Mad Hedge Biotech and Healthcare Letter

September 22, 2022

Fiat Lux

Featured Trade:

(GOOD THINGS COME TO THOSE WHO WAIT)

(NTLA), (IONS), (TAK), (CRSP), (EDIT), (CRBU), (BEAM), (ALNY), (PFE), (REGN)

Mad Hedge Biotech and Healthcare Letter

September 22, 2022

Fiat Lux

Featured Trade:

(GOOD THINGS COME TO THOSE WHO WAIT)

(NTLA), (IONS), (TAK), (CRSP), (EDIT), (CRBU), (BEAM), (ALNY), (PFE), (REGN)

CRISPR technology has been receiving so much hype over the past years. However, the promise of this gene editing platform has yet to be realized.

Crispr gene-editing therapies can apply permanent modifications to our DNA by zeroing in on specific genes and then incapacitating them or reworking harmful segments of their genetic instructions.

While this could change in the coming years, investors have become impatient with the progress and lack of any major breakthrough in genomics. Some are losing confidence that this sector could experience explosive growth.

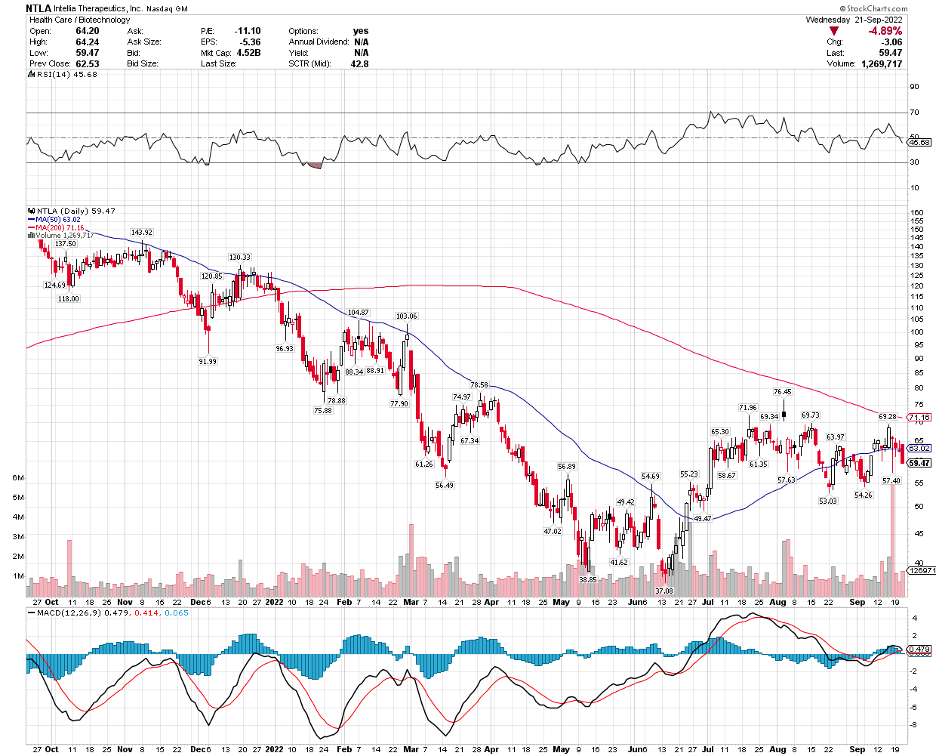

This is what happened with Intellia Therapeutics (NTLA).

Earlier this week, the company showed data that patients who received a one-time gene-editing infusion exhibited sustained improvement in a genetic condition that can result in fatal swelling when left untreated.

To be more specific, Intellia’s update means it could deliver a potentially permanent solution for hereditary angioedema. In this condition, a patient has a miswritten gene in their liver cells that produces a specific protein that triggers a dangerous swelling throughout the body.

Applying the treatment to 6 patients, Intellia’s one-time treatment lowered blood levels of the harmful proteins by more than 90% and decreased the swelling.

This is a more notable effect than the results from existing drugs like Takhzyro from Ionis Pharmaceuticals (IONS) and Takeda Pharmaceutical (TAK).

Despite the encouraging update, Wall Street still spurned the stock, and its price fell.

It looks like investors have lost patience with the slow progress of clinical studies in genetic treatments, pushing some to take advantage of the positive news from Intellia to abandon their positions.

Actually, it’s not only Intellia that suffered from this mistreatment by the market. Investors have also been dumping other stocks utilizing the Nobel-prize-winning technology, Crispr-Cas9, including CRISPR Therapeutics (CRSP), Editas Medicine (EDIT), Caribou Biosciences (CRBU), and Beam Therapeutics (BEAM).

Intellia was hailed the top CRISPR stock in 2021 when the company and its co-collaborator, Regeneron (REGN), shared their promising interim results from a Phase 1 study assessing NTLA-2001, a treatment for a rare genetic disease called transthyretin (ATTR) amyloidosis.

This Crispr infusion candidate managed to knock out rogue genes in the liver cells of 12 patients, halting ATTR’s poisonous effects on their hearts or nerves. Based on clinical data, Intellia’s therapy caused an over 90% drop in the fatal protein triggered by the genetic condition.

If successful, this one-and-done ATTR treatment from Intellia would go head-to-head against other chronic drug therapies like Onpattro by Alnylam Pharmaceuticals (ALNY) or Pfizer’s (PFE) Vyndagel, which generates $2 billion in sales every year.

Many companies use Crispr technology to edit human genomes in an effort to treat and possibly even cure rare genetic diseases. Their treatments typically utilize either an ex vivo or an in vivo approach. With ex vivo therapies, the genes are altered outside the patient’s body.

However, Crispr’s use is not only limited to targeting genetic conditions. There are also gene-editing companies that are working on leveraging the technology to come up with treatments for various kinds of cancer.

In particular, Crispr technology has been a biotech favorite in the development of chimeric antigen receptor T-cell or CAR-T therapies. There are used to genetically engineer immune cells to target specific tumors.

Apart from these, some biotech companies are using Crispr technology to conduct screening. This is different from genetic testing, though.

When using Crispr for screening, the genes are modified in a manner that makes them nonfunctional or inoperative. Crispr screening allows biotechs to explore which genes take on particular functions, which can be critical in the development of drugs and treatments.

Intellia’s recent updates are clear indications that Crispr technology works. Since this will be applied to humans, we should expect the timeline and adaptation to take longer.

I have become more and more thrilled with developments in the gene editing space. Moreover, I believe it’s no longer about “if” but when it will happen.

Overall, the gene editing sector is not for fast-paced investors. This is for those willing to wait for a very long time, particularly for stocks like Intellia Therapeutics.

Mad Hedge Biotech and Healthcare Letter

September 20, 2022

Fiat Lux

Featured Trade:

(A MONSTER BIOTECH ON ITS WAY TO ANOTHER BLOCKBUSTER)

(BMY), (AMGN), (VTYX)

This year's bear market has pushed a lot of businesses to their breaking points. The S&P 500, the benchmark of stock performance in the US, has fallen by 14.6% in 2022.

What’s making things look gloomier is that the tech-focused Nasdaq Composite Index, aka the bellwether growth stock index, has plummeted by 22% thus far. Even the Dow Jones Industrial Average, another leading indicator, has dipped by 11.5%. All these firmly place the entire market in the bear market territory.

In response to the headwinds, investors have spotlighted businesses with steady free cash flow, solid leadership teams, and virtually recession-proof sectors.

This is where Bristol Myers Squibb (BMY) shines as an excellent example of Wall Street’s reinvigorated desire to pour money on long-forgotten movers in the market.

As one of the leading biotechnology companies worldwide, BMY has once again piqued the interest of investors primarily for its ability to defy the bear market. In fact, the company’s stock is up 12% year to date, clearly outperforming the S&P 500 by roughly 29 percentage points.

BMY’s ascent has taken years, with the business benefitting massively from its $74 billion acquisition of another biotech stalwart, Celgene.

This deal granted BMY access to an extensive oncology and autoimmune diseases portfolio, with back-to-back blockbusters like Revlimid and Reblozyl sales practically paying for Celgene’s acquisition price.

Now, BMY has made another move that brought seismic rearrangement within the biopharma sector, particularly in the highly lucrative psoriasis treatments space.

Earlier this month, BMY disclosed that it received FDA approval for its oral plaque psoriasis treatment deucravacitinib. The company plans to market this new drug under the name Sotyktu.

More impressively, Sotyktu was not given any “black-boxed warning” on its label, which typically indicates that a treatment carries significant safety risks.

Unlike most therapies for psoriasis, which use Janus kinase inhibitors, BMY is the first to use and gain approval for a TYK2 inhibitor. Generally, treatments utilizing Janus kinase inhibitors come with “black-boxed warnings.”

The absence of which, in BMY’s candidate, indicates a cleaner label.

This is terrible news for Amgen’s (AMGN) Otezla, which is currently the leader in the psoriasis space. Since this drug uses Janus kinase inhibitors, it has become a “less safe” option for patients. More than that, Sotyktu managed to outperform Otezla in a head-to-head trial.

Aside from that, a “black-boxed warning” would have offered Amgen some defense in protecting Otezla’s market share.

Meanwhile, Sotyktu’s approval brings good news to smaller biotechnology companies, such as Ventyx Biosciences (VTYX), working on similar treatments that use TYK2 inhibitors.

Regarding costs, BMY’s list price for its psoriasis therapy is notably higher than Amgen’s. According to sources, Sotyktu will be given a price tag of roughly $75,000. In comparison, Otezla is priced at approximately $52,000 annually.

Needless to say, Sotyktu is projected to become another blockbuster in BMY’s arsenal. Simply basing the possibilities on Otezla’s recent sales reports would give us a good picture of this new drug’s future.

In 2021, Otezla raked in $2.2 billion in sales for Amgen. Despite the competition, Otezla is still projected to grow and reach $3.2 billion in annual sales by 2026.

Considering that BMY’s Sotyktu will be playing catch up in terms of marketing and distribution, this psoriasis drug is anticipated to reach $2 billion in yearly sales in 2026.

However, this was estimated before the FDA’s surprise approval. The consensus is that the absence of a “black-boxed warning” would significantly boost the projections.

Overall, BMY has always been quite the oddball among its peers. While the SPDR S&P Biotech ETF rose by a staggering 42% in 2021, the company was barely in positive territory.

Due to the impending patent cliffs at that time, BMY was considered a laggard in the biopharma world. Added to those concerns was the company’s move to buy Celgene for a jaw-dropping $74 billion, substantially increasing its debt-to-equity-ratio. Taken together, these threats made BMY an unfavorable investment from 2020 to late 2021.

By 2022, however, BMY will have transformed into a favorite on Wall Street. Investors have regarded it as a safe harbor amid the ongoing bear market.

Moreover, BMY shares have marched even higher thus far by an impressive 12.5%. Meanwhile, the SPDR S&P Biotech ETF has recorded a 21.4% loss this year.

While the rest of the market has been struggling to keep things afloat, BMY’s stock isn’t that far from hitting its 52-week high to date. Hence, it would be an excellent move to buy the dip.

Mad Hedge Biotech and Healthcare Letter

September 15, 2022

Fiat Lux

Featured Trade:

(A LONG-TERM HIGH-RISK STOCK)

(ILMN), (GRAL), (EXAS), (NVTA), (GH), (NTRA)

As Warren Buffett says, it’s wise to be greedy when others are fearful. This is excellent advice these days since we’ve been dealing with fearful times. Even the best growth stocks have been struggling from economic headwinds and the rising panic over interest rate hikes.

That means there are several opportunities for enterprising investors to take advantage of the uncertainties and set themselves up for long-term success by buying quality stocks at discounted prices.

One stock that has been battling issues lately is Illumina (ILMN).

Over the past 10 years, Illumina has delivered 380% returns—resoundingly beating the market’s gain of 241.6%.

To achieve that success, the company sold, installed, and serviced over 20,000 gene sequencer devices, which hospitals and other biomedical centers use to analyze genetic data.

Unfortunately, Illumina’s luck has turned in the last 12 months. The company has been underperforming and has investors worried about the future.

Illumina’s dominance in the sequencer market is one of the significant reasons to invest in its stock.

After all, the significance of genetic information is projected to expand over time. That makes Illumina the clear candidate for a long-term hold despite its current underperformance.

However, it’s understandable for investors to be anxious, especially with the recent move of Europe’s antitrust regulators to bar the $8 billion acquisition of Grail (GRAL).

Here’s a brief background about the deal.

Grail has created a lab test that can identify over 50 types of cancers at their early stages using only a simple blood draw. This is called the Galleri blood test.

Since screenings do not exist for most kinds of cancers, many are not diagnosed until they’re already spread and are, therefore, more challenging to treat.

Although Grail’s test does not promise to detect all cancers, it can catch the 12 most fatal types with roughly 76% accuracy, while its false positives are lower than 1%.

Needless to say, these tests could save thousands of lives annually if adopted across the globe.

This is where Illumina comes in. Since the company develops platforms that sequence genetic tests for various fetal abnormalities and even COVID variants, it has the technology to expand Grail’s operation.

Moreover, Illumina has extensive experience negotiating insurer reimbursements, which means it could accelerate the commercial adoption of Grail’s technology. At the moment, most insurers refuse to cover the costs of Grail’s test.

This resulted in only $12 million in revenue for the company, with over $187 million in operating loss. Grail’s underwhelming performance is one of the reasons investors are baffled over the move to block the acquisition.

Another is that the acquisition does not fall under any of the categories for antitrust reviews under the EU bylaws because Grail does not operate or do any business in Europe.

However, the commissioner decided to invoke a provision under EU’s merger rules that allow member states to reach out to the commission when their governments do not have jurisdiction over the matter. Six countries did so, which led to the review.

The commission is tag-teaming with the US Federal Trade Commission, which also moved to stop the deal in 2021. Both regulating bodies claim that the agreement could impede competition in the embryonic multiple cancer-early detection industry.

According to the EU commission, this acquisition would cut off all of Grail’s rivals in the segment.

This is a tad confusing, though, because Grail has no rivals in the field.

The entire debacle has the scientific community wondering over the real reason, especially since Illumina developed the technology Grail used. Then, it was spun off for financing purposes, but Illumina still retained 20% ownership. Now, the company is merely taking it all back again by acquiring it.

It remains to be seen what will happen in the following months as Illumina plans to appeal the decision.

But why is Illumina still pushing through with this deal?

The reality is that the genetic testing industry is a bloodbath. It can take years for a single genetic test to complete clinical trials, receive regulatory approval, and achieve insurance coverage. This struggle is apparent in so many clinical laboratories such as Exact Sciences (EXAS), Invitae (NVTA), Guardant Health (GH), and Natera (NTRA). Even Grail lost so much while developing its cancer blood test.

Meanwhile, Illumina chooses to market clinical tests its clients have already pioneered. That way, it can still gain profits as a supplier of sequencing tools.

Hence, having Grail back in its portfolio would be a cherry on top of its current strategy.

Looking at the situation right now, it’s a mess. Nevertheless, Illumina’s main line of business is a significant segment to be a part of in the coming years.

I don’t think the company would spend this much time and effort on Grail unless the future payoff would be substantial. Think about it: detecting cancers early? How incredible is this technology? How many lives would be saved because of it?

The long-term investing thesis for betting on Illumina is that it’ll most likely continue to deploy its gene sequencing devices globally, generating more recurring revenue flows in the process.

Simultaneously, the company can expand its domain knowledge and gather a copious amount of data for R&D that would equip it against competitors.

Basically, it has found a way to lock in customers for years while being several steps ahead of its rivals.

As confusing and grim the situation may be, for now, I believe Illumina stock is an excellent investment with or without Grail (but I hope it finds a way to be with it).

Mad Hedge Biotech and Healthcare Letter

September 13, 2022

Fiat Lux

Featured Trade:

(A CROWN JEWEL SCORES A GOAL)

(REGN), (BAYRY), (RHHBY), (SNY), (ALNY), (NTLA)

A stock with high margins offers a better buffer to face adversity and increased expenses.

Suppose a business’s revenue cost is substantial and leaves minimal room for the top line to maneuver and cover overhead and other operating fees. In that case, it can be challenging to stay in the black.

A recent example is Amazon (AMZN), which reports that its cost of sales typically comprises 80% or more of its revenue. When it struggled with the rising expenses in the past quarter, this e-commerce giant posted its first-ever loss in years.

Only a handful of companies manage to stick with this principle. In the biotechnology and healthcare sector, one business that doesn’t have this issue and enjoys gross profit margins of at least 80% or better is Regeneron Pharmaceuticals (REGN).

Regeneron was recently spotlighted following a significant 19.2% jump in its price, translating to a more than $12 billion rise in market capitalization.

The catalyst for this double-digit climb is none other than Regeneron’s crown jewel: Eylea.

The anti-blindness treatment, jointly developed with Bayer (BAYRY), delivered excellent results in two late-stage trials.

This is a huge deal because it supports the application of Eylea at higher doses and longer-lasting intervals.

Previously, Eylea was only permitted to be administered in 2 mg every 8 weeks. The recent trial results proved that the medication can be given at a higher concentration of 8 mg in a more extended period of 16 weeks and can still be effective at battling the disease. Plus, it shows a similar safety profile as the currently approved dosage.

This is a timely development for Eylea, which is set to lose its patent exclusivity soon, bringing anxiety to shareholders.

For context, Eylea accounts for $3.13 billion of Regeneron’s sales in the first 6 months of 2022. In the year's second quarter alone, it generated $2.49 billion in sales, recording a 9% year-over-year increase in its global profits.

In 2021, this eye medication reported $9.4 billion in sales worldwide.

These recent developments are eyed as potential solutions to Eylea’s impending franchise exclusivity loss as it attempts to eliminate a key overhang.

This move could slam the door shut on any talks or fears of potential copycats for at least a few years. It could also make it more competitive against rising competitors in the same space like Roche’s (RHHBY) Vabysmo.

The new data is expected to be used to defend the franchise from biosimilars, generic, and branded competitors. This is because patients are now offered an option for a treatment that needs fewer injections.

Most importantly, this could establish a firmer competitive moat for Regeneron and Bayer. After all, Eylea is projected to rake in more than $6 billion in sales in the US annually in 2023 and 2024.

Looking at their timeline and progress, the new Eylea dosage should be submitted for approval by the end of 2022 and launched by early 2023.

Other than Eylea, Regeneron has also been active in the oncology space.

Leveraging its roughly $6.2 billion sales from its COVID-19 treatment, Regeneron acquired several assets to expand its oncology segment.

Recently reported deals are its $900 million payment to Sanofi (SNY) to acquire non-small lung cancer drug Libtayo and the purchase of Checkmate Pharmaceuticals, which granted it access to promising melanoma candidates.

While these deals may not be as massive as other acquisitions in the industry, adding Libtayo and Checkmate Pharmaceuticals represent critical steps toward the right direction.

On top of these, Regeneron has existing partnerships and collaborations that would last for years. One is with Alnylam (ALNY), which involves treating liver cancer, ocular conditions, and diseases targeting the central nervous system.

Meanwhile, Regeneron expanded its deal with Intellia Therapeutics (NTLA) to give more rights to their in vivo therapeutic candidate developed via CRISPR/Cas9 gene-editing technology and additional targets, particularly for hemophilia A and B.

Overall, Regeneron has been proving to be a noteworthy investment in biotechnology and healthcare. At this point, though, the recent clinical trial results have been added to its share price.

While it isn’t exactly cheap, it’s not an outlandish valuation either. In short, I suggest that you wait and buy the dip.

Mad Hedge Biotech and Healthcare Letter

September 8, 2022

Fiat Lux

Featured Trade:

(WON’T GO DOWN WITHOUT A FIGHT)

(CVS), (SGFY), (AMZN), (HUM), (UNH)

Bigger is better. At least, that’s what CVS Health (CVS) seems to believe.

Recently, the big news in healthcare is CVS’ move to acquire Signify Health (SGFY) for $8 billion, pushing it even nearer to its goal of becoming an integrated healthcare provider.

The deal, anticipated to close by the first quarter of 2023, is an all-cash deal with CVS paying $30.50 per share.

While this deal isn’t exactly something new, Signify has been known to be a great innovator in the fast-moving space.

The critical factor in how Signify is different from other companies lies in its strategy, which leans more on a technology- and data-focused model that caters to the gig economy. Under its scheme, clinicians are likened to Uber drivers in terms of independence.

Meanwhile, CVS’ move to swoop in and buy Signify actually threw a wrench in the plans of another company hoping to dominate in the healthcare space: Amazon (AMZN).

Just a few weeks before this announcement, Amazon’s entry into the healthcare industry felt unstoppable. The e-commerce giant started its journey with the $3.9 billion purchase of One Medical (ONEM), a doctor’s office chain, with the goal of continuing its expansion through a deal with Signify.

The encroachment of the retail giant seemed like a massive issue for existing players in the healthcare industry, particularly CVS, which was said to have lost out in the bidding war for ONEM.

Needless to say, this makes CVS’ success in buying Signify an even sweeter victory.

More importantly, this decisive move from CVS makes it apparent that it won’t go down without a fight. That is, Amazon’s march into the healthcare industry will not be completely unopposed.

Basically, Signify sends clinicians to patients’ homes to help them assess their conditions. However, the company does not offer home health services at all.

CVS’ decision to pursue this deal makes it clear that the company is veering toward primary care delivery. Signify’s services can integrate almost seamlessly with the CVS Health ecosystem, with clinicians being afforded the opportunity to simply direct patients to other CVS products and services.

However, not all plans are perfect.

One red flag in this deal involves the major clients of Signify: Humana (HUM) and UnitedHealth (UNH).

Given that CVS is a competitor, they may be put off by the new arrangement and decide to pull out of their existing contracts. This is an understandable concern since one of the main attractions in availing of Signify’s services is its status as an independent entity. This ensures that it operates without any bias and allows equal participation among all payers.

While Signify execs claim that all stakeholders are “very supportive” of this deal, the effects of the plan remain to be seen.

Either way, home-based healthcare is emerging as a new and lucrative trend in the industry. Hence, more and more companies are expected to make similar decisions.

Earlier this month, Walgreens Boots Alliance (WBA) executed a similar move when it acquired a majority share of CareCentrix. Even UNH shelled out a premium when it bought LHC Group, a home-health provider, for $5.4 billion this spring.

Whether it’s caused by an aging population battling mobility issues or healthier patients who realized the price of convenience during the pandemic, it’s undeniable that the demand for home-based healthcare is growing.

Obviously, companies like CVS are capitalizing on that trend.

So far, CVS’ strategy to develop a one-stop-shop for healthcare looks to be on track. The fact that it’s managing to build out a full-scale integrated model while practically doubling its stock price in the last three years makes it an excellent stock to own for the long haul.

If the company continues this trajectory and expansion into primary care, then CVS could quickly become one of the biggest healthcare stocks globally.