Have Calm Waters Returned for Shipping Stocks?

The shipping stocks have had an OK year so far in 2015. The big question remains: ?Is it real,? and ?Is it sustainable??

This sector has been down for so long that most investors left it for dead ages ago. All that was missing was the tolling of the Lutine Bell at the Lloyds of London insurance exchange to mark news of a sunken ship.

Lured by the heroin of artificially cheap financing during the 2000?s, the industry massively expanded capacity, believing that international trade would continue to grow at double digit rates forever.

It didn?t.

Sound familiar? Think of it as ?subprime at sea.?

Then the 2008 financial crisis hit, and demand evaporated. International trade, the main driver of freight rates, collapsed. Rates dropped as much as 90%, and share prices even more.

In those dark days, readers delighted in sending me maps of laid up ships with forlorn crews in Singapore harbor, which at the worst, numbered in the hundreds. You could almost walk to neighboring Malaysia and not get your ankles wet.

For most industries, the economy bottomed shortly thereafter and began a long, slow recovery. Not so for shipping.

China, the world?s largest buyer of bulk commodities, saw its economy peak in 2010, with annualized GDP growth halving since then from 13.5% to 7.0%.

This unleashed a second, even more vicious crisis for the shipping industry. With massive capital requirements, order times for new ships lasting three years, and hefty cancellation fees common, recovery delays are not what you want to hear about.

Ships ordered at the peak of the financing bubble suddenly started showing up in large numbers. So, the industry remained with excess capacity of 20%, especially in the dry bulk, container and crude oil tanker segments.

This was happening in the face of steadily rising fuel prices, thanks to events in Iran, Egypt, Libya, Syria, the Ukraine and now Iraq. The China slowdown also caused scrap metal rates to plummet, so downsizing shippers were paid less for junking their older, smaller, less fuel efficient bottoms.

American energy independence, thanks to the ?fracking? boom, means fewer ships are needed to carry oil from a tempestuous Middle East.

It has been the perfect storm of perfect storms. All but seven of the 30 largest shipping companies bled money in 2012, lots of it. Cumulative industry losses amounted to a mind numbing $7 billion over the previous four years. Companies continued to hemorrhage cash, and shareholders suffered.

And then a funny thing happened. The Chinese economic data slowly started to get better. Any price tied to business activity in the Middle Kingdom started marching upward in unison, including those for iron ore (BHP), (RIO), the Australian dollar (FXA), and Chinese and Australian stocks (FXI), (EWA).

This improvement, no matter how uncertain it may be, was not lost on the shipping industry. Capesize charter rates surged from $5,000 to $16,500, while Panamax rates are expected to fly from $8,000 to $9,500 by January.

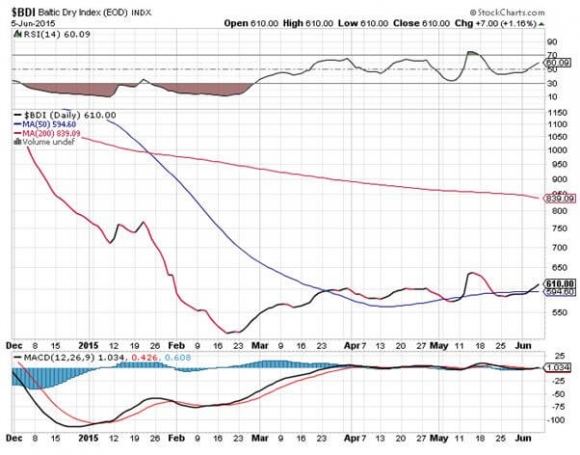

Shipping stocks, the most highly leveraged of asset classes, skyrocketed. This enabled the Baltic Dry Index ($BDI), a measure of the cost of chartering bulk carriers for coal, iron ore, wheat, and other dry commodities, to steadily improve.

Apparently, it is off to the races once again.

I am not normally a person who buys a stock after it has just doubled, unless Costco is running a special on Jack Daniels. But if a share has fallen 99%, a double takes it down to only 98%, leaving it still absurdly cheap.

Shipping stocks fell so far, they were well below long dated option value. That means the market thought all of these guys were going under, which was never going to happen.

This is certainly the case with Dry Ships (DRYS), your poster boy for the Greek shipping industry. Adjusted for splits, the shares cratered from $120 to $0.60. It has just clawed its way up to $0.72. The company?s fleet consists of 38 dry bulk carriers, 10 tankers, and has orders for another four ships.

It has completed a major refinancing that takes the firm out of the fire and puts it back into the frying pan. This should buy (DRYS) some time, while other competitors, like Genco Shipping and Trading (GNK) are expected to go under, removing unwanted overcapacity from the market.

It also wisely diversified into offshore oil drilling right at the bottom of the market, picking up a 59% stake in Ocean Rig (ORIG) and its two semisubmersible rigs.

(DRYS) is not your typical ?widows and orphans? type investment. The web is chock full of allegations of insider trading, nepotism, and self-dealing by senior management.

It is domiciled in the Marshall Islands, so don?t expect much transparency. Pass the smell test, it does not. After all, it is a Greek shipping company.

If (DRYS) scares you, and it should, there are safer ways to play the rebound. The Guggenheim Shipping ETF (SEA) offers a broad mix of industry exposure with lower volatility. It is up a healthy 17% so far this year.

Even in the best-case scenario, shipping will never return to the heady growth rates of the naughts. China is highly unlikely to ever return to the breakneck growth rates of yore. The law of large numbers is kicking in with a vengeance.

It is modernizing its economic strategy, from one led by a low value added commodity exports, to a more domestically driven, services oriented approach. The bad news for shippers: The new model uses fewer bulk commodities, and therefore the ships to carry them.

However, if the China recovery is real, even a modest one, then the shipping industry offers one of the best multiple baggers that I can think of.

Just make sure you don?t get seasick from the volatility.