(NEW AUSSIE TECHNOLOGY WILL BE USED DURING DISASTERS)

September 20, 2024

Hello everyone

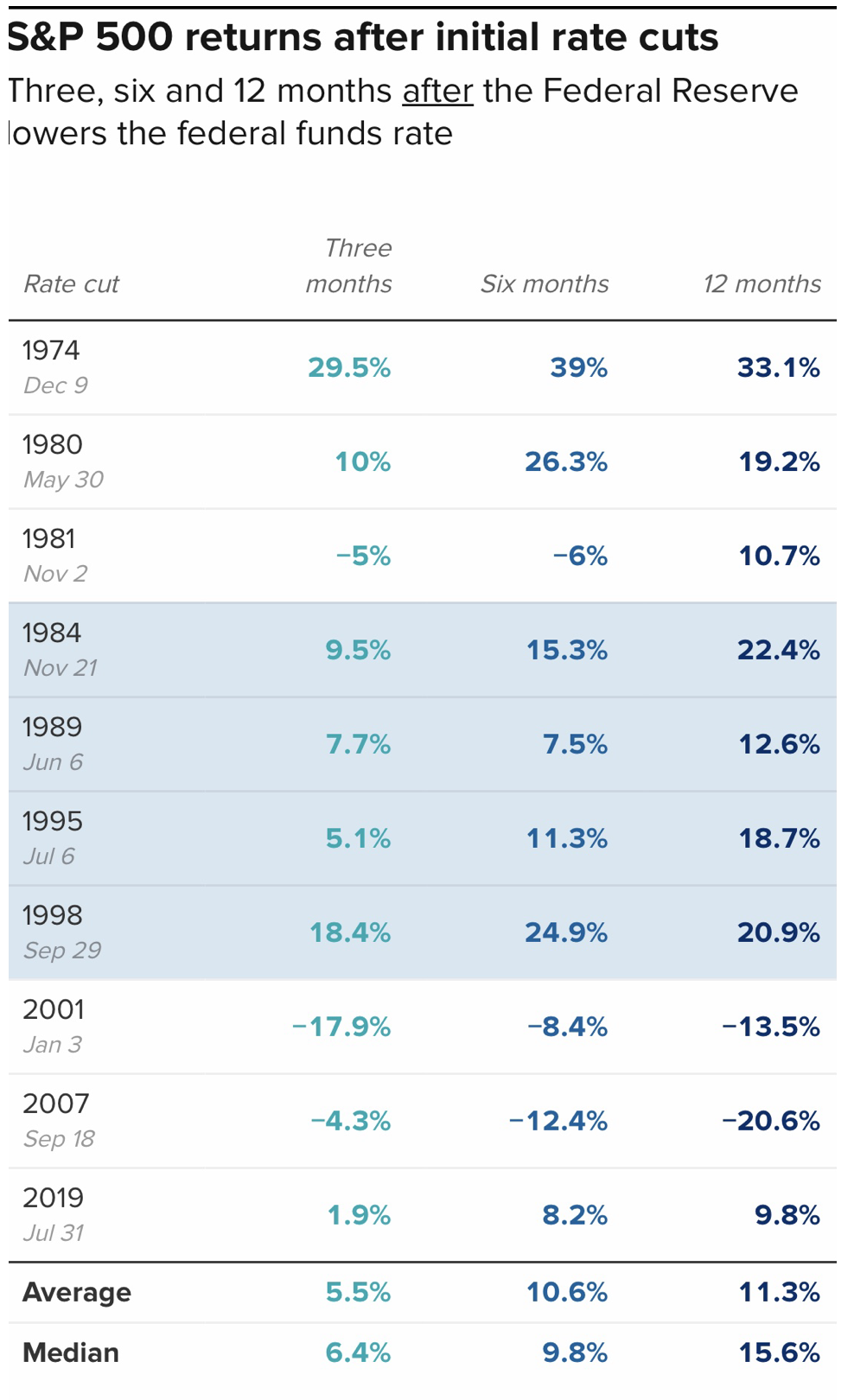

Well, the rate cut show is over.

The number was 0.5 basis points.

Some will think the Fed was late in its policy reaction.

The true ramifications of such a move probably won’t be seen until next year.

Then, a whole new pattern of events may show up.

But let’s concentrate on the near term first.

The market woke up Thursday morning with a spring in its step and decided the 0.5% number was a good policy move.Nearly every sector was on fire.

Surely smoother, more gradual rate cuts – starting earlier - would have been a better policy move than an initial big move with the probability of more to come this year.But what do I know.I’m not an economist.

Still, analysts are divided over the medium- and long-term view of where markets are going.

Some see storm clouds developing on the horizon, while others see clear air ahead with occasional turbulence.

We have more labour reports ahead and the U.S. election, which could well create some chop in the markets.

AUSTRALIAN CORNER

Technology to the rescue during a disaster

New technology to help keep Aussies safe and connected during emergency situations will be rolled out in disaster-ravaged towns from this summer.

The NSW government will have giant orange portable cell towers, called Cells on Wheels (COWs), ready to deploy to bushfire and flood-affected areas, which will allow residents and emergency service workers to stay in touch.

They will provide telecommunications backup when existing infrastructure is damaged or destroyed in natural disasters.

Communities will be able to connect to the COWs via Wi-Fi, enabling them to make data calls or to connect to the internet.

Additionally, the COWs are able to connect to each other to expand coverage.

As part of a $2 million contract. Communications company Pivotel is due to deliver four COWs, which will be available to be sent across the state in a matter of hours.

QI CORNER

SOMETHING TO THINK ABOUT

RECORDING OF JACQUIE’S POST AUGUST ZOOM MONTHLY MEETING

(THE SCIENCE OF AGEING BACKWARDS MAY BE IN OUR POCKETS WITHIN THE NEXT TEN YEARS)

September 18, 2024

Hello everyone.

Today will be a refreshing change of pace and content, as I think we all have endured a lot of noise about this week’s events.

So, let’s jump right in.

Ageing.Or should I say the study and research into ageing backwards is gaining steam?It’s no longer the stuff of science fiction.Affordable treatments that could slow, stop or even reverse your ageing are, thanks to new breakthroughs, less than a decade away.Without even realizing it, you may even be taking some of these pills already.

The biology of ageing essentially causes diseases like cancer, cardiovascular disease, and dementia.For example, while having high blood pressure roughly doubles your chance of a heart attack, being aged 80 rather than 40 multiplies that risk by 10.That means understanding the biology behind these enormous risk increases could lead to the greatest revolution in medicine since the discovery of antibiotics.It could transform not just the treatment but the prevention of disease in the first place.

The pay-off, if we can identify and treat these underlying causes of ageing, is enormous.If we could make people in middle age a bit biologically younger with drugs that address the ageing process, we could improve everything from heart health to wrinkles and delay the onset of cancer, dementia, and frailty, all at the same time.

Andrew Steele, in his text, Ageless: The New Science of Getting Older Without Getting Old, reveals how scientists have identified several so-called ‘hallmarks’ of the ageing process – underlying biological and biochemical processes…

So, what are these biological hallmarks, and what might treatments to slow or stop their currently relentless march look like?

According to Steele, the most promising treatments are:

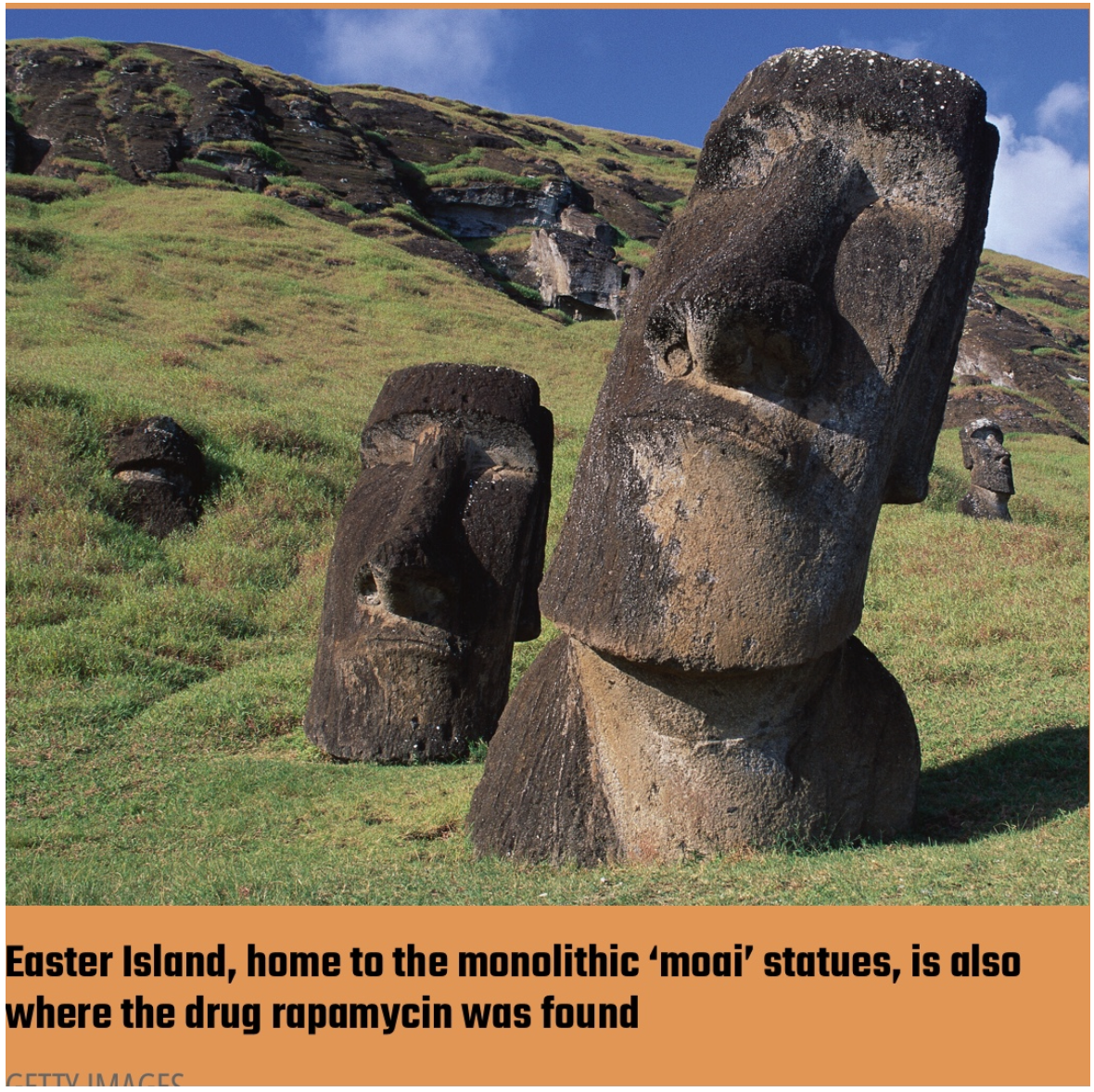

1/ A Miracle Drug from Easter Island

Easter Island, known for its giant stone heads, is also the origin of one of our most promising drugs to improve longevity: rapamycin.

Discovered in a soil sample returned by a Canadian expedition in the 1960s, it was named after the Polynesian name for Easter Island, Rap Nui.The molecule, produced by a species of bacterium, is a pharmaceutical Swiss army knife with applications ranging from treating cancer to suppressing transplant patients’ immune systems to help prevent organ rejection.And we could soon add ‘slowing down the ageing process’ to that list.

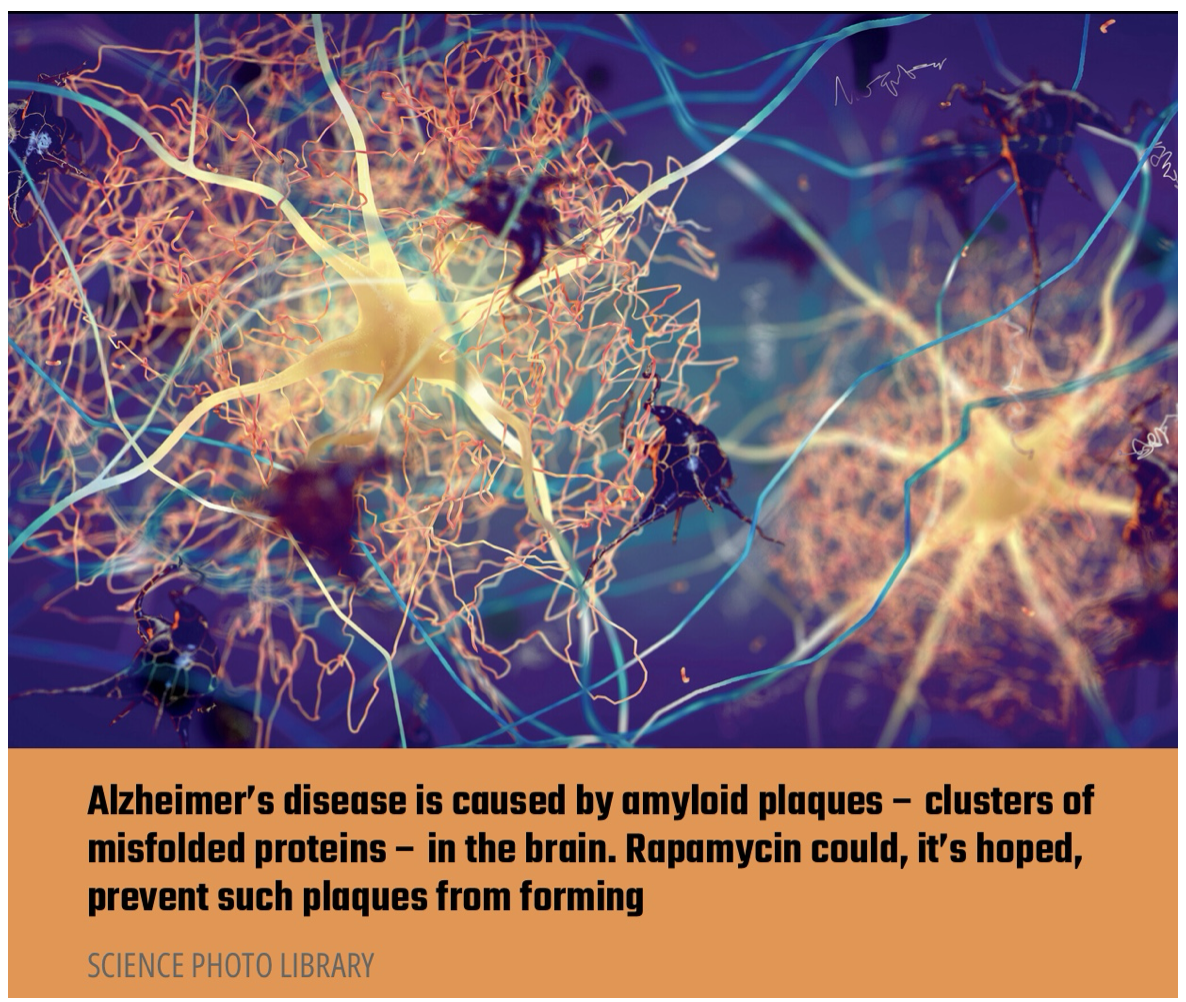

It all comes down to the hallmarks of ageing: the accumulation of dysfunctional proteins as we get older.

‘Autophagy’ – which literally means ‘self-eating’ – allows our cells to recycle malformed molecules and turn them into fresh, functional proteins.Rapamycin can increase our cells’ ability to engage in this anti-ageing spring-cleaning.

Scientists believe that we could improve everything from heart health to wrinkles and delay the onset of cancer, dementia, and frailty.

2/ Drugs in your Medicine Cabinet

Diabetes drugs known as SGLT -2 inhibitors – canagliflozin, dapagliflozin, or empagliflozin – might be giving you health and lifespan benefits beyond helping with your blood sugar. These drugs have been shown to improve wider health in patients that take them, and canagliflozin extended lifespan by 14% in male mice.

Other drugs include Metformin and Acarbose – diabetes drugs, and bisphosphonate drugs- usually used to reduce bone loss, weight-loss treatments like semaglutide, commonly known under brand names like Wegovy or Ozempic.

3/ Bottling Up a Baby’s Biology

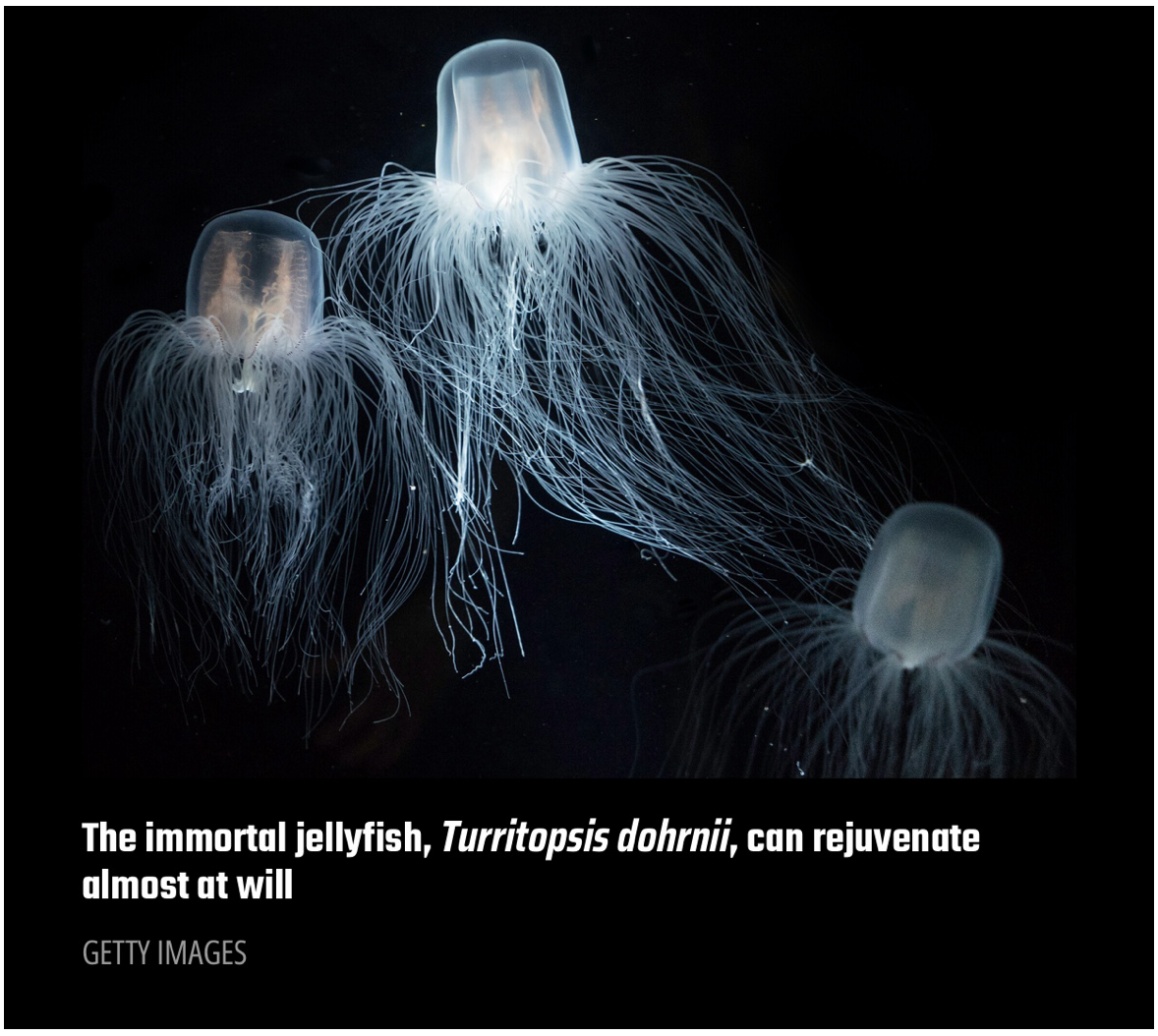

An immortal jellyfish (Turritopsis dohrnii) can, in times of stress, simply revert their biology to the junior ‘polyp’ stage and then grow up all over again, seemingly as many times as they like.In other words, ageing backward isn’t against the laws of biology.But is it possible in humans?

Steele argues that ageing biology, as a field, needs more funding to begin human trials for the promising interventions.If it gets it, Steele says there’s no reason why some of these real anti-ageing medicines couldn’t be approved within a decade, allowing us all to stay healthy for longer.

AUSTRALIAN CORNER

That’s Wednesday evening, September 18 (Australian time) Hope you enjoyed it.

QI CORNER

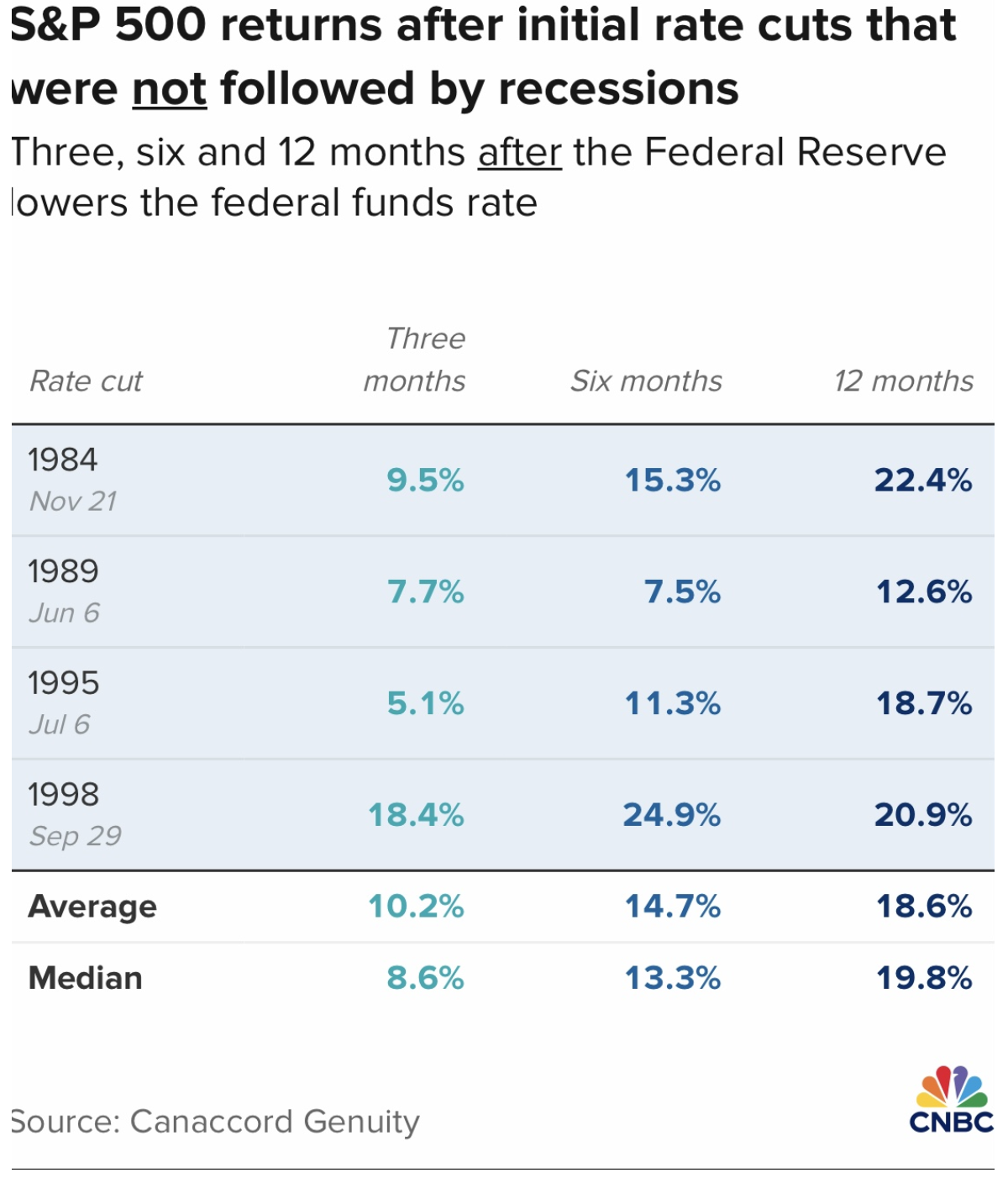

Shaded areas indicate cuts not followed by recessions.

(THE FED RATE CUT SHOW IS HERE – BUT WHAT’S THE NUMBER?)

September 16, 2024

Hello everyone.

Welcome to the biggest show in town this week.It has been hugely hyped, so expectations are high for a spellbinding event that will keep us hanging on every utterance the Fed delivers. Body language interpreters will be busy scribbling notes about Powell’s poker face and hand and arm movements, while other analysts will be dissecting his speech and looking for what was not said, which can also speak volumes.

And the rate cut will be…?

It’s uncertain, but what you can probably bank on is that there will be several cuts within the next year.

If the Fed cuts by 50 bps, markets may interpret that the Fed was behind the curve and made a mistake by not cutting in July and is acting pre-emptively against recession risks – which would be a shift from their typical stance of data dependency.Such a move could see a sell-off in equity markets take place.In other words, a big cut may indicate that the Fed has data that is worse than what we are seeing.

The uncertainty appears to be setting stocks up for an initial sell-off regardless of what the Fed does. We all know that markets hate uncertainty.

The dollar is likely to strengthen on a smaller cut and weaken on a larger one.

Two other major central banks also meet this week.The Bank of England is expected to hold rates at 5%, diverging from the ECB’s recent cut.The Bank of Japan is also likely to hold rates, but the meeting is still worth monitoring given their past surprise moves.

So, sit back and grab a front-row seat.Just make sure you scoop up opportunities’ volatility reveals.

WEEK AHEAD CALENDAR

Monday, Sept. 16

8:30 a.m. Empire State Index (September)

5: 00 a.m. Euro Area Wage Growth

Previous: 5.3%

Forecast: 3.2%

Tuesday, Sept 17

8:30 a.m. US Retail Sales (August)

Previous: 1.0%

Forecast: 0.2%

9:15 a.m. Capacity Utilization (August)

9:15 a.m. Industrial Production (August)

9:15 a.m. Manufacturing Production (August)

10 a.m. Business Inventories (July)

10:00 a.m. NAHB Housing Market Index (September)

Wednesday, Sept 18

8:30 a.m. Building Permits preliminary (August)

2:00 p.m. US Rate Decision

Previous: 5.5%

Forecast: 5.25%

2:00 p.m. Fed Funds Target Upper Bound

Earnings:General Mills

Thursday, Sept 19

8:30 a.m. Current Account (Q2)

8:30 a.m. Continuing Jobless Claims (09/07)

8:30 a.m. Initial Claims (09/14)

8:30 a.m. Philadelphia Fed Index (September)

10:00 a.m. Existing Home Sales (August)

10:00 a.m. Leading Indicators (August)

7:00 a.m. UK Rate Decision

Previous: 5.0%

Forecast: 5.0%

Earnings:Lennar, FedEx, Darden Restaurants.

Friday, Sept. 20

12:00 a.m. Japan Rate Decision

Previous: 0.25%

Forecast: 0.25%

MARKET UPDATE

S&P500

Looking at the market through an Elliott Wave lens, we can interpret that the market has recently completed a corrective Wave ii of 5/ on its September 6 low of 5,403 to enable the resumption of Uptrend onto new highs for the year, with potential for advance toward 6220/6256 over coming weeks.A strong break above 5,652/5,670 will confirm this interpretation.

GOLD

Uptrend in progress.Support = $2,570/$2,530.Next upside target is around $2,640.

BITCOIN

Upside potential.Bitcoin has been undergoing a complex correction since reaching $73,794 in mid-March. The low reached on August 5th at $49,577 may have completed this correction.Through an Elliott Wave lens, it is possible to understand that Bitcoin may now have commenced a Wave 3/ advance toward a target of around $73,826.

Initial target is around $65,000 while holding support at around the mid$58s.

September is living up to its reputation with whiplash type movements, and a double top on the charts.

September 18 interest rate cut is an almost certainty, but how much of it is already priced into the market?

The next sell-off is the one you buy into for a post-election rally.

US dollar begins to weaken and could do so for years.

Tech stocks will rally again after a much-needed correction.

Energy is in the doldrums because of recession fears.

Buy stocks & bonds on dips in ALL sectors.

THE GLOBAL ECONOMY – WEAKENING

The Fed waited too long to cut interest rates as the economy is now undeniably weakening.

Nonfarm payroll report fades at 142,000

Headlines Unemployment rate stays at 4.2%

Previous two months saw substantial downward revisions.

ADP Employment Change Report hits 31/2 year low, up only 99,000 in August.

Personal Consumption Expenditures price index rises a modest 0.2% in July.

UD GDP Reaccelerates to 3.0% growth in Q2, up from the previous estimate of 2.8%

STOCKS – NOSEDIVE

John says if the Fed doesn’t cut by 0.50% in September the stock market will crash

Look for two bottoms on September 18 and October 20.

NVDA dives on fabulous earnings, one of the greatest “Buy the rumour, sell the news” moves of all time.

Broadcom beats and Stock tanks, driven by strong sales of its AI products and VMware software.

Biden blocks Nippon Steel takeover of US Steel, no doubt to save the jobs these deals usually destroy.

Volatility Index soars 50% in a Day, from $14 to $22.

ISM Manufacturing PMI comes in weak, with just 47.2% of purchasing managers reporting expansion in August.

Eli Lily is now a trillion-dollar stock, the first biotech to do so.

Suggestions -

Look to buy JPMorgan as it gets closer to the 200MA.Netflix (NFLX) buy.

UPS- buy/ good LEAPS trade, UNP – China recovery play. Caterpillar (CAT) falling interest rate play – long term hold.

(ROM) Technology ETF – watch for good entry.

BONDS – NEW HIGHS

The Yield curve has de-inverted, meaning that short term interest rates have fallen below long-term ones.

Two-year interest rates at 3.72% are now 0.03% lower than ten-year ones at 3.75%.

It’s a clear signal to the Fed that rates must be cut soon.

Yield Chasers Post Record Demand for Junk Bonds.

That’s helped make 2024 the busiest year for issuance of new corporate high-yield bonds, with $357 billion sold so far.

Market prices in 50-point basis cut for September, holding on to massive rally.

A cut of only 25 basis points on September 18 could give us a $5 selloff.

The September 6 Nonfarm Payroll Report and Unemployment rate will be crucial.

Buy (TLT), (JNK), (NLY), (SLRN) and REITS on dips.

Also 90-day T-bills at 4.97%

FOREIGN CURRENCIES – DOLLAR IS TRASH

Dollar hits seven Month Low, as US interest rates loom.John says it could be a decade long move.

The Yen Carry Trade is Back, with hedge funds piling back into positions they jumped from only two weeks ago.

It’s a matter of math, John says, now that the Bank of Japan has given up on raising interest rates anytime soon.

What this means is more leverage, risk and volatility for global financial markets.John loves the volatility.

The prospect of falling interest rates means that the greenback is out of favour.

Buy (FXA), (FXE), (FXB), (FXC)

ENERGY & COMMODITIES – CRUDE AWAKENING $60 in play

Crude Oil now down on the Year, after a sharp weekend sell-off.

Blame can be spread amongst a weak China, lost OPEC discipline, and over production.

The bearish Goldman Sachs commodities report was also a factor.

US Oil Production hits all-time high.In August 2024, U.S. oil production hit a record 13.4 million barrels per day according to the U.S. Energy Information Administration.

Big Oil has become more productive as horizontal drilling and hydraulic fracturing, which is also known as fracking, have seen technological breakthroughs.

The fossil fuel industry benefits from tax incentives, such as the intangible drilling costs tax credit, that are built into the tax code.The intangible drilling costs tax break is expected to benefit oil and gas companies by $1.7 billion in 2025 and $9.7 billion through 2034.

PRECIOUS METALS – NEW HIGHS

Goldman goes Big on Gold

Central banks in emerging market countries are continuing to buy gold – with purchases tripling since the middle of 2022 amid fears of U.S. financial sanctions and a mountain of sovereign debt.

Goldman is taking a more selective approach to commodity investing, pushing gold but avoiding crude oil and copper prices as China continues to drag.

Silver dives on economic slowdown, enters a sideways range.

A global monetary easing is at hand.

Buy precious metals on the dips because rates are now falling decisively.

Buy (GLD), (SLV), (AGQ), and (WPM) on dips.

REAL ESTATE – READY FOR TAKEOFF

Pending Home Sales drop 5% and 8.5% YOY, on a signed contract basis.

Many buyers are waiting until after the presidential election to make a move

Pending home sales fell in all four regions last month.

The positive impact of job growth and higher inventory could not overcome affordability challenges and some degree of wait-and-see related to the upcoming U.S. presidential election.

Manhattan Commercial Real Estate has bottomed, and bottom fishers are swooping in.Can San Francisco be far behind?

Mortgage Rates Hit New 2024 Low.The average for a 30-year foxed loan was 6.23%, down from 7.5% high.

Sales of new U.S. single-family homes rocket by 10.6%.

(ROBLOX (RBLX) DELIVERS REAL MONEY TO DEVELOPERS IN A NEW INITIATIVE)

September 11, 2024

Hello everyone.

Palantir Technologies & Dell Technologies join the S&P500.

In a couple of weeks, Palantir Technologies Inc. and Dell Technologies Inc. are set to join the S&P500 index.Shares of Palantir and Dell rallied in the extended session Friday after the news, gaining nearly 8% and 7% respectively. This movement is part of a scheduled index rebalancing, which is to take place on September 23.Also joining the S&P500 is the insurance company Erie Indemnity Co. (ERIE)

The three companies will replace American Airlines Group Inc. (AAL), Etsy Inc. ETSY and Bio-Rad Laboratories Inc. BIO in the S&P500.

American Airlines and Bio-Rad will migrate to the S&P MidCap 400 (MID) while Etsy will move to the S&P Small Cap 600 (SML)

Real Money earned by developers on Roblox in a new initiative.

Roblox, a gaming platform that generates billions of dollars a year in the virtual world is getting real.

Last Friday, the company stated that some game developers on the platform will be able to charge users real money rather than relying on payments through Roblox’s digital currency called Robux.The change applies to those games that cost money to play.

Game creators can now more easily sell to users without dealing with an intermediary virtual currency.This conversion to real money is part of the company’s plants to facilitate 10% of all global gaming content sales through the Roblox platform and reach 300 million daily active users.

Chief product officer, Manuel Bronstein, states that the goal is to increase the appeal of the platform to existing developers, who want options to create and make money from their games.

For a game that costs $50, the creator will pocket 70% of the earnings.Those that cost $30 and $10 will lead to payouts of 60% and 50%, respectively.Roblox users will be able to pay with their local currencies later this year from their computers, and the company plans to expand payments to other devices in the future.

The company hopes the pricing plan incentivises developers and small gaming studios who want to do something on a grander scale on the platform and earn bigger payouts.

Roblox derives the bulk of its revenue from sales of Robux, which people typically use to buy virtual goods.Roblox takes a 30% cut from those sales, with the developer getting the rest.

In August, Roblox’s second quarter sales jumped 31% year-over-year to $893.5 million, while its net loss narrowed to $207.2 million from $282.8 million during the previous year.

Roblox will also partner with Shopify, which will see developers able to sell some physical merchandise to U.S. users over age 13.Shopify said it plans for a “larger launch” early next year.

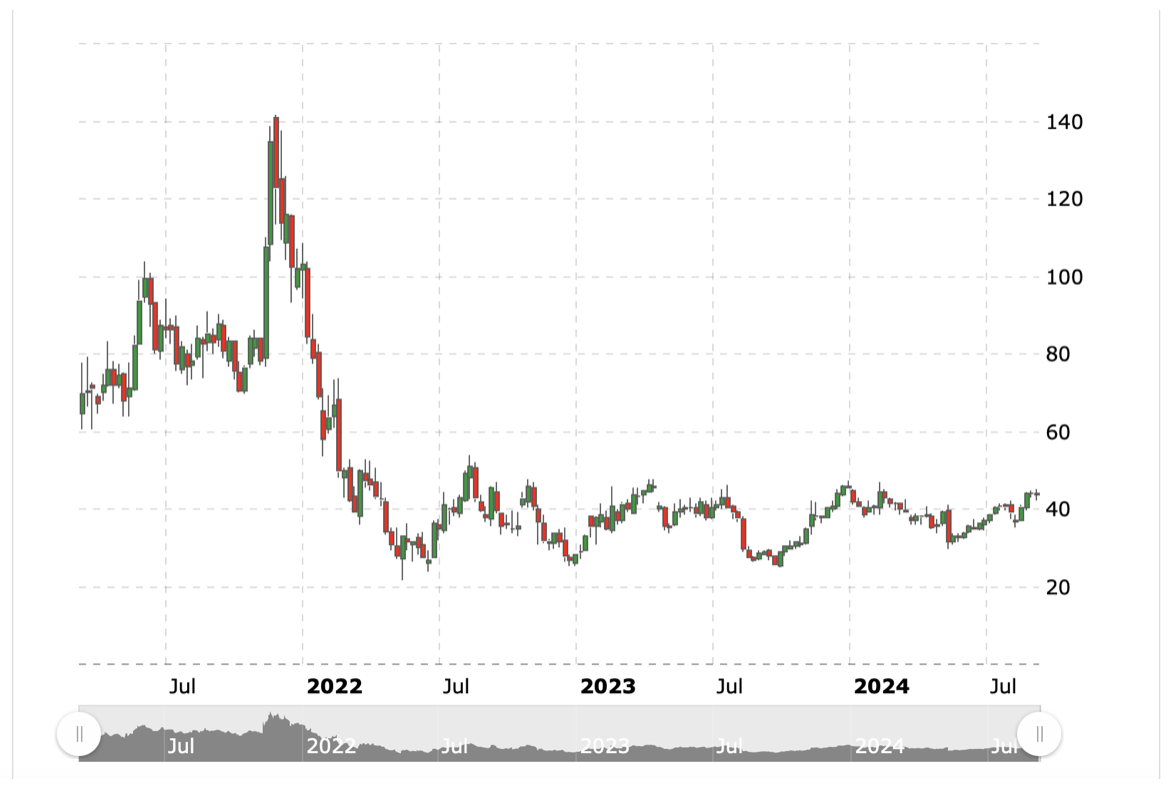

Roblox shares closed slightly lower last Friday at $43.64.They are now down almost 5% for the year, while the Nasdaq is up 11% in 2024.

The stock has dropped close to 40% since its first day of trading in 2021, when Roblox’s business was booming as kids flocked to the app during the pandemic.

ROBLOX CHART

Note: The Roblox article is an item of interest and not a recommendation to buy at this time.

Last Friday, the highly anticipated US jobs data came in slightly lower than expected, with only 142,000 jobs added in August.The US$ shrugged its shoulders at the number but was still weaker on the week.

This week brings the euro into focus with an interest rate decision from the ECB on Thursday.Rates are expected to be lowered by 25bps.US CPI data arrives on Wednesday, with inflation expected to tick lower towards the Fed’s 2% target.

This week will also bring the first presidential debate between Vice President Kamala Harris and former President Donald Trump, an event traders will closely watch as the candidates outline their economic policies.

MARKET UPDATE

S&P500

Corrective sell-off in progress.The question on everybody’s lips: Is this a new bear market or a corrective move?At the moment I view the action in the market as a correction, and support around 5,100 should hold.A sustained break below the aforementioned level would question my thesis and risk a move toward the mid 4,000’s.

GOLD

Gold uptrend persists.Resistance = $2,530.Once this level is cleared the uptrend can extend onto the late $2,500s.

As a caution, any sustained break below $2,470, risks a move to around $$2,400.

BITCOIN

Complex Correction in progress.Resistance = $56,250/$58,500.With downside pressure dominant at the moment, we could see the $50,000 level tested and even test the mid $44k.

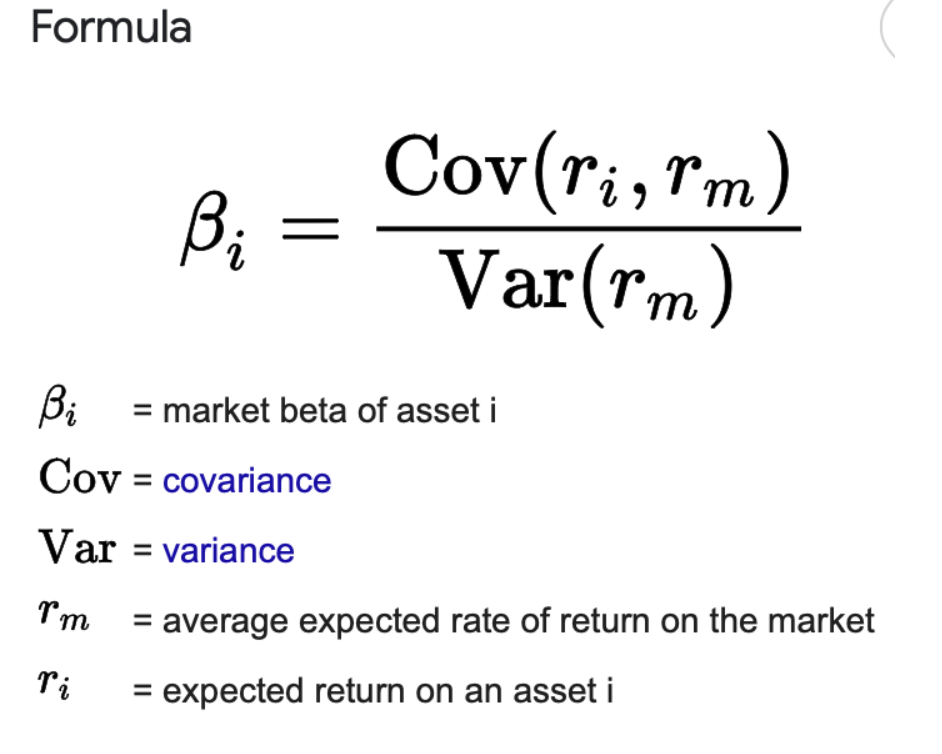

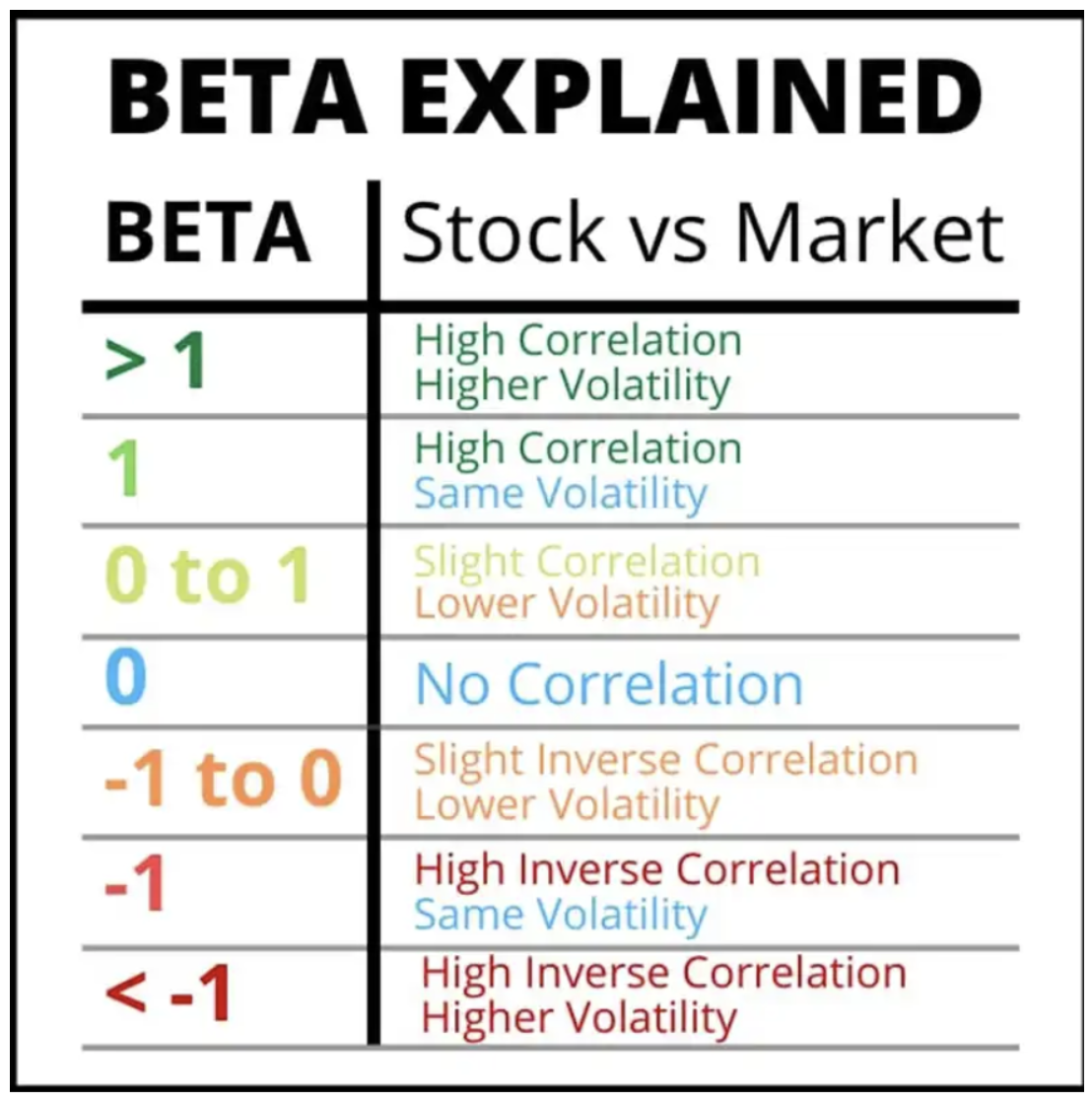

WHAT IS…?

Beta is a statistical measure of a security’s risk or volatility as compared with the market as a whole.

The market has a Beta of 1.0, and individual stocks are ranked according to how much they deviate from the macro market.If stock (XXX) has a beta of 1.5, then we would expect stock (XXX) to move 50% more than the market.So, if the S&P500 moves up/down 1.0%, we would expect (XXX) to move up/down 1.5%.

A higher beta implies greater risk with the potential for higher returns, whereas a lower beta implies lower risk, but also the potential for lower returns.

How do we calculate Beta?

AUSTRALIAN CORNER

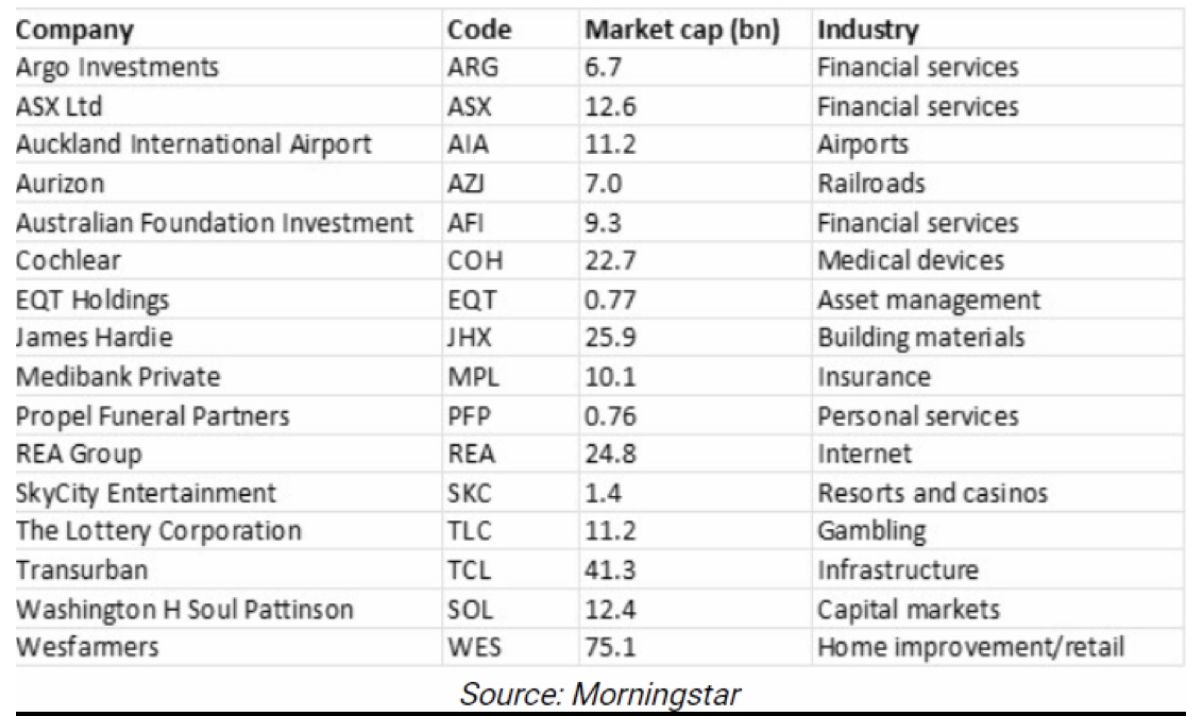

Morningstar says the following companies are stocks that investors could hold for life.

Note:this list does not cater to those who want stocks for dividend income and doesn’t consider valuation.In other words, investors need to look at different stocks for income and should wait for a retracement before scaling into any of the stocks listed here.

The filter that was used included:

Part of the ASX 300 (well established firms with some history of success, which excludes most small caps).

Long runway of growth opportunities (leaning toward companies that have global operations, and/or large markets to operate in).

Sound balance sheet (Not a big reliance on too much debt to generate returns).

Don’t rely on exceptional managers to succeed. (The business needs to stand on its merits).

Unlikely to be disrupted (you are betting on things that won’t change).

James Hardie (ASX: JHX)

Since it pioneered the development of fiber-cement technology in the 1980s, it has dominated the fiber-cement siding category for houses in the US and Australia.It has a long runway of growth and an economic moat based on brand and scale that should keep competitors at bay, resulting in above-average returns for decades to come.

REA Group (ASX: REA)

Owns realestate.com.au – the premier online listing platform for Australian residential real estate.Even during the downturn in listings in 2022, it was able to substantially lift pricing – which demonstrated its immense pricing power and moat.

(INVESTORS ARE PAYING ATTENTION TO CHINA’S EV INDUSTRY)

September 6, 2024

Hello everyone

Xpeng (XPEV) to launch new models later this year.

Chinese EV maker, Xpeng could see a significant move by the end of the year as two new key EV models are being unveiled in the fourth quarter of this year.

JP Morgan has upgraded the China-based electric vehicle maker from overweight to neutral.It also increased its price target for U.S.-listed shares to $11.50 from $8 per share.From Wednesday’s close that implies a 36% upside.

The demand for EV’s globally has cooled in 2024.Consumers have obviously rebelled against the EV adoption marketing slogans & EV technology and have instead dug in their heels…sticking closely to their traditional gas-guzzling machines.

Demand in China for EV’s has been much higher compared to the U.S.The rollout of its Mona M03 and P7 plus sedans could nearly double the company’s overall vehicle delivery from the third to the fourth quarter.

At a starting price of $US16,812.00, the Mon M03 is directed at the lower to middle-income earner.

Looking into 2025, the current estimate is that sales volume can top 300k units thanks to more new models, which is a big jump from 180k in 2024.

Shares could see growth on the heels of the new vehicles.When Xpeng launched its G6 sports utility vehicle in 2023, the stock advanced roughly 30%.

Weekly (XPEV) chart

The Mona M03

I recommended (XPEV) on March 15 this year when it was $10.05.If you bought some shares at that time and are still holding – well done for showing patience.

For those that don’t own the shares, you can either watch the action in the shares from the sidelines or buy a small parcel of the stock over the next month.

You can see from the chart above that the stock has moved sideways since the beginning of year, which could be a precursor to a breakout rally.

China appears to enjoy a solid position in the EV industry. The country is now the world’s largest exporter of cars, having surpassed Germany and is even now outpacing Japan.By destination, the EU holds the majority share, accounting for 47% of China’s EV exports in value last year; exports to Thailand, the Philippines, and India have also proved strong.In a strong contrast, exports to the U.S. fell 32% year over year in January – October, curbed by high taxes and U.S. restrictions.China’s automakers pay a 27.5% import duty to send vehicles to the U.S. compared with just 10% on cars sent to the EU.

Let’s get real.August, September & October are usually very tricky months for the stock market. Or to put it another way, the market is usually awful and moody during these months.So, expect quite a bit of turbulence during this time.

The market could pull back 7-10% during this time.The U.S. election is coming up and the Fed meets in mid-September to deliver rate cuts or not. The environment makes people nervous.And people become cautious at this time.

The release of the non-farm payrolls data this Friday could cause a lot of volatility.If the August data comes in hotter than expected, September rate cut expectations might be quickly marked down.

Still, markets are pricing in a 67% likelihood that the Federal Reserve will cut by a quarter percentage point in September, according to the CME FedWatch Tool.

Stock up on Gold as a hedge against geopolitical and financial risks.

Going into year-end and well into 2025, we should see gold rally toward $3,000, particularly with the near 100% certainty (depending on data) that the Fed will cut rates in September, and possibly again later in the year.

Investment bank analysts at Goldman Sachs point out that emerging market countries are continuing to buy gold – with purchases tripling since the middle of 2022 amid fears of U.S. financial sanctions and a mountain of sovereign debt.

China is weighing on crude oil and copper prices.Its weak real estate sector provides only limited upside for steel, which presents challenges for iron ore prices.But this “winter season” cannot last forever.According to BHP’s CEO, we could start to see a turnaround in China’s real estate sector within the next 12 months.

Analysts at Goldman expect copper to average about $10,100 per metric ton in 2025, well above this year’s average of $9,231.

Goldman’s view long term is that metals important for the energy transition away from fossil fuels, such as copper, will ultimately reach scarcity pricing as demand grows, investment declines, and inventories fall.

Recommendation:Scale into gold and silver stocks on down days over the next eight weeks, particularly if you have no holdings in this sector.

You should be looking at (GLD), (GDX), (WPM), (SLV), (GOLD), & (NEM).

================================================

If you have good profits from any LEAPS recommended earlier this year or last year, consider taking profits.

(THIS WEEK THE JOBS NUMBER WILL BE THE HEADLINE EVENT)

September 2, 2024

Hello everyone.

Week ahead calendar

Monday, Sept. 2

Labor Day Public Holiday (U.S.) Markets closed.

4:00 a.m. Euro Area Manuf. PMI

Previous:45.8

Forecast: 45.6

Tuesday, Sept. 3

9:45 a.m. S&P PMI Manufacturing final (August)

10:00 a.m. Construction spending (July)

10 :00 a.m. ISM Manufacturing (August)

9:30 p.m. Australia GDP Growth

Previous:0.1%

Forecast: 0.3%

Wednesday, Sept 4

10:00 a.m. Durable Orders final (July)

10:00 a.m. Factory Orders (July)

10:00 a.m. JOLTS Job Openings (July)

2:00 p.m. Fed Beige Book

9:45 a.m. Canada Rate Decision

Previous:4.5%

Forecast: 4.25%

Earnings:Hewlett Packard Enterprise, Hormel Foods, Dollar Tree.

Thursday, Sept. 5

8:15 a.m. ADP Employment Survey (August)

8:30 a.m. Continuing Jobless Claims (08/24)

8:30 a.m. Initial Claims (08/31)

8:30 a.m. Unit Labor Costs final (Q2)

10:00 a.m. US Services PMI

Previous: 51.4

Forecast: 51.5

Earnings: Broadcom

Friday, Sept. 6

8:30 a.m. US Nonfarm Payrolls

Previous: 114k

Forecast: 163k

Happy Labor Day!

Welcome to September, which is seasonally the weakest month on the calendar.There are plenty of events this month, which will keep investors pacing the floor.To kick off all the action, we have the job numbers this Friday.

This week’s US employment data will be critical for the September FOMC meeting (September 17-18).A significant miss in jobs data could prompt the Fed to cut rates by 50bps in September instead of 25.

Other events include a rate decision from the Bank of Canada on Wednesday.The BoC was the first to cut rates, and other central banks are now following suit.The Canadian dollar has been making significant gains in recent weeks, particularly against the dollar and the euro, but its strength may not hold if the BoC continues its rate cuts.

Rotation out of tech stocks and into this year’s market laggards should continue.But maintain exposure to Big Tech, which could rally closer to year-end.

A few years ago, China cracked down on gaming.Now, it has a global hit on its hands.In its first attempt at a video game, China has smashed records setting alight the industry’s global ambitions.Black Myth: Wukong is an action game set in mythological China, and it has sold 10 million units three days after its launch on August 20. The rich cultural elements give them a global appeal and set them apart from games developed in other regions.China could be on its way to a mega industry with many other stories that have been passed down over the last millennia, yet to be transformed into video games.

QI CORNER

MARKET UPDATE

S&P 5000

The market is still rallying within its final 5th wave advance to complete its bullish trend sequence from the 3,492 bottom of October 2022.

Support = around 5570

Resistance = 5,735/5765

GOLD

There is potential for more upside here.

Support = $2,470

If we see a strong break of the $2,470 area, a deeper corrective move could see gold correct back to the $2420/$2400 area.

BITCOIN

There has been a lot of choppiness in Bitcoin lately.There is a risk that we could see bitcoin correct towards the $44,000 area before a firm rally takes place.And we might not see this bullish rally take place until late September/October.Be patient.

Markets are going into the worst month of the year overbought and begging for a correction.

September 18 interest rate cut now a sure thing, says John, but how much good news is already priced in?

A lot will depend on NVDA earnings out after the close today.

The next selloff is one you buy into.

US dollar is trash and could stay weak for years.

Technology stocks will recover after a much-needed correction.

Energy gets dumped on recession fears if the Fed acts too slowly.

Buy stocks and bonds on dips, but now it’s ALL sectors.

THE GLOBAL ECONOMY – NEW STIMULUS

Jay Powell says the “time to adjust policy is here.

Where did the 818,000 jobs go?Monthly job gains fell from 250,000 to 175,000.Is the message that the Fed waited too long to cut rates?

Goldman Sachs cuts recession risk to 20%

Consumer sentiment drops, to an eight-month low.

Price Index is a snore, at 0.2% MOM and 2.9% YOY.

US Producer Price Index fades, coming in at a weak 0.1%.

China Loan demand hits 15-year low.

UK grows by 0.6% in Q2, a far cry from the US 2.8% rate.

STOCKS – RECORD RALLY

Stocks mount record rally, up 11%, bringing the Magnificent Seven back to the fore.

Risk is now high, and you can still get 5.01% for 90-day T-bills.

The next dip is one you buy.

However, the bull market is finally broadening out with a big focus on interest sensitives like housing, builders, emerging markets, and small caps.

$6 billion poured into US equity funds last week.

Now it’s volatility that’s crashing, down a record $49 points from $65 to $14 in 9 trading days.

Global EV sales jump 21% YOY, in July thanks to a large rise in China.

Buy on dips: Netflix (NFLX), Caterpillar (CAT), Deere (DE), VISA (V)

BONDS – FROM STRENGTH TO STRENGTH

Market prices in 50-point basis cut for September, holding on to massive rally.

A cut of only 25 basis points on September 18 could give us a $5 sell-off.

The September 6 Nonfarm Payroll report and Unemployment rate will be crucial.

(TLT) could make it to $110 by yearend, keep all LEAPS.

It’s not too late to buy derivative fixed-income plays.

Buy (TLT), (JNK), (NLY), (SLRN), and REITS on dips.

FOREIGN CURRENCIES – DOLLAR IS TRASH

Dollar hits seven-month low, as US interest rate cuts loom.It could be a decade-long move.

The Yen carry trade is back, with hedge funds piling back into positions they baled on only two weeks ago.

It’s just a matter of math, now that the Bank of Japan has given up on raising interest rates anytime soon.

What this means is more leverage, risk, and volatility for global financial markets. I love it!

The prospect of falling interest rates means that the greenback is toast.

Buy (FXA), (FXE), (FXB), (FXC).

ENERGY & COMMODITIES – RECESSION DRAG

Oil collapses to $71 a barrel, taking the rest of the commodity space down with it.

Cut off of 1 million barrels/day of Libyan production gives oil a brief respite.

This is despite the support from multiple Middle Eastern wars.

No one wants to pay for storage during a recession, especially with the current high interest rates.The worst-performing asset class of the year just got worse.

Weak Chinese economic data was the gasoline on the fire.

Replacement by EV’s and the shift out of cars into planes are big factors.

Copper flips from shortage to surplus, as the Chinese economic recovery drags on.

PRECIOUS METALS – NEW HIGHS

Gold pennies new all-time highs as Chinese have no other savings alternative.

Silver takes a break from economic slowdown, and enters a sideways range.

Miners have started to outperform metals for the first time in years, indicating an increase in investor leverage.

A global monetary easing is at hand.

Buy precious metals on the dips because rates are now falling decisively.

Buy (GLD), (AGQ), and (WPM) on dips.

REAL ESTATE – SALES BUMP

Mortgage rates hit the new 2024 low.The average for a 30-year, fixed loan was 6.46%, down from 6.49% last week.

Existing Homes sales jump in July for the first time in five months, up 1.3% to 3.95 million units.

Inventory is up a whopping 20% YOY.

The median home price rose to $442,000, up 4.2% YOY, with some 27% of sales all-cash buyers.

Sales of home over $1 million are up 26% YOY because the supply is up over 30%.

New-home construction dives, in July to the lowest level since the aftermath of the pandemic as builders respond to weak demand that’s keeping inventory levels high.

Total housing starts decreased by 6.8% to a 1.2 million annualized rate last month.

TRADE SHEET

Stocks – buy the next big dip.

Bonds – buy dips

Commodities – stand aside

Currencies – sell dollar rallies, buy currencies

Precious Metals – buy dips

Energy – avoid

Volatility – sell over $30

Real Estate – buy dips

NEXT STRATEGY WEBINAR

12:00 EST Wednesday, September 11 from Lake Tahoe, Nevada

JACQUIE’S POST HOUSEKEEPING

The August Monthly Zoom Meeting will be next Tuesday, September 3rd.I will be sending out the Zoom invitation today.

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.