Mad Hedge Biotech & Healthcare Letter

November 10, 2020

Fiat Lux

FEATURED TRADE:

(PFIZER ADDS EXCLAMATION POINT TO ITS DECLARATION OF INDEPENDENCE)

(PFE). (MRNA), (AZN), (JNJ), (MCK), (GSK), (MYL). (MRK), (BMY)

Mad Hedge Biotech & Healthcare Letter

November 10, 2020

Fiat Lux

FEATURED TRADE:

(PFIZER ADDS EXCLAMATION POINT TO ITS DECLARATION OF INDEPENDENCE)

(PFE). (MRNA), (AZN), (JNJ), (MCK), (GSK), (MYL). (MRK), (BMY)

When Operation Warp Speed was launched, the US government handpicked the most promising COVID-19 vaccine programs and offered them funding—an offer that was welcomed by all those selected except for one: Pfizer (PFE).

While COVID-19 vaccine frontrunners like Moderna (MRNA), AstraZeneca (AZN), and even Johnson & Johnson (JNJ) accepted financial assistance from the US government, Pfizer insisted on funding its own coronavirus program.

Now, Pfizer has taken another step to make it clear that it does not need any help.

In what could only be described as adding an exclamation point to its “declaration of independence” from the US government, Pfizer announced that it won’t use the country’s chosen distribution partner in delivering its COVID-19 vaccine.

For years, the US government has been using McKesson (MCK) to deliver drugs and other treatments.

In fact, this was the same company used by the Obama administration in 2009, when it distributed the H1N1 vaccine and medications.

This won’t be the case for Pfizer’s COVID-19 vaccine though.

According to the company, it has designed its own delivery system to ensure the proper and safe distribution of its product.

In October, Pfizer disclosed its distribution plans that centered on select sites in Michigan, Belgium, Wisconsin, and Germany.

Other than its goal to operate as independently from the US government as possible, one of the concerns of Pfizer is the sensitive nature of its COVID-19 vaccine.

The vaccine has to be kept at an ultra-cold temperature of minus 94 degrees Fahrenheit, which means that the shipments would require close monitoring.

What we know so far is that Pfizer has designed shipping containers that can maintain the temperature of the vaccine for 10 days.

In terms of monitoring, the company has developed a real-time GPS tracking system that will report any deviations in the set conditions.

All these are implemented to ensure that the COVID-19 vaccine does not lose potency before it reaches patients.

Looking at the other vaccine candidates, Moderna might also resort to this kind of distribution arrangement since its vaccine needs to be stored at negative 4 degrees Fahrenheit.

Outside its COVID-19 efforts, Pfizer has been aggressive in pruning its business divisions.

Since late 2019, Pfizer has been implementing strategies to eliminate its underperforming segments.

In August last year, the company forged a partnership with GlaxoSmithKline (GSK) to combine their consumer healthcare sectors.

This led to the formation of the GSK Consumer Healthcare, where Pfizer holds a 32% stake.

This year, Pfizer has been working on offloading its off-patent drug unit, Upjohn, and merging it with Mylan (MYL).

This deal should be finalized by the fourth quarter of 2020, with the merger offering Pfizer’s shareholders with roughly 57% of the new company, Viatris.

When this is completed, Pfizer would become a smaller and more focused biopharmaceutical company.

This means that the company can leverage its $202.27 billion market capitalization to move the needle more substantially in terms of its long-term prospects.

One of the key areas that Pfizer has been working towards becoming a powerhouse is oncology—a sector that has served as a major growth driver for the company for years.

Pfizer has a deep oncology portfolio comprising over 20 approved drugs marketed to different areas including breast cancer, lung cancer, and blood cancer.

However, none of its cancer drugs have managed to breach the $10 billion annual sales mark in this sector.

This is because Pfizer has no absolute mega-blockbuster in the oncology space like its competitors Merck (MRK) with Keytruda and Bristol-Myers Squibb (BMY) with Opdivo.

With the growing number of pipeline candidates in its cancer portfolio, Pfizer is expected to come up with a blockbuster by the fourth quarter this year or before the first half of 2021 ends.

Looking at Pfizer’s pipeline, there are 14 approvals anticipated from today through 2025 in the oncology segment alone.

One contender is its prostate cancer drug Xtandi. Another is a non-small cell lung cancer medication called Lorbrena.

In terms of its current product lineup, Pfizer’s biopharmaceutical operations continue to impress investors.

Despite not having a mega-blockbuster, it still has several top-selling drugs like Eliquis and Ibrance. Both showed 9% increase each in sales for the third quarter of 2020.

Taking all these into consideration, Pfizer is estimated to deliver solid growth in the next few years primarily thanks to its fast-developing oncology segment. This market is forecasted to experience an increase of $240 billion every year by 2023.

Overall, a successful COVID-19 program could provide a one-time earnings boost for Pfizer and a substantial earnings accretion in fiscal 2021.

However, this giant biopharmaceutical company’s extensive lineup of commercialized products and promising oncology pipeline mean that its revenue and share performance do not heavily depend on its coronavirus vaccine.

If Pfizer’s COVID-19 vaccine candidate fails, it won’t be a disaster for its shareholders, especially since the company’s shares do not seem to consider this program in its pricing.

In fact, Pfizer shares are looking inexpensive even without a successful COVID-19 vaccine candidate.

If it does turn out to be a success though, then Pfizer investors could enjoy some COVID-19 vaccine call option for free.

Mad Hedge Biotech & Healthcare Letter

November 5, 2020

Fiat Lux

FEATURED TRADE:

(IT’S GO TIME FOR BIOGEN’S ALZHEIMER’S DRUG)

(BIIB), (LLY), (AXSM), (MYL)

Investing in beaten-up stocks in this period of uncertainty demands nerves of steel.

In fact, some biotechnology and healthcare stocks have been left for dead in recent months. Meanwhile, there are others that continue to deliver amidst the ongoing pandemic.

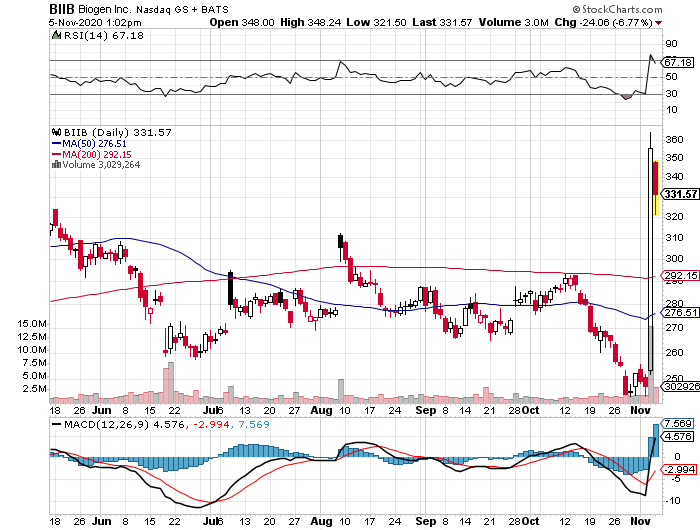

One of them is Biogen (BIIB).

Biogen has been consistently tagged as a high-risk-high-reward stock even before the COVID-19 pandemic started.

However, people seem to miss the fact that the company has relatively low debt and a surprisingly positive free cash flow in the past years.

Since 2019, the banner headline for Biogen has been its experimental Alzheimer’s disease treatment Aducanumab.

Recently, Biogen released promising progress following its decision to submit the Alzheimer’s candidate for a priority review to the FDA. It has also been accepted for review by European health regulators.

Although this move appears risky, the goal is to accelerate FDA’s timeline for Aducanumab.

That is, Biogen’s decision to submit the drug for approval earlier than expected also pushes the decision to an earlier date, which is March 7, 2021.

If approved, then Aducanumab will be the first-ever approved drug for Alzheimer’s disease.

The road to this point was not easy though. Biogen went through a series of failed trials and even a brief period of giving up on the project before the company gave the effort another chance.

Looking at the market opportunity for this sector, Biogen’s about-face no longer comes as a surprise.

For decades now, companies have been looking into ways to at least slow the progress of the condition, treat the symptoms, and offer faster ways to diagnose it.

There is currently no cure for this disease, which is ranked as the sixth leading cause of death in the country and accounts for approximately 2 million deaths globally.

Given that this disease takes years to progress, it means tens of millions of patients live with the condition on a daily basis -- and this sector comprise the target niche for Aducanumab.

In the United States alone, over 5 million people are diagnosed with Alzheimer’s disease annually and this number is projected to increase to nearly triple by 2050.

With all the treatments geared towards Alzheimer’s disease, sales for these products were estimated at $3.5 billion in 2018. This cost is expected to hit a 7.2% compound growth rate yearly until 2030.

If successful, Aducanumab can reach peak sales somewhere between $10 billion and $20 billion.

For context, the annual sales of Biogen today is only under $15 billion.

This underscores the significance of Aducanumab for the company as the drug can more than double its total earnings and even its market capitalization. It can also offer a 3x to 4x jump in Biogen’s share price.

Apart from Biogen, other big names working on an Alzheimer’s treatment are Eli Lilly (LLY) and Axsome Therapeutics (AXSM).

Outside Biogen’s work on Aducanumab, the company also has an impressive asset portfolio.

Its second quarter earnings results for 2020 showed that revenues from its multiple sclerosis drug segment contributed significantly to the company’s profits, with Ocrevus raking in $2.3 billion for the period.

The newly acquired rare spinal muscular atrophy disease drug Spinraza also performed well, reporting approximately $2 billion in annual sales.

Even its embattled multiple sclerosis treatment Tecfidera, which has been facing patent exclusivity issues with generic companies like Mylan (MYL), reported an increase from its notable $1 billion in revenue for the first quarter of the year to $1.2 billion in the second quarter.

Finally, Biogen has been working on expanding its biosimilar segment to increase its competitive advantage particularly for its drugs that are nearing the end of their patent exclusivity.

Amid the pandemic, Biogen’s revenue was up by 1% to hit $3.5 billion in the first quarter of 2020 and increased by 2% to reach $3.7 billion in the second quarter.

The company’s financial results also rose by approximately $100 million in the first three months of this challenging year.

However, a widely known caveat not only for Biogen but also for a number of biotechnology companies is the volatility of the stocks.

There is no one-size-fits-all formula for investing in beaten-up stocks. It comes with zero guarantees that their past performances would make a repeat either.

The strategy for these things though is quite basic. Make sure to look at businesses that offer sufficient bandwidth to bounce back once things normalize and the effects of the pandemic start to ease.

Looking at its overall performance, Biogen has achieved an impressively strong financial position despite the setbacks along the way. The company even offers room for growth regardless of the performance of its much-awaited Aducanumab.

Mad Hedge Biotech & Healthcare Letter

November 3, 2020

Fiat Lux

FEATURED TRADE:

(TESTED AND PROVEN COVID-19 STOCK FOR THESE UNCERTAIN TIMES)

(ABT), (PFE), (AZN), (MRNA)

As we hold our breath for the results of the presidential election, it’s no surprise that investors are wondering how their portfolios will be impacted.

That’s why now is the right time to pick a stock or two that can thrive regardless of who emerges as the victor.

To do this, it’s wise to look at a company that has already experienced a boost under Trump’s presidency and could continue to enjoy the rewards even with a Joe Biden administration.

The obvious common denominator is Trump and Biden’s goal to be aggressive in COVID-19 testing for as long as the virus is around.

Pfizer (PFE), AstraZeneca (AZN), and Moderna (MRNA) are undoubtedly three of the most widely reported coronavirus stocks in the past months.

These companies were the first to launch their COVID-19 vaccine candidates in human trials and are the leaders in the race towards the finish line.

However, long-term investors may find more value betting on one of my preferred COVID-19 stocks: the $188 billion healthcare behemoth Abbott Laboratories (ABT).

Let me tell you why.

In either Trump’s or Biden’s presidency, Abbott stands to benefit.

Regardless of the winner of the 2020 election, Abbott remains a winner for as long as COVID-19 continues to threaten the world.

While the majority of COVID-19 vaccine companies have yet to generate income from their coronavirus programs due to pending FDA approvals, Abbott has been leveraging its pipeline to boost its growth even with the pandemic.

Since the early days of this health crisis, Abbott has been working to stay ahead of the pack.

To date, the company has at least seven COVID-19 tests with emergency use authorization from the FDA and are available in the market.

These tests, which boosted Abbott’s diagnostics sales by 39% in the third quarter, range from detecting active cases to identifying whether a person has been infected with the virus in the past.

The latest swab test to join Abbott’s growing lineup of COVID-19 products is called the antigen test and is designed to deliver results in as fast as 15 minutes and costs only $5.

To add convenience, this test is connected to a mobile to allow users to access their results right away.

Prior to the antigen test, Abbott launched a rapid detection test called BinaxNOW. This test can also return results on-site within 15 minutes. It has a free digital app, which sends users with negative results a “digital health pass” right on their phones.

When BinaxNOW was launched in August, the Trump administration spent $760 million for 150 million tests.

This company has supplied over 100 million COVID-19 tests and generated roughly $881 million in sales in the third quarter, up from the $615 million it reported in the second quarter.

Abbott is one of the safer stocks to own in the healthcare sector, with sales estimates for this company expected to grow by 14% in 2021 and 2022.

So far, Abbott shares have climbed 22% this year. Even amidst the pandemic, Abbott raised its full-year guidance for its earnings per share from $3.25 to $3.55.

While the company has been focused on its COVID-19 programs, this strategy is not a one-time deal.

On the contrary, the popularity of its COVID-19 testing kits serves as the much-needed door-opener for Abbott to expand its medical venues—an effort that generally takes years to develop.

For instance, its diabetes care segment alone managed to achieve a 26.9% year-over-year jump in sales to reach $843 million in the third quarter.

On top of that, Abbott has an incredibly diverse pipeline with over 100 new products across its different business units.

Abbott is a widely known dividend aristocrat, paying quarterly dividends consistently since 1924. It has a proven track record of solid performance and a carefully curated suite of businesses that promises future rewards.

At the rate the company is growing and the future projects it has in its pipeline, this dividend aristocrat would no doubt continue with this proud tradition of rewarding its investors generously.

Mad Hedge Biotech & Healthcare Letter

October 29, 2020

Fiat Lux

FEATURED TRADE:

ROCHE ENTERS COVID-19 FIGHT IN STYLE

(RHHBY), (REGN), (GILD), (MRK), (ALNY), (IONS)

Roche (RHHBY) is making quite an entrance in the COVID-19 antiviral treatment race, forking out $350 million in cash to gain rest-of-the-world rights to a promising new drug created by Massachusetts-based biotech company Atea Pharmaceuticals.

This is an exciting development because the partnership between the two companies holds incredible promise in the search for a COVID-19 cure.

In May, Atea Pharmaceuticals essentially dropped all its projects and rebranded itself as a COVID-19 fighter, attracting a stunning $215 million in its venture round.

Among the marquee names that invested in this 7-year-old biotechnology company are Bain Capital and RA Capital.

Going back to its work with Roche, the $350 million cash is expected to fund the ongoing clinical trials of Atea’s very own COVID-19 antiviral treatment called AT-527.

So far, the candidate is in its Phase 2 trial and slated to start global trials or Phase 3 by early 2021.

Apart from being a potential COVID-19 treatment, AT-527 is also under development as a Hepatitis C medication.

In terms of where AT-527 stands in the COVID-19 treatment race, this drug belongs to the same class as Gilead Sciences’ (GILD) Remdesivir and Merck’s experimental candidate with Ridgeback Biotherapeutics called MK-4482.

Like Remdesivir and MK-4482, Roche’s AT-527 is designed to inhibit the replication of SARS-CoV-2, the virus that causes COVID-19.

Unlike Remdesivir though, which is only available through intravenous infusion, AT-527 is an oral drug, making it a more convenient option.

This isn’t the first time that Roche’s COVID-19 efforts came under the spotlight.

Earlier this month, its COVID-19 work with Regeneron (REGN), called REGN-COV2, has been dubbed as a leading candidate in the race because of the high-profile patient who used it: President Donald Trump.

This partnership with Regeneron is expected to ramp up the manufacturing process by at least 3 and a half times compared to their individual capacities.

Outside its COVID-19 efforts, Roche has proven to be a good long-term investment.

Admittedly, the company’s third-quarter report missed the mark by 4% due to aggressive biosimilar competition. However, Roche’s pipeline of newer products has been growing nicely.

Because of biosimilar competition, sales of cancer and immuno-oncology treatments like Avastin fell by 30%, Rituxan slipped by 33%, and Herceptin dropped by 38%.

However, the performance of Roche’s new drug lineup showed promising results, with sales of these products showing off a 32% growth in the third quarter of 2020.

For example, sales of multiple sclerosis drug Ocrevus rose by 37%, while revenue from cancer treatments like Perjeta climbed 17%, Kadycla rose by 33%, and Tecentriq jumped by 49%. Meanwhile, sales of hemophilia medication Hemlibra increased by 57% .

All in all, the hits and misses cancelled out each other this quarter.

Despite the disappointment in these results, Roche stood by its full fiscal year guidance.

This is a strong indicator that the company sees a brighter fourth quarter. Overall, Roche remains in good shape.

Tecentriq has been expanding to cater to other indications such as liver cancer and even some immuno-oncology applications.

Hemlibra continues to outperform its peers, holding on to 25% of the US market share for Hemophilia-A. Even Ocrevus has been outperforming others.

Regarding pipeline developments, Roche has been pouring resources for the trials of NASH drug candidate Crovalimab, which is now in Phase 3.

The acquisition of Inflazome in September and Enterprise Therapeutics in October indicate that Roche is looking to expand in the cystic fibrosis space as well.

Its recently inked agreement with Dyno Therapeutics also signals its plans to work on gene therapies, making itself a potential threat to the likes of biotechnology companies Alnylam (ALNY) and Ionis (IONS).

Looking at everything it has done and has yet to offer, I believe that Roche shares are undervalued at below the high $40s.

This company has a healthy lineup and promising R&D strategies combined with the capacity to buy high-potential assets.

I can see the company generating mid-single-digit cash flow growth on a long-term basis, and I even expect additional improvements to the dividend.

Given the returns you can get from Roche, I can say that this stock is very much worth consideration for any investor interested in quality growth.

Mad Hedge Biotech & Healthcare Letter

October 27, 2020

Fiat Lux

FEATURED TRADE:

(HOW VERTEX IS CURING THE INCURABLE)

(VRTX), (PTI), (GLPG), (CRSP)

Erratic. Unpredictable. Volatile. Take your pick of the descriptions used when it comes to biotechnology stocks. Each of these adjectives can be a fitting descriptor to the industry most of the time.

However, not all biotechnology companies fall under that category. Some are reasonably stable, offering steady and increasing profits.

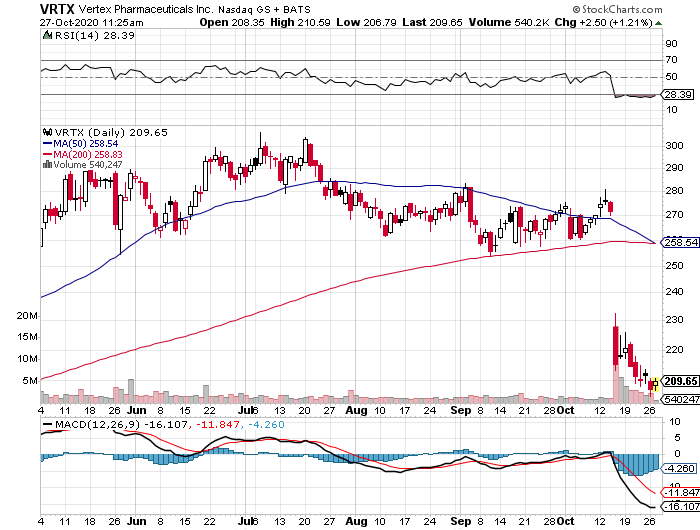

Vertex Pharmaceuticals (VRTX) is one of those biotechnology stocks that you can simply buy and hold for over a decade without losing any sleep.

One of the key factors in Vertex’s success is its monopoly on the cystic fibrosis (CF) market.

CF is a rare and life-threatening genetic disease that affects a patient’s digestive system and lungs. To date, there is no cure for this condition that overshadows the lives of 68,000 individuals in the US and the EU. However, there are treatment options for it.

Vertex developed the first-ever FDA-approved drug, Kalydeco, for the condition. As expected, it gained the much-coveted head start that led to its dominance today.

Its closest rivals, Proteostasis Therapeutics (PTI) and Galapagos NV (GLPG), are years away from ever catching up to the Massachusetts-based biotechnology stalwart. Neither has an approved drug as of today.

Since the approval of Kalydeco in 2012, Vertex stock has been enjoying an upward trajectory. With the recent addition of another CF blockbuster, Trikafta, the company is anticipated to keep its momentum.

From the moment Trikafta was released to the market, Vertex’s revenue and bottom line showed impressive growth. The drug, which is a triple combination therapy, is projected to capture almost 90% of the CF market worldwide.

Needless to say, Vertex has made it in the shade for at least the next 5 years, thanks to its CF market dominance.

In its second quarter earnings report, Vertex showed a 62% jump in its revenue year over year to hit $1.52 billion. Its net income of $837 million demonstrated a whopping 213% increase compared to the same period in 2019.

As anticipated, the star of the show was Trikafta.

The drug raked in $918 million in the second quarter alone – an amount higher than the combined sales of all the drugs in Vertex’s product line and an impressive growth from the $420 million it contributed last year.

As Vertex’s bottom line grew, its margins showed substantial improvement as well. Its operating margin for the second quarter of 2020 is at 57% compared to 44% during the same quarter last year.

With Vertex’s key metrics topping expectations, the company changed its 2020 revenue guidance from $5.7 billion to $5.9 billion, showing off a noteworthy increase from the $4 billion in sales it reported in 2019.

Although its CF pipeline has a number of promising candidates, Vertex is also looking outside the market for additional avenues of growth.

One of the most promising and exciting partnerships it forged in the past decade is with gene-editing company CRISPR Therapeutics (CRSP).

Just looking at this collaboration makes it clear that Vertex is once again playing the long game.

What we know so far is that the two companies are working on a treatment, called CTX001, for rare genetic blood disorders sickle cell disease and transfusion-dependent beta-thalassemia.

They are also developing two potential treatments for alpha-1 antitrypsin deficiency (AATD), which is a rare genetic liver and lung disorder that is similar to CF.

Detractors might point out that Vertex is a pricey stock. However, this biotechnology company currently has $71.2 billion in market capitalization.

More notably, it has no debt and holds $5.5 billion in cash. That puts the true value of Vertex at roughly $65.7 billion.

I believe that the biotechnology company’s overall outlook more than does justice for its valuation.

Granted that it is trading at 11 times its revenue and 26 times its adjusted EPS, its consistent performance and promising future ensure that its investors will be getting more bang for their buck.

In a word, Vertex remains a first-rate biotechnology stock to buy.