Mad Hedge Biotech and Healthcare Letter

May 7, 2024

Fiat Lux

Featured Trade:

(PACKING A HEAVIER PUNCH)

(AMGN), (NVO), (LLY), (REGN)

Mad Hedge Biotech and Healthcare Letter

May 7, 2024

Fiat Lux

Featured Trade:

(PACKING A HEAVIER PUNCH)

(AMGN), (NVO), (LLY), (REGN)

Amgen (AMGN) is having a moment. Early results for their injectable drug MariTide sound pretty darn promising.

But it’s not all roses and sunshine at Amgen. The company also dropped the curtain on AMG786, an experimental oral weight-loss pill that just wasn't cutting it.

It’s tough in the pharmaceutical arena, especially since this whole weight-loss drug market is a gold rush right now. Eli Lilly (LLY) and Novo Nordisk (NVO) are cleaning up, and even Pfizer (PFE), despite their hiccup, isn't going to roll over that quickly.

Now, back to MariTide. Calling it a "multi-blockbuster" sounds flashy, but investors want to see if it can crack the hold those big two already have. Amgen's got a decent track record though, so I wouldn't write them off just yet.

The early scoop on MariTide is pretty tantalizing. The last round of Phase 2 trials showed that three monthly shots could significantly trim the waistline, with the heftier doses keeping the pounds off for up to four months post-treatment.

Actually, MariTide’s core strength is that it’s just once-a-month jab — an easier regimen compared to the weekly routine required by current front-runners like semaglutide and tirzepatide.

Speaking of the competition, Novo Nordisk’s semaglutide and Eli Lilly’s tirzepatide have been seeing users pack the pounds back on pretty quickly after stopping treatment.

That’s not ideal, and it’s exactly the kind of opening Amgen is looking to capitalize on with MariTide.

Now, let’s broaden our scope. It's a bit of a misnomer to just call it an “obesity pipeline” because, let me tell you, this technology is dipping its toes into much more than just shedding pounds.

Those GLP-1 agonists like semaglutide and the double-duty “double G” agonists like tirzepatide? They’re not just one-trick ponies.

Aside from battling the bulge, they’re making waves in treating diabetes, slicing through cardiovascular risks, and even exploring new frontiers like osteoarthritis and sleep apnea.

Heck, they’re even peeking into Alzheimer’s prevention — Novo Nordisk is already revving up for a phase 3 trial.

Despite these lucrative offshoots though, obesity remains the arena’s juggernaut.

Novo Nordisk’s latest data, as bleak as it might seem for global health, paints a picture of a market vast enough to entice anyone. Think about it—out of 813 million people wrestling with obesity, only one million are currently on these incretin drugs.

And with projections pointing to numbers ballooning to 1.2 billion by 2030, well, the potential market is jaw-dropping.

If Amgen’s MariTide hits the mark, we could be talking about a whopping $20 billion in annual sales from just this one contender in about 7-8 years, spanning obesity and a few neighboring conditions.

That’s even if they face a dogfight over pricing and if the average price per patient hangs below what the big guns like Novo Nordisk and Eli Lilly are currently pulling.

Now, think about this — current estimates peg Amgen’s growth from $33 billion this year to a modest $35.1 billion by 2033. My take? That’s wildly conservative.

If you ask me, Amgen's obesity pipeline alone, even with just modest success, could blast those numbers out of the water.

But let's not kid ourselves – MariTide alone won't make Amgen king of the obesity market. To truly capitalize on the segment’s potential, Amgen might need to consider teaming up with those emerging stars working on preserving lean body mass, or even big players like Regeneron (REGN).

They could take a couple of routes here. One slick move could be scooping up some smaller biotech firms or cozying up to bigger fish through partnerships or in-licensing deals to beef up their treatment options.

Alternatively, Amgen could play it cool and simply pair MariTide with their own upcoming products once they hit the market. Sure, this might keep things simple, but it kind of feels like leaving money on the table, isn’t it?

Admittedly, it’s still early days when it comes to these weight loss treatments. One thing's for sure: the next few years will be a wild ride for obesity drugs. After all, it’s clear that the GLP-1 craze is doing for pharma what AI hype is doing for tech stocks. It’s like a rising tide lifting all boats.

Looking ahead, the big winners in the next 18 months are looking to be Novo Nordisk and Eli Lilly. These guys are leading the pack, while others might just not make it to the finish line, ending up as flops in the stock market drama.

Yet, through all this, Amgen stands out as a dark horse.

Even if the obesity pipeline doesn't turn out to be their golden ticket, Amgen's strategic positioning could still deliver solid long-term value.

But, and here’s the kicker, if MariTide and its potential combo treatments hit their stride as hoped, Amgen could sprint ahead in this fast-paced market race — not just in obesity but in those juicy, adjacent niches too. This could spark some serious value creation that current forecasts haven't even begun to factor in.

So, while the market’s getting its gears grinding, Amgen might just surprise us all. I say keep this stock on your watchlist.

Mad Hedge Biotech and Healthcare Letter

May 2, 2024

Fiat Lux

Featured Trade:

(BUT WEIGHT, THERE’S MORE)

(LLY), (NVO)

You know that feeling when you find a crumpled $20 bill in an old jacket? That’s a little like what Eli Lilly must be feeling with tirzepatide, only replace that $20 with a cool $34 billion forecast by 2029. Yeah, it’s been that kind of party over at Lilly.

Tirzepatide, the magic ingredient in both Zepbound for weight loss and Mounjaro for diabetes, is turning heads—and not just because it’s raking in the cash. This drug is proving to be a one-stop-shop for boosting Lilly’s bottom line and shaking up the market.

Since Zepbound’s launch in November 2022, Lilly’s stock has been on a tear, skyrocketing from $349.95 to a whopping $733.51.

That’s a gain of over 109%. It’s like Eli Lilly has turned into the Usain Bolt of the biotech and pharma sector, sprinting past the S&P 500 and its pharma peers without breaking a sweat.

Actually, Lilly's got a double-whammy against the competition. Not only does Tirzepatide keep raking in successful studies, but it's also got a sweet price point.

We're talking about Zepbound being a good 20% cheaper than Novo Nordisk's (NVO) big hitter, semaglutide.

Essentially, patients get the same results, but a lot less strain on their wallet. This combination easily gives Lilly a serious edge in the diabetes and obesity drug battle.

But wait, there’s a hiccup. Despite the blockbuster status of Zepbound, there’s a bit of a snag recently with this drug—supply can’t keep up with demand.

It makes you wonder whether this is a classic case of "too much of a good thing," right?

This shortage has even made the US Food and Drug Administration limited availability list. But fear not, Lilly’s got plans to boost production with a new facility in Concord, North Carolina by year-end.

Still, this supply problem didn’t stop Lilly from coming up with tirzepatide’s latest party trick: tackling obstructive sleep apnea (OSA).

Basically, OSA disrupts your sleep by making your throat muscles a bit too enthusiastic at night. They tighten up and block your airway, leaving you gasping for air (not exactly the recipe for restful sleep). Untreated OSA can be a serious health hazard, linked to heart problems down the line.

And here's a scary statistic: 80 million adults in the US have sleep apnea, but a whopping 85% of those cases go undiagnosed. That's right, millions are unknowingly battling a condition that disrupts sleep, increases the risk of heart problems, and leaves you feeling like a zombie all day.

Given these figures, it’s not surprising that Lilly’s looking to turn this challenge into the next big opportunity.

In fact, recent studies have shown tirzepatide could reduce those pesky episodes of stopped breathing during sleep by about 30 times an hour compared to a placebo. Talk about a breath of fresh air.

So, how much money will tirzepatide rake in at its peak? Well, it's already approved for diabetes AND obesity, but there's room for even more growth.

To date, Lilly is projected to rake in $25 billion in peak sales for this drug, but with recent developments, even that seems low.

Think about this: Tirzepatide made over $5 billion last year – its first full year on the market.

Then, it snagged the obesity indication in November 2023, now pharmacies can't keep it on the shelves, showing demand is off the charts.

Now, I know you’re wondering if you’ve missed the boat with Lilly’s stock price more than doubling in a blink.

But here’s the kicker: there’s potentially a lot more upside. Beyond tirzepatide, Lilly’s got a full deck with new drugs and a solid dividend that’s been fattening wallets at a rapid clip—up 101.6% in the last five years alone.

So, what’s the bottom line? If you’re looking to park some cash in a stock that has a track record of turning medical breakthroughs into gold, you might want to give Eli Lilly a closer look.

After all, betting on a company that’s leading the charge in medical innovation can sometimes feel like finding that $20 bill—only a lot, lot bigger.

Mad Hedge Biotech and Healthcare Letter

April 30, 2024

Fiat Lux

Featured Trade:

(HITTING CTRL+ALT+DELETE ON DRUG R&D)

(DNA), (GOOGL), (JNJ), (ILMN), (JNJ), (ALTO), (GROIV)

Forget your classic biotech launch story. One of 2024's most lavishly funded biotech upstarts is taking a massively ambitious swing at reinventing the entire drug development process.

I'm talking AI, venture billions, and some serious star power all rolled into one wild capital extravaganza.

The company behind this cash-flushed disruption bid is Xaira Therapeutics. And they've snagged a bona fide heavy hitter as CEO — Marc Tessier-Lavigne, the ex-president of Stanford and former chief science officer at Genentech (DNA).

His mandate is simple: turn Xaira's billion-dollar AI vision into cold, hard, realized potential.

Tessier-Lavigne is a true believer when it comes to AI's potential for transforming every clunky, painfully inefficient step of conventional drug R&D. We're not just talking incremental improvements here.

The man thinks smart deployment of generative AI could legitimately deliver "two- or three-fold" increases in both speed AND success rates across the entire confounding slog of getting new medicines approved.

That's one heckuva rallying cry.

But Tessier-Lavigne has legitimate grievances with the antiquated status quo. We all know the drug development game is brutal.

By most credible estimates, only about 1 in 10 drug candidates that make it to human trials ever get approved for use. Attrition rates are staggering, even before reaching those do-or-die clinical trials – that's money, research hours, and hope down the drain.

Xaira plans to flip that script. Their pitch: AI is their ace in the hole.

We're talking about designing entirely new drugs from scratch, pinpointing disease targets faster than ever, and finally cutting those mammoth clinical trials down to size. Think of it as the entire process of getting a machine learning upgrade.

And they're not starting from zero. Xaira tapped into the brains behind groundbreaking protein science: biochemist and computational biologist David Baker's team at the University of Washington. These are the geniuses who revolutionized protein structure prediction, and several of their top scientists are now on Xaira's payroll.

For the key task of AI-driven lead design, Xaira is leaning heavily on the advanced protein modeling systems developed in David Baker's acclaimed lab at the University of Washington.

To actually design the new candidate drug molecules, Xaira is deploying advanced AI systems developed in Baker's lab. We're talking cutting-edge tech like RFdiffusion and RFantibody.

These use similar "diffusion" AI architectures that power viral image generators like DALL-E, except instead of churning out weird digital art, they generate brand-new protein structures from scratch.

On the biology side, Xaira has assembled specialist teams from genomics titan Illumina (ILMN) and proteomics upstart Interline Therapeutics. The goal is to use AI to decipher complex disease mechanisms on a molecular level at an unprecedented scale and quality.

As for the money side, Xaira's co-founders are a duo of biopharma's biggest VC shot-callers: Bob Nelsen from ARCH Venture Partners and Vik Bajaj, who leads the investment crew over at Foresite Capital's in-house incubator.

The rest of Xaira's bulging investor list reads like a who's who of the VC world's heaviest hitters from coast to coast.

But let's get one thing straight: deploying AI for drug discovery itself isn't new. Investors have poured hundreds of millions into previous AI-oriented biotech upstarts with remarkably little tangible progress to show for it so far.

That’s why plenty of scientists remain deeply skeptical about the real-world viability of using in silico methods to design brand-new proteins capable of becoming actual medicines.

But Xaira's leaders are taking an unmistakably bullish stance. As Tessier-Lavigne brazenly stated, "We believe the technology is ready for making therapeutics today. And it's only going to get better and better going forward." Shots fired.

And this startup isn't just flexing impressive scientific ambition and bravado, either.

Xaira's boardroom and executive lineup is stacked with certified rockstars spanning the lofty peaks of biopharma's regulatory, academic, and corporate pillars.

The company's board alone includes former FDA head Scott Gottlieb, Stanford chemist Carolyn Bertozzi (you know, the Nobel laureate), and even ex-Johnson & Johnson (JNJ) CEO Alex Gorsky.

Clearly, this isn't some penny-ante upstart's advisory council.

Speaking of going big, let's talk about Xaira's huge VC funding for a minute. Their over $1 billion haul puts them in a seriously elite company among the top five largest VC-backed biopharma raises of all time.

We're talking the same rarified air as anti-aging disruption play Altos Labs (ALTO) and Roivant Sciences' (ROIV) $1.1 billion mega round from 2017.

That's an outrageously rich launch valuation for an upstart AI biotech without a single disclosed pipeline product. But it reflects the blazing hot enthusiasm and optimism around applying machine learning to overcoming drug development's biggest bottlenecks and inefficiencies.

In that vein, Xaira's most direct competition comes from other prominent AI drug trailblazers like Alphabet's (GOOGL) Isomorphic Labs and Flagship Pioneering's Generate Biomedicines.

All three of these hyper-funded disruptors are in a race to develop superior AI systems for accurately modeling protein structures or generating wholly new proteins from digital representations.

Of course, Xaira's monster ambitions will ultimately live or die based on tangible results and clinical execution over the long haul.

Love it or hate it, though, the great AI-powered biopharma upheaval is officially underway thanks to Xaira's monster VC haul. Whether the company can truly live up to its gargantuan hype and disruption premise, well, that multi-billion dollar enigma should start getting some added clarity in the not-too-distant future.

Let's see if these self-professed drug R&D revolutionaries have the disruptive chops to put their lofty money where their mouths are.

Mad Hedge Biotech and Healthcare Letter

April 25, 2024

Fiat Lux

Featured Trade:

(RACING TO SWAP A GOLDEN GOOSE FOR A NEW FLOCK)

(MRK), (NVO), (LLY), (JNJ), (ABBV), (PFE)

Big pharma usually makes investors smile - fat profits, juicy dividends, and stocks that crush the market.

Lately, though, some of these giants are looking more like grumpy old men. Sure, there are exceptions like Novo Nordisk (NVO) and Eli Lilly (LLY) printing money with their obesity blockbusters.

But what about the rest? Even with Washington breathing down their necks, patent cliffs, and a shaky economy, you'd think these drug titans wouldn't be lagging the market, right? Wrong.

Check out the "Big Eight" top dogs - Johnson & Johnson (JNJ), Merck (MRK), AbbVie (ABBV), Pfizer (PFE), and the rest. Only a few have really delivered the goods in the past five years. AbbVie and Merck have been alright, but the others? They make me want to take a nap.

Now, I'm not saying give up on pharma entirely - there's still money to be made. But you've got to do your homework. Today, let's take a look at Merck.

They raked in $60.1 billion in 2023, making them a heavy hitter. But without their COVID cash machine Lagevrio, growth is...less impressive. Still up, but not setting the world on fire.

The real story is spending - Merck went on a spree, burning through cash on R&D. Why? Their golden goose Keytruda, that $25 billion cancer blockbuster, is facing generic competition soon.

Merck isn't just sitting around waiting for the Keytruda patent cliff either. They're furiously throwing money at new drugs, acquisitions, cancer, heart disease, immune disorders - hoping to find the next Keytruda before the current one fades away. It's like an aging rockstar desperately trying to write another big hit.

But let's be real, finding billion-dollar breakthroughs is a gamble, even for giants like Merck. They've got potential in the pipeline for sure, but it's a long road from the lab to pharmacy shelves. Plenty of drugs flame out along the way.

Looking back, 2023 wasn't a victory parade for Merck. It was more like a mad dash to spend their way out of the looming Keytruda patent cliff. But hey, sometimes you've gotta break a few eggs to make an omelet, right?

Speaking of potential winners, let's talk about those newly approved lung drugs – sotatercept could be a major player.

Merck's vaccine department is looking strong too, with potential blockbusters targeting lung infections and RSV in the pipeline.

Of course, it hasn't all been smooth sailing. That new cough drug, gefapixant, getting rejected by the FDA again? Merck took a hit on that. Still, this biotech’s not giving up. This is a company buying time to build up a whole new arsenal, and the Keytruda cliff might hurt, but they'll come out swinging.

So, let’s forget about that 2023 earnings dip. Merck's forecasting a serious jump in 2024 profits as they dial back the crazy spending. Yes, their balance sheet took a hit, but look at what they're building. They're hunting big deals to bolster that pipeline, and that's a good thing in my book.

Speaking of big moves, Merck's been on a shopping spree. Wall Street might get nervous if they drop another bombshell, but I trust their judgment. These aren't just random buys; this is how they protect their future cash flows. Besides, any short-term drama from a big deal could be a sweet buying opportunity.

And while Merck’s still figuring out which one could be the next big thing, the true star of the show, until that patent cliff arrives, is still Keytruda.

That beast is still growing and could keep going strong for years, especially in early-stage treatments. Plus, that new subcutaneous version of this blockbuster treatment? Talk about extending the gravy train well past the generic competition.

Let's also check out the other horses in this race: sotatercept's early sales numbers, a potential FDA approval for that HER2 drug, the saga of gefapixant's third shot (or not), and the cash potential of V116 and Welireg. Not to mention, juicy updates on that Moderna (MRNA) partnership…Merck’s next months could be packed with surprises.

As for this company’s dividend? Decent track record, but don't expect fireworks after the recent hike. As for buybacks, Merck seems to have...other priorities right now. Those profits are pouring straight into the growth pipeline.

The bottom line: While some of Big Pharma looks pale lately, Merck is still bringing it, share price gains and all. Sure, that gefapixant rejection stings. But Keytruda keeps roaring, and Merck's pipeline is buzzing with potential. I'm not sweating earnings.

Merck's got contingencies lined up for the Keytruda patent apocalypse - new drugs, deals, maybe even extending Keytruda itself. They're playing for the long game here. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

April 23, 2024

Fiat Lux

Featured Trade:

(A DRUG KINGPIN HIDING IN PLAIN SIGHT)

(ABBV)

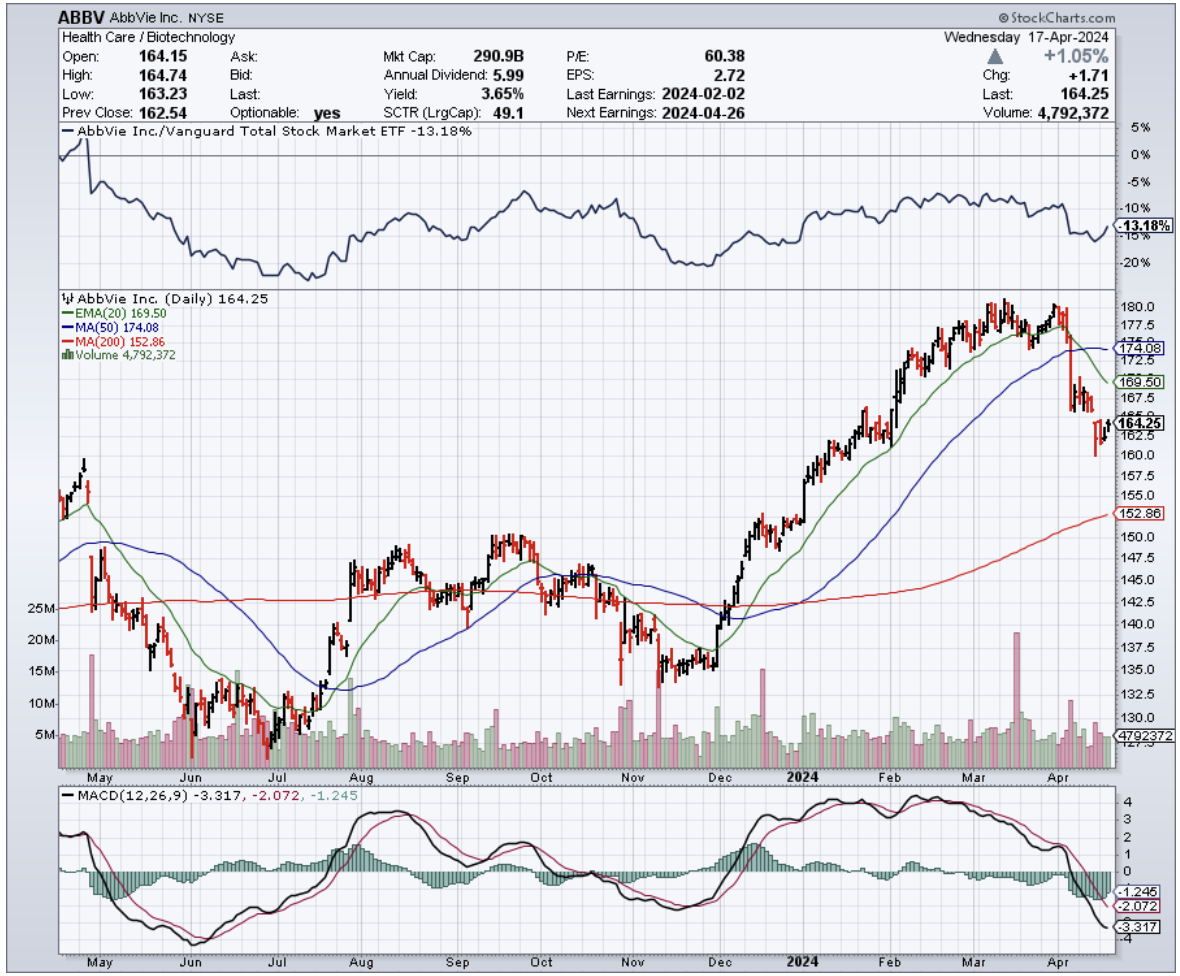

Have you ever thought about big pharma stocks as potential goldmines? I mean, we usually don’t gossip about the likes of AbbVie (ABBV) over lunch, but maybe we should.

After all, those unassuming pharma giants could be hiding some serious potential for your portfolio. Let's dive into whether investing in AbbVie might just be your ticket to millionaire status.

Admittedly, AbbVie isn’t your typical headline grabber unless it’s about their next big thing in medicine. They’ve got a real knack for plucking the right strings in R&D, which not only keeps them competitive but also paves the way for massive returns.

Case in point: Humira. This blockbuster drug treats everything from arthritis to psoriasis and even though it’s facing generic competition left and right, it still bagged $14.4 billion in sales in 2023. That's no small potatoes, considering it’s a chunk of AbbVie's hefty $54.3 billion revenue.

So how does AbbVie keep the Humira money train rolling? They play smart with pricing and patents, and they've got a backup band ready with new drugs like Skyrizi and Rinvoq. These two are set to take over the stage with projected sales hitting a sweet tune of $27 billion by 2027.

And let me tell you, the transition from Humira to these newcomers is like swapping an old favorite band’s vinyl for their latest digital remix — just as good, if not better.

But here’s the deal. AbbVie isn’t just remixing their old hits. They’re producing whole new albums. With every new drug approval, they’re not simply aiming to keep up — they’re looking to lead the charts. And with their pipeline promising a few more blockbusters, it looks like AbbVie could keep the record-topping releases coming.

Take their recent shopping spree for example: snapping up Cerevel for a cool $8.7 billion. This isn’t some random acquisition. It’s a strategic move that bolsters AbbVie's impressive neurology treatment portfolio.

Cerevel is close to getting approval for a new schizophrenia drug, a game-changer that could redefine how we treat this debilitating disorder. Traditional medications often have harsh side effects, but Cerevel's new class of drugs shows promise in minimizing those risks. Think of it as a gentler approach that still packs a punch.

And there's serious money in this space. The neurological market is huge – around $3.82 billion – and growing fast.

Once Cerevel gets its FDA nod, I'm projecting revenues of around $200 million by 2025, and that's just scratching the surface. They could grab a hefty 2% market share by 2028.

But their ambition doesn't stop there. AbbVie wasn't content with just rocking the neurology charts. They also went and snagged ImmunoGen earlier this year for a whopping $10.1 billion, marking their entry into the lucrative battle against solid tumors.

ImmunoGen has this cutting-edge technology called antibody-drug conjugates (ADCs) – it's like guided missiles that pinpoint cancer cells while leaving healthy ones unharmed.

Their drug, Elahere, already got the green light last year for ovarian cancer and raked in a cool $246 million in just nine months. And that's just the start.

The ovarian cancer market is a beast, valued at $4.35 billion and growing rapidly. I predict Elahere's sales could skyrocket to $1.6 billion by 2028.

Now, let’s talk dividends because who doesn’t like a good payout?

AbbVie’s rocking a forward-dividend yield of 3.4%, and they've been increasing their dividends for decades. It’s like getting a steady rhythm of cash that just keeps getting louder.

And don’t forget about the share buybacks. AbbVie bought back nearly $2 billion of its own stock in 2023. That’s a lot of faith in their future hits and a sign that they’re betting big on their own success.

So, sure, AbbVie isn’t going to make you a millionaire overnight — it’s not a lottery ticket. But if you’re in the game for the long haul, this stock could be a key player in your wealth-building lineup.

With a solid track record, a pipeline full of potential, and a strategy that’s clearly focused on growth, AbbVie is looking like a pretty smart pick. I suggest you buy the dip.