The biweekly strategy webinar scheduled for June 15 has been postponed until 12:00 PM EST on June 22. I will have my hands full hosting the Mad Hedge Traders & Investors Summit this week, which I hope you all attend.

I look forward to hearing from you again next week.

John Thomas

CEO & Publisher

Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/05/mr-john-thomas-1-e1595422688475.png567450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-06-13 11:04:032022-06-13 12:08:53The June 15 Biweekly Strategy Webinar is Postponed

Come join me for lunch for the Mad Hedge Fund Trader’s Global Strategy Update, which I will be conducting in London on Monday, June 29, 2022. A three-course lunch is included. This will be my first London Luncheon in six years.

I’ll be giving you my up-to-date view on stocks, bonds, currencies commodities, precious metals, energy, Bitcoin, and real estate.

And to keep you in suspense, I’ll be throwing a few surprises out there too. Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week. Tickets are available for $329.

The lunch will be held at a private club on St. James Street, the details of which will be emailed to you with your purchase confirmation. I just checked with the club and as of today, masks are not required.

I look forward to meeting you, and thank you for supporting my research.

To purchase tickets for this luncheon, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2022/04/London-1.png466620Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-06-10 12:04:322024-10-01 18:02:34SOLD OUT - Wednesday, June 29, 2022 London Strategy Luncheon

Due to overwhelming demand from readers, I am going to review the new Tom Cruise movie, Top Gun: Maverick.

I’m probably the only guy you will ever run into who has flown Mach 2.5 at 90,000 feet, and with 50 years of experience as a combat pilot, it’s safe to say I know my way around a cockpit, all of them.

For a start, they put Top Gun in the wrong state. The Naval Fighter Weapons School moved from North Island, San Diego to far cheaper Fallon Nevada in 1996, where I got my first Covid-19 shot.

But North Island definitely makes a much more scenic backdrop for a romantic backstory, the part where I fell asleep. I know it well and have given many speeches to graduating Top Gun and Naval Seal classes there over the years. You can’t beat those white sand beaches.

Let’s start with the stuff that doesn’t exist. The scramjet that Maverick takes to Mach 10.4 at the beginning of the movie probably won’t fly for another 20 years, it ever. In 2004, an unmanned test of the NASA X-43 scramjet did fly for ten seconds over the Pacific at Mach 10 and then crashed into the ocean.

There is work underway at the Lockheed Skunk Works at Edwards Air Force Base in California (you can see a skunk on the tail of Tom Cruise’s plane), but it’s so secret even I don’t know about it. My friend there, Kelly Johnson, passed away 32 years ago so no more inside tips. When this thing does fly, it will get you from New York to Tokyo in two hours.

The US does have a fifth-generation stealth fighter, the Lockheed Martin F-35 Lightning II that can go up against the Chinese Chengdu J-20 and the Russian Sukhoi-57 and beat them hands down. The F-35 can fly Mach 1.6. The movie implies only the enemy has these advanced planes, forcing our heroes to fly the ever-reliable, but constantly ungraded 44-year-old McDonnel Douglas F/A 18.

It is true that the military will pull old pilots out of retirement for special missions. I am a perfect example. When a pilot joins the military it’s for life and the only way to retire is to die in a crash. Maverick is retrieved from working on a WWII P51 Mustang, which I also fly.

This is because the military never throws anything out and will keep flying planes as long as they can find pilots. Our oldest flying B-52 Stratofortress is 70 years old, is slated to fly for 100 years in total, and was originally designed by Nazi Germany.

I thought the movie did a very accurate representation of high G-forces, which absolutely beat the crap out of you and are fatal above a reading of 10 where your internal organs explode. I have flown G-forces up to 10, and at that pressure, I weighed 2,000 pounds and my arms were so heavy I couldn’t reach the controls. I thought my Russian co-pilot was trying to kill me.

The same is true of the extreme aerobatics in the film, which are exhausting. Sometimes pilots have to be lifted out of their seats after such maneuvers.

Despite these factual transgressions, I enjoyed the movie, even though I spent half the movie saying to myself, “No way.” You can see they had massive support from the Navy and even had Blue Angle pilots flying the aerobatic and combat scenes (Tom Cruise was cut and pasted into the cockpit.) Sure, it was a stretch for them to steal a 52-year-old F-14 swing wing Tomcat and land it on a carrier. This is fiction after all. But it is all about us oldies.

That’s because many of the current Navy leadership were inspired to join by the first Top Gun movie in 1986 in which a much younger Tom Cruise also starred. It became the greatest Navy recruiting device of all time. It’s no surprise the Navy was all over this one like a wet blanket, lending them a squadron on F/A 18’s with real Top Gun pilots. How much did that cost?

Top Gun: Maverick has been far and away the biggest box office blockbuster of 2022 and signaled the return of many moviegoers for the first time since the pandemic. Call it a coming-out party for all of us. A Top Gun Barbie Doll has even hit the stores.

Sure Tom Cruise is getting old (59), but who am I to complain?

A Soviet Mig-29

My Russian Copilot

https://www.madhedgefundtrader.com/wp-content/uploads/2022/06/john-thomas-pilot.png486864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-06-10 12:02:052022-06-10 13:43:48My “Top Gun: Maverick Review”

“Altitude above you, runway behind you, and fuel in tanks on the ground are utterly useless,” said presidential candidate George McGovern, a WWII B-24 Liberator pilot.

https://www.madhedgefundtrader.com/wp-content/uploads/2022/06/george-mcgovern.png350350Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-06-10 12:00:062022-06-10 13:40:30Quote of the Day - June 10, 2022

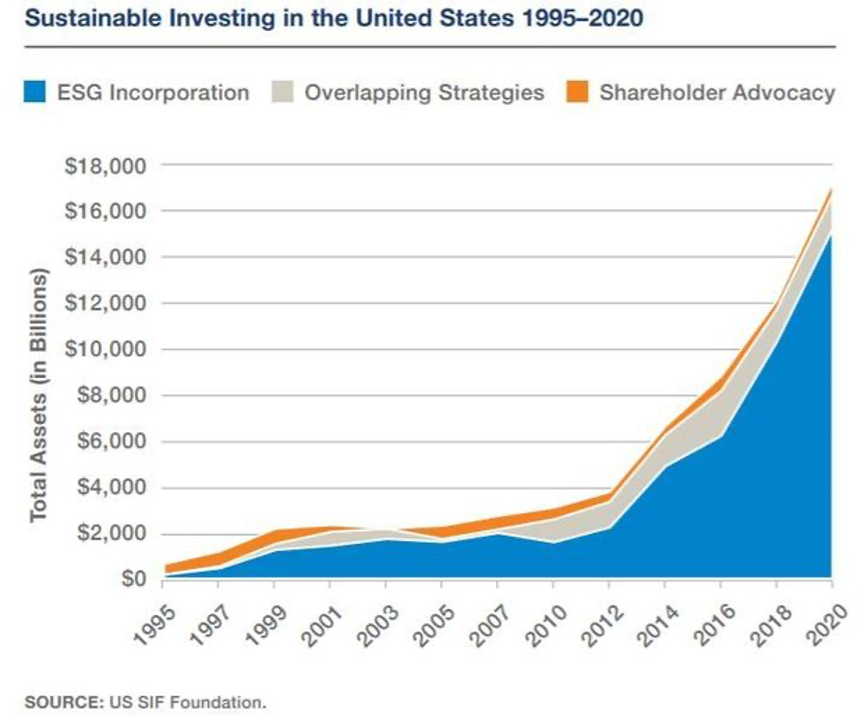

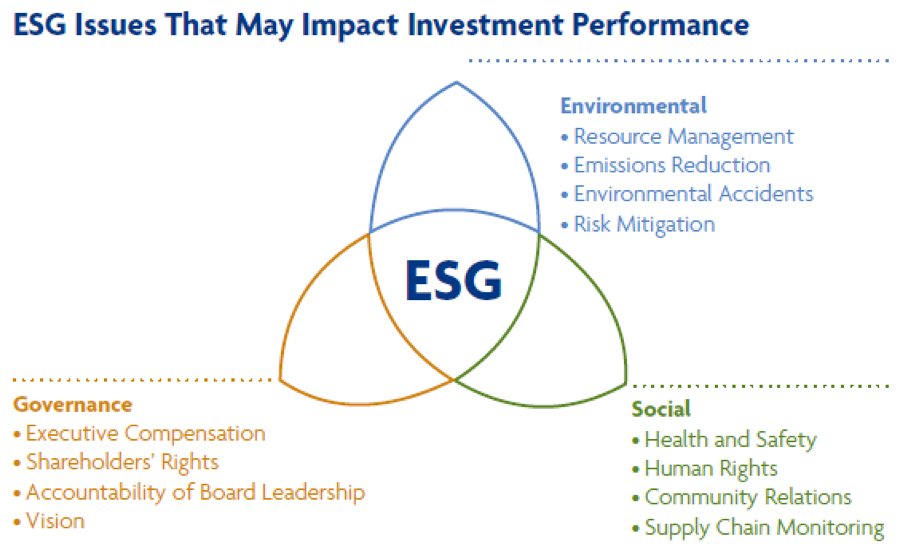

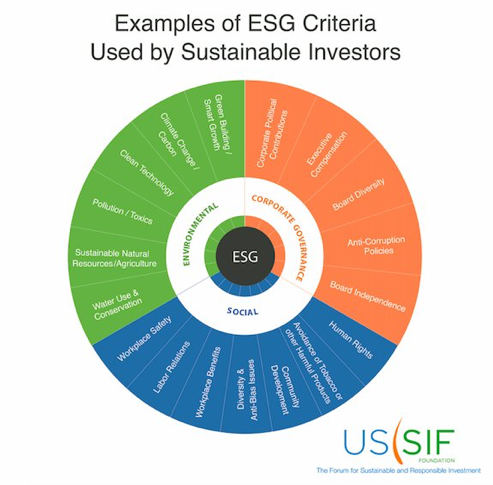

It’s truly astonishing how much money is pouring into ESG investing. Maybe it was another year of blistering heat worldwide that did it. It now accounts for one-third of all US equity investments.

In 2020, BlackRock, one of the largest fund managers in the country, made a major new commitment to ESG investment by rolling out several new ETFs. I thought I’d better take him seriously, as his firm is one of the largest money managers in the world with $10 trillion in assets.

So what the heck is ESG investing?

Environmental, Social, and Governance Investing (ESG) seeks to address climate change in any way shape or form possible. Its goal is to move the economy and capital away from carbon-based energy forms, like oil (USO), natural gas (UNG), and coal, to any kind of alternative.

I am always suspicious of investment themes are politically correct and ideologically directed, as they usually end in tears. I can’t tell you how many people I know who invested their life savings in solar companies to save the world, like Solyndra, Sungevity, American Solar Direct, and Suniva, only to get wiped out when they went under.

As laudable as the goals of these companies may have been, they were unable to deal with collapsing prices, Chinese dumping, and the harsh realities of doing business in a cutthroat competitive world.

As a venture capital friend of mine once told me, “Technology is a bakery business”. If you can’t sell your products immediately, you go broke. Technology always drops prices dramatically and if you can’t stay ahead of the curve you don’t stand a chance.

Still, what I believe is not important. The fastest-growing group of new investors in the market today are Millennials, and they happen to take ESG investing very seriously.

There does seem to be a method to BlackRock’s madness. Over the past year, ESG-influenced funds have grown from 1% to 3.6% of total investment. Other major fund families like Vanguard have already jumped on the bandwagon.

ESG can include a panoply of activities, including, recycling, climate change mitigation, carbon footprint reduction, water purification, green infrastructure, environmental benefits for employees, and greenhouse gas reduction. There are many more.

There is even an ESG rating system for funds and companies produced by firms like Refinitiv, which scores 7,000 companies around the world based on their environmental sensitivity. Companies like United Utilities Group PLC, the UK’s largest water company, get an A+, while China’s Guangdong Investment Ltd, which supplies water and energy to Hong Kong, gets a D-.

It goes without saying that companies from emerging nations tend to score very poorly. So do manufacturing companies relative to service ones, and energy companies versus non-energy ones.

The ESG concept began in 2005 when UN Secretary-General Kofi Annan wrote to 50 global CEOs urging them to take climate change seriously. A major report by Ivor Knoepfel followed a year later entitled “Who Cares Wins.”

The report made the case that embedding environmental, social and governance factors in capital markets makes good business sense and leads to more sustainable markets and better outcomes for societies. The snowball has been rolling ever since.

Themed investing is not new. “Sin” stocks have long been investment pariahs, including alcohol and tobacco companies. As a result, these companies trade at permanently low multiples. The newest investment ban is on firearms-related companies.

ESG investment received a major tailwind in 2021 when the price of oil took off like a rocket. When oil prices rise, it also makes all forms of alternative energy more competitive. But over production by US fracking companies will eventually cause supply gluts that will lead to chronically lower prices. The US happens to have a new 200-year supply of oil and gas, thanks to the fracking revolution.

Saudi Arabia floated their oil monopoly, Saudi ARAMCO, raising a record $26 billion. When Saudi Arabia wants to get out of the oil and gas business, so should you. It’s not because they can’t think of new ways to spend money that they’re unloading it.

That’s why I have been advising followers to avoid energy investments like the plague for the past decade. It’s just a matter of time before alternatives rule the world. Even the oil industry won’t expand production now because they don’t want to buy at the top only to see prices collapse, as they have done many times in the past.

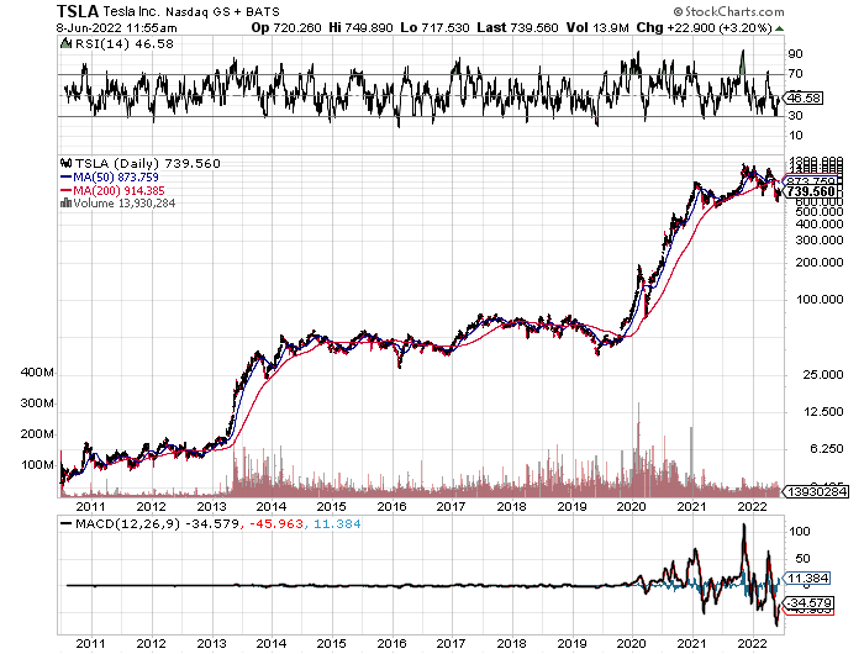

Who is the greenest company in America? That would be electric car and autonomous driving firm Tesla (TSLA). Perhaps ESG investing helps explain why the shares have risen 400 times since I started buying.

What is the top-performing listed stock of the last 30 years? Tobacco company Altria Group (MO), the old Philip Morris.

It’s proof that investment shaming doesn’t always work.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/01/investments.png424570Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-06-09 10:02:432022-06-09 10:21:40What the Heck is ESG Investing?

Come join me for lunch at the Mad Hedge Fund Trader’s Global Strategy Update, which I will be conducting in San Francisco on Monday, June 20, 2022. An excellent meal will be followed by a wide-ranging discussion and an extended question and answer period.

I’ll be giving you my up-to-date view on stocks, bonds, currencies, commodities, precious metals, and real estate. And to keep you in suspense, I’ll be throwing a few surprises out there too. Tickets are available for $249.

I’ll be arriving at 11:30 and leaving late in case anyone wants to have a one-on-one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at a private club in downtown San Francisco near Union Square, details of which will be emailed with your purchase confirmation.

I look forward to meeting you and thank you for supporting my research. To purchase tickets for this luncheon, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2022/04/San-francisco-e1650931095655.png371580Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-06-08 10:04:312024-10-01 18:02:46SOLD OUT - Friday, June 17, 2022 San Francisco Strategy Luncheon

I know all of this may sound confusing at first. But once you get the hang of it, this is the greatest way to make money since sliced bread.

I still have seven positions left in my model trading portfolio, they are all deep in-the-money, and about to expire in seven trading days. That opens up a set of risks unique to these positions.

I call it the “Screw up risk.”

As long as the markets maintain current levels, ALL of these positions will expire at their maximum profit values.

With the June 17 options expiration upon us, there is a heightened probability that your short position in the options may get called away.

If it happens, there is only one thing to do: fall down on your knees and thank your lucky stars. You have just made the maximum possible profit for your position instantly.

Most of you have short option positions, although you may not realize it. For when you buy an in-the-money vertical option spread, it contains two elements: a long option and a short option.

The short options can get “assigned,” or “called away” at any time, as it is owned by a third party, the one you initially sold the put option to when you initiated the position.

You have to be careful here because the inexperienced can blow their newfound windfall if they take the wrong action, so here’s how to handle it correctly.

Let’s say you get an email from your broker telling you that your call options have been assigned away.

I’ll use the example of the S&P 500 (SPY) June 2022 $430-$440 in-the-money vertical BEAR PUT spread.

For what the broker had done in effect is allow you to get out of your put spread position at the maximum profit point days before the June 17 expiration date. In other words, what you bought for $9.00 on May 23 is now worth $10.00, giving you a near-instant profit of $1,200 or 11.11%!

All have to do is call your broker and instruct them to “exercise your long position in your (SPY) June 2022 $440 puts to close out your short position in the (SPY) June 2022 $430 puts.”

You must do this in person. Brokers are not allowed to exercise options automatically, on their own, without your expressed permission. This is a perfectly hedged position, with both options having the same name and the same expiration date, so there is no risk. The name, number of shares, and number of contracts are all identical, so you have no exposure at all.

Calls are a right to buy shares at a fixed price before a fixed date, and one options contract is exercisable into 100 shares.

Short positions usually only get called away for dividend-paying stocks or interest-paying ETFs. There are strategies out here that try to capture dividends the day before they are payable. Exercising an option is one way to do that.

Weird stuff like this happens in the run-up to options expirations like we have coming.

A call owner may need to buy a long (SPY) position after the close, and exercising his long (SPY) call is the only way to execute it.

Adequate shares may not be available in the market, or maybe a limit order didn’t get done by the market close.

There are thousands of algorithms out there which may arrive at some twisted logic that the puts need to be exercised.

Many require a rebalancing of hedges at the close every day which can be achieved through option exercises.

And yes, options even get exercised by accident. There are still a few humans left in this market to blow it by writing shoddy algorithms.

And here’s another possible outcome in this process.

Your broker will call you to notify you of an option called away, and then give you the wrong advice on what to do about it.

There is a further annoying complication that leads to a lot of confusion. Lately, brokers have resorted to sending you warnings that exercises MIGHT happen to help mitigate their own legal liability.

They do this even when such an exercise has zero probability of happening, such as with a short call option in a LEAPS that has a year or more left until expiration. Just ignore these, or call your broker and ask them to explain.

This generates tons of commissions for the broker but is a terrible thing for the trader to do from a risk point of view, such as generating a loss by the time everything is closed and netted out.

There may not even be an evil motive behind the bad advice. Brokers are not investing a lot in training staff these days. In fact, I think I’m the last one they really did train.

Avarice could have been an explanation here but I think stupidity and poor training and low wages are much more likely.

Brokers have so many ways to steal money legally that they don’t need to resort to the illegal kind.

This exercise process is now fully automated at most brokers but it never hurts to follow up with a phone call if you get an exercise notice. Mistakes do happen.

Some may also send you a link to a video of what to do about all this.

If any of you are the slightest bit worried or confused by all of this, come out of your position RIGHT NOW at a small profit! You should never be worried or confused about any position tying up YOUR money.

Professionals do these things all day long and exercises become second nature, just another cost of doing business.

If you do this long enough, eventually you get hit. I bet you don’t.

Calling All Options!

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/Call-Options.png345522Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-06-08 10:02:452022-06-08 14:33:21A Note on Assigned Options, or Options Called Away

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.