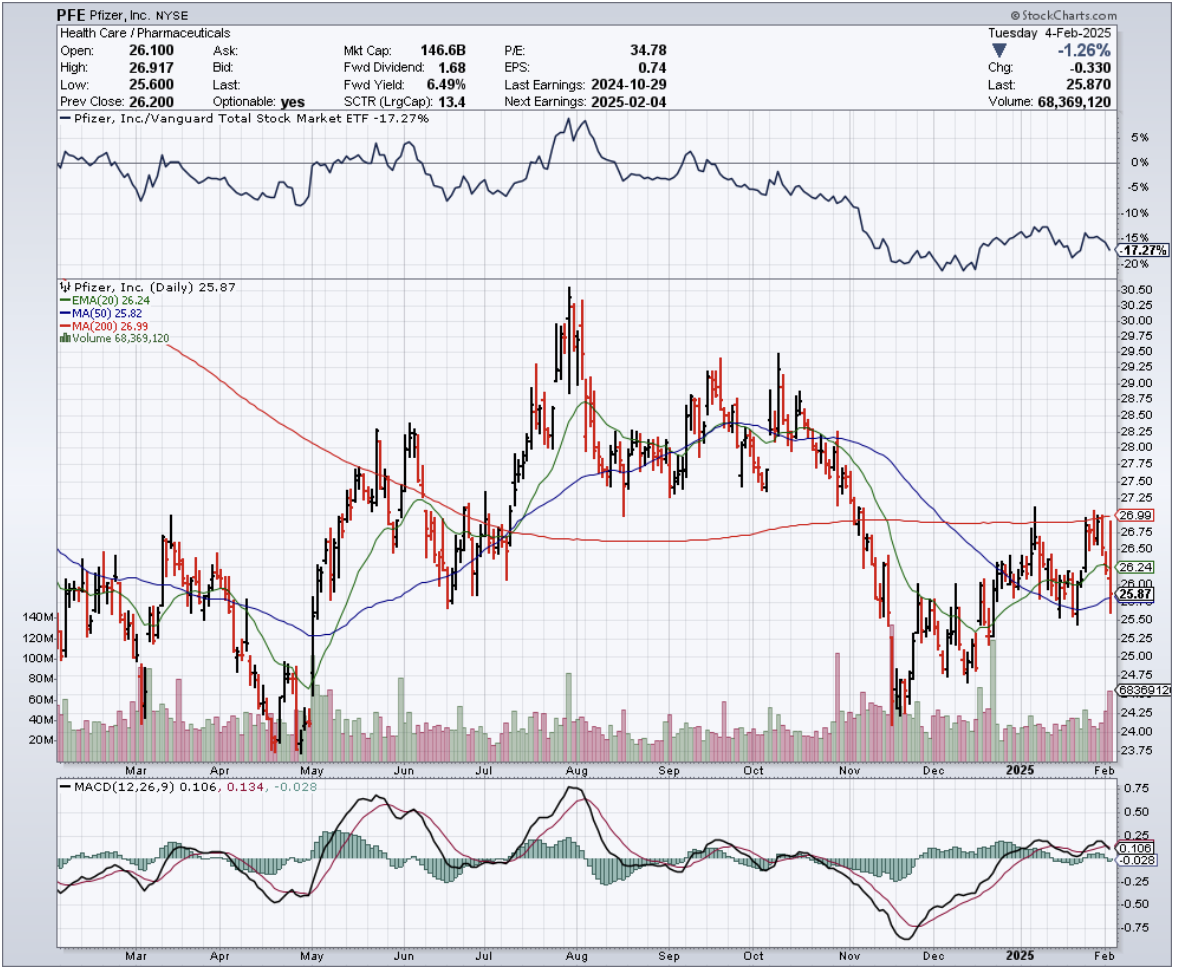

Last Tuesday, while filing away some tax documents, I found myself staring at an old prescription bottle from 2020. The Pfizer (PFE) logo caught my eye, and ironically, that same morning they dropped their Q4 earnings report.

The timing felt symbolic – much like that old bottle, Pfizer's COVID glory days are now just a memory on their financial statements.

The numbers looked good on the surface. EPS of $0.63 beat expectations by $0.17, and revenue came in at a healthy $17.8B, crushing estimates by $540M.

But in the pharmaceutical world, today's blockbuster is tomorrow's generic, and Wall Street knows it. After all, the market's reaction was about as enthusiastic as a patient reading medication side effects.

Let me paint you a picture of what we're dealing with here. Imagine going from making $100.3B in 2022 (those glory days of COVID) to $58.5B in 2023. That's not a haircut – that's a full-blown scalping.

Sure, they bounced back to $63.6B in 2024, but their 2025 guidance of $61.0B to $64.0B suggests they're treading water at best.

Now, here's where it gets interesting, and not in a good way. Remember how I always tell you to look under the hood? Well, Pfizer's engine is about to lose some major parts.

By 2030, they're saying goodbye to patents on Eliquis (a $6.7B revenue generator) and Ibrance (worth $4.8B). That's like losing your two best-performing stocks in your portfolio – it hurts.

Speaking of pain, I had lunch last week with a pharmaceutical industry veteran who couldn't stop talking about the "LOE wave" – that's "loss of exclusivity" in pharma-speak. CEO Albert Bourla puts it at about $17-18 billion in lost revenue over the next 3-4 years.

To put that in perspective, that's like losing the annual GDP of Mongolia. The company's solution? They're promising to deliver $20 billion in new revenues by 2030 through their pipeline of new drugs.

One bright spot worth watching is their oncology division, which grew an impressive 27.4% year-over-year in 2024.

Their promising candidate Atirmociclib, a CDK4i inhibitor for metastatic breast cancer, enters Phase 3 studies in the first half of 2025.

With a 44% historical success rate for these types of studies, it's targeting a massive market – the global breast cancer therapeutics market hit $34.63 billion in 2024 and is expected to reach $89.01 billion by 2034, growing at a healthy 9.90% annually.

That's the kind of growth potential that gets my attention.

The stock currently sports a 6.7% dividend yield, which might look tempting – like that last piece of chocolate cake in the refrigerator at midnight.

But here's the rub: pharmaceutical companies are like Silicon Valley startups with lab coats. They constantly need to innovate just to stay alive. It's not enough to have one hit wonder – you need a whole playlist of blockbusters.

Trading at 8.91x forward earnings with a PEG ratio of 0.20 and 2.5x price/sales, Pfizer does look cheap. But as I always say, sometimes things are cheap for a reason.

Want a shocking comparison? While attending the J.P. Morgan Healthcare Conference, I noticed that analysts are projecting Pfizer's 2029 revenues to be over $5 billion lower than 2024. That's not exactly the inspiring growth story I was hoping to hear.

For those of you hunting for yield (and I know many of you are), let me give you a reality check. That juicy 6.7% dividend looks appetizing until you realize it comes from a company that needs to spend billions just to replace what it's about to lose.

While I love a good yield as much as the next investor, watching a pharmaceutical company's patents march toward expiration is about as comforting as sitting in a dentist's waiting room.

Sometimes the best high-yield investment is the one you don't make – at least until the business fundamentals match the dividend's promise.

Want my advice? Keep an eye on their oncology developments, but keep your powder dry. There's a difference between buying a great company and buying a great stock at the right time.

Right now, Pfizer needs to prove it can fill an $18 billion revenue gap before I'm ready to write them a prescription for my portfolio.