Mad Hedge Biotech and Healthcare Letter

August 6, 2024

Fiat Lux

Featured Trade:

(JUST WHAT THE DOCTOR ORDERED)

(PFE)

Mad Hedge Biotech and Healthcare Letter

August 6, 2024

Fiat Lux

Featured Trade:

(JUST WHAT THE DOCTOR ORDERED)

(PFE)

Remember when everyone thought Pfizer (PFE) was just a one-hit COVID wonder? Well, it looks like they're proving the naysayers wrong. Let's dive into this medical marvel, shall we?

Pfizer just dropped its Q2 results, and boy, did they deliver a shot in the arm to Wall Street expectations. Revenue hit $13.28 billion, beating estimates by 2.02%.

But the real showstopper? Earnings per share of $0.6, smashing expectations by a whopping 30.19%.

Now, I know what you're assuming: "Isn't Pfizer still riding that COVID wave?"

Well, excluding COVID-19 products, revenue growth was actually a healthy 14% year-over-year. It's like Pfizer's been hitting the gym, bulking up its non-COVID muscles.

Speaking of muscles, let's talk about those margins. The adjusted gross margin pumped up to 79% from 76%. That's a 300 basis point improvement.

But that’s not all. Recently, Pfizer hasn’t only been focused on flexing its financial muscles but also trimming the fat.

Their operating expenses only increased by 5% year-over-year. They're also on track to deliver at least $4 billion in net cost savings by the end of 2024.

Clearly, Pfizer's been pinching pennies harder than a Depression-era grandma.

Now, let's talk about Pfizer's pipeline – the real meat and potatoes here. In 2023 alone, they got FDA approvals for 9 new drugs. That's more approvals than a helicopter parent gives on prom night. And they're not stopping there.

By the end of 2024, they're expecting to launch 20 new products or indications. It's like they're running a drug development assembly line over there.

Notably, Pfizer's oncology segment is quickly growing. Sales hit almost $4 billion in Q2, and with the recent acquisition of Seagen, they're positioning themselves as the oncology powerhouse of the future.

We're talking about a potential market size of over $300 billion by 2030. That's enough zeros to make your head spin faster than a centrifuge.

And let's not forget about their market dominance. Prevnar 20 is ruling the pediatric segment with over 80% market share in the U.S.

But the real dark horse here is their foray into the obesity market. With their GLP-1 agonist in development, they're eyeing a piece of a market that's expected to hit $100 billion by 2030.

Next, let's get down to the nitty-gritty of R&D. Pfizer's been pouring money into research like it's watering a money tree.

They spent a whopping $11.4 billion on R&D in 2023, up 10% from the previous year. That's about 15.7% of their revenue – higher than the industry average of 13.4%.

But despite all this good news, Pfizer's stock is trading at just 11 times projected earnings. In fact, Wall Street analysts are giving modest EPS growth projections.

In my humble opinion, though, a fair valuation for Pfizer should be at least 15 times earnings. And with a dividend yield above 5.5% for the next few years, it's like getting paid to wait for the market to wake up and smell the antibiotics.

Of course, it's not all rainbows and unicorns in Pfizer-land.

They've got some patent expirations coming up that could hit sales harder than a heavyweight boxer. Between 2025 and 2030, they're facing potential losses on products that generated $17 billion in peak sales. That's a pill even Pfizer might have trouble swallowing.

And let's not forget about the elephant in the room – healthcare reform.

With politicians yakking about drug pricing like it's the latest reality TV drama, there's always a risk of regulatory headwinds. But Pfizer's diverse portfolio and global reach give it more shock absorbers than a monster truck.

So, what's the play here? Well, assuming Pfizer keeps managing costs like a coupon-clipping grandma, they could easily beat current forecasts by 10% or more by the end of 2024.

If the market finally recognizes Pfizer's potential and grants it a P/E ratio of 14x, we're looking at a price target of $43.4.

That's a 42% upside from the recent closing price – more juice than you'd get from a whole orchard of oranges.

So, here's the bottom line: Pfizer's current stock price is criminally undervalued. With its robust pipeline, improving margins, and commitment to dividends, I'm suggesting you buy this stock faster than you can say "take two and call me in the morning."

Mad Hedge Biotech and Healthcare Letter

August 1, 2024

Fiat Lux

Featured Trade:

(THE PLAYBOOK FOR A BIOTECH TRIPLE CROWN)

(ABBV), (TEVA), (PFE), (AMGN), (AZN), (BGNE), (LLY), (CERE)

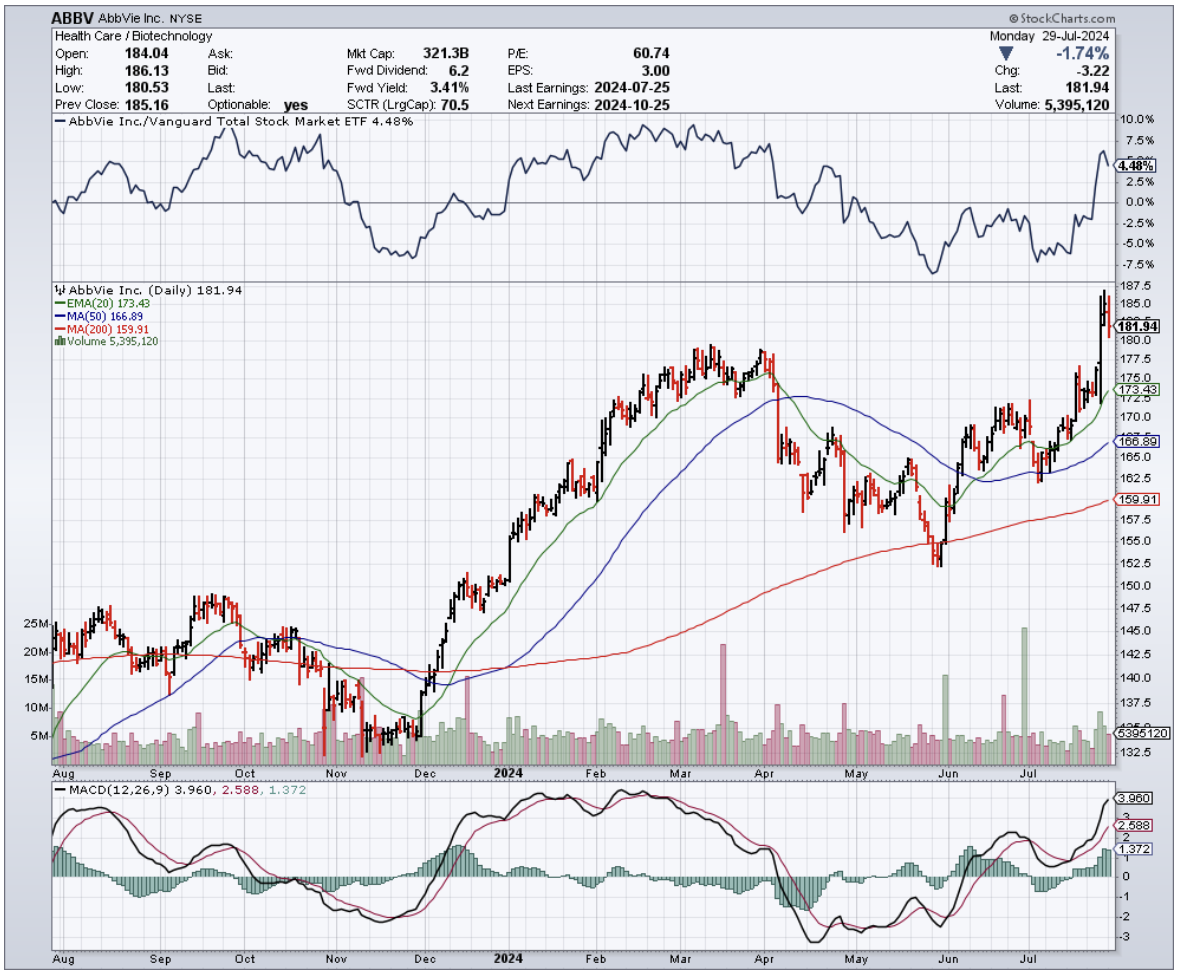

AbbVie (ABBV): A biotech stock that's been on my radar longer than most. If I could travel back to my UCLA biochem days, I'd tell young John to ditch the petri dishes and buy shares in this pharma giant. Why?

Because AbbVie isn't just another pharma play – it's a masterclass in diversification, innovation, and market-beating performance.

This is the stock that could turn a bright-eyed student into a savvy investor faster than you can say "immunology franchise."

In fact, if you've been paying attention to the market, you might have noticed that AbbVie's stock has been outperforming the broader U.S. market since mid-April, and for good reason.

This is a company that's been running at full throttle, posting some seriously impressive numbers in Q2 2024. We're talking $14.46 billion in revenue, a whopping 17.5% increase from the previous quarter and beating consensus estimates by a cool $430 million.

Earnings per share may have fallen just short of analysts' expectations, but they still climbed by a respectable 34 cents to $2.65.

But here's the thing: AbbVie's success isn't just a flash in the pan. This is a company with a diversified portfolio that's driving growth across multiple fronts.

I'm talking about their immunology, oncology, and neuroscience franchises, which together account for a staggering 75% of the company's total revenue.

Let's start with immunology. Now, I know what you're thinking - isn't that just Humira, AbbVie's blockbuster drug for Crohn's disease and ulcerative colitis? Well, yes and no.

While Humira has been facing some generic competition from the likes of Teva Pharmaceutical (TEVA), Pfizer (PFE), and Amgen (AMGN), resulting in a 30% year-over-year decline in global sales, AbbVie's got a couple of other tricks up its sleeve.

Enter Skyrizi and Rinvoq, two immunology drugs that are picking up the slack in a big way. Sales of these bad boys climbed 45% and 56%, respectively, in Q2 2024.

Skyrizi, in particular, has been an absolute beast, raking in $2.73 billion and growing 44.8% year-over-year. And with the FDA giving it the green light for moderate-to-severe ulcerative colitis in June 2024, the sky's the limit for this game-changer.

But AbbVie's not content to rest on its laurels. They're pushing the envelope with Rinvoq, a JAK inhibitor that's been approved for a wide range of indications and is showing some serious promise.

In Q2 2024, Rinvoq brought in $1.43 billion, a 30.8% quarter-over-quarter increase, thanks to strong demand in the U.S., excellent clinical trial results, and FDA approval for treating children with psoriatic arthritis and juvenile idiopathic arthritis.

And let's not forget about giant cell arteritis, a condition that AbbVie's been targeting with Rinvoq.

Recent trials have shown some impressive results, with 46% of adult patients taking Rinvoq 15 mg experiencing sustained remission, compared to just 29% of those on placebo.

No wonder AbbVie's been submitting applications left and right to get this drug approved for even more indications.

But it's not just immunology where AbbVie's making waves. Their oncology portfolio, bolstered by the acquisition of ImmunoGen in mid-February 2024, is also delivering the goods.

Sure, demand for Imbruvica may be declining due to newer BTK inhibitors from AstraZeneca (AZN), BeiGene (BGNE), and Eli Lilly (LLY), but Elahere, an antibody-drug conjugate for ovarian cancer, is quickly becoming a rising star.

In Q2 2024, Elahere sales jumped 65.4% quarter-over-quarter to $128 million, driven by increased marketing, growing awareness among physicians, and promising data from clinical trials.

Finally, let's not overlook AbbVie's neuroscience franchise, which generated a cool $2.16 billion in Q2 2024, a 14.7% year-over-year increase.

Headlining this portfolio are Qulipta and Ubrelvy for migraine treatment, and Vraylar for a range of psychiatric conditions.

Qulipta, specifically, has been a standout, with sales surging 56.3% year-over-year to $150 million, thanks to its convenient oral administration and long-term efficacy data.

Looking ahead, AbbVie's got even more irons in the fire. Their $8.7 billion acquisition of Cerevel Therapeutics (CERE) is set to close soon, bringing promising neuroscience candidates like emraclidine for schizophrenia and davapidon for Parkinson's into the fold.

With all these positive developments, it's no wonder AbbVie's feeling confident enough to raise its full-year adjusted EPS guidance to $10.71-$10.91, up from the previous range of $10.61-$10.81. Talk about a biochemistry experiment gone right!

So, there you have it. AbbVie: a healthcare powerhouse that's firing on all cylinders and poised for even greater success in the years to come. If only I could've shown this to my younger self back in those UCLA labs – he might've traded his test tubes for trading terminals a lot sooner.

Now, if you're ready to take a ride on this rocket ship, I suggest you buckle up and hang on tight. Because let me tell you, dissecting AbbVie's financial DNA has been more thrilling than any fracking adventure or hedge fund rodeo I've ever been on.

And if there's one thing I've learned in my years hopscotching from biochem labs to Wall Street, it's that the view from the top of a well-diversified, innovative pharma giant is always worth the climb. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

July 30, 2024

Fiat Lux

Featured Trade:

(RETAIL THERAPY, MEET RETAIL RX)

(HUM), (WMT), (WBA), (UNH), (CVS), (TDOC)

In my years of covering the markets, from the trading floors of Tokyo to the halls of power in Washington, I've seen my fair share of unexpected partnerships.

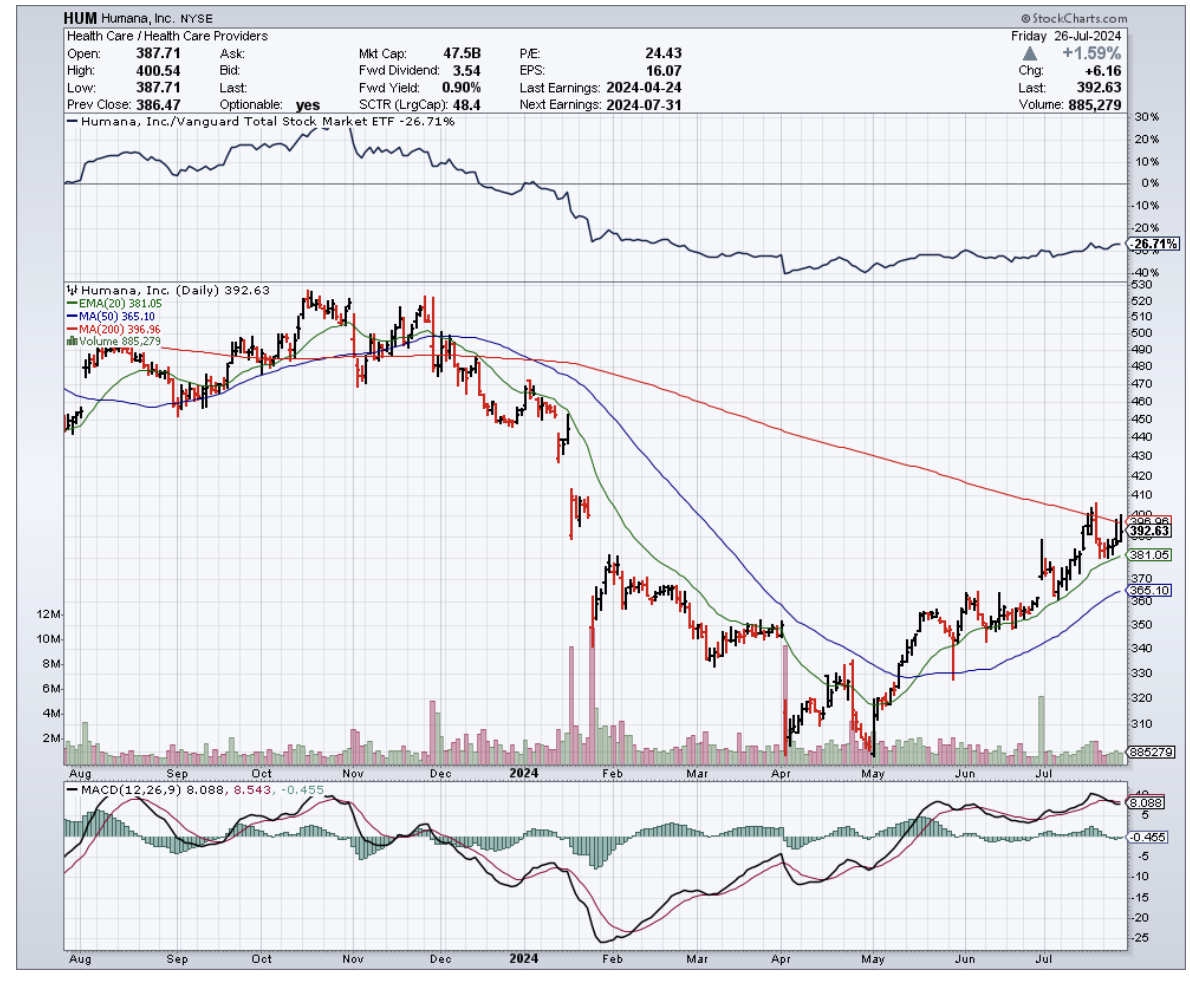

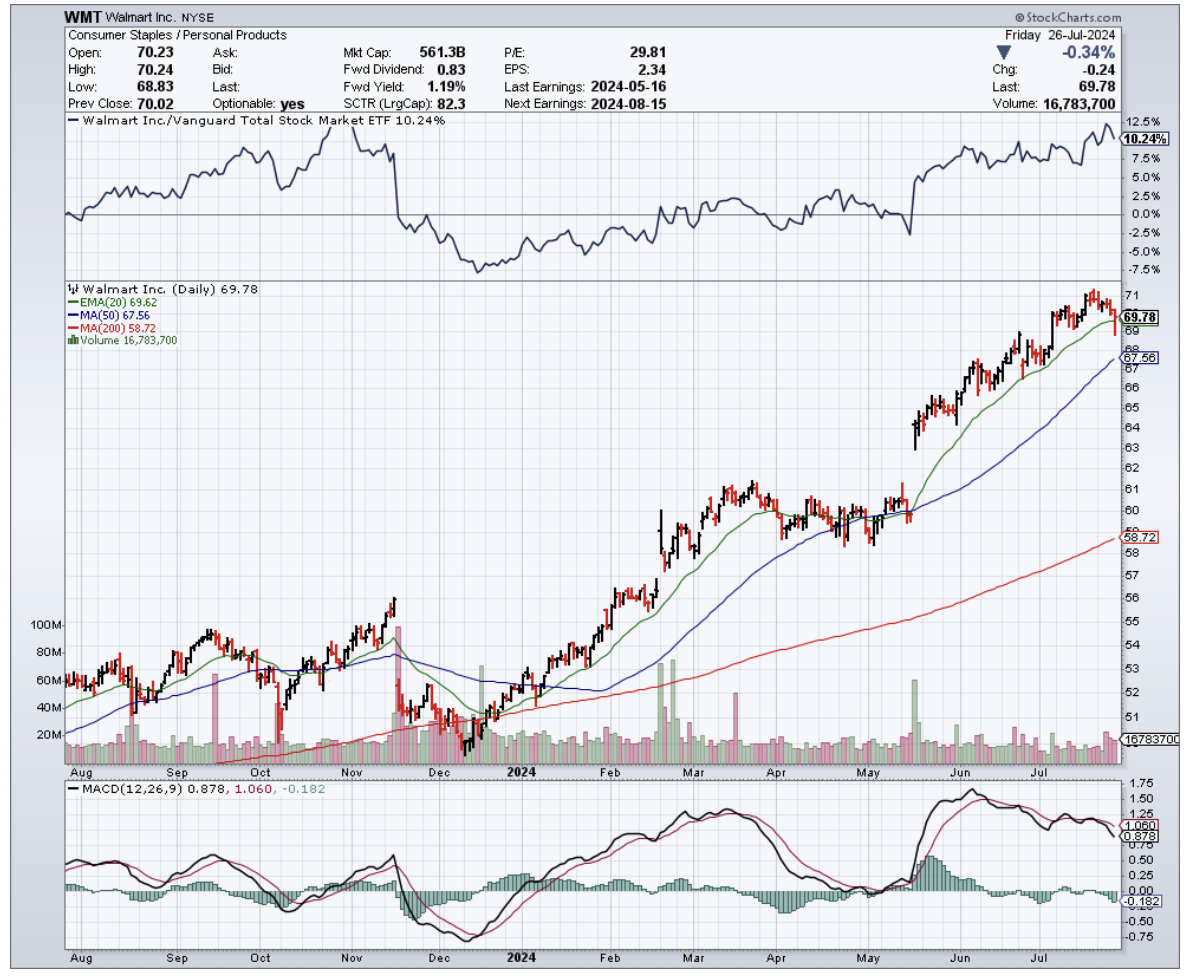

But the recent tie-up between Walmart (WMT) and Humana (HUM) has me sitting up and paying attention.

That’s right. Walmart, the king of rollbacks and home of the $1 hot dog, has found a new tenant for the vacant spaces that used to house its healthcare business: Humana's CenterWell health clinics.

Humana, as you know, is one of the biggest players in the Medicare Advantage game, and is setting up shop in 23 Walmart Supercenters across Florida, Georgia, Missouri, and Texas.

And they're not just dipping their toes in the water – they're diving in headfirst, with plans to have these clinics up and running by the first half of 2025.

Now, I know what you're thinking. "John, why should I care about some dusty old retail giant like Walmart getting into bed with a health insurance company?"

Let me tell you why.

Humana's Q1 2024 earnings were nothing to sneeze at, with revenues growing 11% year-over-year to a whopping $29.6 billion.

And while the company did revise its full-year EPS guidance downward, it maintained its outlook for adjusted EPS and even revised its membership growth in MA plans upward.

This is a big deal, folks. Medicare Advantage plans have been the bread and butter of Humana's business model, underpinning the company's phenomenal share price gains from $25 per share in 2010 to over $550 in late 2022.

With the population aging faster than fine wine, the demand for senior-focused healthcare services will only grow.

But Humana isn't the only one benefiting from this partnership.

For Walmart, renting out these spaces to CenterWell allows them to recoup some of the infrastructure investments they made in building out their 51 Walmart Health clinics, which they recently shut down due to profitability challenges.

It's like finding a roommate to help pay the rent after your startup goes belly up.

But the healthcare industry is like a giant game of Jenga, with players constantly pulling out blocks and hoping the whole thing doesn't come crashing down.

Just look at Walgreens Boots Alliance (WBA), another retail giant that recently announced the closure of 150 of its in-store clinics due to profitability challenges. It's a stark reminder of how difficult it can be to make a buck in this business.

That's why Walmart's pivot to a partnership model with Humana is so intriguing.

By leasing out pre-equipped facilities to CenterWell, Walmart is essentially letting Humana handle the nitty-gritty of patient care while still maintaining a presence in the rapidly growing primary care industry.

It's like having your cake and eating it too, without having to worry about the pesky details of actually baking the cake.

As expected, Walmart and Humana aren't the only ones making moves in the healthcare space.

CVS Health (CVS) and UnitedHealth Group (UNH) are also betting big on primary care, with CVS acquiring Oak Street Health for $10.6 billion and UnitedHealth's Optum division going on an acquisition spree to expand its network of physicians and healthcare providers.

Then, there’s the meteoric rise of telehealth during the pandemic. Companies like Teladoc Health (TDOC) saw their revenues skyrocket as patients turned to virtual care in droves.

While growth has slowed down since the height of the pandemic, telehealth is still a force to be reckoned with and could potentially disrupt traditional brick-and-mortar clinics.

So, what does all this mean for us?

Well, if you're an investor looking to get in on the action, you've got plenty of options. From established players like Humana and UnitedHealth to up-and-comers like Oak Street Health and Teladoc, there's no shortage of companies vying for a piece of the healthcare pie.

With an aging population, rising healthcare costs, and a growing focus on preventative care and chronic disease management, the demand for innovative healthcare solutions is only going to increase in the coming years.

And who knows, maybe one day we'll all be getting our annual check-ups at the local Walmart, with a side of low-priced toilet paper and a jumbo bag of Cheetos.

Stranger things have happened in the wild world of healthcare.

Mad Hedge Biotech and Healthcare Letter

July 25, 2024

Fiat Lux

Featured Trade:

(REVERSING THE FOG)

(SAVA), (ESALF), (BIIB), (LLY), (RHHBY), (ACIU), (AVXL), (ATHA)

Close your eyes and think back to your favorite childhood memory. Maybe it's the smell of your grandma's apple pie wafting through the kitchen, or the sound of your grandpa's belly laugh as he tickled you mercilessly.

Now imagine those memories being ripped away, one by one, until all that's left is a hollow shell of the person you once knew and loved.

That's the heartbreaking reality of Alzheimer's disease, and it's a fate that Rick Barry, the newly minted executive chairman of Cassava Sciences (SAVA), is determined to change.

You see, Barry isn't just some suit looking to make a quick buck. No, sir. This man's got skin in the game, and a personal connection to the fight against Alzheimer's that'll tug at your heartstrings.

His decision to join Cassava's board back in June 2021 was driven by a gut-wrenching story about his buddy's father, Buddy. This once-vibrant Navy fighter pilot and commercial airline captain was reduced to a shell of his former self by the cruel hand of Alzheimer's.

And folks, this ain't an isolated case. We're talking about 6.9 million Americans aged 65 and older living with this wretched disease in 2024, with that number set to double in the next 30 years.

Globally, over 55 million people are grappling with dementia, and Alzheimer's is the big, bad culprit in 60-70% of those cases.

While the situation is admittedly grim, Cassava Sciences offers a glimmer of hope: simufilam.

This experimental drug is Cassava's secret weapon, designed to whip a rogue protein called filamin A back into shape.

When filamin A goes off the rails in Alzheimer's patients, it wreaks havoc on brain function. But simufilam, like a disciplined drill sergeant, could get this unruly protein back in line, normalize cellular processes, reduce inflammation, and give synaptic function a much-needed boost.

Now, I know you're probably skeptical, but the Phase 2 trial results were nothing to sneeze at. A whopping 47% of patients saw their cognitive function improve, and the biomarkers of neurodegeneration and inflammation took a nosedive.

But the real moment of truth lies ahead in the Phase 3 trials, RETHINK-ALZ and REFOCUS-ALZ. These trials are the big leagues, with nearly 2,000 participants and top-line results expected by the end of 2024.

If simufilam can prove its mettle, it could be a game-changer for millions of Alzheimer's patients who are desperate for a breakthrough.

Of course, Cassava Sciences isn't the only horse in this race. The heavyweight contenders like Eisai (ESALF), Biogen (BIIB), Eli Lilly (LLY), Roche (RHHBY), and AbbVie (ABBV) are all jockeying for position, while smaller outfits like AC Immune (ACIU), Anavex (AVXL), and Athira Pharma (ATHA) are making some intriguing moves of their own.

But what really sets Cassava apart is the fire in their belly. When Barry says, "If you create great benefit for your patients, you'll create great value for your shareholders," you can tell he means business. This isn't just about lining pockets – it's about making a real difference in people's lives.

And let me tell you, the impact of Alzheimer's is staggering. Over 11 million Americans are providing unpaid care for their loved ones with Alzheimer's or other forms of dementia.

In 2023 alone, these unsung heroes clocked in a mind-boggling 18.4 billion hours of care, valued at a cool $350 billion.

And to make things worse, 70% of these caregivers are stressed to the max trying to coordinate care, while 66% are struggling to find resources and support. On top of that, 74% are also worried sick about their own health.

Financially, Alzheimer's is a beast that just keeps growing. In 2023, it drained $345 billion from the nation's coffers.

Fast forward to 2024, and that price tag is expected to hit $360 billion. And brace yourselves, because by 2050, we could be staring down the barrel of a $1 trillion problem.

So, is Cassava Sciences stock a slam-dunk investment? Well, that depends on your appetite for risk.

In the biotech world, the stakes are high, and the outcomes are never guaranteed. Simufilam's fate rests squarely on the results of those pivotal Phase 3 trials.

But one thing I can say with certainty is that Cassava Sciences has got guts. They're the underdog taking on Alzheimer's, armed with a potentially groundbreaking treatment and a whole lot of heart.

In a world where roughly 1 in 9 people over 65 are living with Alzheimer's, the impact of a successful therapy would be nothing short of seismic.

As investors, it's easy to get caught up in the cold, hard numbers. But sometimes, it pays to step back and consider the human element.

Behind every stock symbol, there are countless families praying for a miracle, tireless researchers burning the midnight oil, and brave souls like Rick Barry putting their money where their mouth is.

So, while I can't tell you to go all-in on Cassava Sciences just yet, I can tell you this: they're fighting the good fight. And in a world that often seems like it's gone completely off the rails, that's something worth getting behind. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

July 23, 2024

Fiat Lux

Featured Trade:

(DON'T SLEEP ON THIS BIOTECH SLEEPER)

(ATHA), (BIIB), (LLY)

To date, 6.7 million Americans over 65 are already wrestling with Alzheimer's, a number set to double by 2050.

It's a demographic disaster, a slow-motion train wreck that Big Pharma's been slow to recognize.

Companies, including Biogen (BIIB) and Eli Lilly (LLY), working on this are still fiddling with amyloid plaques and tangled proteins, like a plumber trying to fix a leaky nuclear reactor with duct tape.

But one scrappy biotech outfit, Athira Pharma (ATHA), is taking a different tack. They're not chasing the same old tired targets.

Instead, they're looking at the brain's own repair mechanisms, trying to kickstart the engine instead of just patching up the exhaust. It's a high-risk, high-reward play, but isn't that what makes this game so damn exciting?

Athira targets the neurotrophic hepatocyte growth factor (HGF) and its sidekick, the MET receptor. Don't let the fancy names fool you - these little fellas are the unsung heroes of your noggin.

Think of HGF and MET as the brain's maintenance crew. They're not just sitting around twiddling their thumbs. They're constantly on the job, patching up neurons and keeping the lights on upstairs.

Athira's betting the farm that if they can juice up this dynamic duo, they might just be able to slow down the Alzheimer's wrecking ball, or heck, maybe even throw it in reverse.

It's a bold move, I'll give 'em that. While everyone else is trying to sweep up the mess Alzheimer's leaves behind, Athira's aiming to stop the party before it even starts.

If they're right, it could be like discovering fire all over again in the world of neuroscience.

Speaking of which, Athira's lead drug, fosgonimeton (try saying that three times fast), just hit a milestone that's got Wall Street perking up its ears. They've wrapped up dosing in their Phase 2/3 LIFT-AD trial for mild-to-moderate Alzheimer's.

We're talking about 315 patients who've been getting daily shots of this stuff (or a placebo) for 26 weeks. It's like a six-month-long neuroscience party, and we're all waiting to see who's left standing when the lights come on.

Interestingly, Athira's playing it smart with their ongoing Phase 2/3 LIFT-AD trial. They're using something called the Global Statistical Test (GST) as their primary endpoint. It's like they're giving themselves better odds at the casino.

This GST is designed to catch even the slightest whiff of a clinically meaningful treatment effect. It's like using a finely-tuned bloodhound instead of a myopic poodle to find your car keys.

And here's another thing that caught my attention: 85% of the folks from their trials signed up for the after-party - the open-label extension study. That's like people sticking around to help clean up after a rager.

When was the last time you saw that kind of enthusiasm for anything, let alone a clinical trial?

But Athira isn't content with just one target. They've also got fosgonimeton in the ring against Parkinson's with their SHAPE trial.

This Phase 2 slugfest has already shown some positive jabs on cognitive measures for patients with Parkinson's disease dementia and Dementia with Lewy bodies.

And because apparently two fights aren't enough, Athira's also thrown fosgonimeton into the ALS arena. This early-stage trial is like watching a fighter warming up in the gym - we don't know how it'll play out, but the potential is intriguing.

So, what’s next? Well, we’re now staring down the barrel of what could be the biggest shakeup in Alzheimer's research since... well, since we started researching Alzheimer's.

Athira's betting big on their HGF/MET approach, and if it pays off, we might be looking at the medical equivalent of striking oil in your backyard.

Mark your calendars for the end of Q3 2024. That's when we'll find out if fosgonimeton is the real McCoy or just another pie-in-the-sky biotech dream. And don't forget the fireworks show in Madrid this October - Athira's set to strut their stuff at the Alzheimer's conference, and you can bet your bottom dollar I'll be watching.