Featured Trade: (JULY 6 GLOBAL STRATEGY WEBINAR), (MY BRIEFING FROM THE JOINT CHIEFS OF STAFF), (CGW), (PHO), (RSX), (GOOGL), (CSCO), (FXI), (XLK), (WHY THE JGB MARKET MAY BE READY TO COLLAPSE), (FXY), (YCS), (DXJ)

Guggenheim S&P Global Water ETF (CGW) PowerShares Water Resources ETF (PHO) VanEck Vectors Russia ETF (RSX) Alphabet Inc. (GOOGL) Cisco Systems, Inc. (CSCO) iShares China Large-Cap (FXI) Technology Select Sector SPDR ETF (XLK) CurrencyShares Japanese Yen ETF (FXY) ProShares UltraShort Yen (YCS) WisdomTree Japan Hedged Equity ETF (DXJ)

I have always considered the US military to have one of the world?s greatest research organizations. The frustrating thing is that their ?clients? only consist of the President and a handful of three and four star generals.

So I thought that I would review my notes from a dinner I had with General James E. Cartwright, the former Vice Chairman of the Joint Chiefs of Staff, who is known as ?Hoss? to his close subordinates.

Meeting the tip of the spear in person was fascinating. The four star Marine pilot was the second highest ranking officer in the US armed forces and showed up in his drab green alpha suit, his naval aviator wings matching my own, and spit and polished shoes.

As he spoke, I was ticking off the stock, ETF and futures plays that would best capitalize on the long term trends he was outlining.

The cycle of warfare is now driven by Moore?s Law more than anything else (XLK), (CSCO) and (PANW). Peer nation states, like Russia, are no longer the main concern.

Historically, inertia has limited changes in defense budgets to 5%-10% a year, but in 2010 defense secretary Robert Gates pulled off a 30% realignment, thanks to a major management shakeup. We can only afford to spend on winning current conflicts, not potential future wars. No more exercises in the Fulda Gap.

The war on terrorism will continue for at least 4-8 more years. Afghanistan is a long haul that will depend more on cooperation from neighboring Iran and Pakistan. ?We?re not going to be able to kill our way or buy our way to success in Afghanistan,? said the general.? However, the 30,000-man surge there brought a dramatic improvement on the ground situation.

Iran is a big concern and the strategy there is to interfere with outside suppliers of nuclear technology in order to stretch out their weapons development until a regime change cancels the whole program.

Water (PHO), (CGW) is going to become a big defense issue, as the countries running out the fastest, like Pakistan and the Sahel, happen to be the least politically stable.

Cyber warfare is another weak point, as excellent protection of .mil sites cannot legally be extended to .gov and .com sites.?

We may have to lose a few private institutions in an attack to get congress to change the law and accept the legal concept of ?voluntarism.? General Cartwright said ?Anyone in business will tell you that they?re losing intellectual capital on a daily basis.??

The START negotiations have become complicated by the fact that for demographic reasons, Russia (RSX) will never be able to field a million man army again, so they need more tactical nukes to defend against the Chinese (FXI).? The Russians are trying to cut the cost of defending against the US, so they can spend more on defense against a far larger force from China.

I left the dinner with dozens of ideas percolating through my mind, which I will write about in future letters.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/07/General-James-Cartwright.jpg388313Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-07-01 01:07:432016-07-01 01:07:43My Briefing from the Joint Chiefs of Staff

When I first arrived in Japan in 1974, international investors widely expected the country to collapse, a casualty of the overnight quadrupling of oil prices from $3 per barrel to $12, and the global recession that followed.

Japanese borrowers were only able to tap foreign debt markets by paying a 200 basis point premium to the market, a condition that came to be known as ?Japan Rates.?

Hedge fund manager, Kyle Bass, says that the despised Japan rates are about to return. There is nothing less than one quadrillion yen of public debt in Japan today.

A perennial trade surplus powered high corporate and personal savings rates during the eighties and nineties, allowing these agencies to sell their debt entirely to domestic, mostly captive investors.

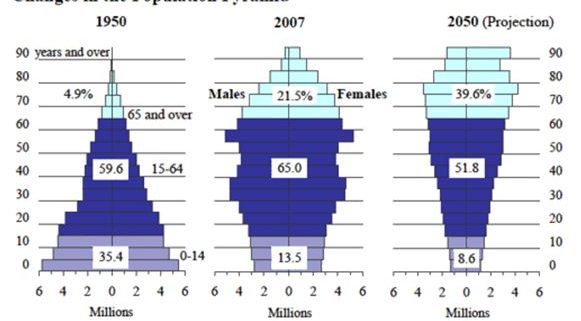

Those days are coming to a close. The problem is that the working age population in Japan has peakedd, and the country is entering a long demographic nightmare (see population pyramids below).

This year, the Ministry of Finance will see ?40 trillion in receivables, the same figure seen in 1985, against ?97 trillion in spending. Interest expense, debt service, and social security spending alone exceed receivables.

The tipping point is close, and when it hits, Japan will have to borrow from abroad in size. Foreign investors all too aware of this distressed income statement will almost certainly demand big risk premiums, possibly several hundred basis points. That?s when the sushi hits the fan.

To top it all, no one in living memory in Japan has ever lost money in the JGB market, so expectations are unsustainably high.

Both the JGB market and the yen can only collapse in the face of these developments. I know that the short JGB trade has killed off more hedge fund managers than all the irate former investors and divorce lawyers in the world combined.

But what Kyle says makes too much sense and the day of reckoning for this long despised financial instrument may be upon us. How much downside risk can there be in shorting a ten-year coupon of negative -0.11%?

Is Kyle trying to show us the writing on the wall?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/07/Population-Pyramid-chart.jpg403581Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-07-01 01:06:232016-07-01 01:06:23Why the JGB Market May Be Ready to Collapse

?Free choice is not relevant in financial markets because there are too many players. A stock with a million holders is much more predictable than one with five.? said Charles Nenner, of Charles Nenner Research in Amsterdam.

https://www.madhedgefundtrader.com/wp-content/uploads/2011/12/dice.jpg127127Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-07-01 01:05:432016-07-01 01:05:43July 1, 2016 - Quote of the Day

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.