Mad Hedge Biotech and Healthcare Letter

March 14, 2024

Fiat Lux

Featured Trade:

(TIPPING THE SCALE)

(NVO), (LLY), (VKTX), (PFE), (TSLA)

Mad Hedge Biotech and Healthcare Letter

March 14, 2024

Fiat Lux

Featured Trade:

(TIPPING THE SCALE)

(NVO), (LLY), (VKTX), (PFE), (TSLA)

Imagine, if you will, me sitting down for my morning coffee, flipping through the latest in the biotechnology and healthcare world, when I stumble upon a story that's about as juicy as they come in the world of pharmaceuticals.

The headline? Novo Nordisk's (NVO) stock is on a joyride to the moon, courtesy of their latest heavyweight champ in the weight-loss drug arena, Amycretin.

And let me tell you, this isn’t some minor upgrade. This new candidate is like Wegovy's bigger, bolder cousin.

Now, for those of you who've been tracking the pulse of the market with me, you know I've got a soft spot for stories like these. It's not every day you see a drug come out swinging, making Wegovy look like it's been skipping gym sessions.

As for Novo, the stock didn't just jump following the reports about Amycretin’s performance. It practically did a backflip, soaring over 7% in Copenhagen. And Stateside? We're talking an 8.4% leap to a whopping $135.28. Yes, my friends, that's record-breaking territory.

Let me put this into perspective. Novo Nordisk, with this surge, practically eyeballed Tesla's (TSLA) market value and said, "Hold my beer."

We're talking about a market cap north of $560 billion. Makes you wonder if Elon's feeling the heat, doesn't it?

But this isn’t the last time we’ll hear about Wegovy. Novo’s former golden child of weight loss hasn't been kicked to the curb yet. Far from it.

In fact, the US Food and Drug Administration (FDA) recently stamped it with a seal of approval for reducing heart attack and stroke risks.

This is huge. Why? Because it cracks the door wide open for Medicare coverage. And considering more than 40% of American adults are wrestling with obesity, that's no small target market.

Now, I hear you asking, "But isn't Wegovy's price tag a bit... steep?" Sure, at over $16,000 annually, it's not chump change.

Still, this approval could shift the entire healthcare chessboard. Imagine, medications that once were shrugged off by insurers now potentially becoming mainstays in treatment plans. More importantly, this decision could lead to a surge in demand like never before.

Let me explain why. Prior to this FDA approval, insurers were practically turning their noses up at coughing up the cash for these types of meds. Despite that, folks were clamoring for Wegovy like it was the last slice of pizza at a party.

What do you suppose happens now that Wegovy's got the golden ticket for conditions that insurance can't help but cover? I mean, we're about to see demand go from "Please, sir, I want some more" to a full-blown Oliver Twist riot.

Given this demand, it’s no longer surprising that the scene is getting crowded with competitors itching for a piece of the pie.

Eli Lilly's (LLY) not sitting this dance out, with Zepbound and Mounjaro drawing eyes and opening wallets. Actually, analysts are already placing bets, with some forecasts shooting as high as $60 billion by 2030 across various applications.

Aside from the established names in this niche, there are also up-and-comers like Viking Therapeutics (VKTX) with its impressive trial results for VK2735. Then there's Pfizer (PFE), fumbling a bit with orforglipron but not out of the game yet.

For all of us watching all these unfold, this is the kind of narrative we live for. Novo Nordisk's Amycretin and the bustling competition in the obesity drug market are not just stories of medical innovation; they're tales of market intrigue, investment opportunities, and, yes, a bit of drama.

Before getting in the fray, I suggest you wait for the dip. For now, just grab your popcorn (low-cal, of course) and stay tuned. This biotech thriller is just getting started, and something tells me the plot twists are going to be worth the price of admission.

Mad Hedge Biotech and Healthcare Letter

March 12, 2024

Fiat Lux

Featured Trade:

(A BIOPHARMA'S RESURRECTION FROM PATENT PURGATORY)

(BMY), (PFE)

So, Bristol-Myers Squibb (BMY), that old stalwart of the biopharma world, is making a comeback, and not just any comeback.

After what seemed like an eternity in the doldrums, with sales taking a hit left and right thanks to the expiration of patents on blockbuster drugs like Revlimid, this giant is stirring again.

And let me tell you, it's about time. My take? Keep a keen eye on BMY because this phoenix is rising.

To put things in perspective (and explain why I’m excited about this), let's not forget this little nugget: in the past year, Bristol-Myers was practically the only biopharma not to get an invite to the price surge party, apart from Pfizer (PFE), which took a 33.4% nosedive. Ouch.

Now, for the important details. After five quarters of watching sales dip like a roller coaster on the downward run, Bristol-Myers is back with a bang — or at least, a firm step in the right direction.

Although the company reported a slight 2% dip in annual sales to $45 billion, the underlying story is one of renewal and optimism. For the first time in a while, there are tangible signs that the company is navigating its way out of the patent purgatory that had ensnared its revenue streams.

Diving into the deep end, their LOE drug revenue shrunk to $7.1 billion in 2023, with Revlimid sales plummeting 36% to a mere $1.45 billion in the fourth quarter alone.

Yet, there's a glimmer of hope with new bloods like Reblozyl and Breyanzi, racking up a cool $423 million in Q4 sales between them.

Meanwhile, the bread and butter of Bristol-Myers, their in-line product portfolio, pulled in $34.3 billion, managing a modest 3% growth last year.

But here’s where it gets interesting: their new product portfolio skyrocketed by 77%, touching $3.6 billion for the year. As we waved goodbye to Q4, these new products were nearly outselling the old guard.

Sure, they're still the newbies, but their slice of the revenue pie jumped from 4.4% in 2022 to about 8% in 2023.

Add to that the success of their cancer treatment Opdivo, which enjoyed a 9% revenue bump, and you've got reasons to be cheerful.

Plus, with the market whispering sweet nothings of a return to growth, with sales expected to hit $46 billion in 2024, it’s hard not to get a little enthusiastic.

Let’s also not forget where Bristol-Myers shines: they've got a knack for snapping up small biotechs, keeping R&D spending savvy while hunting for the next big breakthrough.

In 2023, they're sitting pretty with a $7.51 EPS and operating cash flows to the tune of $14.0 billion. Translation? They've got the war chest to fund their growth crusade starting in 2024.

More importantly, Bristol-Myers has an extremely diverse portfolio.

It's like they've got their fingers in every pie – or, in this case, a smorgasbord of drugs tackling everything from the nitty-gritty of Oncology and Hematology to the intricacies of Immunology/Fibrosis and Cardiovascular health.

This isn't your run-of-the-mill, all-eggs-in-one-basket kind of deal. While some pharma giants are playing a high-stakes game banking on a single blockbuster or a handful of hopefuls, Bristol-Myers’ playing it smart with a kaleidoscope of treatments across the board.

To date, they've got over 12 assets strutting towards the registrational phase with another 30 doing the early-stage clinical studies. If that doesn't scream "long-term growth and earnings potential," I don't know what does.

Looking ahead to 2024, the brass at Bristol-Myers is promising "low-single-digits" revenue growth, while eyeing an EPS somewhere in the neighborhood of $7.10 to $7.40.

Sure, that might look like a step back from 2023's $7.51, but let's not forget their bill for their shopping spree – snagging Mirati Therapeutics for $14 billion isn't exactly pocket change, and neither is giving their new product lineup the grand tour.

What happens next? Well, the market loves a comeback story, especially in biopharma, and Bristol-Myers is penning a gripping narrative.

After a year that tested its mettle, Bristol-Myers is on the upswing, promising more thrills for investors. Admittedly, there might be some bumps along the way as they fold in their latest acquisitions, but any dips could be golden opportunities for the savvy investor.

I suggest you keep Bristol-Myers Squibb on your radar. This biopharma phoenix is just getting its second wind, and the journey ahead looks as promising as ever.

Mad Hedge Biotech and Healthcare Letter

March 7, 2024

Fiat Lux

Featured Trade:

(RALLY CAPS ON)

(VKTX), (LLY), (NVO), (AKRO), (GILD), (BMY), (AMGN), (PFE)

The biotech sector just flipped its rally cap inside out. After a brutal losing streak, it's clawing its way back. The SPDR S&P Biotech (XBI) exchange-traded fund, a barometer for the sector, started to show signs of life when it soared by 5.7% last month, cresting over $100 a share for the first time in two whole years.

While champagne might be premature, this comeback is heating up, and whispers of a full-fledged rally are echoing through Wall Street.

After a rough patch that kicked off in early 2021, seeing the fund take a nosedive of over 60% by late October 2023, the tide began to turn last fall. Initially, whispers of lower interest rates in 2024 sparked interest across small-cap indexes, including our biotech heroes.

Yet, lately, the buzz is all about biotech's own merits — think breakthrough medical trials and the juicy prospect of big pharma playing Pac-Man with smaller but promising biotech firms to beef up their drug pipelines.

And let me tell you, if the current rally's got legs, we might just be witnessing the most thrilling biotech comeback in over half a decade. Especially if the merger and acquisition scene stays hot, we could see biotech stocks climbing even higher.

Take everything that happened in the sector in February as an example. Viking Therapeutics (VKTX) threw down the gauntlet with promising data on its weight loss drug, VK2735, making investors sit up and take notice.

Actually, this candidate is shaping up to be a formidable rival to obesity treatments from Eli Lilly (LLY) and Novo Nordisk (NVO), sending Viking's shares skyward by a jaw-dropping 121% in a single day.

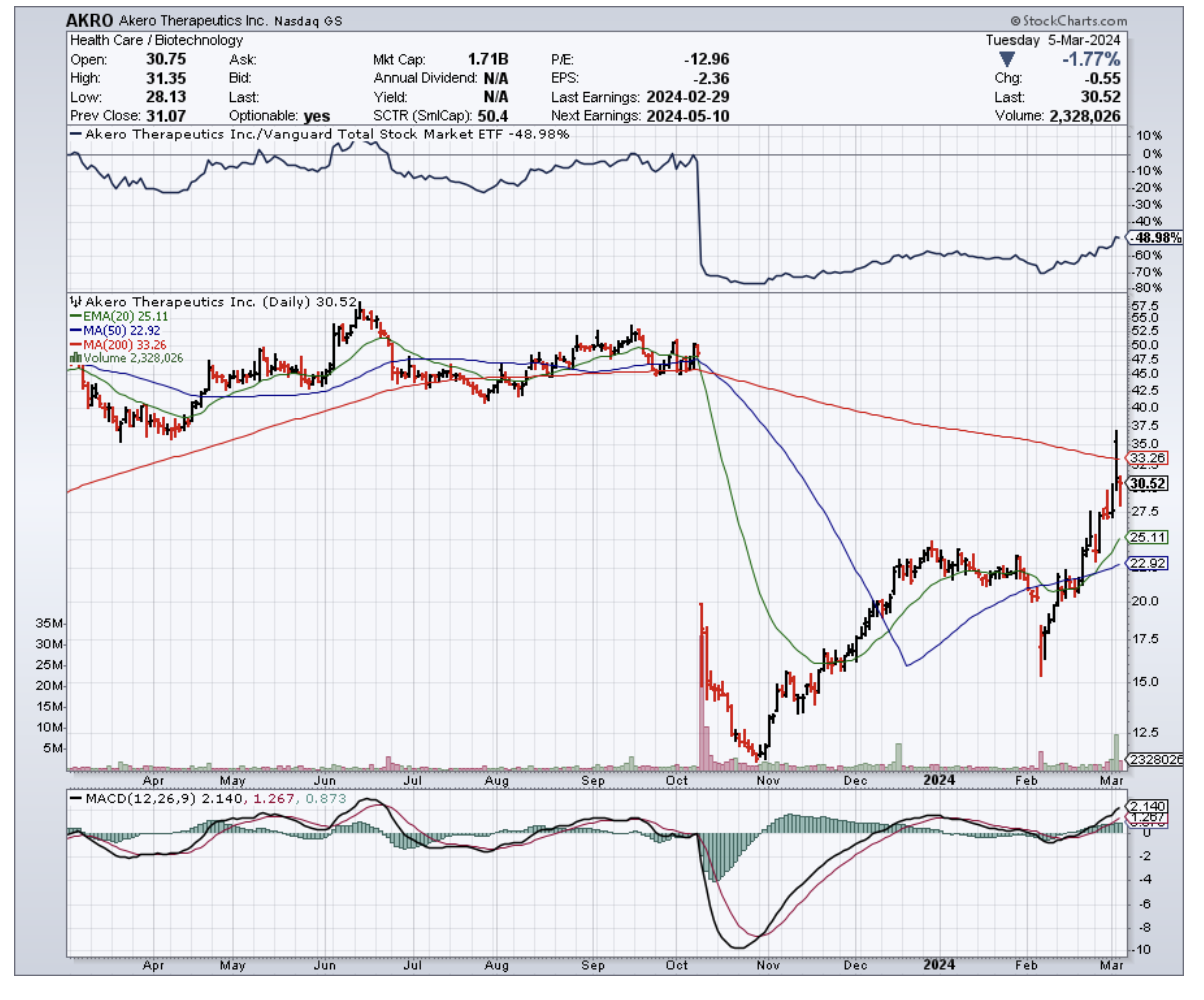

And it's not just Viking stealing the spotlight. Another biotech named Akero Therapeutics (AKRO) also bounced back with some impressive data of its own, challenging the doom and gloom that settled over biotech firms following Eli Lilly's bombshell MASH trial results.

Akero's mid-stage study showed that their drug, efruxifermin, could significantly roll back liver fibrosis in MASH patients — putting a whopping 75% of high-dose recipients on the mend, a stark contrast to the 24% placebo group.

This revelation was a game-changer, especially after Lilly's tirzepatide threw the sector for a loop, hinting at a potential endgame for MASH-specific treatments. But while Lilly's announcement left many details to the imagination, Akero's clear-cut results have reignited excitement over what might be the best MASH treatment yet seen.

As expected, in the midst of this resurgence, the likes of Viking and Akero are catching eyes not just for their groundbreaking treatments but also as tantalizing acquisition targets. Heavyweights like Gilead Sciences (GILD), Bristol Myers Squibb (BMY), Amgen (AMGN), and Pfizer (PFE) are said to be circling, each eyeing a slice of the biotech pie.

As for the biotech investment landscape in general, it's buzzing with renewed vigor. The early months of 2024 have welcomed a smattering of biotech IPOs, a refreshing change after a long drought. CG Oncology's late January debut practically set the market ablaze, doubling in value on its first trading day.

Moreover, public biotechs have found a lifeline in PIPE deals, sidestepping the regulatory hoops of secondary offerings. For instance, Denali Therapeutics' (DNLI) recent PIPE deal, expected to rake in $500 million, is proof of the sector's warming investment climate.

So, dust off those rally caps because the biotech sector isn't just back in the game – it's swinging for the fences.

Breakthrough treatments, a sizzling M&A market, and investors throwing their support behind innovation — this rally has all the ingredients to paint a bright future for the industry. While there will be bumps along the road, one thing's for sure: the biotech sector is poised for a season no one wants to miss.

Mad Hedge Biotech and Healthcare Letter

March 5, 2024

Fiat Lux

Featured Trade:

(THE SKINNY ON ECONOMIC GROWTH)

(LLY), (NVO), (AMGN)

What might just give economies a bigger jolt than the frenzy of the Super Bowl or a jampacked Taylor Swift world tour? If you guessed the recent buzz around weight-loss drugs, take a bow. You see, it's not just about slimming waistlines anymore – these breakthrough medications could be a game-changer for the whole economy.

But first, a sobering reality check: health issues have been nibbling away at the U.S. labor force like a sneaky termite over the last 30 years, shaving off two to three percentage points.

Then there's the matter of early departures from this mortal coil, chipping away another 0.2 percentage points from annual labor growth.

Not to mention the legion of unsung heroes caring for the ailing, effectively benched from the workforce, leading to a 3% labor force deficit.

Among all the health issues affecting the labor force, obesity has been identified as a sneaky little gremlin, dragging down productivity and participation in the workforce.

With obesity affecting 40% of the U.S. population, we're talking about a hefty 1% slash in total output.

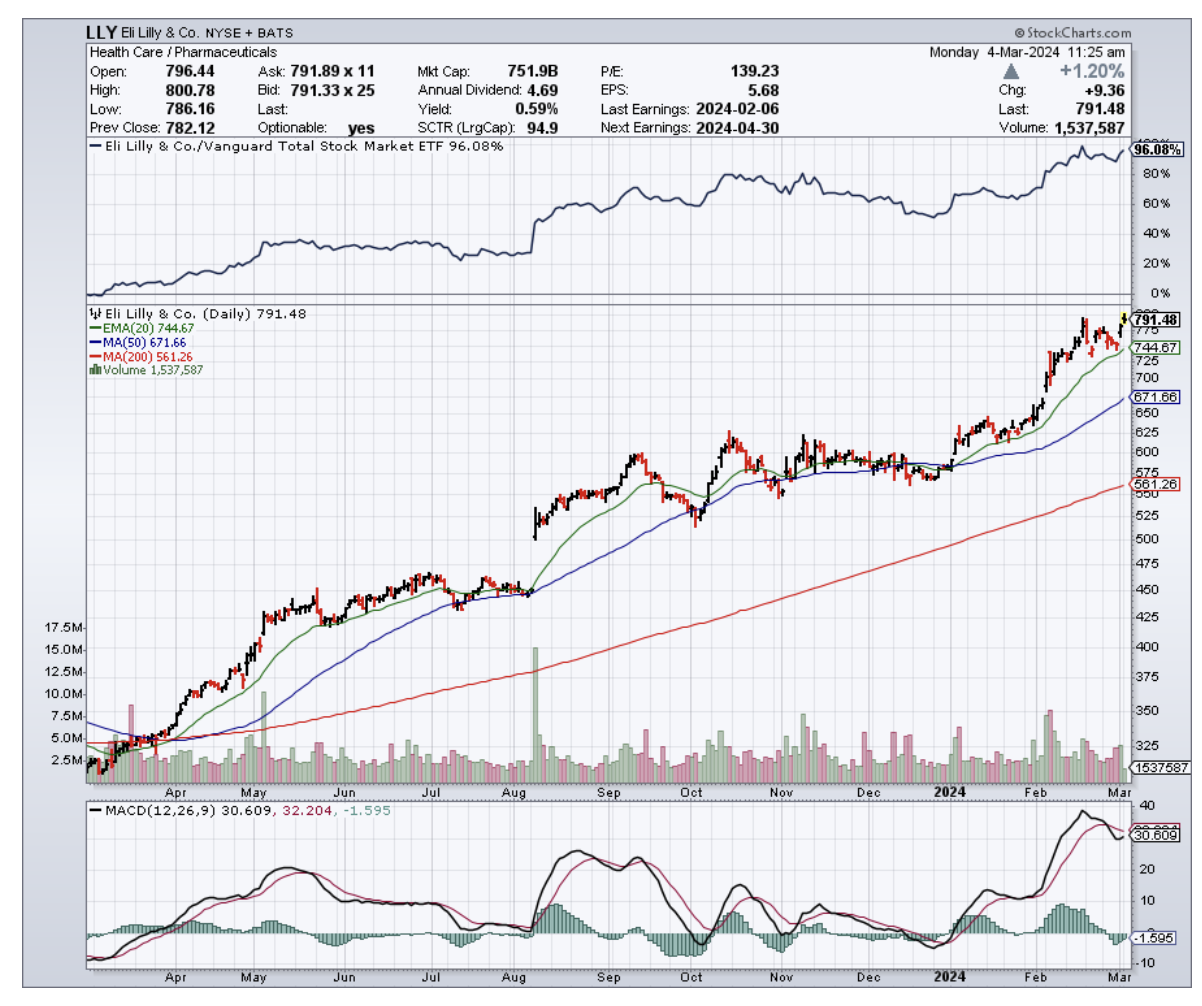

But what if there was a way to combat this? Enter stage left: Eli Lilly (LLY). Sure, you might know them as a big-league player in the pharma world, but did you know they're the brains behind blockbuster medications like Trulicity, Mounjaro, and cancer-battling Verzenio?

And the story gets even more exciting – it's not just their existing all-star lineup that's sent their stock soaring 180% since 2021. Their latest weight-loss marvel, Zepbound, got the FDA's green light last November. Think of it as Mounjaro's twin, sporting the same molecule but with a different name to keep things clear for their existing diabetes patients.

This breakthrough signals a massive shift in the obesity treatment landscape. The global anti-obesity market is projected to explode to a staggering $100 billion annually by 2030 – a dramatic leap from last year's $6 billion. To put that in perspective, global spending on cancer treatments is estimated at $220 billion this year.

Naturally, Lilly is poised to grab a big slice of that pie. Analysts are predicting a healthy 21.4% revenue boost this year, and nearly 24% by 2025. Talk about a growth spurt.

As for earnings? They're looking at nearly tripling in that timeframe. The future's so bright, Lilly might need shades.

But here's the catch: Lilly's stellar rise has its stock priced at a premium, and then some. We're talking 60 times this year's expected earnings. And while the company's profit train is set to chug along, not every stock can keep up those lofty valuations in the long haul.

And let's not forget about the competition. Novo Nordisk (NVO), with its own contenders Ozempic and Wegovy, is nipping at Lilly's heels, even as Amgen (AMGN) and others are hot on the trail with promising candidates of their own.

Yet, Lilly's not sweating it. With Zepbound (aka Mounjaro for the weight-conscious) already making waves as a go-to for obesity treatment, they're sitting pretty. It's like they've already won half the battle, with doctors and patients already in the know about this not-so-secret weapon.

Still, as tempting as it might be to hop on the Lilly bandwagon after seeing those numbers, we need to do a quick reality check before investing. It's important to remember that every stock has its ups and downs.

For starters, Lilly's stellar rise means their stock is trading at a premium – a hefty 60 times this year's expected earnings. And while the company's profit train is definitely chugging along, that kind of lofty valuation might be a bit too spicy for some investors' taste, especially in the long run.

So, what's the takeaway for those who want in on the action? Lilly's current price tag might give you pause, especially if you're looking for a bargain.

It's been a wild ride for this stock, and sometimes the best moves involve waiting for the market to catch its breath.

However, their dominant position in a rapidly expanding market definitely makes them a player worth watching closely. I suggest to buy on the dip.

Switching gears for a second, let’s take a look at the big picture. It turns out that widespread use of GLP-1 medications like Lilly's could deliver way more than just individual weight loss. We're talking about a potential shot in the arm for the entire U.S. economy.

Think about it: if 30 million Americans hop on the GLP-1 train with drugs like Mounjaro and Zepbound, and a conservative 70% of them see benefits, we could see a 0.4% boost in the U.S. GDP. And that's just the starting line.

In a best-case scenario, where 60 million Americans embrace these treatments and a whopping 90% benefit, the GDP could potentially surge by a full 1%. Even with more modest projections, with 15 million users and a 50% success rate, the economic impact would still be noteworthy.

This isn't just pocket change – it's serious economic muscle. With the right push, these weight-loss drugs could be the breakthrough prescription our economy needs, adding some serious pep to our growth alongside countless individual health transformations. Now, isn't that a story worth following?

Mad Hedge Biotech and Healthcare Letter

February 29, 2024

Fiat Lux

Featured Trade:

(A LEAN, MEAN, HEALTHCARE MACHINE)

(MDT)

I admit that predicting where the S&P 500 will land in the next six months is a bit like guessing the next flavor of the month at your local ice cream shop — exciting but wildly unpredictable.

However, history has shown us that over a decade, it's more like betting on the sun rising in the east — pretty darn reliable for those looking to fatten their wallets.

Now, I'm not suggesting you throw your hard-earned cash at just any company that pops up in your stock app. No sir, we’re here for the smart picks.

And who's on my radar today? None other than Medtronic (MDT).

Let’s talk about why this healthcare giant could be the golden goose of your investment portfolio for the next decade.

Imagine a company that’s pretty much the Swiss Army knife of the medical device world, simplifying the lives of patients in 150 countries and tackling over 70 health conditions. Sounds like a dream, right? That’s Medtronic for you.

Sadly, it hasn’t been all sunshine and rainbows for this medical device company. Recently, Medtronic's growth has been more sluggish than a snail on a leisurely stroll, with revenues dipping ever so slightly in the latest fiscal year.

Blame it on COVID-19, people dodging doctor visits, or supply chain snafus; the healthcare sector has been through the wringer.

But, just when you thought it was all doom and gloom, Medtronic surprises everyone with a 4.7% revenue bump in its latest quarter.

With new gizmos and gadgets rolling out and an aging population that’s only going to need more medical attention, Medtronic is poised for a comeback.

Looking at the company’s trajectory and portfolio, I’m inclined to agree with optimists singing tunes of a 5.9% compound annual growth rate for the global medical device market till the decade's end. Considering that Medtronic is positioned in front of this segment, it doesn’t take much convincing that this stock is set for growth in the next years.

That’s not all though. Medtronic is trimming the fat by saying sayonara to its ventilator business, embracing a leaner, meaner approach.

Specifically, it plans to merge the remaining gems of its patient monitoring and respiratory interventions segment into a dazzling new business unit: acute care and monitoring.

Ultimately, the goal is to beef up organic revenue growth and buff up those financials. As they gracefully exit stage left from the ventilator biz, any lingering revenue from these machines will play a cameo in the “other” section of its financials, starting next quarter.

And let’s talk numbers for additional context, because who doesn’t love a good success story?

Over the last three quarters, Medtronic has been strutting its stuff with earnings just north of $3 billion on a revenue runway of $23.8 billion, flaunting a profit margin of 12.6%.

Not too bad, right? Still, there’s room to grow those figures, and a beefier profit margin means a happier ending for investors, with the stock potentially hitting new highs.

Can Medtronic truly follow through with a growth story? Well, its history says yes.

Medtronic's revenue has ballooned by 88% over the last decade, a feat that's as impressive as fitting into your high school jeans.

A significant chunk of this growth spurt came from its $42.9 billion acquisition of Covidien in 2015, which did more than just add a few zeros to its balance sheet — it catapulted Medtronic’s product portfolio and European presence into the stratosphere.

After that, the company continued to expand through a series of mergers, acquisitions, and good old-fashioned organic growth.

Peering into the crystal ball, there’s a strong potential that Medtronic will keep the growth party going at a steady clip of 4% annually in the medium term.

Let’s also not forget about dividends. Medtronic is the kind of company that keeps the dividend party going, having increased its payout for an impressive 45 years. Despite a modest bump this year, the future looks bright for dividend lovers.

So, should you buy Medtronic stock?

If you’re in it for the long haul, Medtronic seems like it's gearing up for an exciting journey. With a leaner, meaner approach and a market ripe for the taking, Medtronic's future looks bright. I suggest you buy the dip.