There’s nothing like a quickie five-day tour of the Southeast to give one an instant snapshot of the US economy. The economy is definitely overheating and could blow up sometime in 2019 or 2020.

Traffic everywhere is horrendous as drivers struggle to cope with a road system built to handle half the current US population. Service has gotten terrible as workers vacate the lower paid sectors of the economy. Everyone you talk to tells you business is great, from the CEOs down to the Uber drivers.

I managed to miss Hurricane Michael by two days. Hartsfield Jackson Atlanta International Airport was busy with exhausted transiting Red Cross workers. The Interstate from Savanna to Atlanta, Georgia was lined with thousands of downed trees. In Houston mountains of debris were evident everywhere, the rotting, soggy remnants of last year’s Hurricane Harvey.

I managed to score all day parking in downtown Atlanta for only $8. I kept the receipt to show my disbelieving friends at home.

Bull markets climb a wall of worry and this one has been no exception. However, the higher we get the greater the demands on the faithful.

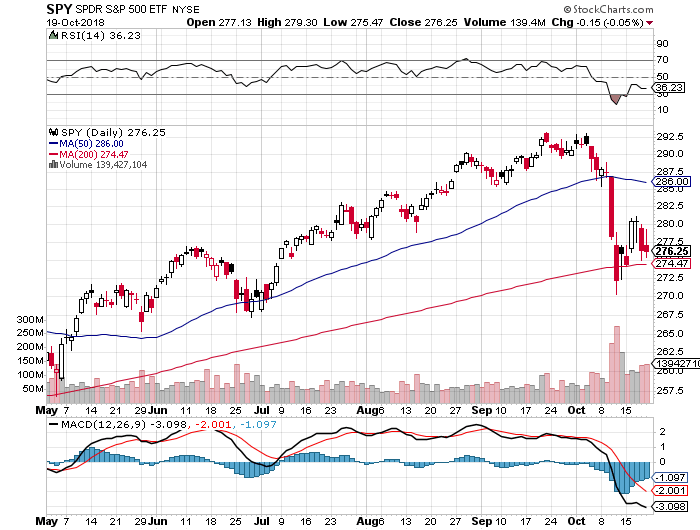

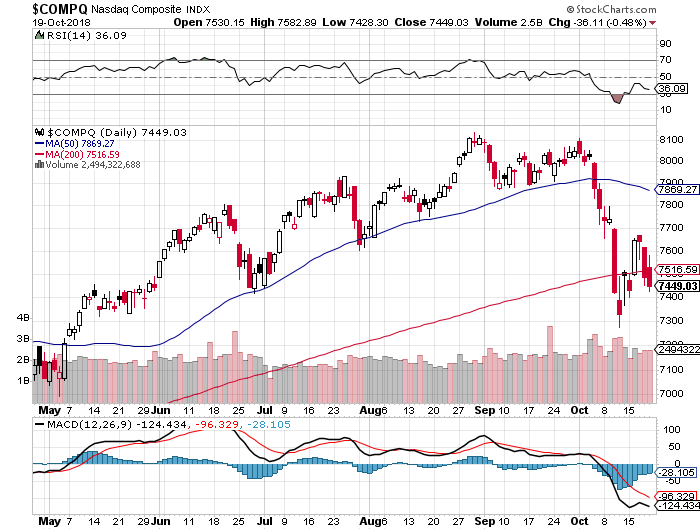

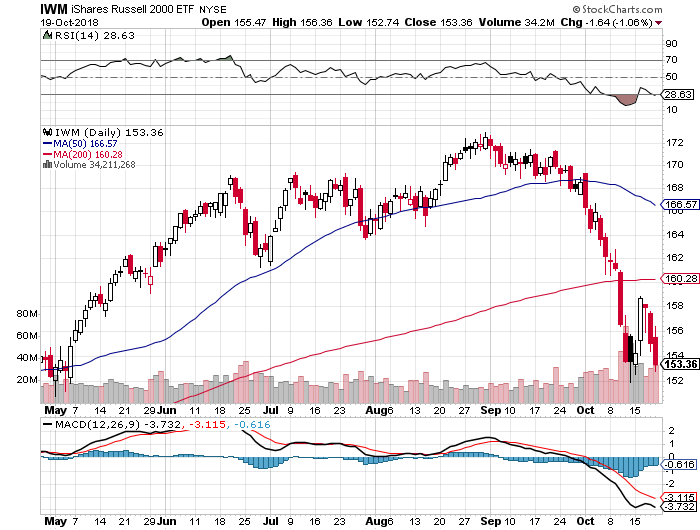

Last week saw my Mad Hedge Market Timing Index plunge to an all-time low reading of 4. I back-tested the data and was stunned to discover that October saw the steepest selloff since the 1987 crash, which saw the average crater 21% in one day.

And while evidence of a coming bear market is everywhere, the reality is that stocks can keep rising for another year. Market bottoms are easy to quantify based on traditional valuation measure, but tops are notoriously difficult to call. Look for one more high volume melt up like we saw in January and that should be it.

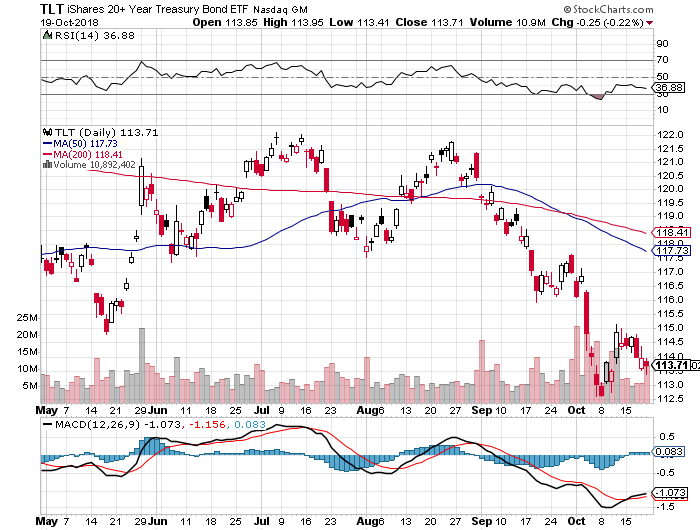

Real interest rates are still zero (3.2% bond yields – 3.2% inflation), so there is no way this is any more than a short-term correction in a bull market.

The world is still awash in liquidity

The Fed says they’re still raising rates four times in a year no matter what the president says. Look for a 3.25% overnight rate in a year, and 4% for three months funds. If inflation rises to 4% at the same time, real rates will still be at zero.

There certainly has not been a shortage of things to worry about on the geopolitical front. After Saudi Arabia was caught red-handed with video and audio proof of torturing and killing a Washington Post reporter, it threatened to cut off our oil supply and dump their substantial holding of technology stocks.

Tesla made another move towards the mass market by accelerating its release of the $35,000 Tesla 3. Production is now well over 6,000 units a month.

If you had any doubts that housing was now in recession, look no further than the September Existing Home Sales which were down a disastrous 3.5%. In the meantime, the auto industry continues to plumb new depths. In some industries, the recession has already started.

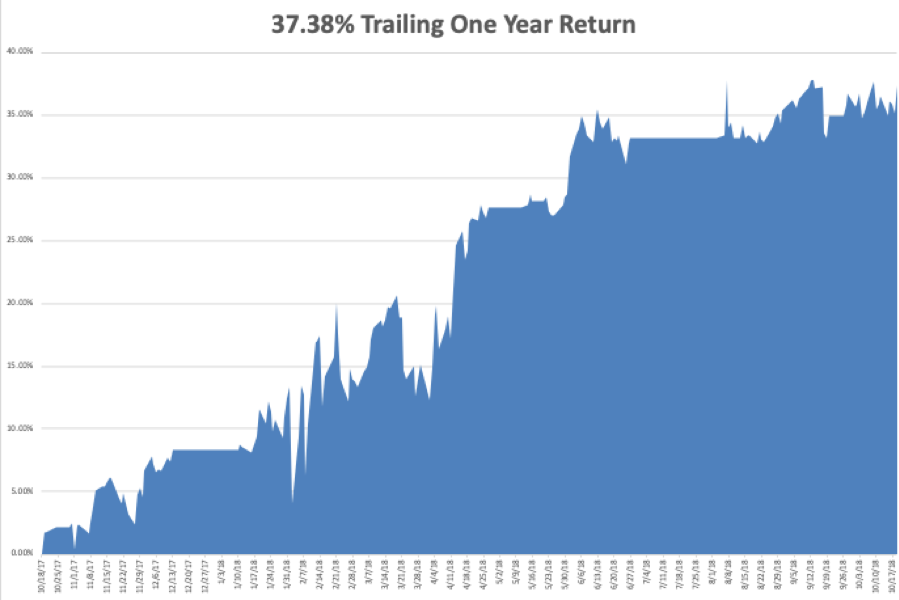

We have been killing it on the trading front. My 2018 year-to-date performance has bounced back to a robust 29.07%, and my trailing one-year return stands at 35.37%. October is up +0.68%, despite a gut-punching, nearly instant NASDAQ swoon of 10.50%. Most people will take that in these horrific conditions.

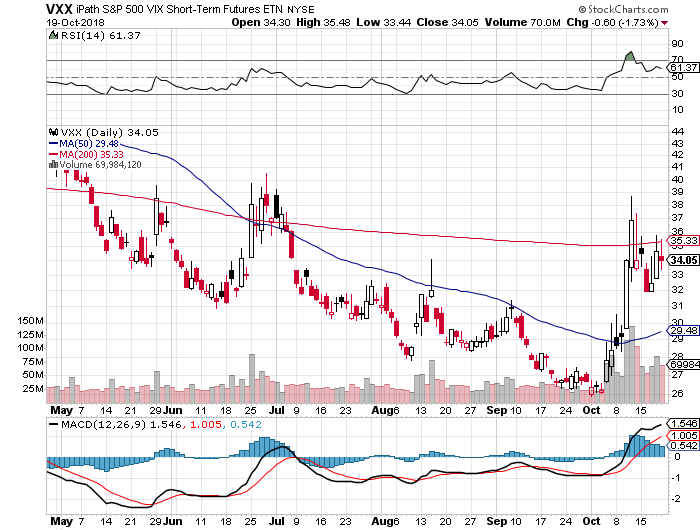

My single stock positions have been money makers, but my short volatility position (VXX), which I put on early, refuses to go down, eating up much of my profits.

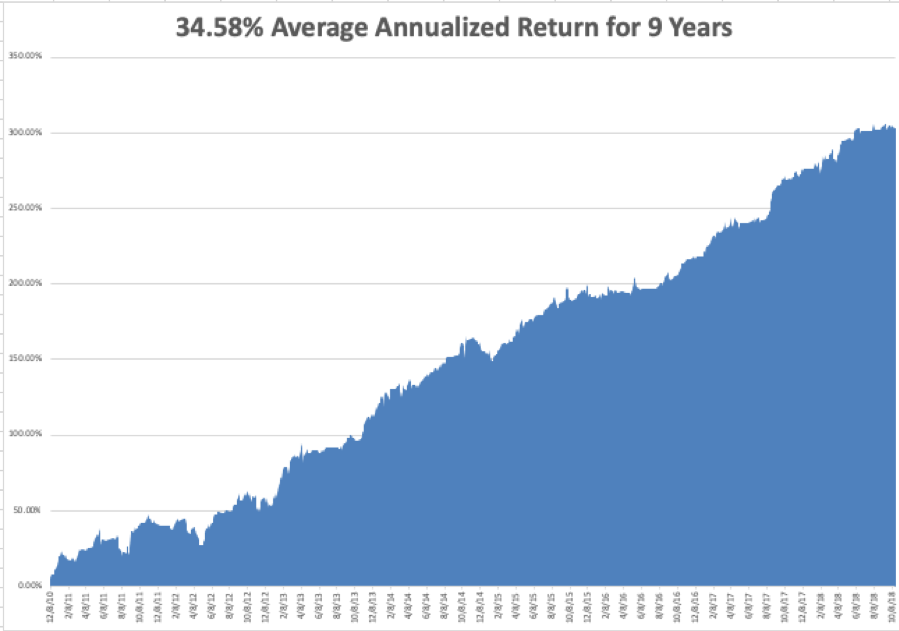

My nine-year return appreciated to 305.54%. The average annualized return stands at 34.58%. Global Trading Dispatch is now only 44 basis points from an all-time high.

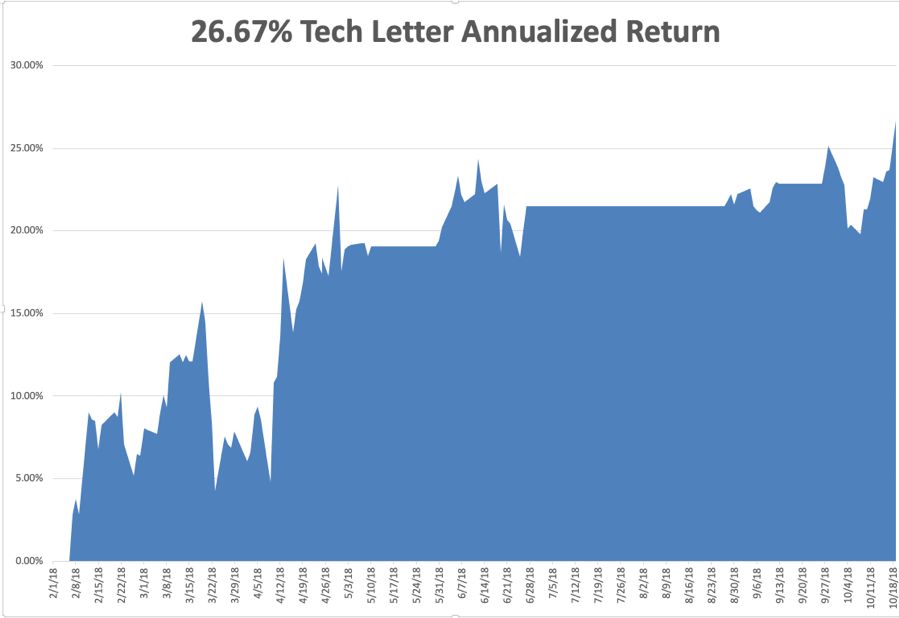

The Mad Hedge Technology Letter has done even better, blasting through to a new all-time high at an annualized 26.67%. It almost completely missed the tech meltdown and then went aggressively long our favorite names right at the market bottom.

I’d like to think my 50 years of trading experience is finally paying off, or maybe I’m just lucky. Who knows?

This coming week will be pretty sedentary on the data front, with the Friday Q3 GDP print the big kahuna. Individual company earnings reports will be the main market driver.

Monday, October 22 at 8:30 AM, the Chicago Fed National Activity Index is out. 3M (MMM), and Logitech (LOGI) report.

On Tuesday, October 23 at 10:00 AM, the Richmond Fed Manufacturing Index is published. Juniper Networks (JNPR), Lockheed Martin (LMT), and United Technologies report.

On Wednesday, October 24 at 10:00 AM, September New Home Sales will give another read on entry-level housing. At 10:30 AM the Energy Information Administration announces oil inventory figures with its Petroleum Status Report. Advanced Micro Devices (AMD), Ford Motor (F), and Microsoft (MSFT) report.

Thursday, October 25 at 8:30, we get Weekly Jobless Claims. Alphabet (GOOGL) and Intel (INTC) report.

On Friday, October 26, at 8:30 AM, a new read on Q3 GDP is announced.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I am headed up to Lake Tahoe this week to host the Mad Hedge Lake Tahoe Conference. The weather will be perfect, the evening temperatures in the mid-twenties, and there is already a dusting of snow on the high peaks. The Mount Rose Ski Resort is honoring the event by opening this weekend.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

“The next time we have a global economic crisis it will be much worse than in 2008. There will be money printing and war. The whole system will collapse. You don’t want to own government bonds and cash. Equities don’t do well, but at least you still have the ownership of companies. Precious metals do well in that environment, and so does oil,” said Mark Faber, publisher of the Gloom, Boom, and Doom Report.

Global Market Comments

October 19, 2018

Fiat Lux

Featured Trade:

(LAST CHANCE TO BUY TICKETS NOW FOR THE MAD HEDGE LAKE TAHOE CONFERENCE FOR OCTOBER 26-27)

(FIVE STOCKS TO BUY AT THE BOTTOM),

(AAPL), (AMZN), (SQ), (ROKU), (MSFT)

Tickets for the Mad Hedge Lake Tahoe Conference are selling briskly. If you want to obtain a ticket that includes a dinner with John Thomas and Arthur Henry you better get your order in soon.

The conference date has been set for Friday and Saturday, October 26-27.

Come learn from the greatest trading minds in the markets for a day of discussion about making money in the current challenging conditions.

How soon will the next bear market start and the recession that inevitably follows?

How will you guarantee your retirement in these tumultuous times?

What will destroy the economy first, rising interest rates or a trade war?

Who will tell you what to buy at the next market bottom?

John Thomas is a 50-year market veteran and is the CEO and publisher of the Diary of a Mad Hedge Fund Trader. John will give you a laser-like focus on the best-performing asset classes, sectors, and individual companies of the coming months, years, and decades. John covers stocks, options, and ETFs. He delivers your one-stop global view.

Arthur Henry is the author of the Mad Hedge Technology Letter. He is a seasoned technology analyst and speaks four Asian languages fluently. He will provide insights into the most important investment sector of our generation.

The event will be held at a five-star resort and casino on the pristine shores of Lake Tahoe in Incline Village, NV, the precise location of which will be emailed to you with your ticket purchase combination.

It will include a full breakfast on arrival, a sit-down lunch, coffee break. The wine served will be from the best Napa Valley vineyards.

Come rub shoulders with some of the savviest individual investors in the business, trade investment ideas, and learn the secrets of the trading masters.

Ticket Prices

Copper Ticket - $599: Saturday conference all day on October 27, with buffet breakfast, lunch, and coffee break, with no accommodations provided

Silver Ticket - $1,299: Two nights of double occupancy accommodation for October 26 & 27, Saturday conference all day with buffet breakfast, lunch and coffee break

Gold Ticket - $1,499: Two nights of double occupancy accommodation for October 26 & 27, Saturday conference all day with buffet breakfast, lunch, and coffee break, and an October 26, 7:00 PM Friday night VIP Dinner with John Thomas

Platinum Ticket - $1,499: Two nights of double occupancy accommodation for October 26 & 27, Saturday conference all day with buffet breakfast, lunch, and coffee break, and an October 27, 7:00 PM Saturday night VIP Dinner with John Thomas

Diamond Ticket - $1,799: Two nights of double occupancy accommodation for October 26 & 27, Saturday conference all day with buffet breakfast, lunch, and coffee break, an October 26, 7:00 PM Friday night VIP Dinner with John Thomas, AND an October 27, 7:00 PM Saturday night VIP Dinner with John Thomas

Schedule of Events

Friday, October 26, 7:00 PM

7:00 PM - Exclusive dinner with John Thomas and Arthur Henry for 12 in a private room at a five-star hotel for gold and diamond ticket holders only

Saturday, October 27, 8:00 AM

8:00 AM - Breakfast for all guests

9:00 AM - Speaker 1: Arthur Henry - Mad Hedge Technology Letter editor Arthur Henry gives the 30,000-foot view on investing in technology stocks

10:00 AM - Speaker 2: Brad Barnes of Entruity Wealth on "An Introduction to Dynamic Risk Management for Individuals"

11:00 AM - Speaker 3: John Thomas - An all-asset class global view for the year ahead

12:00 PM - Lunch

1:30 PM - Speaker 4: Arthur Henry - Mad Hedge Technology Letter editor on the five best technology stocks to buy today

2:30 PM - Speaker 5: John Triantafelow of Renaissance Wealth Management

3:30 PM - Speaker 6: John Thomas

4:30-6:00 PM - Closing: Cocktail reception and open group discussions

7:00 PM - Exclusive dinner with John Thomas for 12 in a private room at a five-star hotel for Platinum or Diamond ticket holders only

To purchase tickets, click: CONFERENCE.

“When we launch a product, we're already working on the next one. And possibly even the next, next one.” – Said CEO of Apple Tim Cook

Global Market Comments

October 18, 2018

Fiat Lux

SPECIAL TRAVEL PLANNING ISSUE

Featured Trade:

(IS AIRBNB YOUR NEXT TEN BAGGER?)

“The red light on a television camera going on has the same effect on members of Congress as a full moon does on werewolves,” said former Secretary of Defense, Robert Gates.

Global Market Comments

October 17, 2018

Fiat Lux

Featured Trade:

(WHO WAS THE GREATEST WEALTH CREATOR IN HISTORY?)

(FB), (AAPL), (GOOG), (AMZN),

(XOM), (BRKY), (T), (GM), (VZ), (CCA),

(WHY DOCTORS MAKE TERRIBLE TRADERS?)

Global Market Comments

October 16, 2018

Fiat Lux

Featured Trade:

(WHY COAL IS A SHORT),

(KOL), (BHP), (UNG),

(TESTIMONIAL)

What has been one of the top performing asset classes since the beginning of 2016?

Is it Apple (AAPL), Amazon (AMZN), gold (GLD), oil (USO), or collectible French postage stamps?

If you said “Coal,” you win the kewpie doll.

In fact, the 19thcentury energy source was one of the best investments you could have made over the past three years.

Indeed, the Van Eck Coal ETF (KOL) has picked up an eye-popping 210% since it printed its $5 low the first week of 2016.

Google (GOOG) eat your heart out.

You might give credit to the president for the meteoric move, thanks to policies so overwhelmingly helpful to the industry that they brought tears to the eyes of the owners of coal mining companies.

But you’d be wrong again.

Most of the move took place before the election.

As a result, I have recently been deluged from readers asking if it is time to buy this prehistoric energy source.

My answer is no, not ever, and not even with Donald Trump’s money.

However, my answer relies more on basic market dynamics rather than any environmental sympathies I might have.

You can blame China.

The Beijing government is manipulating its domestic coal industry to prevent them from defaulting on hundreds of billions of dollars with of loans to local banks.

So, it has cut back the number of days the industry can operate from 330 to 276 days a year.

What happens when you restrict supply and increase demand? Prices go through the roof as they have done smartly.

It gets better.

The Middle Kingdom was hit with rainstorms of biblical proportions, flooding many mines and forcing them to close many mines. The sushi hit the fan.

That forced major consumers, the big steel producers, and electric power plants to resort to the international spot market, or the “seaborne market” to cover shortages to avoid shutting down themselves.

Who is the world’s largest supplier to the seaborne market?

That would be BHP Billiton (BHP), the largest capitalized company in Australia, which has seen its shares appreciate by 144% since 2016 bottom.

I have been following coal for 45 years ever since I was the coal correspondent for the Australian Financial Review during the 1970’s.

I had to write a mind-numbing five pieces a week on coal (the AFR was a daily). So it’s safe to say that I know which end of a lump of coal to hold upward.

For a start, you never want to invest in an asset that is dependent on government fiat for rising prices. They can change their minds at any time. The loans in question could get paid off.

And you can count on the world market to suddenly find new supplies whenever a commodity price doubles.

Remember the Rare Earths bubble where we were active players?

After a hyperbolic bubble, prices fell by 90%. Rare earth turned out to be not so rare. Only the cheap labor to extract them free of environmental regulation was.

So you can count on the current coal bubble to deflate eventually. The perfect storm is about to run in reverse.

That leaves us with the long-term fundamentals of coal which are bleak, to say the least.

China is far and away the world’s largest coal consumer at 49%, followed by the US at 11%. This is why China is also the world’s largest producer of greenhouse gases.

China is making every effort to reduce reliance on these cheapest form of energy, thanks to the blinding, choking smog alerts besetting its largest cities.

It is only still using coal because with an economy growing at 6.6% a year plus, it has to rely on every energy form just to keep the lights only. Power brownouts can lead to political instability.

Coal consumption in the US has been in a death spiral for years falling from 50% to 33% of electric power generation over the past decade.

That led to the bankruptcy of several of its largest players such as Arch Coal (ACI) and Peabody Energy (BTU).

The collapse of natural gas prices to $2/btu made a cleaner burning alternative cost-competitive. And gas lacks the nitrous and sulfur oxides and particulate pollution prevalent in coal.

Read the prospectus of any electric power companies and you will find them besieged by lawsuits from consumers claiming that the coal they burned caused their asthma and cancers. Utility companies would love to be rid of it.

And then there’s solar energy.

California governor Jerry Brown has signed the nation’s toughest climate legislation, mandating that all power come from alternative sources by 2030.

On several days this year, alternatives already accounted for 100% of the state’s total power production.

While ambitious, the target is viewed as doable. Solar energy, which now accounts for 5% of the state’s power output, will do the heavy lifting.

Many other states are expected to follow suit. No room for coal here.

The United Kingdom has already taken this path as have many other nations.

It says a lot that a country that ran a coal-based economy for 300 years announces the closing of its last mine which it did a few years ago. It will replace the power output with alternatives.

Having lived in England during the violent miner’s strikes during the early 1980s, it was quite a revelation.

So the writing is on the wall. Another major producer, Anglo American (NGLB.BE) sold two major mines in Australia.

Coal is clearly an energy source whose time has clearly come and gone. So, will the price of coal. The next recession, which may only be a year off, could well drive the entire industry into bankruptcy.