We are living in the era of Artificial Intelligence (AI), and it will change our lives in many ways.

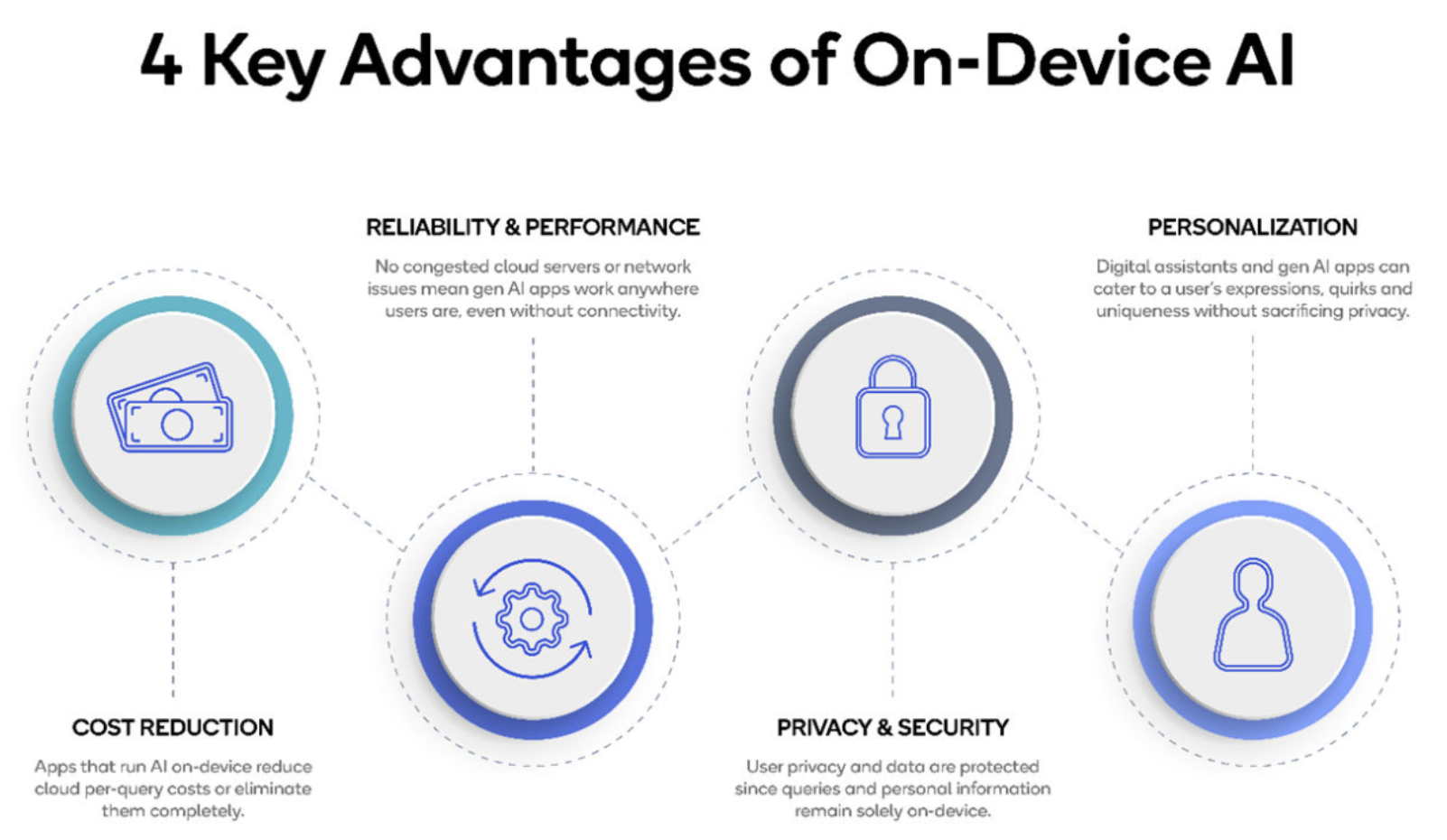

Within AI there is currently a large focus on Tiny AI or Minature AI which aims to improve the sustainability of artificial intelligence, thereby reducing its high carbon footprint. This emerging technology compresses the size of artificial intelligence algorithms - which use far less computing power - especially those that use large quantities of data and computational power. What this means is that this technology – Minature AI, can fit and run within microprocessors on consumer or the Internet of Things (IoT)-enabled devices. For instance, we can point to natural language processing (NLP) models like Google’s BERT. The larger version of BERT has 340 million data parameters and training it just once costs enough electricity to power a U.S. household for 50 days. In another example, we learn that a single training session of GPT-3, a popular language that produces human-like text, has the same carbon footprint as traveling 700,000 kilometers by car.

Tiny AI is a power saver and addresses the carbon footprint of artificial intelligence. It aims to reduce the amount of power needed by building algorithms into hardware at the periphery of a network, where they can perform data analytics at low power, avoiding the need to send data back to the cloud for processing.This improves latency as well as power consumption and enables Tiny AI to run on devices like our mobile phones, increasing their functionality but also improving our privacy as the data stays on the device.

As AI keeps popping up in our everyday lives, it raises several privacy concerns.Do you ever get the feeling that you are being constantly monitored in some way, or your privacy is being compromised?Smart home devices use AI to personalize the experience for each user.However, they store large amounts of data that is not particularly relevant for their applications, on the cloud – making it vulnerable to hacking.There is a demand now for on-device AI which enhances both privacy and safety for Smart Home Devices.The Tiny AI algorithms would run on consumer phone hardware, eliminating the need to analyse data on the cloud, thus reducing a significant amount of energy.Furthermore, it would also ensure ultra-low latency.Think about Google Assistant, the voice assistant on Google’s phone and smart home devices.After Google trimmed down its code so that it runs on-device rather than sending data to the cloud for processing, it processes requests a lot faster than it did before.

Tiny/miniature AI will impact all industries.This technology will facilitate the running of machine learning (ML) models to the smallest of chips and a diverse range of devices.This allows devices to be smart without connecting to the internet.Think for a moment about an autonomous car that doesn’t need to connect to the cloud or simply use a mobile phone to diagnose diseases in remote areas without the internet.Along with better algorithms, advances in embedded devices are advancing the trend.This allows for the development of devices that consume very little power and run for months or years.Now that’s a win-win for people and the environment.

(AUSTRALIAN RESEARCH IS UNLOCKING THE ENERGY OF THE STARS)

September 25, 2023

Hello everyone.

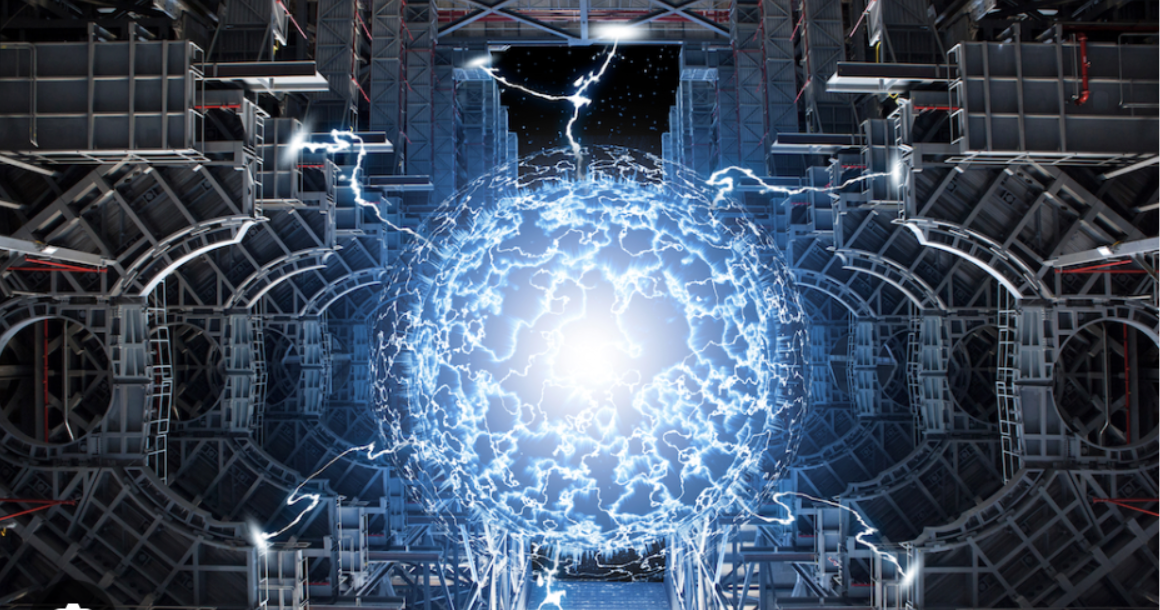

Students at a leading university in Australia are building a device capable of nuclear fusion – the process that powers stars and could unlock enormous amounts of carbon-free energy on Earth.

The magnet-powered, doughnut-shaped “tokamak” machine will be the first nuclear fusion device designed and built by students and will drive experiments aimed at bringing fusion to a commercial reality.The students will conduct experiments on superheated plasma with the machine to help industry partners accelerate fusion research.One focus will be how the machines handle plasma flares.

Fusion unleashes four million times the energy of coal, uses hydrogen as fuel, is regarded as safer than fission reactors and produces far less radioactive waste.

Nuclear fusion is the opposite of fission, which powers current reactors by splitting uranium atoms to unleash heat and radiation.

Fusion forces two atomic nuclei together instead.The atoms merge and become a different element, and the leftover atomic mass converts to astronomical amounts of energy.

It’s the same reaction that erupts in the sun’s core.In essence, nuclear fusion would bottle the power of a star.

Merging two atoms is difficult because the positive nuclei repel each other, like the same end of two magnets.The crushing gravity and immense heat of stars overcomes this repulsion and forces atoms to fuse.

A tokamak achieves fusion with magnets that whip hydrogen plasma (a charged gas) around a circular vessel and heat the gas to between 100 and 300 million degrees.

With experiments well under way, the next step will be to engineer the hardware that can maintain constant, safe, commercially viable fusion power that makes up for the massive amounts of energy used to blast a laser or fire up a tokamak. The target is to achieve 500 to 1000% more energy.

Experts say the technology won’t be developed quickly enough to help decarbonize energy grids and stop the climate crisis.Nonetheless, fusion energy could define how we power civilisation in the second half of this century.Most experts expect the technology to become commercially viable in 15-20 years.

There are endless possibilities with this technology.We need to prepare ourselves for a new nuclear society.

Nuclear fusion could transform our world as early as 2030 if research and funding are poured into this area.

Today I will provide you with a summary of John’s latest webinar which was done on Wednesday, September 20.

Webinar Title:Comatose

Lunches:

September 29 Zermatt, Switzerland

October 6 – Frankfurt, Germany (Dinner)

October 13 – Kiev, Ukraine

October 20 – London, England

October 31 – Miami, Florida

Trade Alert Performance:

No Trades/Positions

2023 year to date +60.80%

Average annualized return +48.15% for 15 years

+83.85% trailing one-year return.

Waiting for a better risk-reward before we enter any trades.

Method to My Madness

Big tech flatlines, leading to a comatose market.

Government shutdown is a new drag on all risk assets.But the tech sell-off will be brief.Too many people are trying to get into accelerating long-term earnings.

Bonds probing lows on rising interest rate fears.

Fall will present the best buying opportunities of the year.

Precious metals should be at the top of the buy list to cash in on an economic recovery.

Patience is key here.Let the market come to you.

The Global Economy - Best House in a Bad Neighbourhood

The U.S. has the strongest major economy in the world, while Europe, China and Russia are in recession.

United Auto Workers go on strike, bring the Big 3 Detroit automakers to grinding halt.

U.S. Wholesale Prices jump 0.7% in August.

Consumer Price Index Rises 0.6% in August – the hottest read in 18 months.

U.S. jobless claims fall again to 220,000 – a drop of 5,000.The economy is reigniting again.

Beige Book shows consumer spending slowing.Rate Hikes will drag on the economy for at least a decade, as the Fed $8.24 trillion balance sheet unwinds.

Australian economy surges, as the return of Asian tourists and infrastructure spending kick in.

Fed will start cutting interest rates next year.Market discounts events 6-9 months in advance as they are forward looking.

Mad Hedge Profit predictor at 53 = no trades.

Thank you for all the donations to my Ukraine humanitarian mission. Much appreciated.

Stocks – Going Nowhere

Stocks are chopping around in a narrow range on low volume with a slight downward tilt.

Government shutdown prospect is pouring water on any spark.Government runs out of money on September 30.

Salesforce beats with revenue up 11% YOY.

Raytheon takes a hit from Jet Engine problems.

Arm Holdings jump 25% on first day of trading.Masayoshi Sohn is happy because he still owns the remaining 90% of the company.This is where the hot money is going.

Caesars Entertainment and MGM suffer major hack.They have paid 15 million to end the issue.

Oracle disappoints on fading cloud growth in the recent quarter.

Vinfast IPO burns latecomers, as the money losing Vietnamese EV maker crashes after launch, down 83%.

No short-term trades here.

Buy the dip in Homebuilders.S&P should go to new highs by year end.Tech stocks continue to move side-ways for now.

TSLA target is $300-$400 by the end of the year.

NVDA is a screaming buy at $400.

BA is a good buy here.Also, a good LEAPS candidate.Enter 200-210 LEAPS and you’ll get a 100% return on your money in a year.

All the banks are good buys here as this sector is cheap and will roar back on an economic recovery.

Bonds

10-year Treasury Yield hit new 16-year high at 4.38%.

Government shutdown is new negative.

The U.S. Budget deficit is climbing once again increasing treasury bond sales.

The whole falling interest rate, rising bond price trade have been delayed for six months thanks to Fitch downgrade and hotter-than-expected economic growth at 2.40% for Q2.

Keep buying 90-day T-bills now pushing a 5,48% risk-free yield.

Still looking like a 3.50% 10-year yield by the end of 2023.

Junk Bonds ETFs (JNK) and (HYG) are holding up extremely well with a 6.5% yield.

Bonds (TLT) still likely to hit $110 by year-end.

Scale into Bonds now – beneficiary of falling interest rates and an economic recovery.

RE: TSLA trade idea:scale in on a one-month basis.You need to work out how much you want to buy, and then buy 1/30th of that amount every day for a month.You won’t get the absolute bottom, but when the turnaround happens then it goes up 50-100%.That’s the way to play TSLA.

Saudi Arabia created a short squeeze in oil by taking 5 million barrels off the market with Russia.That got prices up.Saudis tend to back off when oil gets to $100 as it adversely affects their investments in Europe and the U.S.After topping $100, Saudis may start bringing supply back on.

You can take the option of taking profits if you did the oil trade in June.

We are waiting for a capitulation in Bonds (TLT).

An 85-90 call spread is then offering you 100% one year out.

I recommend 4 months T-Bills which expire in January as it takes advantage of the cash squeeze you always get in the new year.

Returns on 4 months T-bills are much higher than 3, 2, or 1-month T-bills.

For me to do a trade now, it must have a very low risk and a 20% return.The market is not offering this, so no trades.Instead buy T-bills which give you a guaranteed return.

Foreign Currencies:

Fed gives an adrenaline shot to the U.S.$.

Long of the year may be setting up in the Yen.This could spell the end of a zero-interest rate policy in the Land of the Rising Sun, the last country to use it.

Collapse of the U.S.$ is a 2024 story.

Aussie $ collapse prompted by slowing Chinese economy – not buying their energy or commodities.

Buy (FXE), (FXB), (FXA), (FXY).

Energy and Commodities

Saudi production cutback is now at 4 million barrels/day, a 20-year high, squeezing prices to a new 2023 high.

Biden may counter with a release from the Strategic Petroleum Reserve on SPR.

Gas prices jump 10% in Europe, as a long-threatened strike ensues at Australia export facilities.Chevron used the strike to cancel contracts in anticipation of long-term falling gas demand.

Electrification will be the big theme of this century.

The power grid has to increase fivefold in size to accommodate the electrification projects already underway.

Precious Metals

Fed knocks precious metals markets for the short term.But gold is headed for $3000 by 2025. The driver will be falling interest rates.Silver is the better play here.Russia and China are still stockpiling to sidestep international sanctions.

Real Estate – A Slow Awakening

New U.S. Home mortgages hit 27-year low and have virtually ground to a halt.A 30-year fixed rate at 7.27% is the cause, which no one can qualify for.Yet, home prices are going up.Climate risk is a growing factor in home selection.Home builder sentiment turns down for the first time in 7 months in August to 45.High mortgage rates are taking their pound of flesh. Home builder incentives are making a comeback.

Crown Castle International (CCI) – great LEAPS opportunity right here at $96.97.

Home Construction (ITB) at $81.88.Let it fall a little more and buy it.

Next Strategy Webinar from Zermatt, Switzerland on October 4, 2023.

Cheers,

Jacquie

John’s journey starts in London, then Switzerland, Frankfurt, Poland, Ukraine, and back to London.

The Tesla pick-up truck, Cybertruck, is a one-of-a-kind vehicle.It has an exoskeleton that is nearly impossible to penetrate, a stainless-steel reinforced body, and armor glass. Every component is designed for superior strength and durability. The Tesla internals are made of a paper composite material, making it environmentally friendly and durable. The material is heated and made to look like marble giving it a luxury look. And it can run 500+ miles on a single charge.What’s not to like?

Yes, the Cybertruck runs on electric power, but let’s think about how the car was put together in the first place.Large amounts of energy, aluminum, and mined materials are needed to build the Cybertruck. Doesn’t this go against Musk’s climate-preserving principles?Eliminating tailpipe emissions is all very well, but when you are mining battery materials to achieve this end, the process itself is environmentally damaging. The negative effects include groundwater pollution from mining scraps and chemicals and the fact that underage labour is used at many mines outside Western countries.

While it may produce less carbon pollution, its status as an entirely environmentally friendly vehicle is debatable.The tires and the weight of the car are a problem.Heavy EVs seem to create more harmful tire dust than conventional vehicles and the tiny particles that are shed float in the air and leach into our waterways, which damages human health and wildlife.A hazardous chemical treatment typically used on tires is linked to declining salmon populations in the U.S. and tire dust is arguably seen as an unregulated contributor to lung and heart disease.

The tire wear is much greater because of the added weight of the vehicle, and researchers in this area state that most of this will be created under acceleration, braking, and cornering.

The Cybertruck is a niche, fashion statement vehicle, but will it meet the needs of customers who want it to equal a regular pick-up?

One thing that could put many off is the price. Most customers buy a pick-up truck with a purpose in mind. It should be functional, reliable, and economical.Tesla is known for its pricey cars, so buyers of regular pick-up trucks may not find the Cybertruck an affordable vehicle.Additionally, Tesla has no experience designing and manufacturing pick-up trucks. The company has only designed SUVs and sedans, so early customers may find some shortcomings in the design and performance of the Tesla pick-up truck.

On the plus side, the Tesla pick-up truck is sure to offer advanced features and technology not offered by any other regular pick-up trucks.Tesla is known for incorporating cutting-edge technology into its vehicles. Self-driving features and high-tech infotainment systems spring to mind. This would appeal to the tech-savvy community.

Additionally, Tesla has a reputation for producing high-quality vehicles that need little maintenance in their lifetime.As a reliable and economical vehicle, the Cybertruck could be seen as more attractive in that it would probably require less maintenance and replacement parts than a regular pick-up truck.

So, with the pros and cons put on the table, we will have to wait for the first Tesla Cybertrucks to hit the road before customer reviews and testimonials tell the real story.

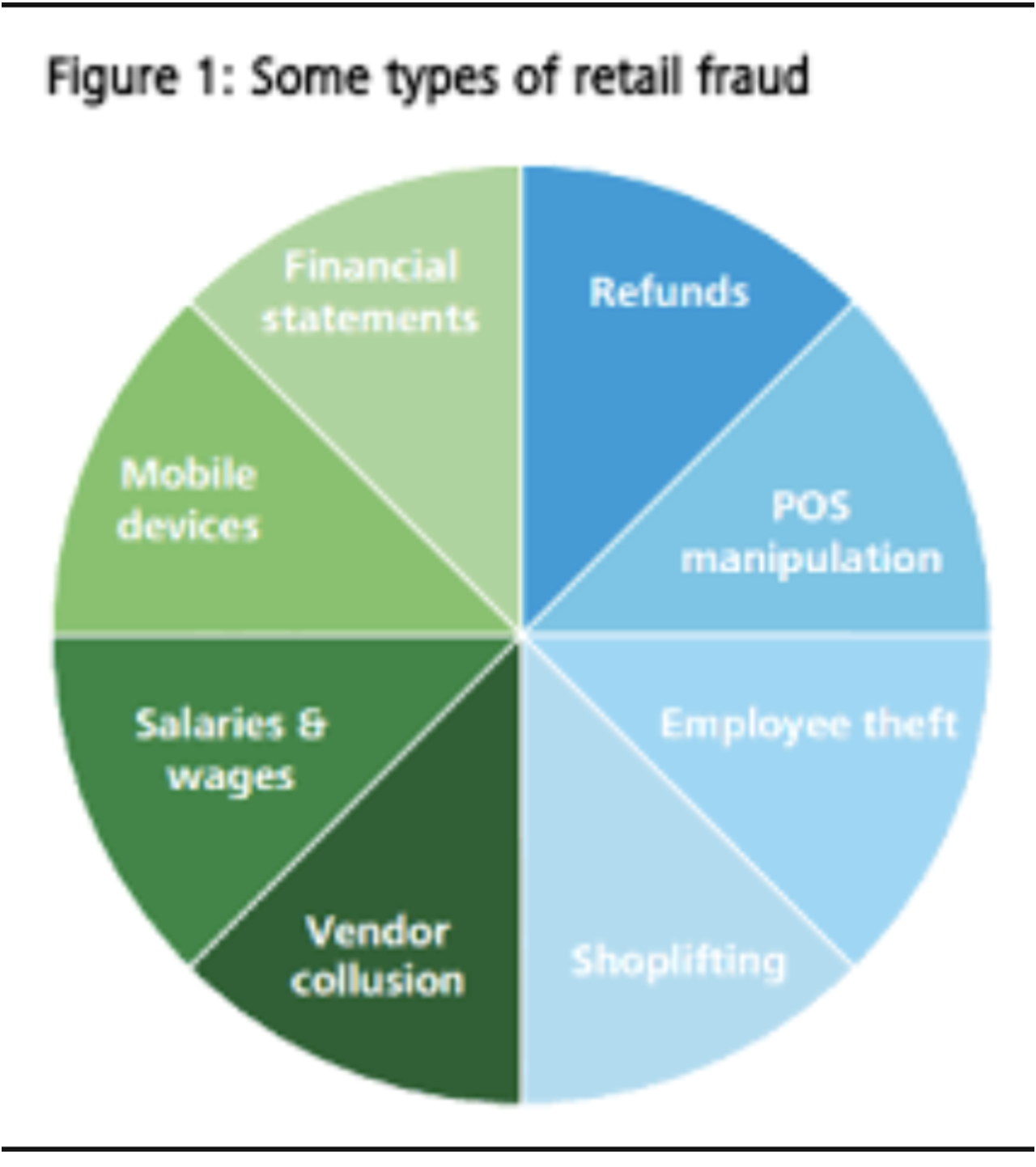

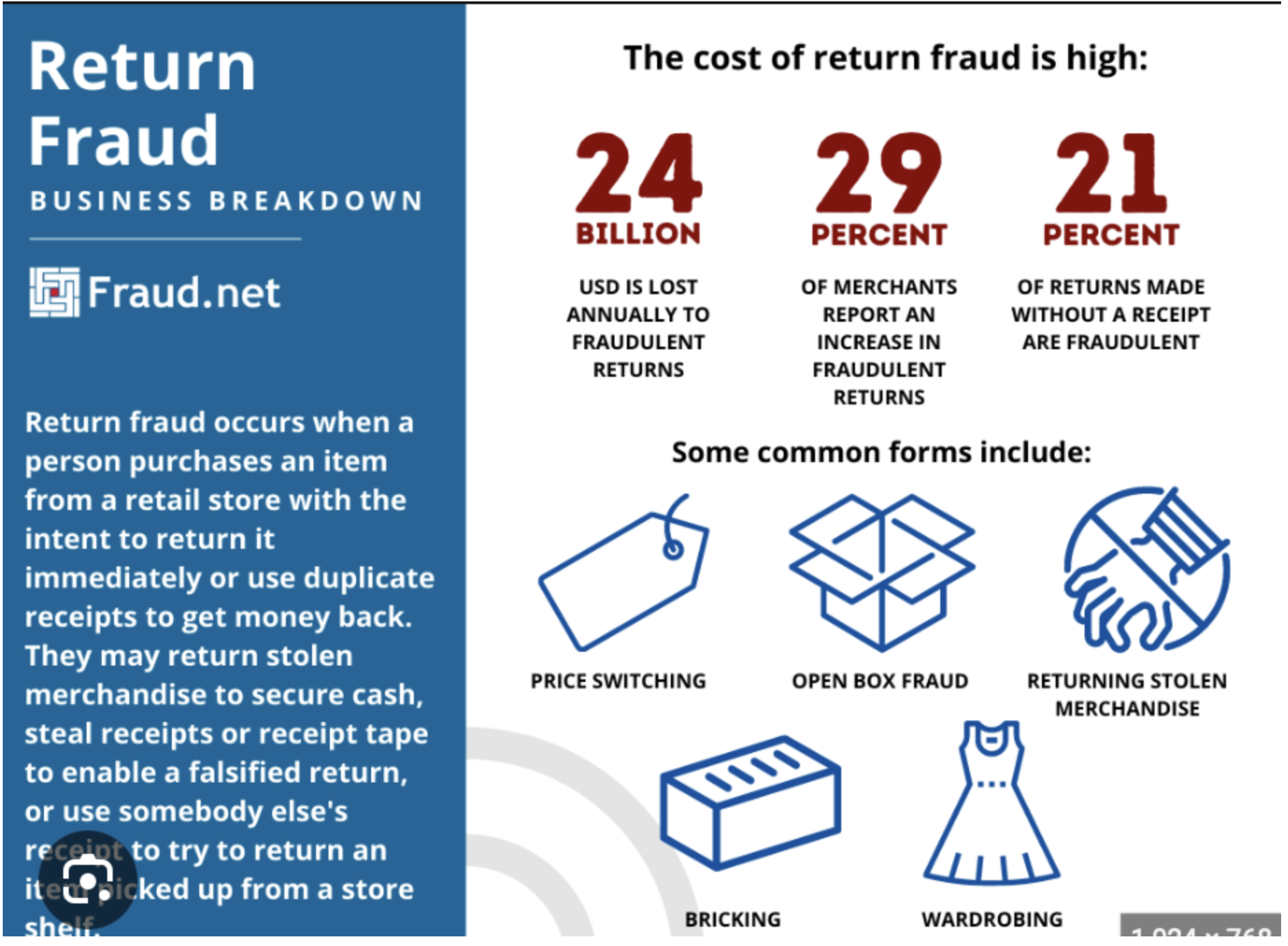

Every year global companies are losing large amounts of money by virtue of customers abusing company policies. Return fraud, coupon stacking, and fake accounts are costing retailers around $100 billion annually.

Some would say it is the cost of doing business.

But for retailers, it is a hard act to swallow.

Some of the practices customers use include using multiple email addresses to take advantage of promotions more than once.Another one is buying multiple items with the intention of returning most of them or wearing an item with plans to return it and not pay for it.

Some customers also buy an item and then say it is faulty and request another item be sent. Company policy requires that a new item be sent out for free as a replacement for the faulty one, (which isn’t faulty at all). These customers are then on-selling the items through another online shop. This technique is common for limited-edition sneaker drops.

Another type of policy abuse includes using bots to buy out highly valued items and re-selling them for a higher cost on a third-party platform (like the example given above). An example here would be concert tickets, which happened during sales for Taylor Swift’s Eras Tour.

These lax policies are allowing fraudsters to have a field day.

In one example I read about a pet supply company based in the U.S. that lost $3.5 million in the first quarter of 2023 after a small group of serial fraudsters exploited a promotion code for a 35% to 50% discount.

Trying to fight back against this type of abuse is extremely difficult as companies don’t have the resources or the time to check every claim. Perhaps red-flagging customers who appear to show repeated behaviors is a way to fight bad actors who are taking advantage of programs.

In other news…

Arm debuted on the stock market on September 14. IPO was priced at $51 a share.It jumped nearly 20% during intraday trading.At the open it was valued at almost $60 billion.

Many of us are on the lookout to increase our income.

There are some ways to do this.

We know with interest rates surging our cash in savings accounts receive higher yield and 90-day T-bills also offer a good 5%+ yield.

But is there anything else besides Bonds where investors can find robust returns?

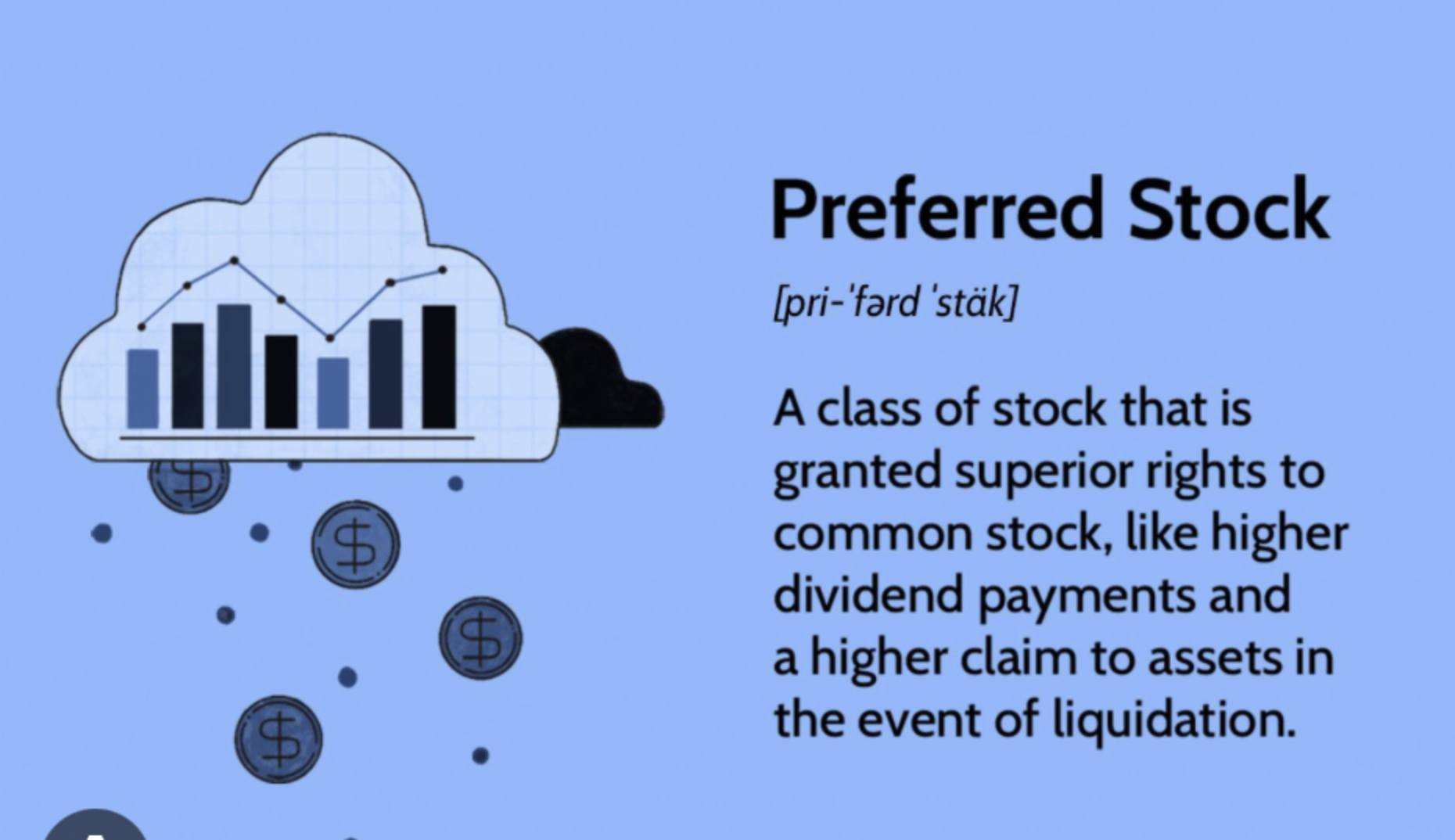

Preferred stocks are one option that comes to mind.Both my mother and I owned these in the 1990’s and early 2000’s. They combine elements of stocks and bonds in one investment.

Preferreds are attractive because they provide the stability of fixed-dividend payments, which is bond-like, but they also offer equity like appreciation. So, it is a nice balance. (Note, that the equity price appreciation is often lower than common stock.)

Bonds are offering 5%+ right now, but a preferred stock gets investment grade security that yields 6.5% - which is solid income – without taking on too much credit risk.

Most investors are attracted to preferred stocks because they offer more consistent dividends than common shares and higher payments than bonds. Preferreds are issued with a fixed par value and pay dividends based on a percentage of that par, usually at a fixed rate. Let’s say that a preferred stock had a par value of $100 per share and paid an 8% dividend. To calculate the dividend, you would need to multiply 8% by $100 (the par value), which comes out to an annual dividend of $8 per share. If dividend payments are made quarterly, each payment will be $2 per share.

One downside of preferreds is that they don’t have the same voting rights as common shareholders.The company is not beholden to preferred shareholders the way it is to traditional equity shareholders.

To recognise a preferred stock, look for a P at the end of the ticker symbol.

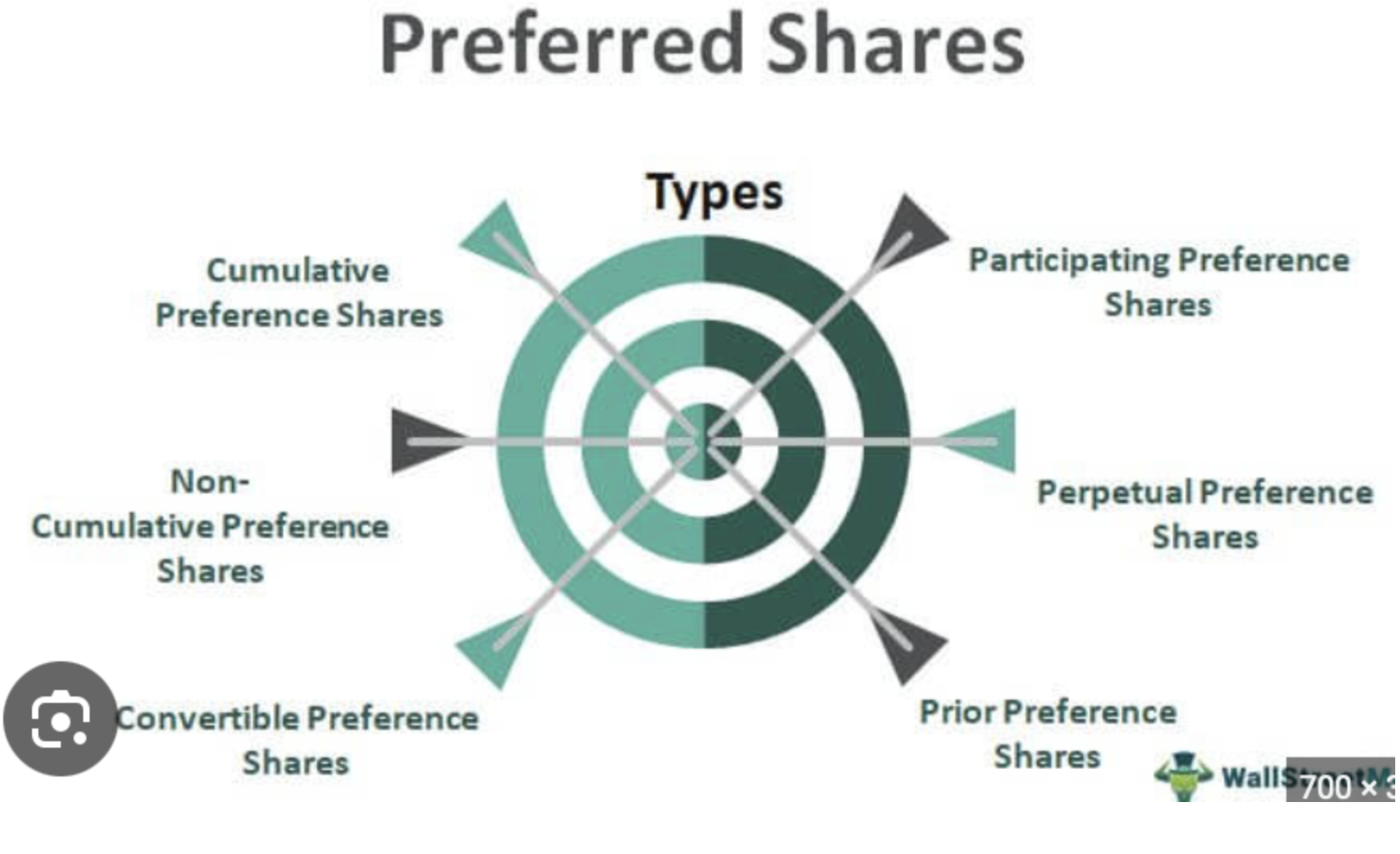

Convertible shares are preferred shares that can be exchanged for common shares at a fixed rate. This can be very lucrative for preferred shareholders if the market value of common shares increases. (This is the type of preferred shares my mother and I held). Once the shares have been exchanged the shareholder gives up the benefit of a fixed dividend and cannot convert common shares back to preferred shares.

Cumulative preferred shares have a clause that protects the investor against a downturn in company profits.If revenues are down, the issuing company may not be able to afford to pay dividends.Cumulative shares require that any unpaid dividends must be paid to preferred shareholders before any dividends can be paid to common shareholders. If a company guarantees dividends of $10 per preference share but cannot afford to pay for three consecutive years, it must pay a $40 cumulative dividend in the fourth year before any other dividends can be paid.

Non-Cumulative shares do not entitle an investor to missed dividends. (If one year the company decides not to pay dividends, they won’t pay it the next year.As a result, the investor loses his or her right to claim any unpaid dividends.) Interest on a non-cumulative deposit is paid on a regular basis, whereas interest on a cumulative deposit is paid at maturity.

Participatory Preferred shares provide an additional profit guarantee to shareholders. All preference shares have a fixed dividend rate, which is their chief benefit. However, on top of that chief benefit, participatory shares guarantee additional dividends in the event that the issuing company meets certain financial goals. So, for example, if the company has a really good year and meets a predetermined profit target, holders of participatory shares receive dividend payments above the normal fixed rate.

Instead of looking for single stocks that offer preferreds, you could look at SPDR ICE Preferred Securities ETF (ticker: PSK), which yields 6.5%.

You could also look at ETF’s that focus on dividend paying stocks which offer another avenue for income. Pro-Shares S&P Dividend Aristocrats ETF (NOBL) is one that comes to mind. It’s an $11.65 billion fund that tracks the S&P 500 Dividend Aristocrat Index. The yield is 1.95% and year to date return is 4.43%.

The yield doesn’t appear crash hot when you first see it, but long-term, you have to remember this is stock investing, and therefore you get the opportunity for price appreciation.So, over the long term you will most probably receive better returns those bonds.

The much talked about recession that may happen or may not happen, whether it be hard, soft or in the middle of those descriptions is background noise at the moment, but it is always wise to hold high quality companies in a stock portfolio, and companies that have dividends which keep growing tend to be those high-quality companies.

We all think about it sometimes – retiring.What we would do, how we would spend our time, places we would see, hobbies we would take up, and causes we would support and become involved in.

But sometimes I hear that the reality doesn’t measure up to our idealized vision of the future.

One of the biggest cons I hear about is the loss of meaning in a person’s life.People retire and they think “now what”.Some people move into another career, with far less stress, while others have trouble finding that sense of peace and joy they were aiming for when they retired. This can lead to negative effects on mental health. Of course, then there could also be many years of low income, which limits the choices available to the retiree.

However, there are some studies that suggest that retiring early can actually lengthen your life.In a 2017 study in the Journal of Health and Economics in Amsterdam economists showed that male civil servants over the age of 54 who retired early were 42% less likely to die over the subsequent five years compared to those who continued working.The reasons were twofold:retiring frees you up allowing you more time to concentrate on and invest in your health.That could be sleeping more, exercising more, or addressing health issues promptly by seeing your GP.And secondly, work can be stressful, and retirement can alleviate that stress.We all know that stress can lead to hypertension, a risk factor for various potentially fatal conditions. Positive health effects of retirement have also been found by studies using data from Israel, England, Germany, and other European counties.

I think we would all agree that doing some sort of work gives your life meaning and purpose.Advice from a Japanese doctor and longevity expert who lived until 105 is “Don’t retire.”

Being in a work environment can keep your mind and, in some cases, your body active.If you work alongside others, that might also provide a sense of belonging.Social isolation is linked to cognitive decline and even death. Working can offer people a sense of purpose, which has a host of health benefits, including a healthier heart and lower risk of dementia.One study found that the longer you work, the lower your risk for dementia.

Of course, you have the option of volunteering after you retire.Sharing your skills with those who need your help.This can be very fulfilling work and can benefit you immensely because you are supporting a cause you are passionate about.

For those who choose to retire early, you need to keep challenging your mind.Learning a language or learning a new technology will keep your cognitive ability alive and well.

Leaving your job can come at a cost, but it does give you more free time.There are always trade-offs.If you spend that time wisely, you might be able to prolong your life.

(MARKET MOVEMENTS CAN BE UNDERSTOOD WITH THIS METHOD)

September 8, 2023

Hello everyone,

We have all heard of technical analysis and how it can fine-tune our entries into and exits out of trades.

I’m sure many of you have heard of moving averages, (RSI) Relative Strength Index, (MACD) Moving Average Convergence Divergence, Fibonacci, Elliott Wave theory, and Stochastics.

But have you ever heard of the Wyckoff Method?

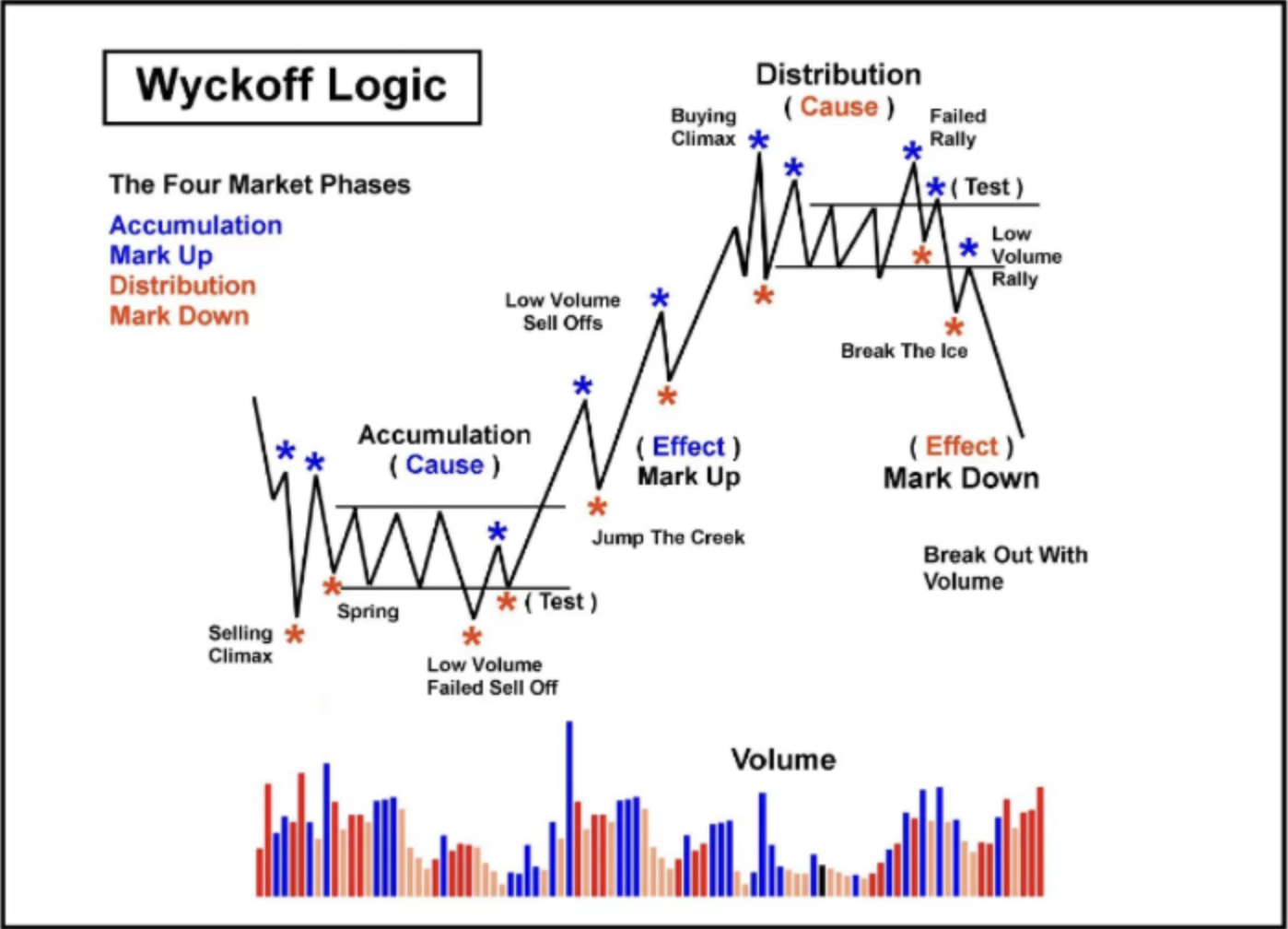

What is the Wyckoff Method?

The Wyckoff Method is a technical analysis approach to the markets that investors can use to decide when to buy and sell.The Wyckoff market cycle reflects Wyckoff’s theory of what drives a stock’s price movement.The method is based on the premise that stocks and markets move in predictable cycles.Wyckoff identified nine primary cycles, each of which has a characteristic pattern of price movement.The approach is relatively simple:when well-informed traders want to buy or sell, they carry out processes that leave their traces on the chart through price and volume.

There are four phases of a Wyckoff market cycle: accumulation, markup, distribution, and markdown.

At the top of the markup phase, another event is expected to happen – the Wyckoff distribution phase where the buying pressure ends, and smart traders take their profits and close their positions.

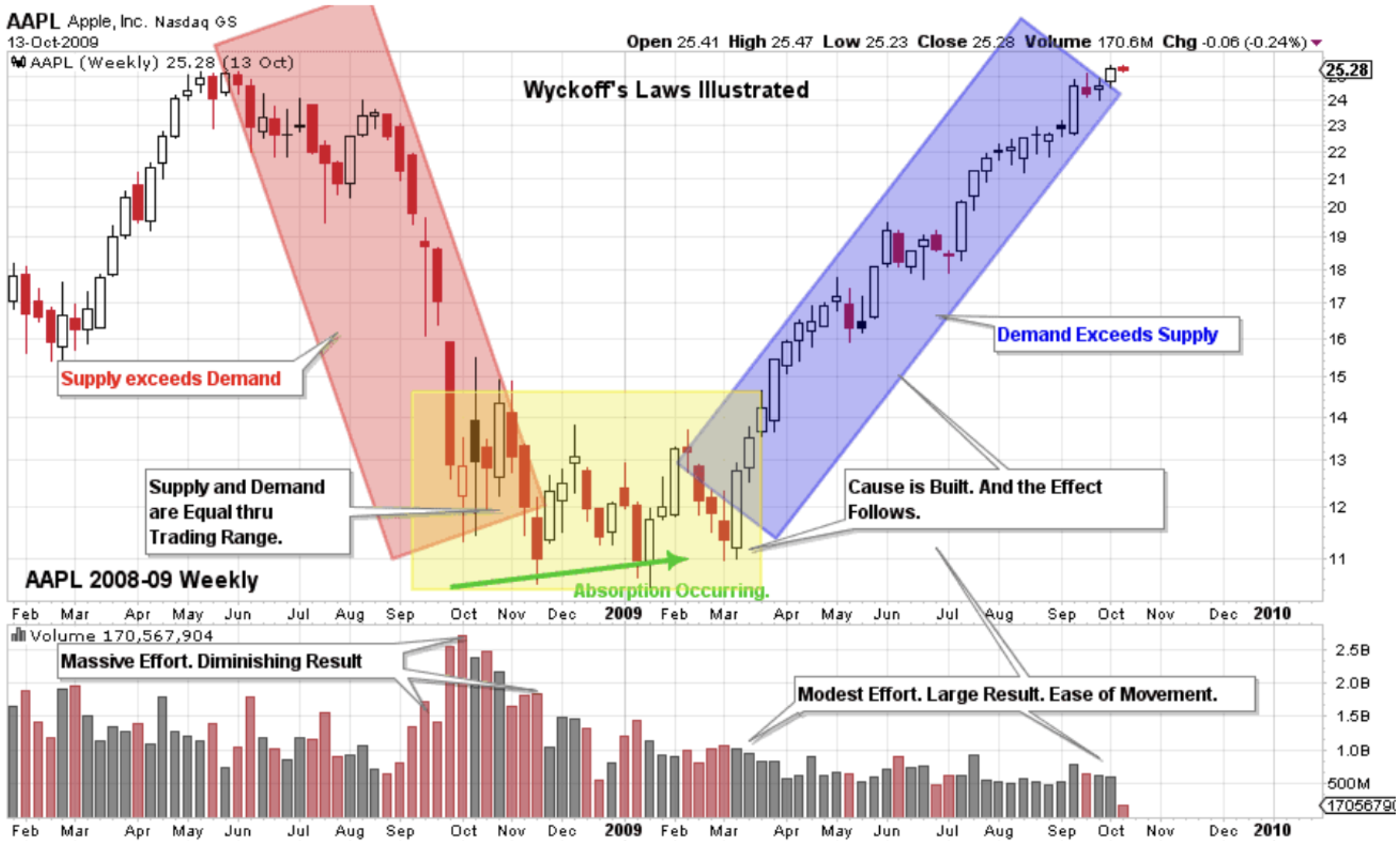

The Wyckoff Method is based on three laws:the law of Supply and Demand, the law of Cause and Effect, and the law of Effort vs. Result.

The Law of Supply and Demand states that the price of a stock is determined by the balance between the supply of shares available for purchase and the demand for those shares.When demand for a stock is high, the price will rise, and when supply is high and demand is low, the price will fall.

The Law of Cause-and-Effect states that every price move has a cause, whether it is a fundamental development or market speculation.By identifying the cause of a price move, traders can better understand the likely direction of future price movements.

The Law of Effort vs Result states that the market moves in trends and that these trends are characterised by periods of accumulation, markup, distribution, and markdown.The effort, or the amount of buying or selling pressure, and the result, or the price movement, can be used to identify the stage of the trend and make informed trading decisions.

The Wyckoff Method was developed by Richard Wyckoff (1873-1934).It consists of a series of principles and strategies initially designed for traders and investors and can be applied to all financial markets.

Wyckoff started as a stockbroker at the age of 15 and by the age of 25 he already owned his own brokerage firm.

Through his observation, while working as a broker Wyckoff noticed the manipulations the big operators carried out and with which they obtained high profits.

He stated that “it was possible to judge the future course of the market by its own actions since the price action reflects the plans and purposes of those who dominated it.”

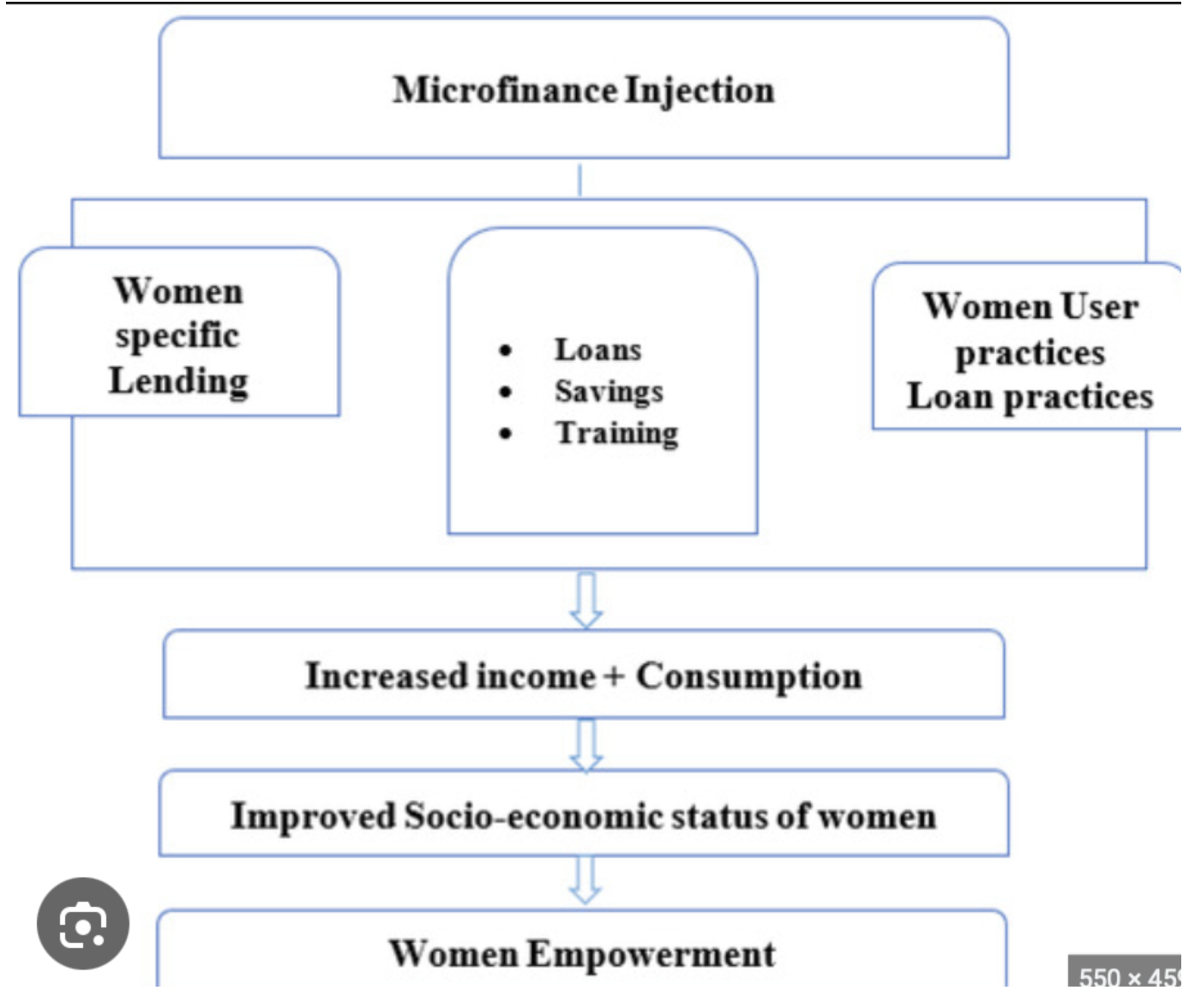

I came to understand a lot about microfinance when I was living in the U.K. while my son was at school there.My sister-in-law runs a charity based in Uganda.She saw first-hand the difference microfinance made for women in rural Ugandan communities. During many of our lengthy discussions about her experiences with these Ugandan women, I came to appreciate the power of microfinancing and how empowering it is for women in undeveloped parts of the world and developed parts of the world.

What is Microfinance?

Microfinance is typically seen as a financial service that many financial institutions and non-.

profit organisations provide to an individual or group of people who are excluded from traditional banking services.Many microfinancing entities offer small portions of working capital loans as credits.The small portions of capital loans are called microloans or microcredits.

Types of microfinancing.

Microcredit is a part of the larger microfinance industry which focuses on providing individuals having low income with credit, savings, insurance, and other possible financial services.The interest on the loan and the amount of the loan will depend on the size of the business and whether it is in an urban or rural area.For example, a farmer may require small funds to buy seeds for the season.In this case, the microcredit institution or non-profit can offer the farmer small lines of credit and small loans.

Microloans are short term loans in small amounts for entrepreneurs, small business owners, who need an injection of capital to start a business.These loans can also be used to pay salaries of newly appointed employees or simply for maintaining cash flow. The main purpose of these loans is to promote socio-economic development and support new start-ups.

Microinsurance targets people in the informal sector and is available for people on low incomes.Microinsurance can help in one-time events such as a day trip or emergency health requirements.It is available to people who hold few or no assets.It may be used to cover an agricultural crop.

Micro savings are the savings accounts that allow individuals and businesses to save money in smaller amounts or increments.Usually has zero service fees and flexibility on withdrawals.

The main characteristics of Microfinance:

Collateral is rarely required.Many microfinancing institutions offer collateral-free financing services to individuals and businesses.

Most borrowers have low incomes. The purpose then is to provide financial assistance to people – businesspeople or entrepreneurs - who do not have access to easy banking solutions.

The type and amount of the loan varies according to location and business.Microfinancing institutions usually provides lines of credit and loans in smaller amounts.The amount may vary depending on the type of business and the location.

Loan tenure is usually short.Individuals can repay the amount in smaller installments.The borrowers repay the amount of the loan within the time that micro-financing institutions decide.

The purpose of microfinancing is to generate business income for people in undeveloped parts of the world.

Benefits of Microfinance

Microfinance can help small businesses and individuals in both financial and social ways.They create self-dependency and sustainability in the economic aspects of their business.Microfinance motivates entrepreneurs and gives them the confidence to start a small business.It also helps individuals spend their savings on basic requirements, such as installing power or other necessary goals.With the help of microfinance, small businesses and individuals can put their ideas into reality.Microfinance provides security, economic growth, and business opportunities.

Provide accessibility.Imagine you were a woman living in rural Uganda with six kids.You cannot afford medication for your chronic ailments, education for your children, or birth control pills to stop having children. You have no identification papers that we mostly take for granted.I’m talking about a birth certificate, driver’s license, etc. Arguably, there are many, many women in Uganda who have zero assets and often fail to get loans from major banks.They also don’t have the necessary paperwork or certifications traditional banks require for loans.Microfinance makes it easier for these individuals to get financial assistance.

Microfinancing offers better loan repayment to women entrepreneurs.So, this helps empower women in their communities.

Microfinancing provides education opportunities.Many small families in rural areas depend on farming for their income.This can make it difficult for them to invest a lot of money in the education of their children.Additionally, such families may require men at the farm, so their children usually work with them.In such cases, microfinance can help families to focus on providing better education to their children.

Microfinancing can help create job opportunities.Microfinancing often provides businesses with an opportunity to create employment. Businesses can hire employees for different job roles.A business properly funded through microfinance can create local job opportunities can help in local economic growth.

Relieving financial burdens when starting a new business is made possible through microfinancing. Anyone knows that the immediate costs of a new business venture can create stress and worry.Microfinancing reduces monetary issues by providing them with financial services that allow them to pay their monthly bills.Therefore, with the heavy lifting done by microfinance, the business owner can focus on improving products and services for his/her target audience.It follows then that entrepreneurial activities become less stressful and allow other community members to engage in such businesses.

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.