Mad Hedge Biotech & Healthcare Letter

April 30, 2020

Fiat Lux

Featured Trade:

(GILEAD SCIENCES GOES BALLISTIC ON REMDESIVIR TRIAL)

(GILD), (PFE), (JNJ)

Mad Hedge Biotech & Healthcare Letter

April 30, 2020

Fiat Lux

Featured Trade:

(GILEAD SCIENCES GOES BALLISTIC ON REMDESIVIR TRIAL)

(GILD), (PFE), (JNJ)

Gilead Sciences (GILD) is aggressively pushing to bring the coronavirus disease (COVID-19) to its proverbial knees before this year ends.

The ongoing coronavirus disease (COVID-19) pandemic has brought about substantial disruptions to the world economy, not to mention the devastating losses it caused families watching their loved ones succumb to this deadly virus.

Apart from Gilead, other biotech giants like Pfizer (PFE) and Johnson & Johnson (JNJ) are also hard at work looking for a COVID-19 cure.

Luckily, reports indicate that they may finally see a light at the end of the tunnel as one experimental treatment showed promising efficacy for fighting the health crisis.

Based on the contextual analysis of the leaked information on the clinical trials conducted by Gilead, the biotech company’s decision to bet on Remdesivir as a probable COVID-19 treatment could pay off soon.

At this point, Remdesivir is still under investigation in several Phase 3 clinical trials. These involve more than 2,400 participants scattered in 152 clinical sites.

One of these locations is the University of Chicago Medical Center, where 125 patients who tested positive for COVID-19 are treated every day with infusions of Remdesivir. Out of these individuals, only two deaths were reported with the majority already discharged.

Based on this subgroup alone, the fatality rate among the tested subjects is 1.6%.

Although Remesivir’s results still need further validation particularly in terms of adding a placebo arm in the clinical tests, the initial findings are already quite impressive. For context, data from John Hopkins University revealed that the fatality rate in the entire United States is roughly 4.69%.

Apart from that, another key detail points to the high probability of Remdesivir’s efficacy against COVID-19.

Among the 125 patients who underwent the treatment, 113 of them experienced severe symptoms.

As explained by the World Health Organization, the vast majority of those classified as severe cases involve the elderly and the immunocompromised. In one study, the infection death rate of individuals in this category fall somewhere between 1.93% up to 7.8%

Reassessing Remdesivir’s results from this perspective, we finally understand the excitement surrounding the drug’s efficacy despite the lack of a placebo trial.

In terms of questions on Remdesivir’s economic potential, we can take a look at past respiratory outbreaks like the H1N1 in 2009 and the 1918 Spanish flu for guidance.

Despite “flattening the curve,” at the time, both diseases had resurgences that reached second and third waves after the initial outbreaks were contained.

Combined, the H1N1 and the Spanish flu infected roughly 24% to 33% of the entire global population prior to subsiding for good.

Hence, high demand for Remdesivir will be expected even after the world manages to contain the first COVID-19 outbreak.

What does this mean for Gilead investors?

Remdesivir results are expected to come back positive by the end of April. With the FDA’s Coronavirus Treatment Acceleration Program, the drug is estimated to gain approval in a few months' time.

If successful, Remdesivir is projected to rake in more than $1 billion in sales throughout the coronavirus outbreak period. This estimate is based on the sheer number of people infected and are potentially at risk.

The estimated sales figure is also based on the assumption that Gilead can produce enough Remdesivir supply to treat up to 500,000 patients and that the drug will cost roughly $2,000 for a single-course treatment.

Adding Remdesivir in its lineup, Gilead has adjusted its 2020 revenue guidance to surpass $22 billion with sales growing by more than 4%, thanks to this potential COVID-19 drug alone.

However, Gilead offers more than a promising COVID-19 treatment.

The biotech giant prides itself of a strong lineup, showing off a particular dominance as the market leader for HIV treatments.

Its top HIV drug Biktarvy saw a whopping 300% increase in its sales last year, reaching $4.7 billion in 2019 alone -- and it still hasn’t reached its peak.

Analysts noted that Biktarvy has more room to grow in the next years, with the HIV drug anticipated to continue serving as Gilead’s significant growth driver until 2033.

Another HIV market leader is Descovy, which is set to be the preferred choice among 40% to 45% of patients by the end of 2020.

Despite these promising developments, Gilead stock is still pretty cheap.

To date, this biotechnology company is trading at 13.2 times forward earnings with a measly PEG ratio of 0.3.

At this price -- and considering the company’s strong portfolio and pipeline candidates -- investors on the lookout for biotech exposure but are worried about the consequences of the COVID-19 pandemic should definitely add Gilead into their core holdings.

![]()

Mad Hedge Biotech & Healthcare Letter

April 28, 2020

Fiat Lux

Featured Trade:

(THE FIVE FRONTRUNNERS IN THE RACE FOR A COVID-19 VACCINE)

(GSK), (SNY), (REGN), (TBIO), (VIR)

We’re finally pulling out the big guns.

Almost five months into this debilitating global pandemic, GlaxoSmithKline (GSK) and Sanofi (SNY) announced a collaboration to come up with a coronavirus disease (COVID-19) vaccine.

These vaccine heavy-hitters not only assured that the product would be ready by the second half of 2021 but also that they would be able to manufacture hundreds of millions of doses every year.

This is actually pretty impressive considering that the typical timeline for a vaccine takes at least a decade.

What we know so far is that Sanofi will conduct tests on its experimental vaccine using GSK’s adjuvants.

Adjuvants are added to improve the efficacy of some vaccines. These can also lower the amount of vaccine protein needed for every dose, boosting the likelihood of creating a shot that can be manufactured in large quantities.

According to GSK and Sanofi, human trials will begin in the second half of 2020.

GSK’s coronavirus adjuvant already demonstrated its value during the H1N1 influenza pandemic back in 2009 when this technology played a major role in the success of the Shingrix shingles vaccine.

As for Sanofi, the giant biotech company will be using a previously approved influenza vaccine for this joint effort.

GSK shares rose by 2% following the announcement while Sanofi got a 4.1% increase.

While both companies shared that they don’t really expect much profit from this COVID-19 vaccine, they plan to reinvest any short-term earnings in preparatory measures to better handle future pandemics.

Aside from this joint effort, GSK and Sanofi are also taking multiple shots in the hopes of solving this COVID-19 health crisis.

Sanofi is testing its malaria drug which contains hydroxychloroquine.

If you recall, this is the same drug that Donald Trump hailed as a “miracle” coronavirus cure earlier this year. Days following the president’s announcement, Sanofi offered to donate 100 million doses of hydroxychloroquine to 50 countries.

On top of that, Sanofi is also working with Regeneron (REGN) to assess whether its existing arthritis treatment Kevzara can work as a coronavirus medication.

It also has an ongoing collaboration with Translate Bio (TBIO) to come up with another COVID-19 vaccine using messenger RNA.

Outside its coronavirus efforts, Sanofi has been looking into streamlining the company’s focus to improve margins and shift into more lucrative growth areas. So far, so good.

One of the more drastic measures is eliminating diabetes and cardiovascular research sector of the company.

Funding for these was reallocated, with the acquisition of cancer and auto-immune biotechnology company Synthorx serving as a strong indication of the direction the company plans to take.

Apart from growing its immuno-oncology department, Sanofi is also betting on eczema treatment Dupixent -- a move that saw them rewarded almost immediately.

The company’s recent earnings report showed that Dupixent sales jumped 135% in the fourth quarter of 2019, with annual sales soaring to an impressive $2.3 billion. This indicates a 152% increase from the year prior.

Riding this momentum, Sanofi received FDA approval to expand the use of multiple myeloma drug Sarclisa in April.

This marks another significant win for the company.

Multiple myeloma ranks second in the list of most common blood cancer types, with the disease affecting roughly 32,000 Americans annually. It cannot be cured as well, which means that treatments are needed throughout the patients’ lives.

Needless to say, Sanofi has several platforms to contribute to finding the cure and even a vaccine for COVID-19. More importantly, the company has managed to transform itself into a more streamlined and innovative business.

Sanofi would be a wise choice for investors interested in a stock to hold for the long term. This company doesn’t only hold a starring role in the search for a coronavirus vaccine but also offers more opportunities beyond the current pandemic.

Meanwhile, GSK is also not limiting its adjuvant technology to Sanofi but to other companies developing COVID-19 vaccines as well. The list includes Vir Biotechnology (VIR) and even Chinese biotech company Clover Biopharmaceuticals.

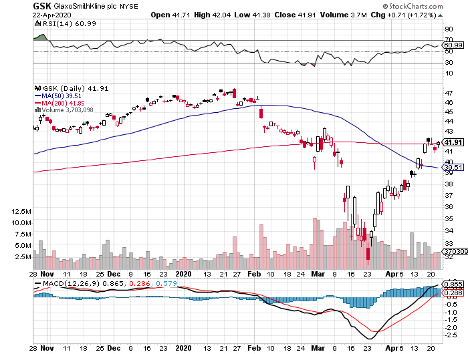

Despite its active participation in the coronavirus vaccine race, GSK tumbled down to over its 10-year low in March.

Although the pandemic’s negative impact looks discouraging, I think the overreaction is good news for value and dividend traders as the stock now trades at bargain-bin valuations.

Hence, investors could enjoy GSK’s lucrative 5.8% dividend at relatively cheap costs.

It also doesn’t hurt that GSK offers a diversified portfolio that all but guarantees minimal losses for its investors.

Its biggest revenue driver is the pharmaceutical arm of the business, which raked in total revenue of roughly $21.68 billion in 2019.

GSK’s vaccine segment contributed 8.87 billion while the consumer healthcare sector brought in over 11 billion.

Although smaller than its pharmaceutical arm, both segments are quickly catching up to GSK’s biggest moneymaker. In fact, its vaccine segment recorded revenue growth of 21% while its consumer healthcare arm jumped by 17%.

Overall, GSK is a compelling addition to any investor’s portfolio. Its impressive dividend combined with its diversified business makes this biotechnology company a wise choice as well.

The collaboration of GSK and Sanofi is considered as the most significant and promising COVID-19 vaccine effort to date.

This partnership not only maximizes the expertise of the two leading vaccine makers in the world but takes advantage of their manufacturing capacity as well, which is a critical concern given that a COVID-19 vaccine would have to be distributed to millions, if not billions, of individuals across the globe.

Mad Hedge Biotech & Healthcare Letter

April 23, 2020

Fiat Lux

Featured Trade:

(POST-PANDEMIC STOCKS TO DIVERSIFY YOUR PORTFOLIO)

(BPMC), (NVTA)

The biotechnology sector had been starved for love on Wall Street for the past few years despite the life-changing research and the introduction of fresh and innovative treatments for previously incurable conditions.

A year ago, the sector had the lowest price earnings multiple with the fastest earnings growth.

That couldn’t last.

With the outbreak of the catastrophic coronavirus disease (COVID-19) pandemic the public has fallen in love with the sector. While the biotechnology sector tanked in March with everything else, several industry benchmarks have been outperforming the broader market so far.

The harsh truth is that cures and vaccines remain far off.

The biotech sector is likely to become the next decade’s largest growth story.

The key is to find companies with strong balance sheets along and leadership that can manage any financial storm.

Nonetheless, there are biotech companies worth considering now, particularly those selling at bargain bin prices but with mature pipelines and promising soon-to-launch commercial products.

One compelling stock for long-term holding is Blueprint Medicines (BPMC).

This company develops targeted medicines for rare genetic types of cancer. So far, Blueprint has three treatments lined up for release in the market in the next 18 months. Just last month, the company announced the FDA approval of its first-ever cancer drug Ayavakit.

Ayavakit, which will be marketed as a treatment for a rare, genetically linked kind of gastrointestinal cancer, comes with a jaw-dropping price tag of $32,000 for a 30-day supply.

This cost is twice the amount of what was originally forecasted. However, analysts claim that this price is “justifiable” considering Ayavakit’s effectiveness and the absence of competition.

Riding the momentum of Ayavakit’s FDA approval, Blueprint has already filed for a second application in a bid to expand the indication for the drug to include patients suffering from gastrointestinal stromal tumors who already underwent three other treatments but failed.

According to the World Health Organization, 5,000 to 6,000 Americans are diagnosed with these tumors every year. Blueprint believes there's a strong chance this gets approved since 86% of their participants in the clinical trial responded to the drug.

Another potential blockbuster for Blueprint is a lung cancer drug currently dubbed as Pralsetinib. If the company gets approved, it can tap into a lucrative market as lung cancer comprises almost 25% of all cancer diagnoses.

Despite the COVID-induced economic crisis, Blueprint remains an attractive investment since it raised money prior to the pandemic. That means the company is well-capitalized.

Admittedly, the stock has gone down by 42% since its July 2019 high and only trades for $57 these days.

Although the company may experience disruptions in the near term, it’s undeniable that patients will still need their medications. Hence, business will definitely come back.

Another scenario is that Blueprint attracts more attention from aggressive acquirers.

So, if you’re looking into how to maximize this opportunity, keep it in mind that your reward all depends on the size of the position you plan to take.

Obviously, this stock comes with its own risks so it might not be an attractive option as a cornerstone of your portfolio. However, adding it to your diversified portfolio could offer you with market-beating returns in the long run.

Another stock that has been disrupted but still presents enticing rewards in the post-COVID days is Invitae (NVTA).

It peaked around February at $28 but went down to trade at a measly $9 to $12 as the coronavirus situation worsened. In fact, Invitae shares bottomed sometime in March at around $7. Since then, investors have been snapping it up at this low price.

Invitae offers genetic testing for kids with developmental issues, so you can easily see why the company isn’t going out of business anytime soon.

Fueling investors’ enthusiasm on this biotech stock are the series of acquisitions it made recently, with the company pouring money on virtual medicine.

In a way, you can say that Invitae is actually quite prepared for what’s happening today.

Just last month, Invitae acquired Orbicule BV otherwise known as Diploid. This recently acquired company develops an AI software that analyzes next-generation sequencing data combined with a patient’s information in order to diagnose genetic disorders.

The terms had Invitae buy 2,800,623 shares of Diploid’s common stock plus roughly $32 million in cash.

In April, Invitae acquired two companies.

One is YouScript Incorporated, which offers clinical decision support and functions as an analytics platform. This deal consisted of 2,293,452 shares of common stock plus $25 million in cash.

The second is Genetic Solutions, operating under the name Genelex, which is a precision medicine company.

With these acquisitions, Invitae needed to raise capital at a bargain-basement price. Does that mean that this genetic testing stock bottomed out?

That’s highly unlikely, but it’s virtually impossible to time market peaks and troughs anyway. The only reasonable means to deal with the current situation is to adopt a long-term mindset.

Keep in mind that this coronavirus pandemic will eventually pass. When it does, the biotechnology industry will return to growth.

After all, the revolutionary and groundbreaking drugs developed by this sector are critical.

For any growth investor on the lookout for high-value and sustainable options, the biotech industry can turn out to be the most lucrative one out there.

Mad Hedge Biotech & Healthcare Letter

April 21, 2020

Fiat Lux

Featured Trade:

(GETTING YOU BANG PER BUCK WITH ALEXION PHARMACEUTICALS)

(ALXN), (GILD), (RHHBY), (REGN), (SNY)

Since nobody can actually control when to get sick or what type of disease to acquire, it makes absolute sense that biotech stocks remain one of the wisest bets if you want to put your hard-earned cash to work.

The question, therefore, is what are the best biotech stocks to buy now?

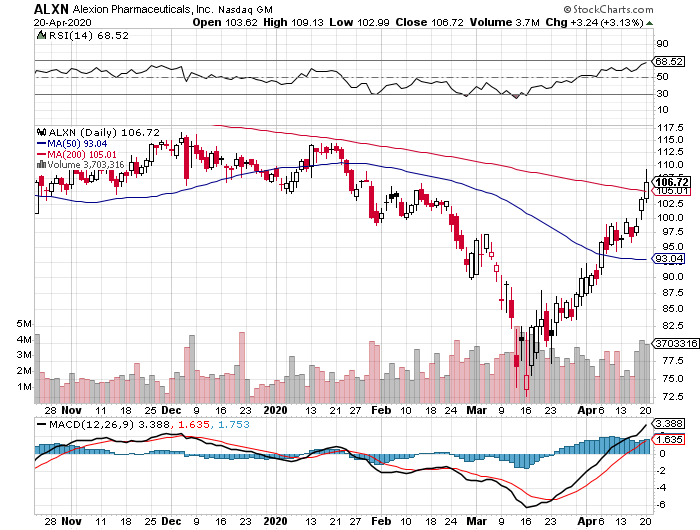

Looking at the biotechnology stock prices today, I can say that Alexion Pharmaceuticals (ALXN) will give you the most bang for your buck.

For over a decade, this ultra-rare-disease biotechnology company had been regularly valued at roughly 22 to 67 times its cash flow and frequently well above 30 times forward EPS.

Now, you can buy this top biotech stock for less than eight times its Wall Street profit consensus in 2021 and 10 times its cash flow for next year as well. It definitely doesn’t hurt that its PEG ratio is less than 1, categorizing it as an “undervalued” stock today.

However, its attractive pricing isn’t the only thing that’s putting Alexion in the news these days as this biotech company has been active in the race to find a coronavirus cure since early February.

When news about the pandemic broke, Alexion decided to repurpose its rare chronic blood disease bestseller Soliris as a potential COVID-19 treatment since the drug showed promising results on patients with severe pneumonia or acute respiratory distress syndrome.

Alexion’s efforts have been quite promising so far, with the biotech company targeting to commence a Phase 2 study of Soliris within the month. What we know so far is that this experiment will involve 10 patients as part of the proof-of-concept trial.

Apart from Alexion, other top biotech companies repurposing old drugs in search of a COVID-19 cure are Gilead Sciences (GILD) with Remdesivir, Roche (RHHBY) with Actemra, and Regeneron (REGN) and Sanofi (SNY) with Kevzara.

Outside its coronavirus treatment efforts, Alexion actually prides itself on a promising pipeline. To date, three treatments are projected to turn into blockbusters soon.

The first is Strensiq, which is formulated to treat a rare disease commonly known as hypophosphatasia. Patients with this disorder have an enzyme deficiency, making them unable to properly process calcium and phosphorus. As a result, they end up with malformed bones and teeth.

The second treatment is Kanuma, which is for patients suffering from lysosomal acid lipase (LAP) deficiency. People with this condition lack a key enzyme, preventing them from effectively breaking down fats.

Both conditions are extremely rare. Hypophosphatasia affects only 1 in 100,000 people while LAP is suffered by 1 in 40,000 individuals.

The third treatment is Ultomiris, which is widely regarded as Soliris’ successor.

For years, Soliris has been Alexion’s major moneymaker. However, uncertainties on the company’s hold on its patent exclusivity have started to shake investors’ faith in this stock. With one of Soliris’ key patents set to expire in 2021, the biotech company has to brace itself for the onslaught of generic competition.

This is where Ultomiris comes in.

Alexion has been busy migrating its customers to opt for Ultomiris before Soliris’ key patent expires.

To make this offer enticing, the biotech company has priced the newer drug to be slightly cheaper than the old blockbuster. Ultomiris costs $458,000 while Soliris is priced at $500,000.

To sweeten the deal further, the newer treatment is only required once every eight weeks. In comparison, Soliris’ treatment schedule is bi-monthly.

Basically, it’s as if Alexion has effectively restarted the clock in its patent exclusivity on this ultra-rare disease indication. The company aims to convert at least 70% of its users by mid-2020.

From a financial point of view, Alexion is performing quite well. Its fourth-quarter report showed that the company earned $1.4 billion in revenues, demonstrating a 23% increase from the same quarter in 2018.

Meanwhile, it raked in $5 billion in full-year sales for 2019. This indicated a 21% jump from its relatively paltry sales of $4.1 billion.

Looking at the metrics, Alexion is one of the surprisingly cheap stocks considering its growth. It also has the added bonus of dominating its chosen ultra-rare disease space.

This is typically a good strategy to avoid competition while also being able to seek high price points for its innovative treatments. The fact that insurers generally cover these treatments all but guarantees that Alexion is secure in terms of cash flow predictability.

Despite the panic induced by the coronavirus market, investing opportunities are everywhere --- if you know where to look.

Alexion is a solid company with strong growth prospects and is selling at a reasonable price. Any opportunistic investor worth his salt would know that this is the ideal time to strike.

Mad Hedge Biotech & Healthcare Letter

April 16, 2020

Fiat Lux

Featured Trade:

(CRISPR THERAPEUTICS’ CANCER BREAKTHROUGH),

(CRSP), (VRTX)

The findings for the first-ever human trial that uses CRISPR gene-editing technology to alter the immune cells of cancer patients have been announced.

The trial, which is hailed as the first of its kind to ever publish its results, centered on three patients suffering from advanced cancer who are all in their 60s. The goal is to determine whether or not their bodies could tolerate the genetically edited immune cells.

The patients received doses of CRISPR-modified variants gathered from their own T cells, which were specifically edited to transform into more efficient cancer-killing cells.

The results showed that there were no issues reintroducing the edited cells back into the bodies of the patients. More impressively, the modified cells managed to survive longer than the anticipated period.

In fact, these cells were detected in the patients’ bodies nine months following the novel treatment.

Doctors also noted that the patients’ symptoms stabilized throughout the treatment period. One of them even saw a reduction in tumor size.

While the treatment was only a one-time injection and was not carried on for a longer time, the fact that no major complication happened during the trial has health experts hailing it a success. Hence, more trials of this nature can be expected in the near future.

As expected, this trial boosted gene-editing stocks -- and CRISPR Therapeutics (CRSP) is one of the beneficiaries of this positive news.

This development is anticipated to further fuel investor interest in CRISPR Therapeutics especially after it released an impressive fourth-quarter financial report that beat revenue expectations.

The company’s profits grew to $77 million, indicating a substantial jump from the measly $100,000 it reported in the fourth quarter of 2018. As for its cash and cash equivalents, the amount increased by 106.7% from $456.6 million last year to $943.8 million.

Meanwhile, its total annual income increased from $3.1 million to a whopping $289.6 million.

A quick look at the changes done by the company revealed that the surge can be mostly attributed to CRISPR Therapeutics’ collaboration with Vertex Pharmaceuticals (VRTX) and not product sales.

Nonetheless, the improvement in the gene-editing company’s performance is still impressive considering that analysts only estimated their earnings to reach $45.2 million in the said quarter.

While these numbers are already turning heads, CRISPR Therapeutics is expected to dominate more headlines in 2020.

So far, the company has four major treatments in development.

One is called CTX001, which is for genetic blood disorders specifically sickle cell disease and transfusion-dependent beta thalassemia. Results involving this treatment should be out sometime this year.

The other three, CTX110, CTX120, and CTX130, are cancer treatments commonly known as CAR-T therapies.

CRISPR Therapeutics is an obvious leader in the race to commercialize CRISPR/Cas9 gene-editing services and products.

The lowdown is that its treatments under development, which involve groundbreaking innovations focused on rare diseases, have the potential to turn in hundreds of billions in sales. More impressively, CRISPR Therapeutics is poised to achieve this in record time --- way ahead of its competitors.

So, what’s the catch?

Well, CRISPR Therapeutics’ whole platform could end up amounting to nothing more than a fascinating science experiment. If that happens, then this stock would be worthless.

However, Vertex Pharmaceuticals has a stellar track record of picking winners. Its decision to splurge on CRISPR Therapeutics and back the latter’s research speaks volumes of the mid-cap biotechnology company’s potential to turn into a frontrunner in this novel world of gene editing.

Needless to say, CRISPR Therapeutics’ current valuation arguably indicates a once-in-a-lifetime buying opportunity. However, this high-risk investment would only appeal to aggressive investors.