Mad Hedge Biotech and Healthcare Letter

October 11, 2022

Fiat Lux

Featured Trade:

(A GUARANTEED WIN IN HEALTHCARE)

(PFE)

Mad Hedge Biotech and Healthcare Letter

October 11, 2022

Fiat Lux

Featured Trade:

(A GUARANTEED WIN IN HEALTHCARE)

(PFE)

The previous month was another difficult time for the markets, with the S&P 500 sliding 9%. Meanwhile, the index has already fallen 24% year to date, dragging several quality businesses along with it.

The silver lining for long-term investors is that many of these beaten-down stocks won’t remain down for long. That means buying flailing quality stocks today, as risky as it may sound, could offer you an opportunity to lock in several high-yielding businesses at cheaper valuations.

In the biotechnology and healthcare world, one of the most promising buys so far is Pfizer (PFE).

This company’s stock price has fallen by 16% in the past six months as Pfizer’s COVID-19 vaccine profits are anticipated to decrease. However, there’s something that investors appear to be overlooking.

The sales of the COVID-19 vaccine, Paxlovid, may gradually decrease, but the fact remains that its bolstering Pfizer’s pipeline. While its bottom line will expectedly show signs of decline as concerns around the coronavirus subside, its revenue won’t disappear completely.

Paxlovid sales are estimated to reach roughly $12 billion in the second half of 2022.

After all, health officials are continuing to administer booster shots, and there’s really no concrete answer if and when that will eventually end.

Moreover, Paxlovid is one of only two preferred antiviral treatments for patients at high risk for severe COVID-19. Based on CDC data, 50% to 60% of the US population aged 12 and above will experience one or more symptoms for progressing to a more severe stage of the disease.

This, along with the additional approvals in other countries, has reaffirmed the $22 billion revenue guidance for Paxlovid this 2022.

Needless to say, injecting this much cash flow into a company—even a large-cap business—would move the needle and put it in a very healthy financial position.

Pfizer’s continued strength amid the chaotic year can be seen in its second-quarter financial report in 2022. In fact, Pfizer reported its highest quarterly sales ever in its history in this quarter.

The company recorded its revenues increased to $28 billion, up by 47% compared to the $19 billion it reported in the same period in 2021. Its net income climbed by an impressive 78% year over year from $5.6 billion in the same period in 2021 to $9.9 billion.

This increase is driven by the substantial contributions of its COVID-19 products, Paxlovid and Comirnaty.

Hence, Pfizer has all but guaranteed that it can stay profitable and deliver outstanding results despite the anticipated decline in Paxlovid sales.

On top of that, the low earnings multiple indicates that a lot of bearishness was already built into the stock. But, the market’s fears seem to do little to slow down Pfizer.

Pfizer has increased its budget for R&D from $2.2 billion in the second quarter of 2021 to $2.8 billion in the same period in 2022.

The company has been aggressive in its decision to acquire several businesses in 2021 and 2022, growing its presence and expanding its portfolio.

More importantly, these new additions have transformed Pfizer into a more diversified company. For example, the company closed on the deal buying ReViral, which is a clinical-stage organization that focuses on treatments for the respiratory syncytial virus (RSV). The addition of ReViral’s resources provides a more solid direction for Pfizer’s ongoing RSV trials.

Aside from that, there are several additional opportunities for this drugmaker.

Pfizer is known to be able to consistently deliver positive free cash flow, which means it's in excellent shape to pursue expansion and growth opportunities while still comfortably paying out a solid dividend. Over the last five years, Pfizer has boosted its dividend by 25%.

So far, the company’s dividend yield is at 3.7%, which is more than twice the S&P 500 average of 1.8%.

Overall, Pfizer is a solid business with an expanding portfolio, a growing pipeline, tons of cash, and an impressive yield. It’s almost impossible to go wrong with this business, particularly at its low valuation these days.

Mad Hedge Biotech and Healthcare Letter

October 6, 2022

Fiat Lux

Featured Trade:

(A SOLID BIOTECH THAT CAN SURVIVE THE CRASH)

(GILD)

In years filled with virtually never-ending market volatility fears, the third quarter of 2022 seems to be one for the books.

We’ve gone through wild currency fluctuation, with the British pound practically free-falling to a record low against the US dollar.

The US Treasury yields rose to their peak since April 2011, while the S&P 500 is going into its third-consecutive quarter marked with losses for the first time since we experienced the 2008 financial crisis.

On top of these, the Federal Reserve disclosed that rates would climb even higher than expected as the previous month’s inflation data came in scorching.

The situation across the globe isn’t exactly showing any indications of improvement. Sanctions on Russia are becoming more severe following the Kremlin’s decision to annex certain areas of Ukraine formally. Meanwhile, emerging markets look to be down in the dumps as well.

Amid the market turmoil, some stocks managed to weather the storm and still hold the potential to deliver good results.

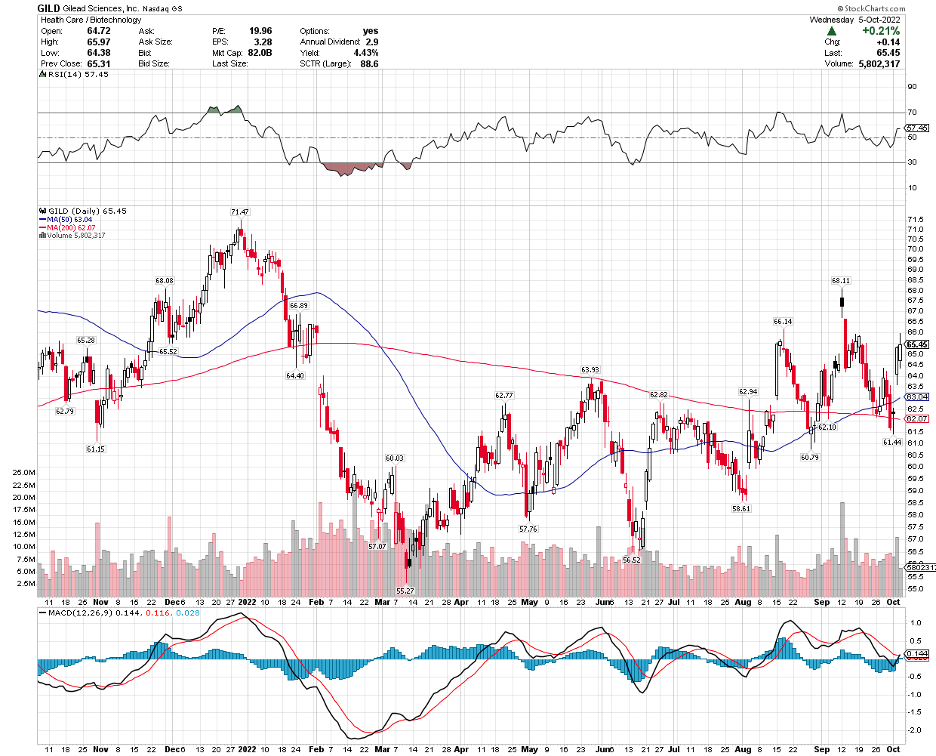

One of them is Gilead Sciences (GILD).

Gilead rose to fame when it launched an effective treatment for HCV, which came after its excellently timed (or lucky) acquisition of Pharmasset for $11 billion. This created a massive boost to the company’s business, with shares peaking at more than $100 per share in 2015.

With HCV finally having a solution, the boom did not last. Obviously, sales from the drug were not recurring since the patients were already getting cured.

At that time, Gilead bolstered its pipeline with a flourishing HIV business. However, the company’s revenues and earnings eventually became flat.

In the meantime, Gilead went after more expensive deals, including a $21 billion acquisition of Immunomedics to gain access to Trodelvy, a $12 billion contract with Kite Pharma to get their hands on Yescarta, and multi-billion deals involving Forty-Seven and Galapagos. Unfortunately, none of them delivered the same pay-off as the Pharmasset deal.

However, Gilead has been gaining traction recently.

Wall Street has been desperately looking for businesses that could help investors regain their losses, and it looks like Gilead is part of the very short list of companies that made the cut.

While it hasn’t exactly done anything groundbreaking as of late, the company’s consistency and foreseeable growth are boosting its attractiveness to investors.

Right now, Gilead’s HIV franchise is singlehandedly supporting the entire market cap of the stock. That’s impressive and promising, considering the company also has a burgeoning oncology sector.

For context, Gilead’s oncology franchise is estimated to hit roughly $5 billion in sales by 2030.

Meanwhile, Gilead has another HIV blockbuster making waves in Lenacapavir. Earlier in 2022, the company managed to expand the covered distribution channels of this HIV treatment and gained marketing authorization in the EU.

Given the current performance of its HIV franchise and the promise of expansion for Lenacapavir, this particular segment can be conservatively estimated to report at least single-digit growth through the early 2030s.

Overall, Gilead has been recording solid results for this year. In the first quarter, sales climbed 3% to $6.6 billion, partly thanks to its Veklury sales and the gaining momentum of its cell therapy business.

While growth was not as impressive, the 10% earnings yield, stability, and, of course, 5% dividend yield make Gilead a compelling choice. Admittedly, we’ve witnessed how interest rates climb higher, which results in additional competition for the 5% dividend yield, but the company appears to be holding up nicely in this aspect.

Gilead’s apparent independence from its COVID-centered product shows a highly encouraging trend. In August, Gilead shared its second quarter report showing revenues rising 1% to $6.3 billion. The “positive” note is that Veklury, a COVID-19 treatment, fell 46% while other products jumped 7% to contribute $5.7 billion.

Riding this momentum, Gilead shared another bolt-on deal worth $405 million to acquire MiroBio, a biotechnology company based in the UK. MiroBio develops treatments that aim to restore immune balance.

In summary, Gilead remains a solid bet in these trying times. It has established programs, which are expected to rake in higher earnings in the years to come, and an ability to execute great deals to bolster its pipeline—all while keeping its debts and costs well under control. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

October 4, 2022

Fiat Lux

Featured Trade:

(A POWERHOUSE BIOTECH GOING HIGHER)

(VRTX), (BIIB), (CRSP)

There is no single recipe for building wealth over the years. There are several ways to achieve this goal. However, a particularly effective one is recognizing solid businesses that deliver revenue and profit over time.

You can easily find many excellent candidates in the biotechnology and healthcare world. Actually, a lot of biotech stocks have managed to outperform the struggling market this 2022.

One name that emerged virtually unscathed from the onslaught of economic, political, and financial crises is Vertex Pharmaceuticals (VRTX).

Admittedly, the market downturn has yet to end. That means the company could still experience the effects of macro headwinds and tensions in the near future.

With that said, Vertex is one of the few companies equipped with the right tools to deliver excellent returns in the long run.

One of the reasons Vertex is at the top of the list in the biotech world is its history. The company has been generating solid returns for investors for quite a while now.

In fact, it has impressively surpassed the S&P 500 Index in the past 10 years.

Apart from that, Vertex continues to boost its revenue and profits courtesy of its monopoly in the market for treatments that target the underlying reasons or causes behind cystic fibrosis (CF).

Vertex is the market leader in the CF space worldwide. The company sells four therapies targeting this condition.

The company’s latest approval in this segment was for Trikafta, which received the green light in 2019. By 2021, Trikafta was already able to rake in over $5.6 billion in revenue.

Trikafta can be used as a treatment for up to 90% of CF patients. This number goes beyond any of those delivered by other Vertex products. More importantly, Trikafta will keep its patent exclusivity until the late 2030s.

That provides Vertex with plenty of time to make headway and expand the application of the product to cover previously untapped markets—a strategy that the company has been perfecting over the years.

Vertex has been busy winning approvals in new age groups and more reimbursements in several countries to ensure longer-lasting dominance in this segment.

Recently, the biotech has launched its Phase 3 trials for a candidate that may be an even better product than Trikafta.

While details have been kept under wraps, Vertex shared that the product would be a one-time curative treatment. Needless to say, this would translate to a massive payday for Vertex.

If everything goes according to plan, this new candidate might be launched by the first quarter of 2023.

At the same time, the biotech has been working on promising candidates for much-needed treatment areas, projected to generate billions of dollars in revenue.

This move is aligned with the strategy Vertex has been using over the years: target diseases with only a handful (if any) of safe and effective therapy options.

Among Vertex’s promising but ambitious programs is VX-880, a potential treatment for Type 1 diabetes.

While this could be a long shot, Vertex’s decision to buy ViaCyte for $320 million speaks volumes of the biotech’s seriousness about the endeavor. For context, ViaCyte is a private company focused on developing a functional cure for Type 1 diabetes.

This acquisition enables Vertex to add researchers who have been working on the same goal for years to contribute their expertise to the pipeline. Plus, ViaCyte can bolster Vertex’s manufacturing expertise for cell-based therapies targeting Type 1 diabetes.

Of course, there’s the work with CRISPR Therapeutics (CRSP) to develop gene therapies. Combining this collaboration with ViaCyte’s pipeline, which includes gene-edited cells created to evade the immune system, means Vertex could design a program eliminating the necessity for immunosuppressive therapy.

Meanwhile, there are other solid candidates in the biotech pipeline.

So far, Vertex has been having discussions with the FDA. The company has recently provided proof of concept data for its candidate for Exa-cel in sickle cell disease and transfusion-dependent thalassemia. Given the progress, the product should be slated for release by early 2023.

Another is VX-147, which is a kidney disease candidate that’s currently in crucial development. To date, the product is on track for accelerated approval and could start generating sales by late 2024.

On top of these, Vertex has been working on alternatives for opioids to avoid overdoses. Amid the growing concerns and data on the addictiveness of opioids, these continue to be prescribed as treatments.

This epidemic shows no signs of slowing down, with the CDC’s recent estimate increasing to 75,000 Americans dying from an overdose. According to the CDC, over 2 million Americans are addicted to opioids.

One explanation for this issue is that there is no effective alternative. While Vertex’s initial candidates failed to show an optimal profile, its latest candidate may very well be the answer.

The new candidate, VX-548, was created based on observations and research on families in Pakistan with the rare ability not to feel or experience any pain.

Due to this particular genetic abnormality, members of these families are able to walk on hot coals, get stabbed with knives, and jump from heights, and experience absolutely no pain at all.

The genetic mutation stops the peripheral nervous system from sending pain signals to the brain.

Vertex and other developers like Biogen (BIIB) are attempting to develop drugs that mimic the pain-blocking ability resulting from this genetic mutation.

If successful, VX-548’s greatest asset is its non-addictive potential, thereby making premium pricing more likely justified.

The current market for acute pain treatments annually is $4 billion, and that number is for generic pricing.

Considering that the pricing of a branded treatment would probably be at least double, then the commercial potential is massive.

Over the next 10 years, Vertex is expected to launch new biotech treatments which, combined with its current CF franchise, will propel its earnings, profit, and share price to even higher heights.

It’s currently facing the bear market without so much as breaking a sweat, with stock prices climbing by roughly 28% so far this 2022 compared to the market’s 19% decline. I suggest you don’t wait too long to buy into Vertex, as this is a top-tier biotech.

Mad Hedge Biotech and Healthcare Letter

September 29, 2022

Fiat Lux

Featured Trade:

(TAKING ON THE WEIGHT OF THE WORLD)

(LLY), (NVO)

This is not your run-of-the-mill weight-loss story.

The number of obese American adults has climbed from 13% to 43% in the last 60 years. That’s approximately 100 million individuals in the United States alone.

The average American male currently weighs about 200 pounds, up from 166 back in 1960, while the average female is at 171 pounds, up from 140.

Obesity, or just being overweight, has several ripple effects. This carries the risk of diabetes, cardiovascular issues, and even cancer. It can also interfere with a person’s work, sleep, and other day-to-day activities.

Many factors have been studied as potential reasons behind obesity, but it has become very clear that solving the epidemic would need more than simply diet and exercise.

Taking on this challenge are Eli Lilly (LLY) and Novo Nordisk (NVO), competitors that came up with a promising drug, known as incretins, to hopefully solve the issue.

Amid all the dietary fads, supplements, and exercise trends we’ve seen, we are on the cusp of finally getting safe and effective drugs for this condition.

We can go as far as claiming that these could very well be our best hope in the fight against obesity. This epidemic has been threatening the way of life of over 100 million Americans and roughly half a billion people globally.

Nobody has ever witnessed the weight loss offered by this new category of drugs, called incretins.

Scientific research has enabled people to shed over 20% of their weight. Needless to say, incretins could become the top-selling drugs in the history of the pharmaceutical industry.

For context, a drug is tagged as a “blockbuster” when it manages to record $1 billion in sales annually. To date, the top-selling drug worldwide is Humira from AbbVie (ABBV), with roughly $20 billion in yearly sales.

If each obese American sought treatment (and given the projected prices of these drugs) the yearly sales for incretins would hit at least a trillion dollars.

Obviously, insurers would refuse to pay these sums, which is why studies have been conducted to show how these drugs could effectively prevent critical conditions like diabetes and heart disease. That is, it will be considered a maintenance drug.

Marketing incretins as treatments for diabetes and obesity could rake in $50 billion to $60 billion in sales over the next decade. As of the moment, the market is dominated by a duopoly of Eli Lilly and Novo Nordisk.

Recently, Eli Lilly gained much attention after its diabetes drug Mounjaro received FDA approval. While the product was given the green light earlier in 2022, the company has also become more aggressive in marketing it as an anti-obesity treatment.

When it goes to market, Mounjaro is expected to go head-to-head against Novo Nordic’s Wegovy. Both target basically the same market, but Eli Lilly’s candidate showed better results.

According to Eli Lilly, patients given the highest dosage of Mounjaro recorded an average weight loss of 22.5% over roughly 18 months.

In terms of sales potential, Wegovy reached $183 million in the first quarter of 2022. With Eli Lilly hot on its heels, investors should expect a slide in Novo Nordisk’s sales for this product.

When Mounjaro was initially released, it was expected to reach peak sales of $15.4 billion. However, the drug’s effectivity and potential to address weight loss boosted predictions to $25 billion.

The reason for the increase in confidence in Eli Lilly’s drug is pretty simple. Offering treatment to 1.6 million Americans yearly would generate $20 billion in sales in the US alone—which only comprises 2% of the estimated population of obese individuals in the country.

Either way, it’s a massive market. Dominating a small portion would already move the needle for any biopharmaceutical company. Hence, I recommend you buy the dip for these companies aiming to solve the obesity epidemic.

Mad Hedge Biotech and Healthcare Letter

September 27, 2022

Fiat Lux

Featured Trade:

(LAST CHANCE AT SALVATION)

(BIIB), (ESALY), (RHHBY), (LLY), (NVS), (AMGN), (REGN), (BMY), (ABBV), (MRK), (PFE)

Biogen (BIIB) is taking another crack at Alzheimer’s. This is a crucial moment for the biotech following its move to abandon its plans to market Aduhelm, another Alzheimer’s treatment after healthcare insurers refused to pay for it despite gaining FDA approval.

The moment of truth will come this fall when Biogen and Eisai (ESALY) are anticipated to share the results of their massive trial created to determine whether lecanemab, their latest candidate for Alzheimer’s, can deliver its promise to decelerate the progression of the neurodegenerative condition in early-stage patients.

Needless to say, an effective Alzheimer’s drug would not only bring incredible development and hope for patients and their loved ones but also offer a much-needed reprieve for Biogen.

Success would push the biotech to pursue a quick turnabout, with Biogen and Eisai already planning to request an accelerated approval. If the Phase 3 data turns out promising, then the next move would be to clear the way to get Medicare coverage, ensuring that the Aduhelm debacle won’t happen again.

In terms of market opportunity, treatments like lecanemab can rake in over $20 billion in sales in the United States alone.

Still, investors remain cautious. After all, betting on a positive result of an Alzheimer’s trial has proven to be a wrong move in the past—a sentiment that’s apparent in Biogen’s beaten-down price these days.

When Aduhelm gained approval in June 2021, Biogen’s shares climbed almost 40%. Unfortunately, the price steadily fell as the biotech encountered roadblock after roadblock since the drug’s approval and commercialization.

Last year, Biogen shares rose from $270 to hit $400 following Aduhelm’s approval. These days, the biotech has been trading at roughly $205. That’s about 40% below its price in 2018.

By April 2022, Biogen threw in the towel when Medicare flat-out rejected any request to pay for Aduhelm.

More than that, though, Biogen’s results for its lecanemab trial could spell the difference for other Alzheimer’s drugs in late-stage development, including the candidates from Roche (RHHBY) and Eli Lilly (LLY).

What would happen if Biogen fails again?

A failure would make the beginning of a new period for the biotech. Looking at Biogen’s pipeline and portfolio, it’s clear that the next move would either be to sell off pieces of the company or become more aggressive in pursuing mergers.

With the primary business unable to deliver, the expectations shift to the pipeline to pick up some slack. Unfortunately, Biogen’s lineup looks underwhelming. Its disastrous Aduhelm project caused too much damage to the biotech’s finances, restricting its clinical trials.

While Biogen remains the biggest pure neurology biotech thus far, this position is under attack, and its pipeline seems too slow to react in the wake of back-to-back failures.

Reviewing Biogen’s pipeline in Phase 3 trials does not show any candidates that stand out as groundbreaking or transformative. None has the capacity to anchor the company anytime soon.

Apart from that, Biogen is facing fierce competition in its other treatments, including its MS portfolio from the likes of Novartis (NVS), Amgen (AMGN), and Regeneron (REGN).

Meanwhile, more and more pharma names are challenging its neurology drugs like Bristol Myers Squibb (BMY), AbbVie (ABBV), and Merck (MRK). Even Pfizer (PFE) is making a play in this sector with its plan to acquire neurology biotech pure-play Biohaven.

Given Biogen’s track record, the best thing to do right now is to sit and wait until the data are out. If the data turns out positive, then the opportunity would be massive enough for investors to buy in later.

Besides, Eli Lilly and Roche will also release their results in the following months. Those will offer a clearer path and better flesh out the picture of the future of this segment. Most importantly, these will provide investors with safer options to make their bets.