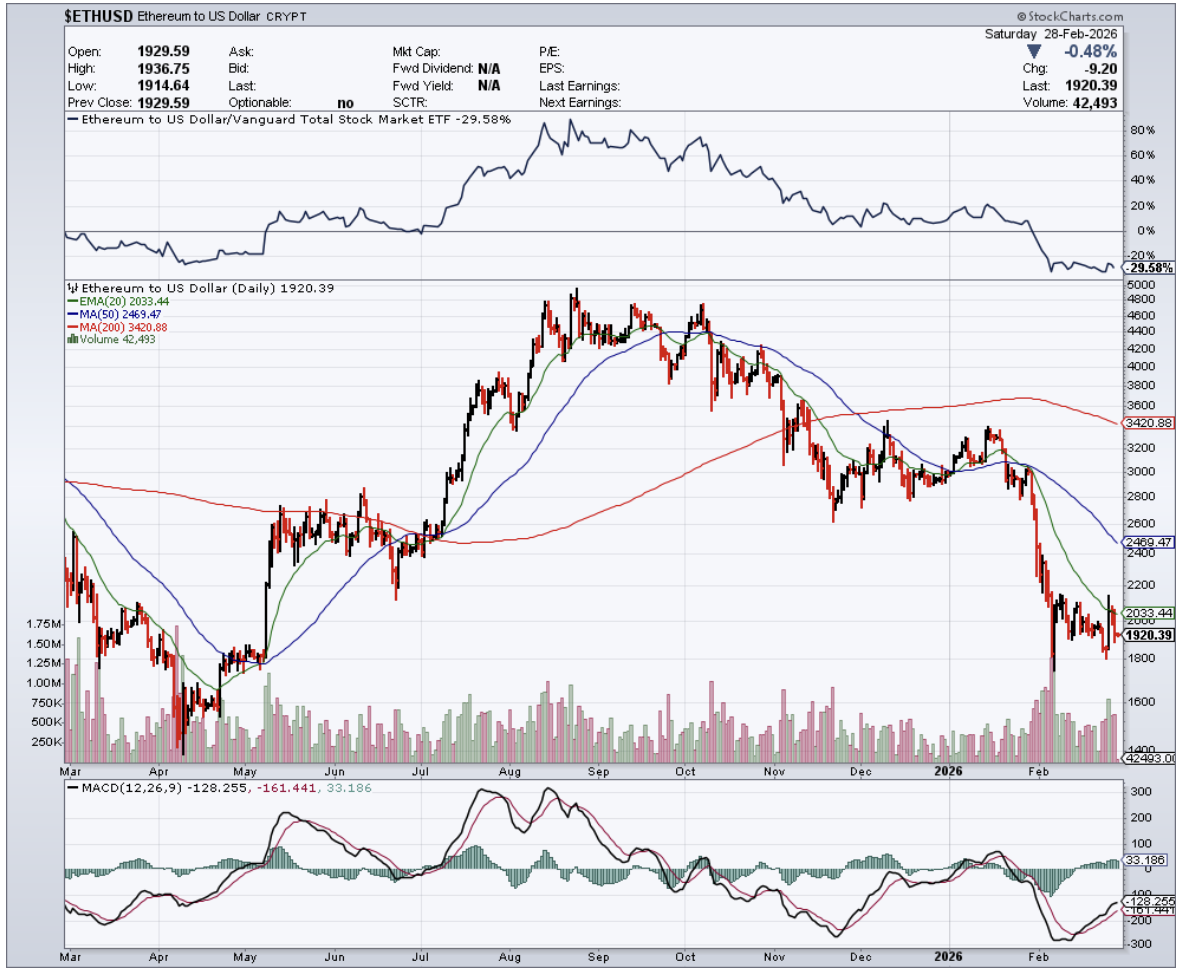

ETH has recently posted its sixth consecutive weekly loss, the longest uninterrupted downtrend since the brutal 10-week drawdown from March to June 2022.

The Crypto Fear & Greed Index has been pinned in Extreme Fear territory for most of the month. Vitalik sold. Miners sold.

Trump rattled global markets with a 15% global tariff increase that sent Bitcoin (BTC) below $65,000 and had the Federal Reserve's rate-cut timeline quietly sliding toward irrelevance. On the surface, it looks like a crime scene.

Beneath the surface is where it gets interesting.

On Binance, the average ETH whale sell order size has dropped from 2,250 ETH in early January to 1,350 ETH in recent weeks. That's not a subtle shift.

Large holders are withdrawing from the sell side - not because they've gone neutral, but because they're busy doing something else.

The realized price curve of ETH-accumulating whale addresses has bent downward for the first time, which in plain English means these holders aren't selling into weakness.

They're buying more, pulling their average cost basis lower. Balances have surged, and realized cap has increased in precisely the price zones where retail sentiment is most catastrophic.

That's accumulation, not capitulation.

The macro backdrop provided excellent cover for the panic. Trump's pivot to Trade Act Section 122 after the Supreme Court struck down his earlier tariff authorities caught markets flat-footed on February 23rd and 24th.

The resulting inflation fears did what they always do - they hammered high-beta assets first and asked questions later. Cryptocurrency, leveraged to global liquidity conditions, took the hit squarely.

Regulatory hope evaporated on roughly the same timeline.

The Clarity Act, which had been trading at an 82% probability of passage on prediction markets just weeks earlier, collapsed to around half that within three days as Senate negotiations stalled over stablecoin reward provisions.

Institutional desks don't wait around for legislative clarity that isn't coming. They de-risk, and they did.

The project-specific catalysts added fuel. Vitalik Buterin sold 1,869 ETH for approximately $3.67 million over two days in late February, part of a pre-announced plan from January to allocate 16,384 ETH toward Ethereum ecosystem initiatives.

The sales were transparent and strategic. The market's 5% reaction to them was neither.

Meanwhile, Bitcoin miner Bitdeer (BTDR) liquidated its entire self-mined BTC treasury (roughly 1,133 coins for $62 million) to fund a pivot toward AI cloud infrastructure.

Cango (CANG) followed the same playbook in early February, selling 4,451 BTC for $305 million.

The mining industry's exodus from Bitcoin treasuries into data center land is a structural shift worth watching.

Then there's the Jane Street story, which exploded across crypto circles this month and deserves more than a dismissive wave.

Since late 2024, Bitcoin has experienced sharp sell-offs clustering around 10 am Eastern, a pattern the community dubbed the "10 am dump."

A viral long-form post on X argued that Jane Street, operating as an Authorized Participant for BlackRock's (BLK) IBIT and other spot ETFs, was programmatically selling Bitcoin at market open to drive spot prices lower, then accumulating ETF shares at a discount - a structural arbitrage made possible by their privileged access to the ETF creation and redemption mechanism.

The post pointed to Jane Street's Q4 2025 13F filings showing $790 million in IBIT holdings, suggesting those long positions were hedged or net short through undisclosed derivatives.

The theory holds that without this daily suppression, Bitcoin would already be trading above $150,000. That's an extraordinary claim, and extraordinary claims require more than a 13F filing and a pattern of morning selloffs.

But the timing is genuinely strange: following a federal lawsuit in February from Terraform Labs' bankruptcy administrator accusing Jane Street of insider trading tied to the 2022 Terra collapse, the 10 am dump pattern stopped.

Bitcoin staged a sharp V-shaped rebound. Correlation isn't causation, but it's enough to keep a lawyer busy and a trader alert.

The practical question for ETH holders is what the whale accumulation data is signaling about the timeline. Bottoming processes are rarely clean.

The 2022 analog that everyone is reaching for ended with a cycle low before stabilization - it didn't bounce straight from the sixth weekly loss. Patience remains the operative word, and the on-chain data suggests the smart money has plenty of it.

The Tokyo whales of 1992 weren't smarter than everyone else. They were just less impressed by the headlines.