Janet Yellen?s Dirty Little Secret

Given that this is a presidential election year, much has been made of the national debt.

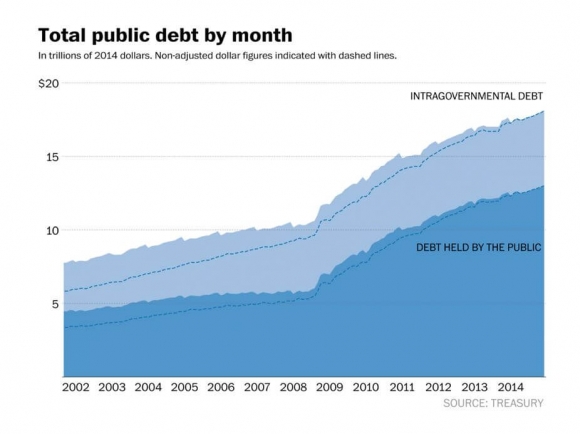

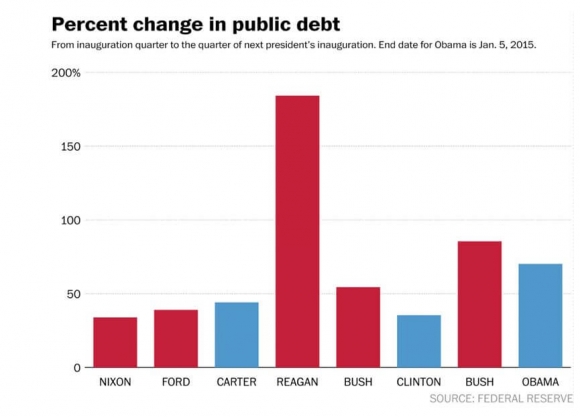

Since President Obama came into office on January 20, 2009, it has skyrocketed from $10.2 to just over $19 trillion, a gut punching increase of 86.2%.

Has Obama just bankrupted the United States? Is default just around the corner, as aspirant Donald Trump claims?

Are we all going to hell in a hand basket?

I hardly think so.

And I can say so with great confidence, thanks to Federal Reserve Chairwoman, Janet Yellen?s, dirty little secret.

I have to tell you that it is quite handy knowing the Fed chairwoman?s dirty little secrets. It has enabled me to become bullish on the Treasury bond market when the rest of my hedge fund brethren were bearish beyond belief.

And my readers have profited as well, moving in and out of bullish United States Treasury Bond Fund (TLT) call spreads more than once.

My former Berkeley Economics professor?s dirty little secret isn?t actually her secret.

She inherited it from her predecessor, Ben Bernanke. And it was from Ben (no longer ?Mr. Chairman?) that I learned one of the closest held mysteries among central bankers today.

Ben confided in me his analysis over a fine Italian dinner at Perbacco's on San Francisco?s California Street late last year (click here for ?Dinner With Ben Bernanke?).

While it is true that the national debt has increased by some $9 trillion over the past 7 1/2 years, there is less there than meets the eye. Much less.

That includes the $4 trillion purchased by the Federal Reserve as part of its aggressive five-year monetary policy known as ?quantitative easing?.

It also includes another $1 trillion of Treasury holdings by dozens of other federal agencies, such as Fannie Mae, Freddie Mac and Sallie Mae.

So the net federal debt actually issued during Obama?s two terms is not $9 trillion, but $4 trillion. That?s a big difference.

These numbers would make Obama one of the most fiscally conservative presidents in US history (see tables below). And he pulled off this neat trick ?despite US tax revenues utterly collapsing in the aftermath of the Great Recession.

What the Treasury has in effect done is taken one dollar out of one pocket and put it in the other, 5 trillion times.

There has been no change in the nation?s indebtedness or net worth as a result of these transactions.

In fact, these bonds were never even really issued. They only exist on a spreadsheet, on a server, on a mainframe, somewhere at 1500 Pennsylvania Avenue, NW, Washington DC.

And here is the real shocker.

The Treasury can cancel this debt at any time.

They can just decide to use one set of figures on the plus side of the balance sheet to offset an equal amount on the negative side, and poof, the debt is gone forever, and the national debt is only $14 trillion.

It wouldn?t even require an act of congress. It could simply be carried out through a presidential order.

That would give America one of the lowest debt to GDP ratios in the industrialized world.

I actually recommended that the White House use this ploy to get around the last debt ceiling crisis.

What was fascinating to me is that they instead took the political decision to give the Republicans in the House enough rope to hang themselves by threatening to put the country into default.

It worked.

If a future president Hillary is put into a similar dilemma with a future recalcitrant Republican House, she will revisit this option.

Trust me.

All of this sounds nice in theory. But how would markets respond if this were the true state of affairs in the debt markets?

A non-stop 30-year bull market in all debt instruments to continuous new all time highs would ensue. Ten year Treasury bonds would plunge to 1.34% and threaten lower still.

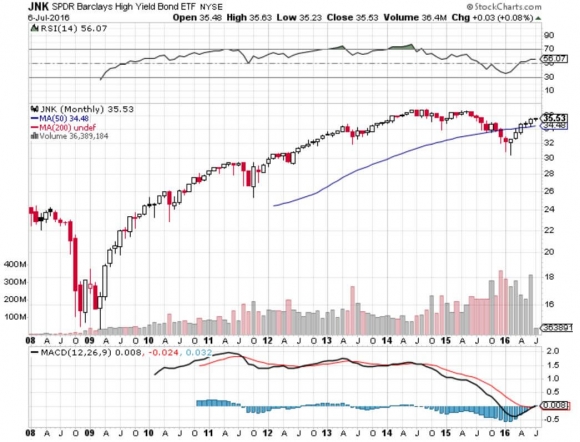

The buying panic for debt instruments by a yield-starved world would spill over into lesser quality credits, like junk bonds (HYG), municipal bonds (MUB), and corporates (LQD).

Prices for marginal debt securities in emerging markets (ELD) would boom. Even the pariahs of the credit markets, master limited partnerships (AMLP) would see yields collapse by a third in only six months.

Am I ringing any bells here people? Do these sound like debt markets you know and love?

A half-century of trading has taught me to never argue with Mr. Market. He is always right.

The current Fed strategy is to not sell any bonds at all, but let the balance naturally run down through maturity. That is how the Fed balance sheet has shrunk from $4 trillion to $3.5 trillion since QE ended nearly two years ago.

By keeping it's bonds, the Fed has a valuable tool to employ if it ever senses that real inflation is about to make a comeback, without having to raise the overnight deposit rate. It simply can raise bond market rates by selling some of its still considerable holdings.

?FED SELLS BOND HOARD.?

How do you think risk markets would take that headline? Not well, not well at all.

However, as deflation is now accelerating, that is a highly unlikely prospect for the foreseeable future.

There are other reasons to keep the $5 trillion in phantom Treasury bonds around.

It assures that the secondary market maintains the breadth and depth to accommodate future large scale borrowing demanded by another financial crisis, Great Recession or war.

Yes, believe it or not, governments think like this.

I remember that these were the issues that were discussed the last time closing the bond market was considered. That was at the end of the Clinton administration in 1999, when paying off the entire national debt was only a few years off.

But close down the bond market, and fire the few hundred thousand people who work there, and it could take decades to restart.

This is what Japan learned in the 1960?s. It took the Japanese nearly a half-century to build the bond infrastructure needed to accommodate their massive borrowings of today.

The Chinese are learning the same thing as they strive to construct modern debt markets from whole cloth. It is not an overnight job.

One of the most common questions I get from foreign governments, institutional investors, and wealthy individuals in my international travels is ?What will come of America?s debt problem??

The answer is easy. It will all go to debt heaven. It will disappear.

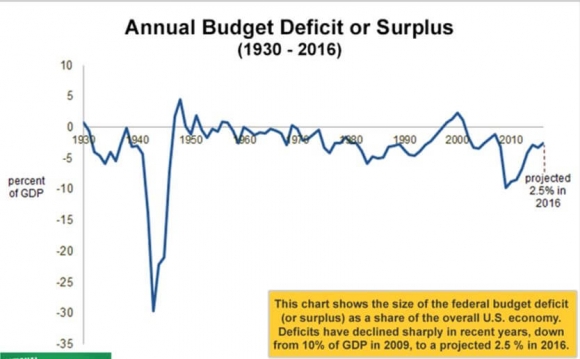

US government finances are now improving at a pretty dramatic pace (see more charts and tables below).

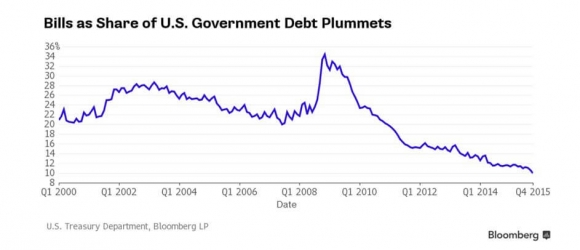

The budget deficit has shrunk by 75% over the past seven years. Debt to GDP is plunging. New government bond issuance is grinding to a near halt.

A severe government bond shortage has emerged.

Under current law, the US should see a balanced budget within three years.

Then a massive demographic tailwind kicks in during the 2020?s, as 85 million Millennials grow up to become big time taxpayers.

In the meantime, the last of the benefit claiming baby boomers finally die off, eliminating an enormous fiscal drag.

?Depends?? and ?Ensure? prices will crater.

The national debt should disappear by 2030, or 2035 at the latest. The same is true for the Social Security deficit. That?s when we next have to consider firing the entire bond market once more.

That is what happened to the gargantuan debt run up by the Great Depression, the Civil War, and the Revolutionary War.

Government debt always goes to debt Heaven, either through repayment during period of demographic expansion and economic strength, or via diminution of purchasing power caused by deflation.

That?s why we have governments, to pull forward economic growth during the soft periods in order to even out economic growth and job creation over the very long term to accommodate population growth.

The French were the first to figure all this out in the 17th century. They were not the last.

That is, unless another George W. Bush comes along, and debts explode and revenues vaporize.

That would create another half century of employment opportunities for bond traders, yet again.

History doesn?t repeat itself, but it certainly rhymes.