Global Market Comments

January 26, 2026

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or TACO RIDES AGAIN!),

(SPY), ($INDU), (GLD), (B), (NEM), (GDX), (GS), (TLT), (KO), (CSCO), (MDLZ), (TAN), (BA), (MOS), (IPI), (MU)

Global Market Comments

January 26, 2026

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or TACO RIDES AGAIN!),

(SPY), ($INDU), (GLD), (B), (NEM), (GDX), (GS), (TLT), (KO), (CSCO), (MDLZ), (TAN), (BA), (MOS), (IPI), (MU)

?It is difficult to get a man to understand something when his salary depends upon his not understanding it.? said the Pulitzer Price winning author, Upton Sinclair.

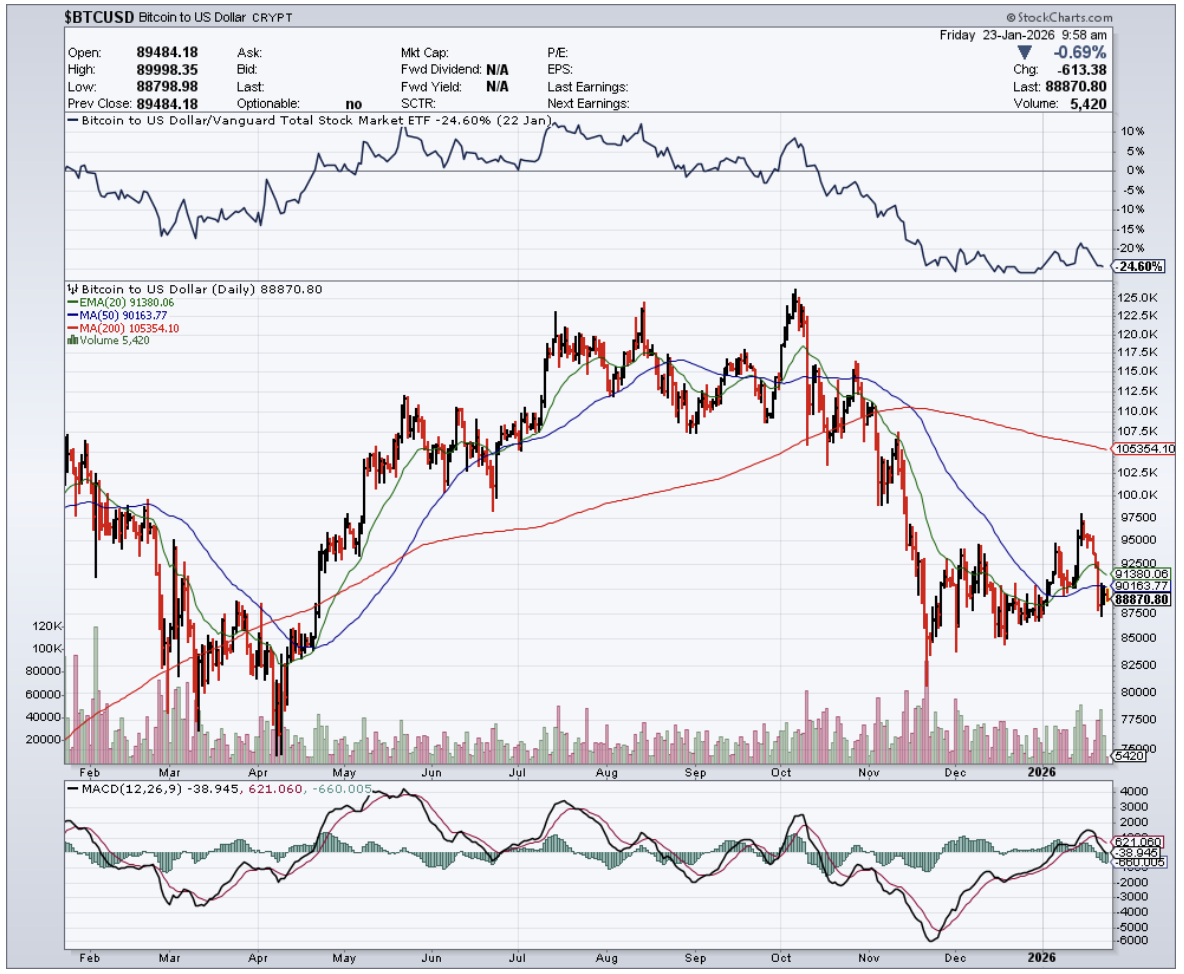

Bitcoin lately has been resting, and the good thing is, it hasn’t been overly choppy.

After reaching prior cycle highs, it retraced into a broad consolidation range that reflects digestion rather than exhaustion, and that is a sign of things to come.

We are well past the era of large-scale asset purchase programs, and many outsiders expected the transition away from ultra-loose monetary policy to be disorderly.

That has not been the case.

Orderly normalization matters for an inherently volatile asset like Bitcoin, and so far, that is largely what markets have experienced.

Inflation readings have established a clear upper bound relative to earlier peaks, and as subsequent data settled into a lower but still elevated range, Bitcoin’s long-term narrative remained intact rather than impaired.

As the price of Bitcoin has persistently maintained levels well above prior-cycle ranges, the talking heads and diva hedge fund managers have largely stopped questioning its legitimacy.

It’s about time.

That shift represents a meaningful validation milestone for the asset class.

At a broader level, the Federal Reserve remains constrained.

Each policy path carries trade-offs, and most of them are structurally favorable to scarce, non-sovereign assets. The primary risk remains a loss of confidence driven by uncontrolled inflation, which would destabilize the U.S. dollar itself.

Conversely, periods of renewed liquidity support or slower-than-expected tightening continue to reinforce Bitcoin’s role as a hedge against monetary debasement.

Inflation ultimately proved more persistent than initially described, and that persistence has gradually eroded confidence in central banks’ ability to fine-tune outcomes. That erosion continues to benefit Bitcoin’s positioning as a long-duration alternative asset.

Liquidity-driven moves in Bitcoin have increasingly followed a familiar pattern of anticipation followed by consolidation rather than violent reversals.

High inflation surprises that once would have caused panic selling now tend to reinforce Bitcoin’s perceived store-of-value characteristics over longer horizons.

Sometimes markets still need to take one step back to move two steps forward.

Risk-off reactions driven by currency strength and macro uncertainty continue to weigh on speculative assets in the short term, but those reactions have become more contained than in earlier cycles.

Doubts about inflation being temporary have long since faded, and the market has broadly accepted that a structural shift in the global economic backdrop is underway.

Another knock-on effect has been recurring concerns about stagnating growth paired with elevated inflation, a combination that complicates capital deployment across traditional assets.

That environment makes it psychologically harder for investors to commit aggressively to large alternative investments, including real estate, during periods of uncertainty.

This helps explain extended consolidation phases rather than decisive breakouts in either direction.

On a constructive note, the supply of bitcoin held on exchanges remains structurally lower than in prior cycles, suggesting a continued preference among investors to self-custody rather than keep coins readily available for sale.

That behavior aligns with a market in observation mode rather than distribution.

Long-term holders continue to represent a dominant share of total supply, and their reluctance to sell has become a defining feature of Bitcoin’s maturity.

Short-term consolidation phases have repeatedly given way to renewed trend moves once macro uncertainty clears or stabilizes.

At the household level, the case for holding Bitcoin has strengthened rather than weakened.

Living costs remain elevated across energy, housing, food, transportation, and other essentials, reinforcing awareness of currency debasement among everyday consumers.

Against that backdrop, Bitcoin continues to be viewed by many as a hedge against long-term monetary erosion rather than a short-term trading vehicle.

Interest-rate expectations now shift incrementally rather than violently, and markets have adapted to a world where higher rates do not automatically invalidate the Bitcoin thesis.

A measured approach to policy normalization has reduced the shock factor that once triggered sharp selloffs.

A move of this magnitude would have produced far deeper drawdowns in earlier years. Instead, Bitcoin has increasingly absorbed macro stress while maintaining structural support.

That resilience remains one of the strongest signals that Bitcoin has evolved beyond a purely speculative asset and into a durable component of the global financial landscape.

Global Market Comments

January 23, 2026

Fiat Lux

Featured Trade:

(THE KINDLE EDITION OF THE JOHN THOMAS BIO IS OUT)

'If you can get a dividend higher than the yield on ten-year debt, it's an opportunity we haven't seen in our lifetime. On a five-year horizon, investing in large multinationals with high dividends will have a large payday' said Lawrence Fink, CEO of Black Rock.

If you want to insulate yourself from the daily gyrations of cryptocurrency but still gain exposure to the economic infrastructure that supports it, there is a clear historical lesson in the rise and collapse of Silvergate Capital Corporation (SICPQ).

You never needed to open a cold wallet or custody a digital asset to participate in what Silvergate represented. The company, through Silvergate Bank, operated as a regulated U.S. bank providing fiat services to cryptocurrency exchanges, brokers, and institutional investors. It held a full bank charter and positioned itself not as a speculative crypto participant, but as financial plumbing for the digital asset economy.

For several years, that positioning appeared durable. Digital assets embedded themselves into global markets, and demand for compliant fiat on-ramps and off-ramps expanded alongside them. Silvergate built its franchise around this demand, offering real-time U.S. dollar settlement between crypto exchanges and institutional counterparties through its proprietary payments network. As participation increased, liquidity clustered inside the system, reinforcing customer dependence and operational stickiness.

Deposit growth followed industry expansion. Institutional crypto firms maintained large, non-interest-bearing balances to support trading, custody, and settlement activity. Those deposits funded securities portfolios and lending activity tied to crypto markets, producing strong net interest income during periods of market stability. The model worked as long as confidence held and liquidity remained abundant.

The vulnerability emerged from concentration. Silvergate’s funding base was overwhelmingly composed of crypto-related deposits that were uninsured, institutional, and highly sensitive to market stress. When confidence in centralized crypto intermediaries weakened, deposit outflows accelerated. Meeting those withdrawals required selling securities into unfavorable market conditions, eroding capital, and compressing liquidity in a self-reinforcing cycle.

The bank’s exposure was compounded by leverage products secured by digital asset collateral. While structurally conservative by traditional banking standards, these products intensified balance sheet sensitivity during periods of volatility. The same mechanisms that once amplified growth compressed margins and capital when market conditions reversed.

Competition did not arrive in the form many anticipated. Large financial institutions such as JPMorgan Chase (JPM) and Morgan Stanley (MS) did not need to aggressively fund crypto markets to exert pressure. Their diversified funding, deep liquidity, and regulatory insulation allowed them to wait while specialists absorbed sector-specific risk.

At its peak, Silvergate serviced a broad network of crypto-native and institutional firms, including Binance.US, Coinbase (COIN), Fidelity Digital Assets, PayPal (PYPL), and CME Group (CME). These relationships reflected genuine demand for crypto-aligned banking infrastructure, but they did not immunize the institution from systemic liquidity risk.

Silvergate ultimately exited the banking system through voluntary liquidation, ending its role as a crypto-focused financial intermediary. The broader digital asset market persisted. Banking services reallocated. Infrastructure adapted.

As of 2026, the lesson is not that crypto banking lacks demand, but that demand alone does not confer durability. Financial institutions whose balance sheets are tightly coupled to a single volatile sector must manage liquidity, concentration, and confidence with exceptional discipline. When those elements fail to align, network effects reverse as efficiently as they once compounded.

Silvergate’s legacy now sits as a structural case study in how regulated finance intersects with digital asset markets, and where that intersection can fracture under stress.

Global Market Comments

January 22, 2026

Fiat Lux

Featured Trade:

(FRIDAY, FEBRUARY 13, 2026 ANTARCTICA STRATEGY LUNCHEON)

(A CHEAP HEDGE FOR THIS MARKET),

($VIX), (VXX), (SPY), (GS), (GLD)

“Incentive structures work, so you have to be very careful about what you incent people to do because various incentive structures create all sorts of consequences which you can’t anticipate,” said Apple founder Steve Jobs.

Come join me for lunch at the Mad Hedge Fund Trader’s Global Strategy Luncheon, which I will be conducting in Buenos Aires, Argentina on Friday, January 30, 2026. The cost of the luncheon will be $247.

An excellent meal will be followed by a wide-ranging discussion and an extended question-and-answer period. I will also discuss the results of two weeks of my research in Argentina’s capital city.

I’ll be arriving early and leaving late in case anyone wants to have a one-on-one discussion or just sit around and chew the fat about the financial markets.

The lunch will be held at an exclusive downtown Buenos Aires hotel. The precise location will be emailed with your purchase confirmation.

I look forward to meeting you, and thank you for supporting my research.

To purchase tickets for the luncheons, please click here.