Global Market Comments

February 20, 2026

Fiat Lux

Featured Trade:

(TRADE ALERT - (PANW) – BUY LEAPS)

Global Market Comments

February 20, 2026

Fiat Lux

Featured Trade:

(TRADE ALERT - (PANW) – BUY LEAPS)

Global Market Comments

February 19, 2026

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

You can count on a bear market hitting sometime in 2038, one falling by at least 25%.

Worse, there is almost a guarantee that a financial crisis, severe bear market, and possibly another Great Depression will take place no later than 2058, which would take the major indexes down by 50% or more.

No, I have not taken to using a Ouija board, reading tea leaves, or examining animal entrails in order to predict the future. It’s much easier than that.

I simply read the data just released from the National Center for Health Statistics, a subsidiary of the federal Centers for Disease Control and Prevention (click here for their link).

The government agency reported that the US birth rate fell to a new all-time low for the second year in a row, to 60.2 births per 1,000 women of childbearing age. A birth rate of 125 per 1,000 is necessary for a population to break even. The absolute number of births is the lowest since 1987. In 2017, women had 500,000 fewer babies than in 2007.

These are the lowest numbers since WWII, when 17 million men were away in the military, a crucial part of the equation.

Babies grow up, at least most of them. In 20 years, they become consumers, earning wages, buying things, paying taxes, and generally contributing to economic growth.

In 45 years, they do so quite substantially, becoming the major drivers of the economy. When these numbers fall, recessions and bear markets occur with absolute certainty.

You have long heard me talk about the coming “Golden Age” of the 2020’s. That’s when a two-decade-long demographic tailwind ensues because the number of “peak spenders’ in the economy starts to balloon to generational highs. The last time this happened during the 1980’s and 19990’s stocks rose 20-fold.

Right now, we are just coming out of two decades of demographic headwind, when the number of big spenders in the economy reached a low ebb. This was the cause of the Great Recession, the stock market crash, and the anemic 2% annual growth since then.

The reasons for the maternity ward slowdown are many. The Great Recession certainly blew a hole in the family plans of many Millennials. Falling incomes always lead to lower birth rates, with many Millennial couples delaying children by five years or more. Millennial mothers are now having children later than at any time in history.

Burgeoning student debt, which just topped $1.5 trillion, is another. Many prospective mothers would rather get out from under substantial debt before they add to the population.

The rising education of women is another drag on childbearing and is a global trend. When spouses become serious wage earners, families inevitably shrink. Husbands would rather take the money and improve their lifestyles than have more kids to feed.

Women are also delaying having children to postpone the “pay gaps” that always kick in after they take maternity leave. Many are pegging income targets before they entertain starting families.

As a result of these trends, one in five children last year was born to women over the age of 35, a new high.

This is how Latin Americans moved from eight to two-child families in only one generation. The same is about to take place in Africa, where standards of living are rising rapidly, thanks to the eradication of several serious diseases.

The sharpest falls in the US have been with minorities. Since 2017, the birth rates for Hispanics have dropped by 27% from a very high level, African Americans 11%, whites 5%, and Asian 4%.

Europe has long had the same problem with plunging growth rates, but only much worse. Historically, the US has made up for the shortfall with immigration, but that is now falling thanks to the current administration's policies. Restricting immigration now is a guarantee of slowing economic growth in the future. It’s just a numbers game.

So watch that growth rate. When it starts to tick up again, it’s time to buy….in about 20 years. I’ll be there to remind you with this newsletter.

As for me, I’ve been doing my part. I have five kids aged 15-34, and my life is only half over. Where did you say they keep the Pampers?

I’m Doing My Part

“It’s easier to get out of Cuba than to get out of Facebook,” said a market analyst.

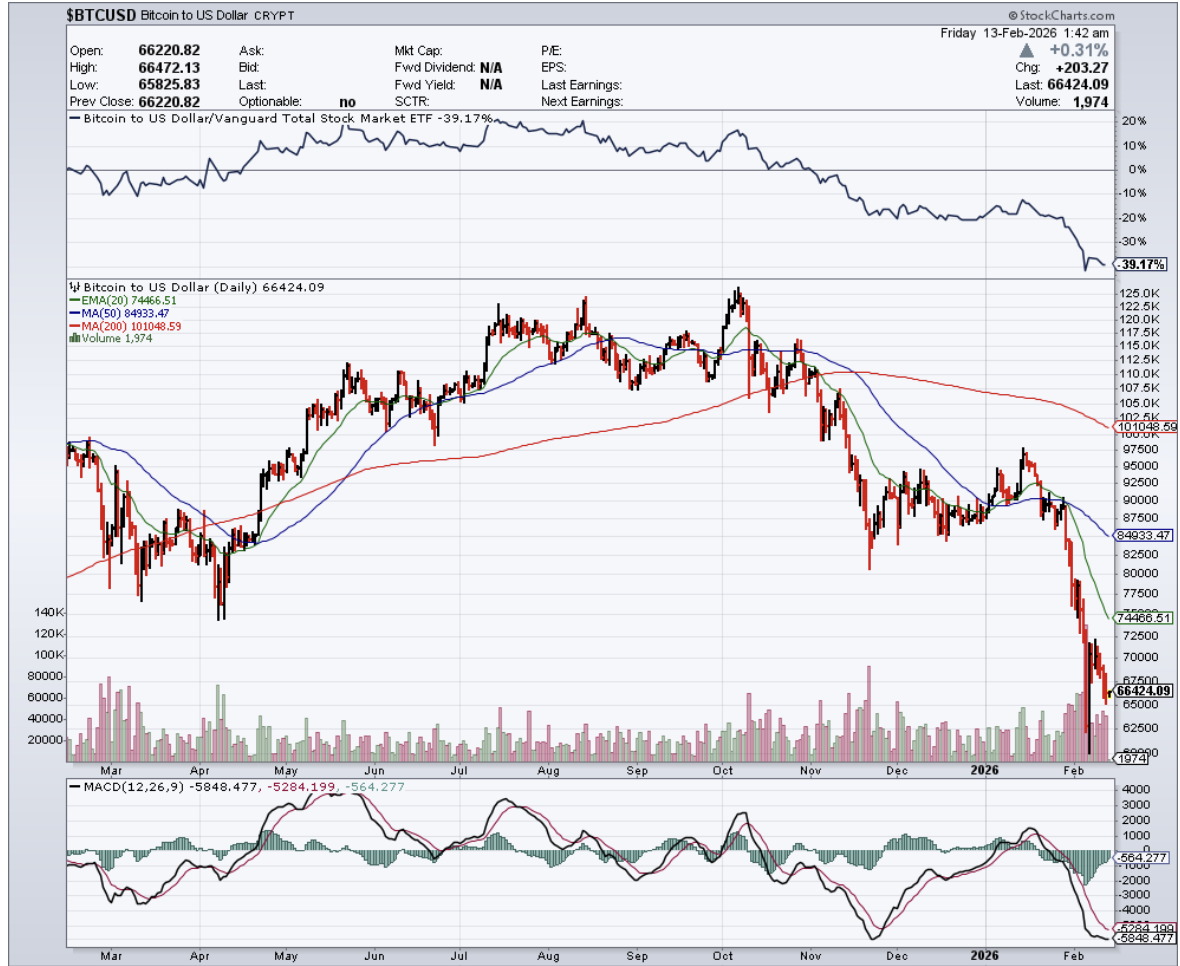

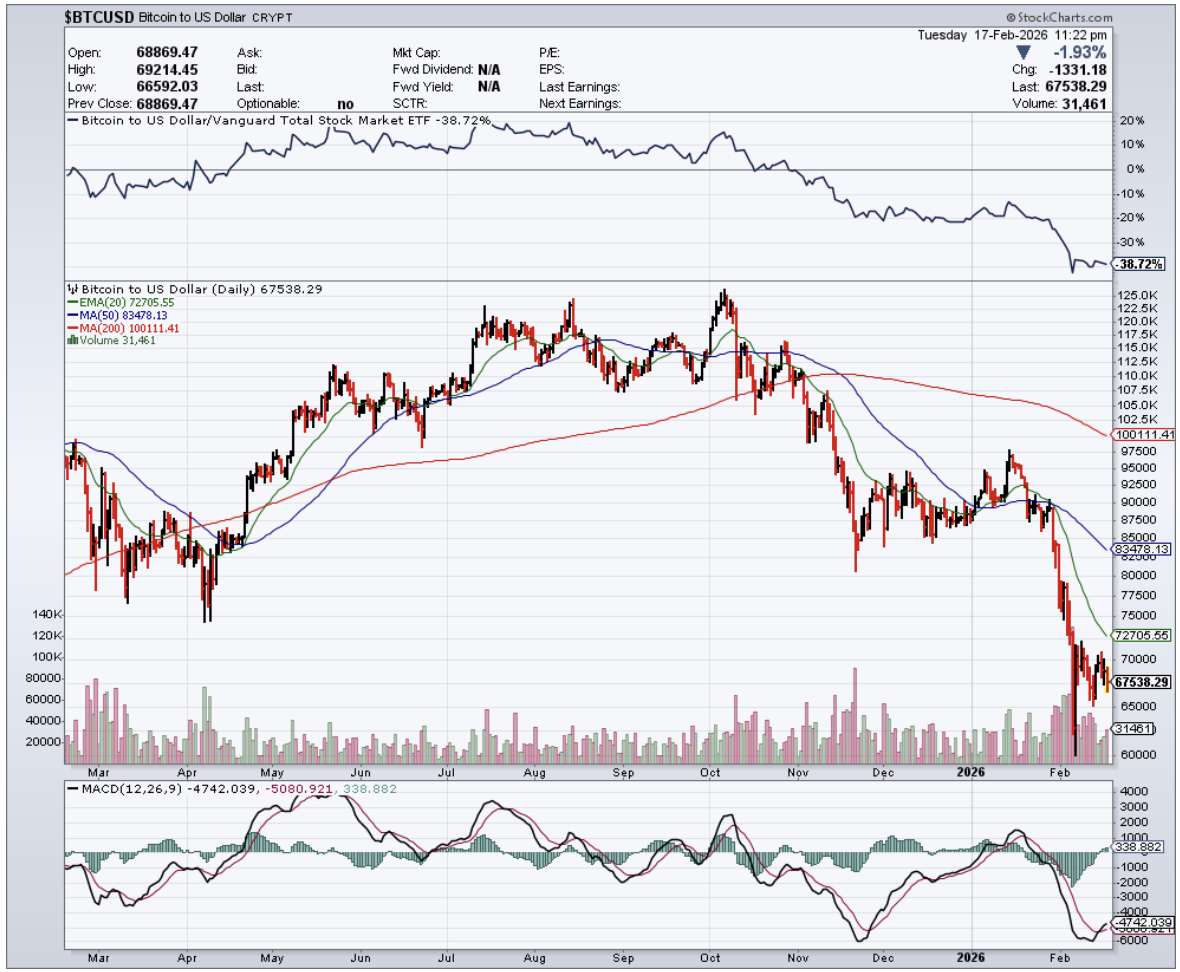

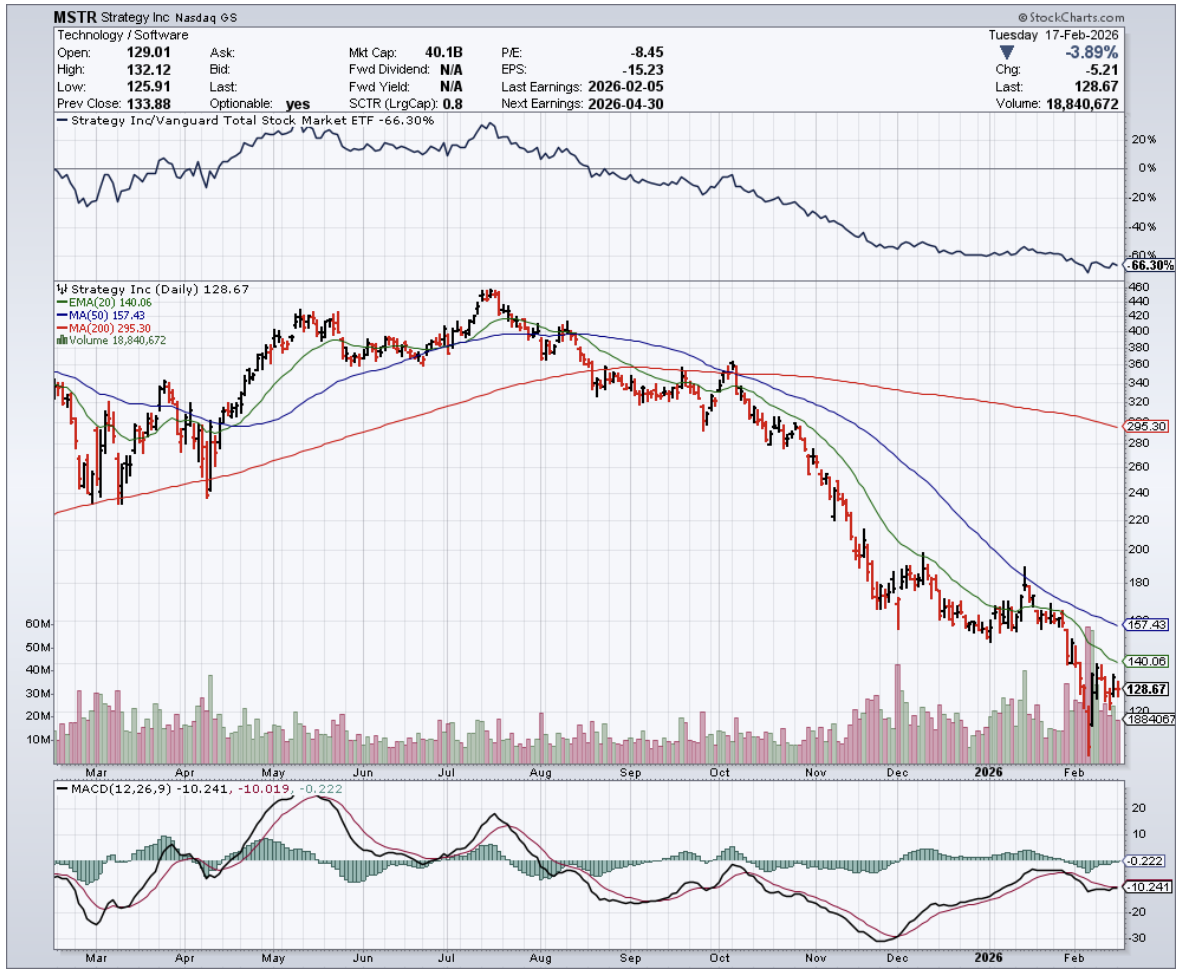

Strategy's (MSTR) carrying $8.2 billion in debt, most of it convertible, with $2.25 billion in cash reserves and over 714,000 Bitcoin (BTC) on the balance sheet.

The CEO says Bitcoin would need to drop to $8,000 and sit there for five years before they'd have a real problem.

The bears say this is a leveraged disaster waiting to implode. The bulls say it's genius financial engineering. I say the numbers tell a more interesting story than either camp wants to admit.

The company started life as a business intelligence software firm. That business still exists, quietly generating revenue in the background, but nobody's pricing MSTR on software fundamentals anymore.

Michael Saylor transformed the company into a publicly traded Bitcoin treasury, and the stock now trades purely on Bitcoin exposure.

When Bitcoin rises, MSTR typically outperforms. When Bitcoin falls, MSTR drops harder. That's the whole trade - leveraged upside and amplified downside.

Three metrics cut through the noise better than any price chart.

Forced liquidations show you when leveraged positions are getting washed out beyond fundamental value.

Long-term holder behavior reveals whether Bitcoin believers are actually holding or quietly heading for exits.

Bitcoin ETF flows tell you when institutional money managers think the worst is over.

I track all three because they separate actual risk from perceived panic.

Forced liquidations matter because MSTR's leverage amplifies Bitcoin moves in both directions. When Bitcoin drops sharply, margin calls force leveraged traders to sell, creating declines beyond fundamentals.

November 2025 and mid-January through early February 2026 saw forced liquidations soar, bringing steep dives exceeding normal corrections. MSTR's share price reflects these exaggerated moves.

Long-term holder data provides the second metric. As of February 10, holders with Bitcoin for over ten years control 17.2% of the supply. Combined holders from 1 to 10 years account for another 30.8%.

Nearly half the Bitcoin supply is held by people who've demonstrated multi-year conviction. These holders don't contribute to volatility - newer entrants trading Bitcoin as one asset class among many create the price swings.

Bitcoin ETF flows round out the picture. From January 16 through early February, outflows far surpassed inflows. Since February 6, inflows have consistently exceeded outflows. If that continues, it signals fund managers believe the worst may be over.

The debt structure deserves a closer look. Most of the $8.2 billion is convertible notes with no collateral requirements and no forced liquidation risk.

The company holds $2.25 billion in cash, providing roughly 2.5 years of dividend coverage for preferred shares.

CEO Phong Le said Bitcoin would need to stay at $8,000 through 2032 before debt coverage becomes a problem. Saylor said if issues arise, they'd refinance.

Whether that's possible in a distressed scenario is unknowable, but it's at least 6 years away under pessimistic assumptions.

The preferred stock structure adds complexity. MSTR issued multiple classes paying 8% to 11.25% dividends.

As the company pays these, the $2.25 billion cash reserve depletes. When that happens, they'll likely issue more common shares, creating predictable dilution that investors can model.

Between 2023 and early 2024, you could write "AI" in a presentation and ride the thematic wave.

Bitcoin-exposed stocks traded with roughly 80% correlation - buy any name, and you get the same trade. That correlation dropped to approximately 20%.

The market stopped treating Bitcoin plays as a basket and started differentiating between companies that can actually monetize exposure versus companies just burning cash.

MSTR's getting repriced as investors figure out whether leveraged Bitcoin accumulation with convertible debt makes sense.

I'm bullish on both Bitcoin and MSTR.

The leveraged structure means MSTR outperforms Bitcoin on the upside. The debt structure is more defensible than bears claim, and the runway extends further than most investors realize.

MSTR trades as a binary bet.

You either believe Bitcoin appreciates over time despite volatility, or you think the growth trajectory is unsustainable, and this is capital looking for a place to die.

There's no middle ground.

The emotional intensity around both Bitcoin and MSTR tells me most investors are making decisions based on where they bought rather than what the balance sheet shows.

The framework for navigating this is pretty straightforward.

Track forced liquidations to identify when price moves exceed fundamentals. Watch long-term holder behavior to gauge conviction among true believers.

Monitor ETF flows for signs that institutional money thinks we've seen the worst. Free cash flow, leverage structure, and whether the company's actually accumulating Bitcoin per share (not just in absolute terms) round out the analysis.

Companies selling stock during panic create some of the best buying opportunities of the decade, provided the balance sheet can survive to benefit.

MSTR's balance sheet suggests more runway than the disaster scenarios imply. Whether Bitcoin hits $8,000 and sits there for five years remains to be seen.

But if you're waiting for that scenario to invest, you've already made your bet.

Global Market Comments

February 18, 2026

Fiat Lux

Featured Trade:

(THE NEW OFFSHORE CENTER: AMERICA),

(SIGN UP NOW FOR TEXT MESSAGING OF TRADE ALERTS)

“In the US, you had ten bad years in a row (during the Great Depression) and it still turned out to be a pretty good century, said Lloyd Blankfein, CEO of Goldman Sachs.

Global Market Comments

February 17, 2026

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or ABANDON SHIP!),

(SPY), (EEM), (EWZ), (XLP), (XLU), (XLRE), (XLE), (XHB), (XLB, (CRM), (XLF), (LSTR),

(JBHT), (XLY), (JNJ), (CL), (O), (NEE), (SCHD)

“US stock performance was good in 2025, but is set to be outperformed by Japan, Europe, and emerging markets,” said a top manager at bond giant PIMCO.

It’s here - rules, and a mountain of them.

They didn’t stop until they got their cut.

Blame the industry for attracting the ire of the all-mighty rule makers.

This means that growth in this sector won’t be as gangbusters moving forward, if ever.

It’s a net negative for the original vision of crypto because the industry relies on that extra supercharger growth to attract incremental investors, and all in one poof, it's gone, like the wind.

What exactly happened?

The Financial Stability Oversight Council (FSOC), the U.S. regulatory panel comprising top financial regulators, successfully pushed Congress to enact legislation addressing risks digital assets pose to the financial system, including strict oversight of crypto spot markets and stablecoins.

Anything that Congress touches turns to higher costs and more red tape.

The FSOC's current enforcement regime follows a slate of directives that were released throughout the mid-2020s. The administration’s mandate effectively forced U.S. government agencies to double down on digital asset sector enforcement and close holes in regulation.

Legislative clarity has largely replaced the ambiguity of the past, with bills now codified to address stablecoins and digital commodities regulation.

Federal financial regulators now possess explicit rulemaking authority over the spot market for cryptocurrencies that are not securities, addressing conflicts of interest and abusive trading practices.

It’s not a joke that regulation has raced to the front and center of the crypto narrative as the defining constraint on the industry.

It has been relentless.

Just as we thought the worst had passed, the industry was forced to reckon with the consequences of the trust-toppling scandals that induced this heavy-handed regulation.

The poster child for this era remains reality TV star and influencer Kim Kardashian.

She is the Hollywood socialite who pushed Ethereum Max, a digital coin that aptly borrowed its name from the second biggest crypto, Ethereum.

What were the results?

Ethereum Max is effectively dead, prompting investors to sue Kardashian, who initially failed to disclaim that her marketing was being paid for by the company that owned the token.

Kardashian’s legal battles became a landmark case for influencer liability, even as her lawyers argued there was insufficient evidence that her endorsements led to the plaintiffs buying EMAX.

She paid a settlement of $1.26 million.

EMAX's value was based on the greater fool theory because it had no utility whatsoever.

As investors and promoters like Kardashian talked up such coins, more people invested, and the price went up, allowing the investors at the beginning to cash out.

Kardashian was paid $250,000 by Ethereum Max for her marketing efforts.

Altcoins like EMAX lack the stability of established assets like Bitcoin and Ether.

And EMAX never returned to meteoric highs, meaning the greater fool theory in this coin only reached so high for the previous investors to cash out.

EMAX remains a cautionary tale because investing in such assets is akin to pouring money down a black hole, with the asset depreciating rapidly.

While the exact number of people who invested based on celebrity endorsements is history, data from that period found that Kardashian's advertisement reached about one in five US adults and roughly 30% of crypto owners.

This was a public relations disaster that permanently damaged the crypto industry.

It’s bad enough that the industry impoverished many of its participants during the purge, but it also involved the lowest level of brain activity on the human planet.

One might conclude that the Kardashian fiasco marked the bottom of the industry's reputation, because how much lower and pitiful could crypto get?

The one silver lining in the market's survival is that the big holders haven’t sold out, which bodes well for crypto now that capital markets have stabilized.

That appears to be the last leg crypto is standing on, which could be either scary or a sanctuary, depending on how you look at it.

Lastly, steer away from anything other than Bitcoin if you are going to invest.