Global Market Comments

January 17, 2020

Fiat Lux

Featured Trade:

(BETTER BATTERIES HAVE BECOME BIG DISRUPTERS)

(TSLA), (XOM), (USO)

Global Market Comments

January 17, 2020

Fiat Lux

Featured Trade:

(BETTER BATTERIES HAVE BECOME BIG DISRUPTERS)

(TSLA), (XOM), (USO)

Global Market Comments

January 16, 2019

Fiat Lux

Featured Trade:

(WHAT THE HECK IS ESG INVESTING?),

(TSLA), (MO)

(WILL UNICORNS KILL THE BULL MARKET?),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

I am always watching for market-topping indicators and I have found a whopper. The number of new IPOs from technology mega unicorns is about to explode. And not by a little bit but a large multiple, possibly tenfold.

Some 220 San Francisco Bay Area private tech companies valued by investors at more than $700 billion are likely to thunder into the public market next year, raising buckets of cash for themselves and minting new wealth for their investors, executives, and employees on a once-unimaginable scale.

Will it kill the goose that laid the golden egg?

Newly minted hoody-wearing millionaires are about to stampede through my neighborhood once again, buying up everything in sight.

That will make 2020 the biggest year for tech debuts since Facebook’s gargantuan $104 billion initial public offering in 2012. The difference this time: It’s not just one company but hundreds that are based in San Francisco, which could see a concentrated injection of wealth as the nouveaux riches buy homes, cars and other big-ticket items.

If this is not ringing a bell with you, remember back to 2000. This is exactly the sort of new issuance tidal wave that popped the notorious Dotcom Bubble.

And here is the big problem for you. If too much money gets sucked up into the new issue market, there is nothing left for the secondary market, and the major indexes can fall by a lot. Granted, probably only $100 billion worth of stock will be actually sold, but that is still a big nut to cover.

The onslaught of IPOs includes home-sharing company Airbnb at $31 billion, data analytics firm Palantir at $20 billion, and FinTech company Stripe at $20 billion.

The fear of an imminent recession starting sometime in 2020 or 2021 is the principal factor causing the unicorn stampede. Once the economy slows and the markets fall, the new issue market slams shut, sometimes for years as they did after 2000. That starves rapidly growing companies of capital and can drive them under.

For many of these companies, it is now or never. They have to go public and raise new money or go under. The initial venture capital firms that have had their money tied up here for a decade or more want to cash out now and roll the proceeds into the “next big thing,” such as blockchain, healthcare, or artificial intelligence. The founders may also want to raise some pocket money to buy that mansion or mega yacht.

Or, perhaps they just want to start another company after a well-earned rest. Serial entrepreneurs like Tesla’s Elon Musk (TSLA) and Netflix’s Reed Hastings (NFLX) are already on their second, third, or fourth startups.

And while a sudden increase in new issues is often terrible for the market, getting multiple IPOs from within the same industry, as is the case with ride-sharing Uber and Lyft, is even worse. Remember the five pet companies that went public in 1999? None survived.

Some 80% of all IPOs lost money last year. This was definitely NOT the year to be a golfing partner or fraternity brother with a broker.

What is so unusual in this cycle is that so many firms have left going public to the last possible minute. The desire has been to milk the firms for all they are worth during their high growth phase and then unload them just as they go ex-growth.

Also holding back some firms from launching IPOs is the fear that public markets will assign a lower valuation than the last private valuation. That’s an unwelcome circumstance that can trigger protective clauses that reward early investors and punish employees and founders. That happened to Square (SQ) in its 2015 IPO.

That’s happening less and less frequently: In 2019, one-third of IPOs cut companies’ valuations as they went from private to public. In 2019, that ratio has dropped to one in six.

Also unusual this time around is an effort to bring in more of the “little people” in the IPO. Gig economy companies like Uber and Lyft have lobbied the SEC for changes in new issue rules that enabled their drivers to participate even though they may be financially unqualified. They were all hit with losses of a third once the companies went public.

As a result, when the end comes, this could come as the cruelest bubble top of all.

Global Market Comments

January 15, 2020

Fiat Lux

Featured Trade:

(FRIDAY, JANUARY 31, 2020 GUADALCANAL STRATEGY LUNCHEON)

(A RADICAL VIEW OF THE MARKETS),

(INDU), (SPY)

Come join me for lunch at the Mad Hedge Fund Trader’s Global Strategy Update, which I will be conducting in Honiara in the Solomon Islands at 12:30 PM on Friday, January 31, 2020.

An excellent meal will be followed by a wide-ranging discussion and an extended question-and-answer period.

I’ll be giving you my up-to-date view on stocks, bonds, currencies, commodities, precious metals, energy, and real estate.

And to keep you in suspense, I’ll be throwing a few surprises out there too.

Tickets are available for $299.

The lunch will be held at the only decent hotel in the Solomon Islands, one of the poorest countries in the world. Malaria is endemic, so bring your Malaria pills (start taking them three days before departure). Typhoid shots will also be helpful.

If you have any questions about the Guadalcanal luncheon, please email me at support@madhedgefundtrader.com. Just put “Guadalcanal Luncheon” in the subject line.

I look forward to meeting you and thank you for supporting my research. To purchase tickets for this luncheon, please click here.

When the Commandant of the Marine Corps asks for a favor, you say “Yes Sir” without hesitating. So when General David H. Berger called me and asked to represent him at the 78th annual memorial service for the 1942 Battle of Guadalcanal, I started booking my flight.

It seems I’m the only living Corps veteran who had both a father and an uncle fight at Guadalcanal, who also speaks Japanese. That will enable me to sympathize with the Japanese families attending the service who lost loved ones.

I have acted as a diplomatic representative for the Marine Corps for many decades. Over the years, I have met presidents, Medal of Honor winners, and Navaho code talkers. My favorite was always the annual D-Day memorials at the Normandy beaches where I usually participated in a flyover. For a history buff like me, it’s a dream come true. Plus, Normandy had better food.

Guadalcanal was the decisive battle of WWII. The Americans lost 7,000 men, 25 ships, and 175 planes. The Japanese lost 30,000 men, 25 ships, including a major battleship, and 450 planes. Before Guadalcanal, the Japanese had never lost a battle. After Guadalcanal, they never won. If the US had lost Guadalcanal, WWII would have continued until 1948 or 1949.

What if the consensus is wrong?

What if instead of being in the 11th year of a bull market, we are actually in the first year, which has another decade to run? It is not only possible, it is probable. Personally, I give it a greater than 50% chance.

There is a possibility that the bear market that everyone and his brother has been long predicting and that the talking heads assure you is imminent, has already happened.

It took place during the fourth quarter of 2018, when the Dow Average plunged a heart-rending 20%. How could this be a bear market when historical ursine moves down lasted anywhere from six months to two years?

Blame it all on hyperactive algorithms, risk parity traders, and hedge funds, which adjust portfolios with the speed of light. If this WAS a bear market and you blinked, then you missed it.

It certainly felt like a bear market at the time. Lead stocks like Amazon (AMZN), Apple (AAPL), Facebook (FB), and Alphabet (GOOGL) were all down close to 40% during this hellacious three-month period. High beta stocks like Roku (ROKU), one of our favorites, was down 67% at the low. It has since risen by 600%.

In my experience, if it walks like a duck and quacks like a duck, then it is a bear. If true, then the implications for all of us are enormous.

If I’m right, then my 2030 target of a Dow Average of $125,000, an increase of 331% no longer looks like the mutterings of a mad man, nor the pie in the sky dreams of a permabull. It is in fact eminently doable, calling for a 15% annual gain until then, with dividends.

What have we done over the last ten years? How about 13.08% annually with dividends reinvested for a total 313% gain.

For a start, from here on, we should be looking to buy every dip, not sell every rally. Institutional cash levels are way too high, and bearishness is rampant.

It all brings into play my Golden Age scenario of the 2020s, a repeat of the Roaring Twenties, which I have been predicting for the last ten years. This calls for a generation of 85 million big spending Millennials to supercharge the economy. Anything you touch will turn to gold, as they did during the 1980s, the 1950s, and well, the 1920s. Making money will be like falling off a log.

If this is the case, you should be loading the boat with technology stocks and biotech stocks at every opportunity. Although stocks look expensive now, they are still only at one-fifth peak valuations of the 2000 summit.

Let me put out another radical, out-of-consensus idea. It has become fashionable to take the current red-hot stock market as proof of a Trump win in the 2020 election.

What if the opposite is true? What if, in fact, the market is discounting a Trump defeat? It makes economic sense. It would bring an immediate end to our trade war with the world, which is currently costing us 1% a year in GDP growth. Take Trump out of the picture and our economy gets that 1% back immediately, leaping from 2% to 3% growth a year.

The last Roaring Twenties started with doubts and hand wringing similar to what we are seeing now. Everyone then was expecting a depression in the aftermath of WWI, now that the big-time military spending was ending. After a year of hesitation, massive reconstruction spending in Europe and a shift from military to consumer spending won out, leading to the beginning of the Jazz Age, flappers, and bathtub gin.

I know all this because my grandmother regaled me with these tails, an inveterate flapper herself. This is the same grandmother who owned the land under the Bellagio Hotel in Las Vegas until 1978 and then sold it for $10 million.

It all sets up another “Roaring Twenties” very nicely. You will all look like geniuses.

I just thought you’d like to know.

"Where a calculator on the Eniac is equipped with 18,000 tubes and weighs 30 tons, computers in the future may have only 1,000 vacuum tubes, and weigh 1.5 tons," said Popular Mechanics magazine in 1949.

Global Market Comments

January 14, 2020

Fiat Lux

Featured Trade:

(FRIDAY JANUARY 27, 2020 FIJI STRATEGY LUNCHEON)

(SHOPPING FOR FIRE INSURANCE IN A HURRICANE),

(VIX), (VXX), (XIV),

(THE ABC’s OF THE VIX),

(VIX), (VXX), (SVXY)

Global Market Comments

January 13, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE TITANIUM MARKET)

(SPY), (TLT), (TSLA), (GLD), (USO), (NFLX), (DIS), (LEN), (BA)

It is not true that this is a Teflon market, rising almost every day for four months.

It is a titanium market.

The more worries placed in front of us, the faster it rises. And this is happening in the face of falling earnings. This can only end in tears. The only question is how many pennies we can pick up in front of the steam roller before we get run over.

Here’s another sobering prediction. Goldman Sachs’ David Kotick expects that a Democratic win in this year’s election will cause S&P earnings to drop from $169 in 2019 to $163 in 2021, the result of rising corporate tax rates.

Take the earnings multiple down from the present 20 to 15 times earnings where it was three years ago, and the stock index can plummet by 25%.

These are numbers to take seriously, especially given that the president is behind the front runners by 14 points in the national polls.

It all underlines the rising risk that the election poses to the market. Everyone I know to a man is pulling money out of the market, and inquiries about long volatility strategies (VIX) are rising daily.

The general agreement is that in 2020, we are going to have to work a lot harder for a lot less money. There isn’t going to be a repeat of the 28% gain we saw in 2019.

If there is, you want to sell all your stocks and your home, change your name, and move to Brazil, where there is no extradition treaty, because the following crash will be so enormous that no one will be spared.

The end of January 2018 comes to mind, which, after a meteoric move, markets plunged 17%.

Cash is a position, it is an opinion, has option value, and it is probably the best one of all to have right now. You can’t take advantage of any 17% dives if you go into them fully invested. I believe that once the New Year equity allocation is done, we could have a problem.

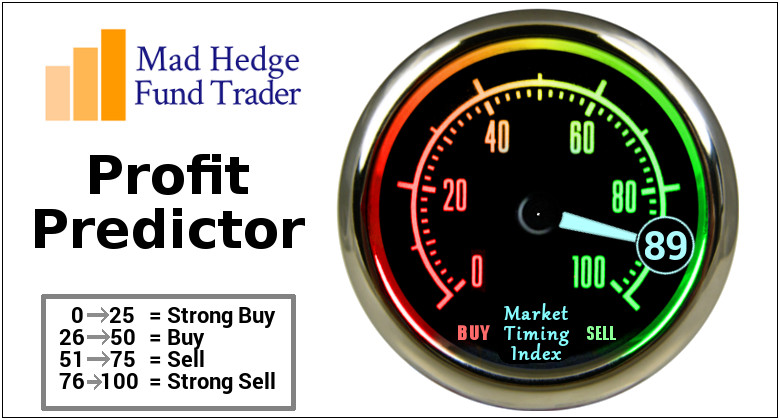

Risk exploded with the US assassination of an Iran general, with the country vowing revenge. Airline stocks globally went into free fall, and oil prices soared. Wildly overbought markets got their comeuppance, with the Mad Hedge Market Timing Index at an all-time high of 97. Wait three days for markets to price this in. I told you 2020 would be harder!

Gold approached a seven-year high on Iran attack, as over-leveraged traders scrambled for cover. So far, gold and oil are the trades of the decade, which is only seven days old. Keep buying (GLD) on dips, oil (USO) not so much. $1,927 an ounce, here we come!

Tesla deliveries hit new high in Q4, to a record 112,000. There was clearly a stampede before the $3,250 per vehicle clean air subsidy expired at yearend. Musk also cut prices 16% to $43,000 for the Shanghai-made Model 3, creating another stampede there. Keep buying (TSLA) on dips.

The Tesla market cap just peaked at $86 Billion, with the stock at an incredible $490 a share, making it the most valuable American car company in history. What is 25% of the global car market worth in a decade? Apparently quite a lot.

Netflix won big in the Golden Globes, capturing 17 nominations, with Amazon Prime close on their tail. It’s all about content streaming now. If they can only figure out how to take on Disney Plus and Apple Plus. Avoid (NFLX), buy (DIS) and (AMZN).

The S&P Case Shiller National Home Price Index rose 2.2% in October. Phoenix (5.8%), Tampa (4.9%), and Charlotte, NC (4.8%) showed biggest gains. Only San Francisco was down, the victim of lost SALT deductions. Housing still has another decade to run. Buy (LEN) on dips.

Boeing backs simulator training as a path back to flightworthiness for the 737 MAX. As a former flight instructor myself, this is what I have been advocating all along. Whenever things start to improve for Boeing, another crash happens as did with an antiquated 737 in Tehran last week, accidentally shot down by their own people. Keep buying dips in (BA).

The ADP Report showed a red-hot December, with 202,000 private sector job gains. If so, interest rate rises may come sooner than you think.

I never thought I’d say this, but the Mad Hedge Trade Alert Service has made no money so far this year. Of course, the year is only seven trading days old.

Buying the Mad Hedge Market Timing Index at 90 and selling it at 97 is not my kind of market. Nor should it be yours. The money being made now is very high-risk.

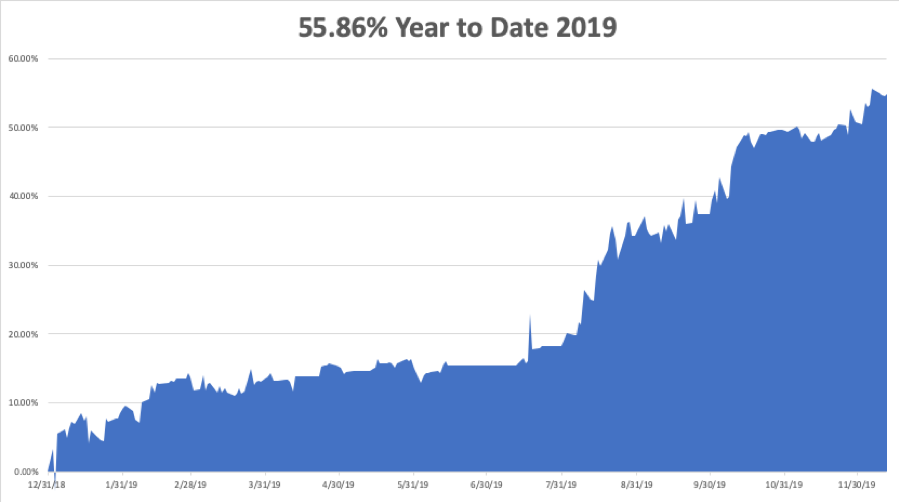

Better to sit on your laurels of a 55.86% profit last year and wait for a better entry point.

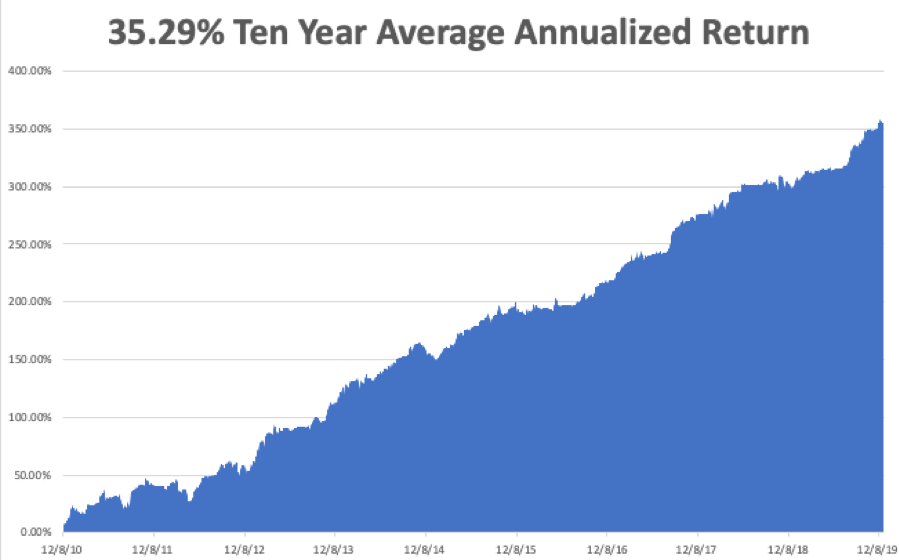

My Global Trading Dispatch performance held steady at +356.91% for the past ten years, an all-time high. My 2019 year-to-date came in at a final +55.86%. We closed out December with a market beating +4.97% profit. My ten-year average annualized profit ground back up to +35.28%.

The coming week will be a noneventful one on the data front, with only housing data gaining our attention..

On Monday, January 13 at 9:00 AM, Consumer Inflation Expectations for December are out.

On Tuesday, January 14 at 7:00 AM, the NFIB Business Optimism Index is released.

On Wednesday, January 15, at 6:15 AM, New York State Manufacturing is announced.

On Thursday, January 16 at 8:30 AM, Weekly Jobless Claims come out. December Retail Sales are published at 9:30.

On Friday, January 17 at 9:30 AM, December Housing Starts s are printed. At 10:30 Industrial Production is released.

The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I will be leading an Orienteering class in San Francisco this weekend, teaching 20 Boy Scouts how to use a compass and navigate over a ten-mile course. Hey, how bad can it be? I found California! Spoiler alert: after a ten-mile hike, we end up at the Ghirardelli Square Chocolate factory at Fisherman’s Wharf.

When I applied for the position, I listed as qualifications 50 years as an FAA commercial pilot and navigator, and a stint as a Marine Corps combat pilot.

They accepted me on the spot.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader