John tells us that this could be the year of the 5% correction, and you need to buy everyone.

Expect an OK first half and a weak second half.

All interest rate plays remain pariahs, including gold, silver, homebuilders, bonds, and REITS.

Deregulation and end of antitrust plays will continue to be bought, including banks, brokers, money managers, nuclear, and Tesla.

US dollar rockets at higher rates for longer.

Technology stocks fade on threats to international business and slowing growth sales.

Energy reaches top of recent trading range on a strong economy.

John says to buy financial as the only sure thing this year.

THE GLOBAL ECONOMY – STRONG U.S.

December Nonfarm Payroll comes in hot at 256,000.

Headlines unemployment rate at 4.1%

CPI comes in at six -month low at 3.2% YOY.

JOLTS soars, coming in at 8.0 million, versus an expected 7.7 million.

US Online sales rose by 3% over the holidays.

Services PMI comes in hot at 54.1

Los Angeles fires to cost $230 billion, with only $30 billion covered by insurance.Inflation will rise as the cost of construction, labour, and materials soar.

Tame PPI boosts stocks, with the Producer Price Index rising 3.3% on an annual basis in December 2024.

STOCKS – CORRECTION TIME

The Trump bump is gone – stock markets have given up all their post-election gains.

John says that bank stocks will be the leaders this year with the MAG7 catching up later.

Bonds are now the big market risk.If we break a 10-year Treasury yield of 5.0% and take a run to 5.5%, the 5% stock correction turns into an 11% stock correction.

Technology was hit very hard.

Cleveland Cliffs Ramps up its bid for US Steel, bringing in Nucor as a partner.

$4 Trillion in Asset Management disrupted by Los Angeles fires.

Elon Musk sued by SEC for insider trading.Stock is up $20.

(Financials are good stocks to buy this year – look at the banks).

John believes we will get a sideways range for around 6 months in tech and then an upside breakout.Tech boom is just getting started.John doubts whether we get more than a 10% correction. John thinks that the first half of 2025 will be strong and the second half weak.

John’s advice:

Buy 5% dips on (JPM) JPMorgan and 10%-20% dips in (TSLA)Tesla.

Buy 90-day T-bills – 4.4%

Banks/financials: buy in the money LEAPS after a down move. Buy call spreads.

2025 will offer a limited number of stocks to trade.Think banks/financials, nuclear energy, and Tesla among a few others.

BONDS – THE BIG MARKET RISK

Bonds hit 14-month lows at a 4.80% yield, as fixed-income dumping continues across the board.

“Higher rates for longer” don’t fit in here anywhere.But there may be a BUY setting up for (TLT) at 5.0%.

Bond yields have rocketed 130 basis points since September.

National debt tops record $36 trillion and could rise another $10 trillion.

TIPS are making a comeback.

FOREIGN CURRENCIES – U.S. dollar surges

Dollar hits two-year high, on rising U.S. interest rates, and higher highs beckon.

Ten-year U.S. Treasuries have risen from 3.55% to 4.80%, a 14-month high.

Higher for longer interest rates mean higher for longer US dollar.

Don’t sell the US dollar until the next recession is on the horizon.

Avoid (FXA), (FXE), (FXB), (FXC), and (FXY).

ENERGY & COMMODITIES – A RALLY AT LAST!

Oil finally rallies, but only to the top of the recent range with the Gaza peace deal back on the table.

China ratchets up the trade war, banning the export of crucial metals essential for all tech applications.

Strategic Petroleum Reserve at multi-year lows, but Biden has stepped in as a buyer.

Blame a weak China, lost OPEC discipline, and overproduction by Iraq.

Avoid the worst-performing asset class in the market.

IEA predicts price declines this year.

Unlimited new drilling and opening of federal lands will crash oil prices.

PRECIOUS METALS – STRUGGLING TO RECOVER

Gold has recovered half of its post-election losses on the central bank and Chinese flight to safety buying.

Interest rates higher for longer is a death knell for precious metals, with gold down 8.3% after November 5.

The opportunity cost of owning gold is about to rise sharply.

Gold has become the only way the average Chinese can save as they can no longer speculate in real estate or copper and don’t trust the Chinese Yuan, so there is support lower down.

Central banks in emerging market countries are continuing to buy gold - $5.3 billion this year.

Avoid (GLD), (SLV), (AGQ), and (WPM).

REAL ESTATE – POOR OUTLOOK

High rates could leave real estate dead in the water for all of 2025.

However, a strong economy is allowing commercial real estate to recover in New York and San Francisco.

LA fires are creating a massive housing shortage there, with 12,000 homes burned.Higher housing prices and rents are a consequence.

Mortgage demand grinds to a halt on 7.17% rates for the 30-year fixed.

TRADE SHEET

STOCKS – buy the next big dip

BONDS- sell rallies

COMMODITIES- stand aside

CURRENCIES – stand aside

PRECIOUS METALS – stand aside

ENERGY – buy nuclear dips

VOLATILITY – sell over $30

REAL ESTATE – stand aside

NEXT STRATEGY WEBINAR

12:00 PM EST Wednesday, January 29, 2025, from Salt Lake City UT.

(THE BOND MARKET IS SPOOKED BY TRUMP ERA POLICIES)

January 15, 2025

Hello everyone

WHAT IS THE BOND MARKET SAYING?

Fears that the President-elect’s agenda, which has the rally cry “America First”, will reignite inflation and set in motion a wave of economic damage have unsettled bond markets and sent the US dollar sharply higher.

Last Friday, after the sizzling hot jobs report, bond yields spiked, and the US dollar strengthened.But the US is not unique here.A global surge in yields and a significant appreciation of the US dollar in recent months has unsettled investors and policymakers.

The global sell-off of bonds started in mid-September, days ahead of the US Fed’s 50 basis point cut to the federal funds rate.The Fed followed that with a 25-basis point cut in November and another 25-basis in December.

It seems odd, doesn’t it?Yields are rising as central banks like the Fed and the European Central Bank are cutting their policy rates.However, central banks tend to respond to the data in front of them while markets are more forward-looking.

The US jobs report, which showed 100,000 more jobs added in December than forecast, and unemployment falling, could be read as an indicator that the US economy is growing more strongly than investors had anticipated.

However, the longer-term trend, and the fact there has been a rise in yields globally, strongly suggest there are other factors at play here.

The US Treasury bond market tends to lead global bond yields. While some domestic circumstances might help explain movements in other markets, the underlying shift in yields on the longer-dated bonds in recent months appears to have been driven out of the United States.

In that market, the yield on the 10-year bonds has risen from 3.62 percent in mid-September to 4.76 percent, and the yield on the 30-year bonds from 3.93 percent to 4.95 percent.On Friday, the 30-year yield briefly spiked over 5 percent.

In Australia, the 10-year yield has been quite volatile but has trended up from 3.8 percent to 4.55 percent over that period, and the 15-year yield from 4.04 percent to 4.75 percent, even as the economy has essentially been flat-lining.

When the markets made big bets on the re-election of Donald Trump before the November election, share market investors were very bullish but bond investors appeared cautious about the implications for inflation of Trump’s economic agenda.

Now, it seems that bond investors are essentially pacing the floor far more intensely about Trump’s agenda than they were last year.And equity investors are beginning to share the bond investor’s pattern of angst.

Initially, equity investors were delighted about big tax cuts and deregulation, (which ought to mean more growth), but when Trump’s tariffs and his plans for mass deportation of illegal immigrants are factored in, it creates a definite unease about a new and significant outbreak of inflation.

The movement in the longer-term yields can, therefore, be seen as the pricing in of the risks of the Trump agenda.The tariffs on everyone have a global dimension.

Minutes from the December policy meeting show that the Fed has been pricing in the potential impacts of Trump’s trade, immigration, fiscal and regulatory policies.

The Fed’s own projections reflected an expectation in December of at least two more rate cuts this year.Market pricing agreed.

Fast forward a few weeks, and we get the uneasy realization that some US economic analysts are not only talking about just one rate cut but also the potential for rate hikes.

Not something that any of us want to think about.

Higher long-term interest rates and a higher US dollar increase borrowing costs, increase uncertainty, and certainly have a negative impact on emerging market economies, especially low-income countries.

Since September 2024, the US dollar has powered ahead by more than 9 percent against a basket of its major trading partners’ currencies (more than 12 percent against the Australian dollar).

Trump’s anticipated tariffs and the US dollar rally are linked together. When one country imposes tariffs on another, the imposing country’s currency tends to strengthen, and the currency of the country subjected to the tariffs tends to weaken.

So, with that in mind, if Trump’s words are followed by real actions, the dollar ought to strengthen further.I mean, we could be seeing the Euro at 0.9500, and the Aussie below 0.6000.An ever-strengthening dollar besides higher US interest rates rings alarm bells for the global economy, particularly debt-laden emerging economies.

Now, how do you think share markets are going to respond to this?

An attack of the glums would probably hit quite quickly.

Investors who cheered Trump’s tax cuts deregulation and stretched market valuations have been quietly digesting the implications of getting what they wished for:

An over-heated economy.

A massive increase in US government deficits and debt (with a consequent increase in the supply of bonds and another source of pressure for higher interest rates if the market is to absorb them)

A new round of inflation that forces the Fed to respond.

The above does not seem like a recipe for a continuation of last year’s bull market.

Neither would it lend itself to global economic growth and geopolitical stability.

Bonds are speaking; is anyone listening?

The environment is at the red end of risk.

Uncertainty has gripped markets - Trumps’ agenda seems to be entirely at odds with the anticipated economic effects of its implementation.

We will have to wait and see exactly what Trump’s actions are.

(THE MARKETS IN 1973 AND 2025 – DRAWING COMPARISONS)

January 13, 2025

Hello everyone

WEEK AHEAD CALENDAR

MONDAY 01/13

2:00 p.m. Treasury Budget (December)

6:30 p.m. Australia Consumer Confidence

Previous: -2%

TUESDAY 01/14

6:00 a.m. NFIB Small Business Index (December)

8:30 a.m. Producer Price Index (December)

Previous: 0.4%

Forecast: 0.3%

WEDNESDAY 01/15

8:30 a.m. Consumer Price Index (December)

8:30 a.m. Empire State Index (January)

11:00 a.m. New York Federal Reserve Bank President and CEO John Williams speaks at CBIA Economic Summit and Outlook 2025

Earnings:Citigroup, Goldman Sachs, Wells Fargo, JPMorgan Chase, BlackRock, Bank of New York Mellon

THURSDAY 01/16

2:00 a.m. UK GDP Growth

Previous: -0.1%

Forecast: 0.2%

8:30 a.m. Continuing Jobless Claims (1/4)

8:30 a.m. Export Price Index (December)

8:30 a.m. Import Price Index (December)

8:30 a.m. Initial Claims (1/11)

8:30 a.m. Philadelphia Fed Index (January)

8:30 a.m. Retail Sales (November)

10:00 a.m. Business Inventories (November)

10:00 a.m. NAHB Housing Market Index (January)

Earnings:J.B. Hunt Transport Services, Morgan Stanley, U.S. Bancorp, Bank of America, PNC Financial Services Group, M & T Bank, United Health Group

FRIDAY 01/17

2:00 a.m. UK Retail Sales

Previous: 0.2%

Forecast: 0.4%

8:30 a.m. Building Permits preliminary (December)

8:30 a.m. Housing Starts (December)

9:15 a.m. Capacity Utilization (December)

9:15 a.m. Industrial Production (December)

9:15 a.m. Manufacturing Production (December)

Earnings: State Street, Schlumberger, Fastenal, Citizens Financial Group, Regions Financial, Truist Financial, Huntington Bancshares

We had a scorching hot jobs report last Friday, which puts in doubt the path of rate cuts by the Fed.We know the probability of cuts was revised down from four to two this year, but there is now some head-scratching going on with many wondering if there will be any cuts at all. The notion of rate rises is also being tossed about.

So, with that in mind, the inflation reading this week will be of paramount importance to the market.The CPI and PPI will be watched closely by investors – we may find that we have to deal with pricing pressures for quite a long time.The December consumer price index is expected to rise 0.3% in the month and 2.8% in the year, according to consensus estimates from FactSet.That’s compared to respective increases of 0.3% and 2.7% in the previous report.

Our market is already at historically stretched valuations as we start the year at 22 times forward earnings, which means investors will have to rely on earnings growth to power the market this year.And this is where the real challenge lies – can companies negotiate through rising inflation, higher yields, a strong dollar, and deliver on expectations?

Big banks launch the earnings season this week.

Finally, we need to understand the consumer’s environment, and see if they are still spending, so retail sales data should be on your radar.

What has Donald Trump promised to do from Day One through to his first 100 days?

Lifting environmental restraints and expanding oil and gas exploration.

Cut in support for electric vehicles.

Close the border with Mexico.

Deport millions of undocumented migrants.

Wind back the Biden administration’s environmental programs.

Pardon peaceful rioters who stormed the Capitol in the 2021 insurrection.

End the war in Ukraine.

Suspend refugee admissions.

Ban “woke” inclusivity programs.

Cut back on government spending.

DRAWING PARALLELS BETWEEN 2025 AND THE EARLY SEVENTIES

Doug Kass has been a very successful fund manager over the long term.Recently, he has been comparing the state of the current market and the Wall Street of 50 years ago.

He states: “With the 10-year Treasury yield reaching multi-month highs, my baseline expectation is that January 2025 could represent an important top in stocks – much like it did 53 years ago in 1972.”

Let’s revisit 1972 for a minute.

Richard Nixon was President.

A gallon of gas costs 36 cents.

The median family income in the U.S. was $11,120.

The average individual income was just over $6000.

The highest-grossing film in 1972 was Francis Ford Coppola’s The Godfather.

Roberta Flack’s “The First Time Ever I Saw Your Face” was the top song.

Kass points out that the December 2024/January 2025 tops in the stock market could resemble the tops in the market in December 1972/January 1973.

In drawing the comparison between each period, Kass demonstrates that:

Both periods featured combative presidents – Richard Nixon in the past and incoming President-elect Donal Trump in the present.

In both periods, interest rates and inflation increased from the prior few decades, and public sector debt was climbing rapidly.

P/E [price to earnings ratio] was extremely elevated in both periods.

A top was completed in January 1973 – leading to a poor year for the S&P 500 Index.

Kass expects “an important market top, a down year for the averages…”

Let’s end on a positive note here as Kass explains that in 2025 he does like companies that will be helping to expand the utility grid and cloud computing.

MARKET UPDATE

S&P500

A hot jobs report sank the market on Friday.A close below the $5825/35 support area will be a bearish sign.Support at the base of the rising wedge ($5675 ~) may again trigger a good-sized bounce.Resistance = ~$5870/80

GOLD

Some movement in gold recently could continue to the upside, however, it is still believed that the topping process is not yet complete.So, you might use the upside movement to sell more calls (if you wish).Support is seen at around $2630/$2600.Resistance is seen around the $2690/$2630 area.

BITCOIN

Topping formation for a few months is taking place.After our $108,389 top, Bitcoin is ranging between support and resistance levels.Support around $91,000 may hold temporarily, however, a break there could lead to the mid $85,000 zone and even lower.Initial resistance is now around $97,500 and $102,000.

Firstly, I’m deeply sorry for anyone who has been affected by the L.A fires.Losing everything in a fire is traumatic; I do hope the community comes together to give comfort and people supporteach other during this devastating time.

The market is expressing a topping pattern.So, we would be wise to take some funds off the table.As I said in my Monday newsletter, there is a real possibility that we could expect movement towards $5000 and under in the S&P500.So, let’s bank some profits.

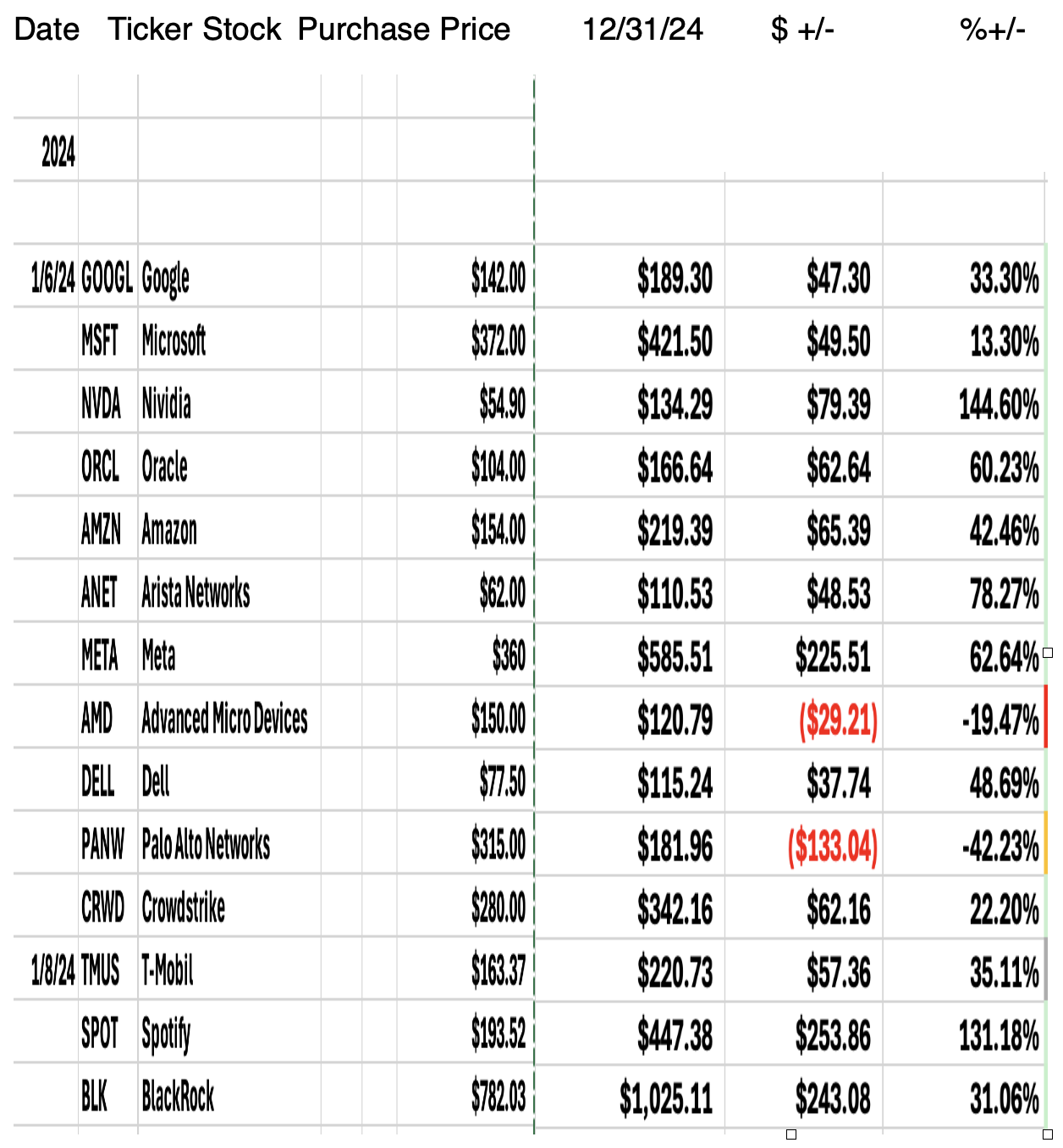

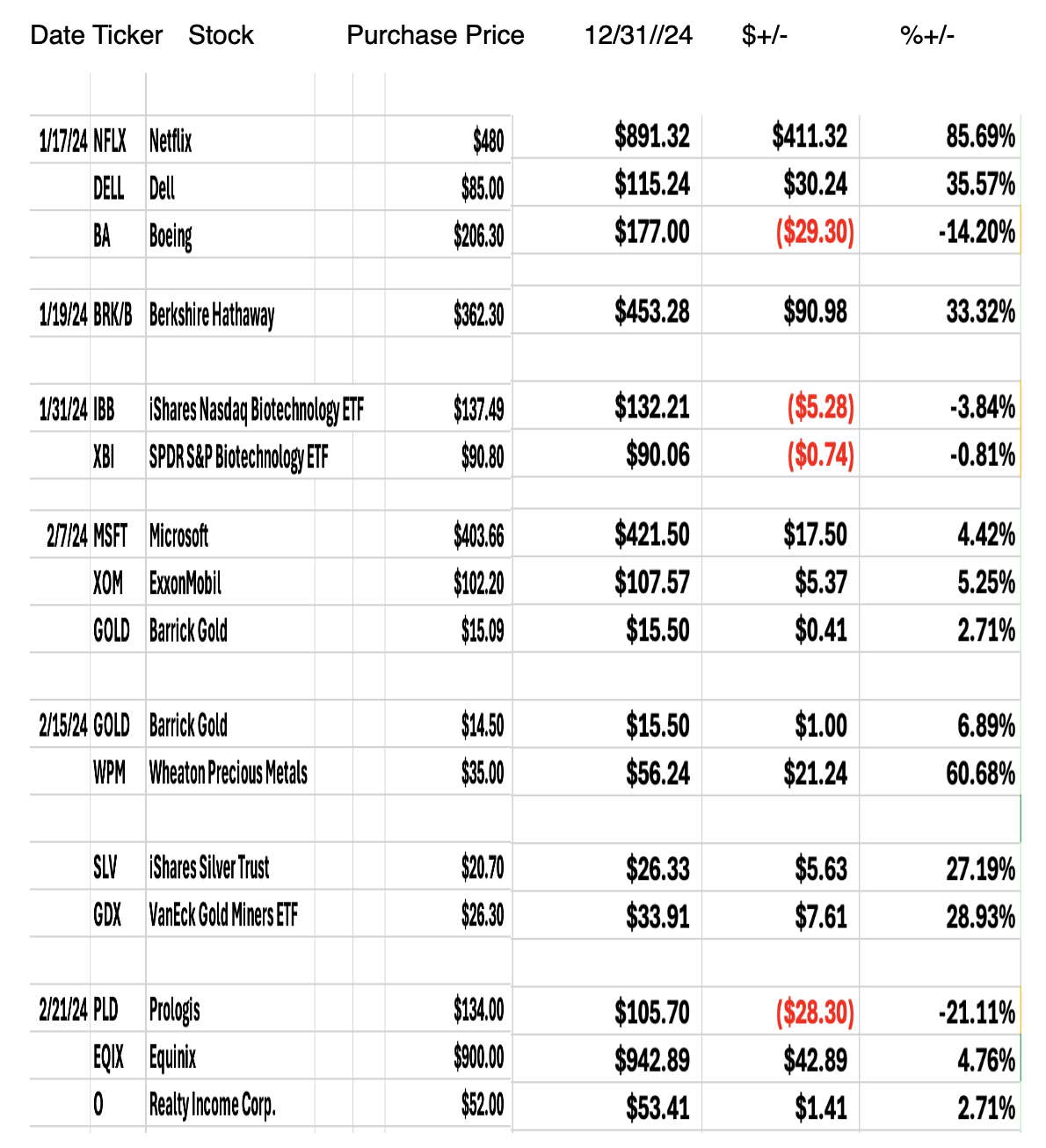

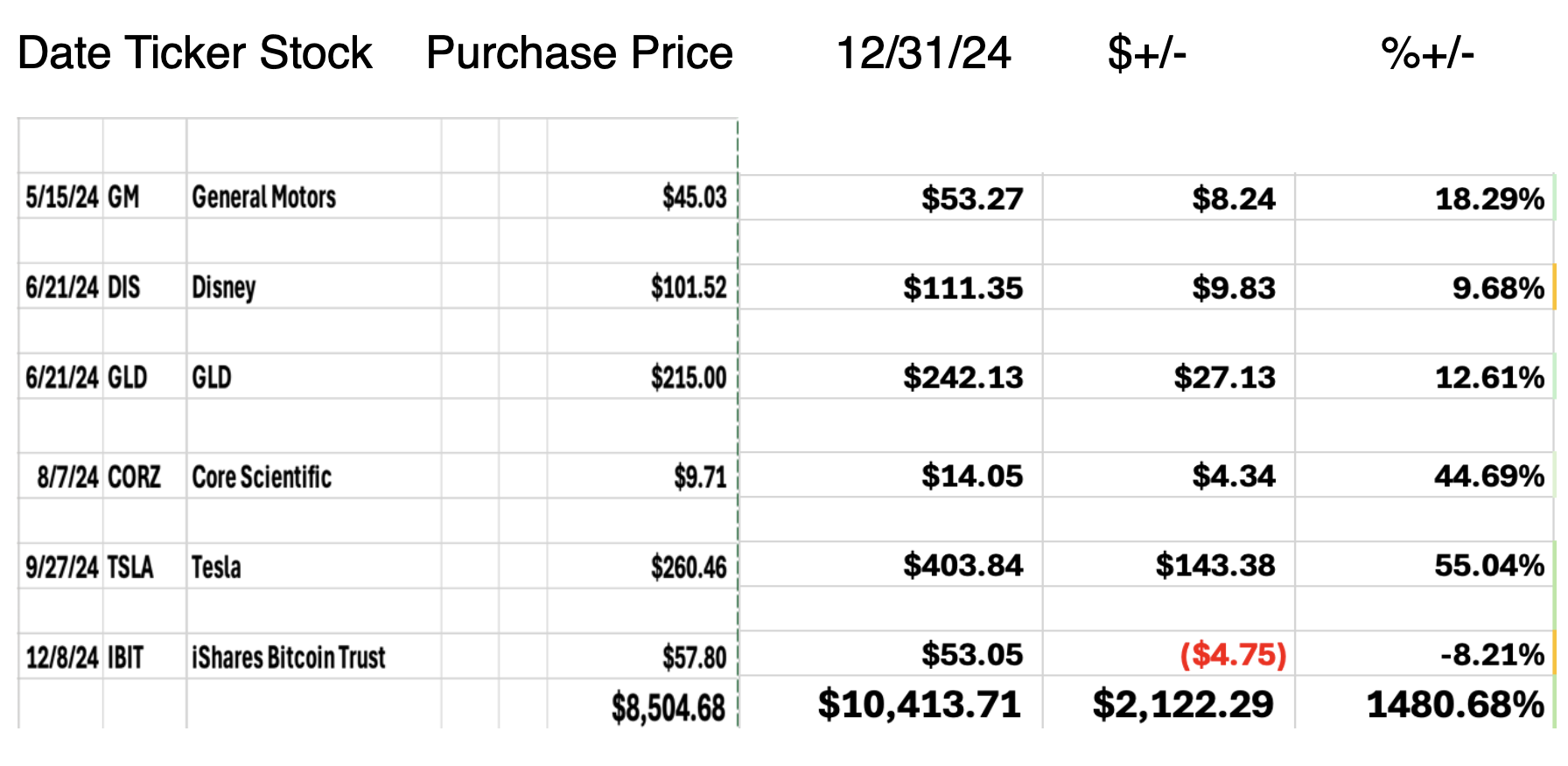

Below I’m showing our portfolio and our end-of-year performance.

On the left, I show the date, ticker symbol, stock, and purchase price, and on the right, I show the price of the stock on December 31, 2024, + the $ gain/loss and the % gain/loss for the year.

Energy was our worst-performing sector.We can expect further lightning bolt movement in oil followed by a low and then a move up.The timing of these moves is hard to nail down.

I have cut and pasted from my Excel spreadsheet, instead of sending the whole thing out to you.

So, if you had bought one stock in each of the above companies when I suggested, you would have been ahead by $2,122.29 or 1480% for the year.(Two people have checked these numbers besides me).

Let’s take some profits now on the following stocks:

On November 8, 2023, we bought Digital Ocean (DOCN) at $26.30.On January 8, 2024, the stock sits at $34.48.Sell the stock and take profits.

Profit = $8.18 OR 31.10%

On November 27, 2023, we bought Dell (DELL) at $75.00.

On January 6, 2024, we scaled in again at $77.50.

Again, on January 17, 2024, we scaled in at $85.00.

On January 8, 2024, the stock sits at $119.31.Sell the stock and take profits.

Profit = $75.00 -$119.31 = $44.31 OR 59.08%

Profit =$77.50 - $119.31 = $41.81 OR 53.94%

Profit = $85.00 -$119.31 = $34.31 OR 40.36%

If you bought any of the Home Builders: Lennar, Pulte Group, D. R. Horton, Toll Brothers, I advise you to sell out of them.Interest rates will stay on the high side.

On October 10, 2024, I presented a list of stocks where you could add weight.The Home Builders were part of this list and looked promising with the prospect of many more interest rate cuts.Now, however, that does not look likely to happen, so we need to cut this sector from our portfolio.On October 10, the stocks were at the following prices.On January 8, 2025, the stocks listed these prices.I advise to scale out on days when the market and these stocks show an uptick.

D.R. Horton $183.39 - $139.90

Lennar $178.20 - $133.54

Toll Brothers $149.07 - $127.03

Pulte Group $138.66 - $110.46

On April 3, 2024, we bought Taiwan Semiconductor (TSM) at $140.22.On January 8, 2024, it’s at $207.12

(This is a brief look into the work of Lawrence McDonald’s text How to Listen When MarketsSpeak:Risk, Myths, and Investment Opportunities in a Radically Reshaped Economy. We learn what some of his research shows, and this piece here is via his blog, The Bear Traps Report.

Over the last 250 years or so, all American political parties have played “games” at the closing stage of each administration.Take 2000, for instance, when the incoming George W. Bush team discovered that every keyboard in the White House and other administrative officers was missing the “W” key.

The outgoing Clinton staff had removed all the “W” keys to annoy the new administration after an extremely contentious election.

The damage was no big deal – around $15,000.

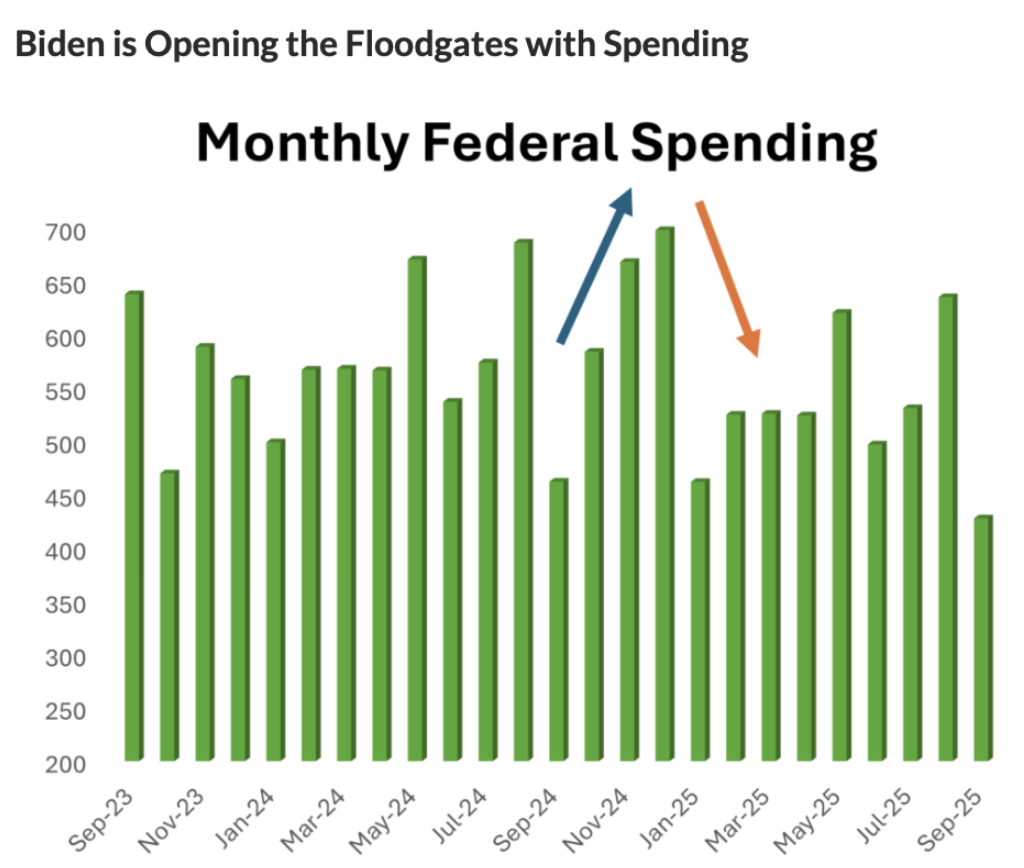

The outgoing Biden administration will be no different.But their mischievous acts may be a little more unpalatable.Under the existing budget, Bien is opening the floodgates with spending.

Spending for 2025 is expected to exceed $2 Tr by the time Biden leaves DC on January 20th.This is over 30% of the annual budget, and Trump will have to cut spending for the rest of the year to stay within the limits of the allocated budget.This could mean a notable slowdown in GDP growth in the first quarters of 2025.

The government’s fiscal year started on October 1st, and Biden could be on course to spend almost $2TR by the end of December and a deficit that may exceed $800bl (+60%y/y).

So, when Trump steps in on January 20th, he has three-quarters left of the government’s fiscal year; by then Biden has possibly spent more than 30% of the total allocated budget.

Lunatics – as Usual – on Capitol Hill

Congress, in its usual fashion, has failed to agree on the next budget, so the government is currently operating under a “continuing resolution” (CR). This continuing resolution means the government is allowed to spend the same amount of money they spent last year, which is $6.75TR. The government’s fiscal year started on October 1st, and Biden is on a run rate to spend almost $2TR by the end of December and a deficit that may exceed $800bl (+60% y/y). So, when Trump comes in on January 20th, he has three quarters left of the government’s fiscal year, but by then, Biden has spent more than 30% of the total allocated budget.This forces Trump to cut spending right off the bat. We estimate spending could drop by $500bl quarter over quarter, or 25% from Q4 to Q1. This is an estimate, and the timing of spending can change. But the fact is that Biden is emptying the coffers before Trump gets in. Every week, more money and weapons are sent to Ukraine, more subsidies are given to semiconductor makers to build plants in the US, and more government employees are hired.

US Yields Surge While Others Languish

Since September, US Yields have surged over 20% on Biden’s sugar high, while Canadian and German yields are down since then, Chinese yields have collapsed, and UK yields are only modestly above the September level.

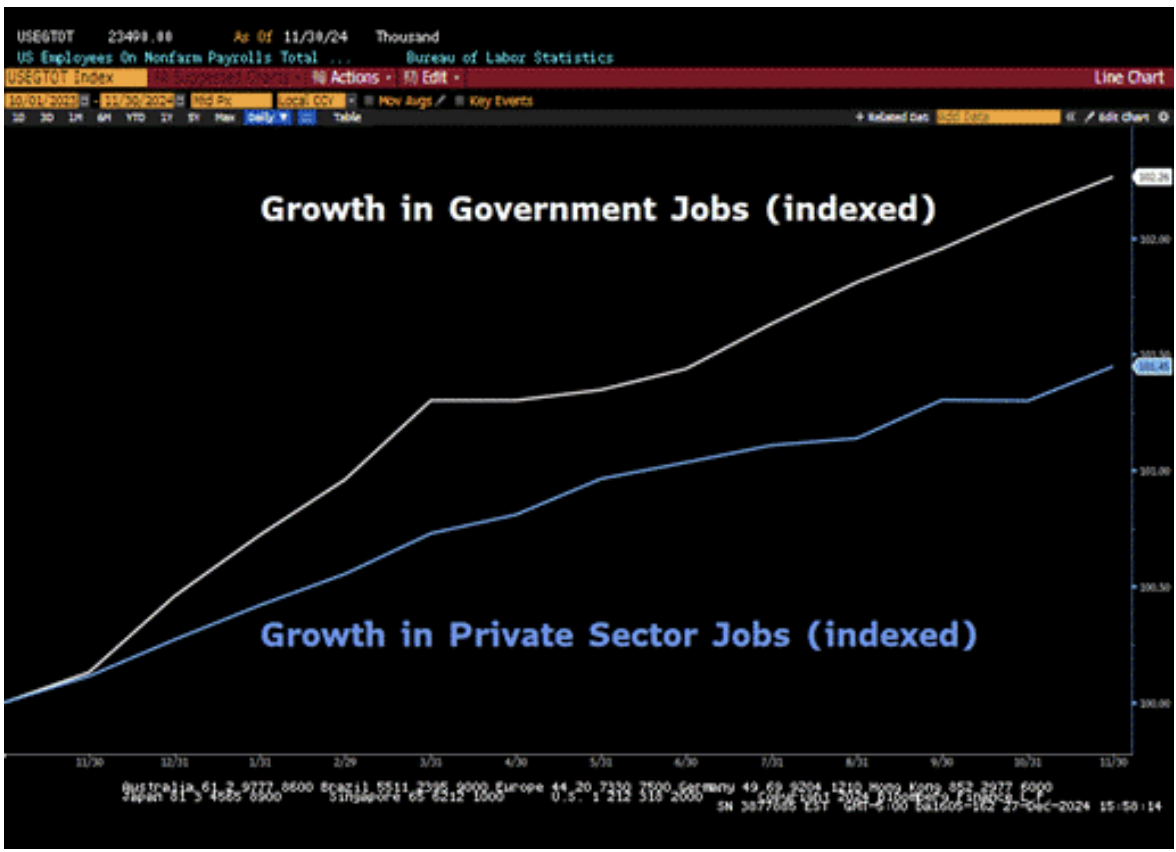

Government Job Growth Twice the Rate of the Private Sector

Private sector job growth has lagged government job growth significantly in the last year as the government keeps hiring people.

Why is this so Bad?

We believe that this spending deluge by Biden on his way out is partially to blame for the surge in bond yields in Q4. Some may say it’s because of Trump and his promised tax cuts, but the Republican House majority is so slim that it’s unclear how much of a fiscal stimulus Trump is actually able to get through Congress. Also, the incoming Senate majority leader Thune (R, SD) has said he will only get one bill through reconciliation in FY 2025 and another one in FY2026. His priority is on immigration and energy legislation, so a fiscal spending bill might not come until late 2025 or early 2026 if anything. But if yields are being pushed up by all this spending in Q4, then what will happen if spending falls back in early 2025? And what will happen to GDP growth? A $500bl drop in government spending from Q4 to Q1 is the equivalent of 1.7ppt of growth. So, if Q4 nominal growth comes in at 5.7% annualized, this could drop to 4% in Q1 if government spending slows down accordingly.

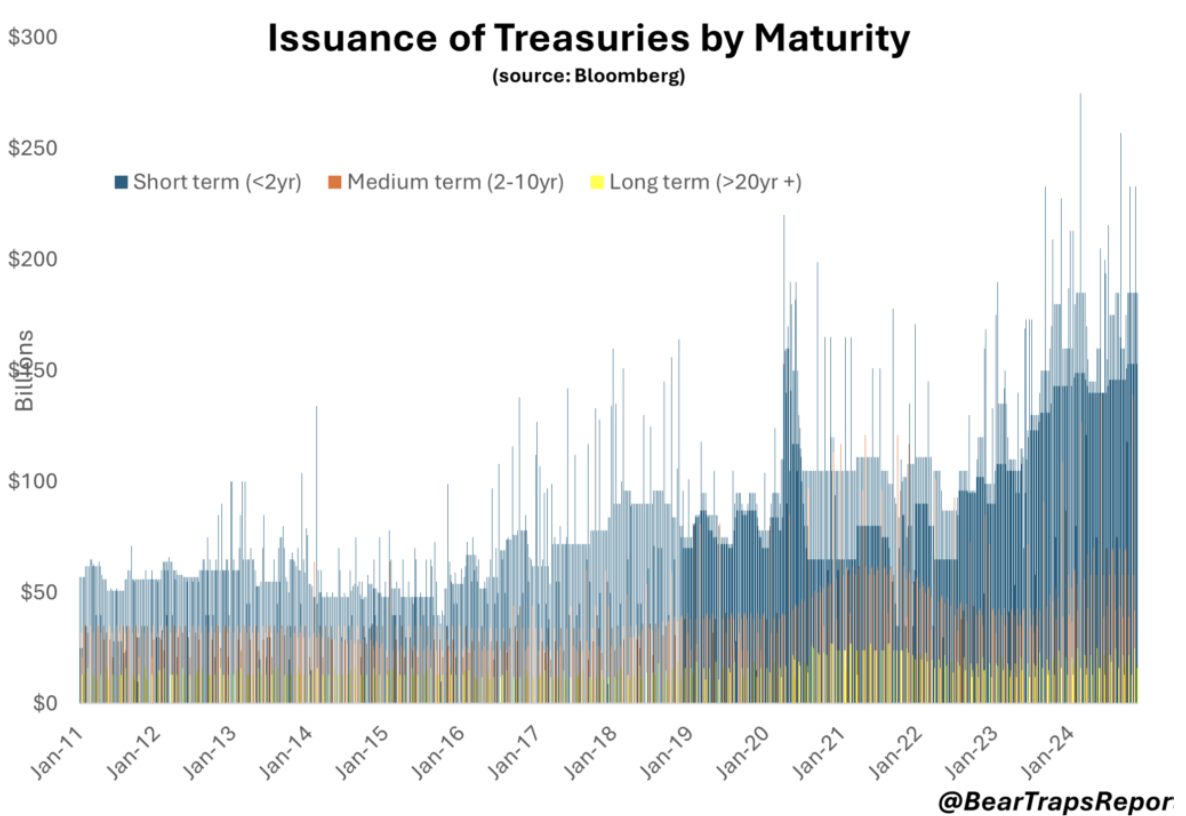

Treasury’s Reliance on Short-Term Debt Exploded in Recent Years

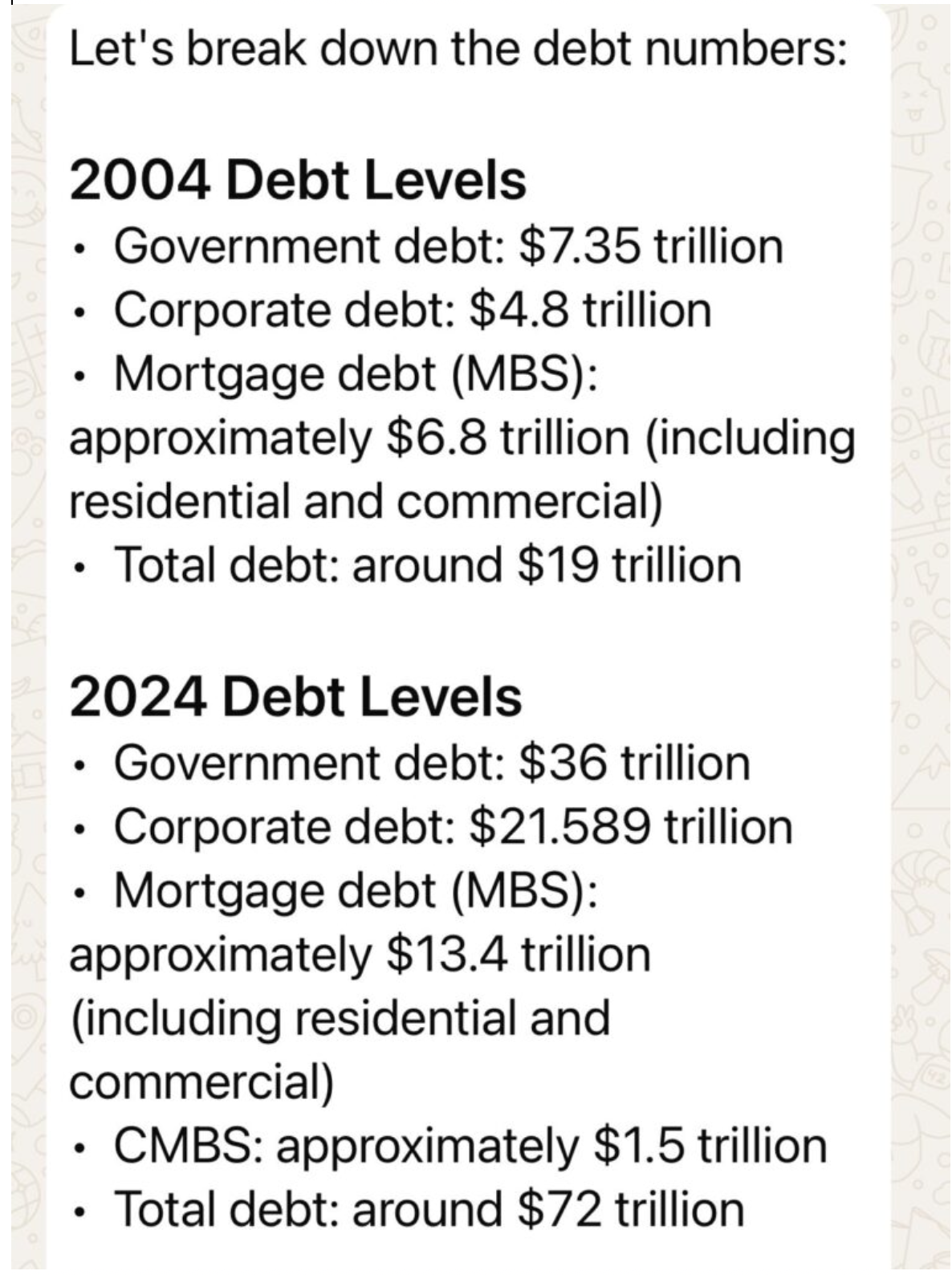

Election Rigging? We are witnessing a Covid era like spending in 2024 without a pandemic. The Treasury Department has come to rely on short-term bills to fund the government. But with $36Tr of debt, the Treasury has to issue bills almost every dayto keep funding the government and to refund maturing debt.

*CBO data, Bloomberg. The average weighted coupon on the U.S. debt load is about 2.7% vs. over 4.5% for 10-year U.S. Treasuries. As bonds mature, they get refinanced at much higher yields.

$10Tr of Debt Refinancing Next Year

In 2024 Treasury faced around $10Tr of maturing debt. To refinance this debt, it issued a whopping $26Tr of bills and bonds. More than 84% of that paper was short-term bills with a maturity of 6 months or less. Treasury keeps re-issuing bills with a maturity of 4 to 8 weeks or 3,4 to 6 months, which are the most popular maturities in a continuing, ever-increasing roll down of the debt, day after day, month after month.

Apple Long-Term Bonds and Interest Rates

ALERT– By issuing nearly a colossal load of extremely short-term bills, Janet Yellen succeeded in suppressing bond volatility in an election year and, in our view, strategically placing that bond market volatility into 2025 after the election. You can “why” see above, she wanted LESS long-term paper in circulation markets in the election year. Now, in 2025 – this paper has to be rolled over and termed out into longer-dated bonds. The USA is behaving like a financially trapped emerging market country. Living on the “front end” of the yield curve is a VERY dangerous game.The Apple AAPL 2.55% bonds due 2060 are trading down at 57 cents on the dollar. If long-term bond yields go to 6%, take a guess where this bond will trade. Near 47 cents on the dollar? Now think of the trillions of USD loans issued in 2017-2021 on bank balance (commercial real estate, mortgages, corporate debt outstanding). Losses are in the trillions of dollars with higher incoming interest rates.

Interest Rates UP – Bond Prices DOWN

Never, ever forget that 6% today is equivalent to the destructive capacity of 10% twenty years ago. Interest rates up, mean bond prices down. A 1% move in interest rates higher today is an entirely different, far more lethalequation.

Incoming Stress Points

In 2025 the U.S. Treasury faces $9.6Tr of maturities in their so-called publicly held debt. In Q1 alone — the government faces $5.58Tr of maturities (bonds coming due, redemption), but 86% of those are short-term bills that the Treasury department rolls over into new 4-week, 8-week, 3,4, or 6-month bills, among others. As a result, almost daily bill auctions are coming to a theater near you, as the Treasury Department mindlessly keeps pushing new paper into the market to pay back the colossal amount of maturing debt.

Is There Any Reason to Buy Treasuries?

The new Treasury department under Scott Bessent may reduce bill issuance a bit and increase coupon paying issuance, just to alleviate some of the pressure on the bills market and extend the duration of outstanding US debt. Now that the big slush fund that bought all these bills, the so-called Reverse Repo Facility (RRP), is close to being depleted, it will be harder to sell all that short-term paper. In addition, Goldman Sachs expects that the Federal Reserve will stop the run-off of treasuries from its balance sheet by the end of January and begin buying treasuries again with the proceeds of the maturing MBS on its balance sheet. As such, the Fed becomes a modest buyer of treasuries next year, which allows the Treasury to increase coupon issuance without disrupting the long end.

One big bullish catalyst for treasuries would be a regulatory change to exempt treasuries from the Supplemental Leverage Ratio (SLR). It is unclear if and when this would be implemented, although Bessent was hinting at regulatory relief for banks to boost banks’ treasury holdings. Exempting treasuries allows banks to hold more Treasuries on their balance sheets without needing to hold additional capital against them, freeing up the capacity for banks to participate more actively in the Treasury market. It’s unclear how much treasury demand that would create, but in 2021 when the temporary SLR exemption was reinstated after COVID, prime dealers reduced their Treasury holdings from $250bl to $125bl in 2 months. A change in the SLR ratio may come but is going to take months before the rules are changed. A phase-out of QT for treasuries would be a more immediate, albeit more modest, relief for the bond market. According to this timeline, the Fed will end up buying $100bl of treasuries in 2025, a big change from the $500bl of treasury sales in 2024.

We have been very critical of Yellen’s term at the Treasury, but upon some further reflection, we think it’s really the case that Yellen’s only real issue was acting in the short-term interests of her boss and her party as opposed to thinking longer-term about how the government finances itself on a sustainable basis.

Her decision to fund the government with T-bills over duration securities and violate long-standing Treasury Department “norms” was incredibly short-sighted, but as someone who works for the President, ORDERS to follow.

Many have been super critical of her for these decisions because she should know what they would lead to and how really what she (and Powell together) has done is favor asset owners and the wealthy over everyone else in America, exacerbating wealth inequality to precarious levels in this country while still not bringing inflation back down to target. So ultimately, her decisions got her team knocked out of office anyway.

Looking forward, though, the issue is that there is no one in the government who is really thinking about and acting on behalf of the longer-term interests of the country when it comes to how much debt we are raising and how we are financing the government. The myopia about these decisions to get the existing political party in control through the next election is incredibly concerning.

The Fed has said this is not their lane; however, they are elected to 14-year terms and are supposed to be above politics. There are things they could have done to offset the politicization of the Treasury. They chose not to, they continue to protect asset holders and the Treasury market, decisions that really just make them become political as well. They could have better neutralized Treasury’s political decisions through more active QT, actually selling securities instead of just rolling them off, not adding to their duration holdings such that the weighted average maturity (WAM) of their positions is longer than Treasury’s own WAM. Powell’s Fed needs to be getting way more criticism than they are currently about these decisions which have made it harder to bring inflation down for the average American.

So, if the Treasury is not going to think long-term and the Fed is not going to either (the Fed actually is complicit because they don’t allow any real treasury market dysfunction to exist, which would be the way to deal with these long-term issues by having the market/bond vigilantes do their thing), then who will? This is a problem, the bond market is starting to figure it out, term premiums are starting to normalize, and the new administration will have to make some big decisions early on in their term.

Maybe @elonmusk and @DOGE can look into this as well. Someone has to!

QI CORNER

NVIDIA just dropped Project DIGITS, a $3,000 personal AI supercomputer that looks like a Mac Mini but packs 1,000x the power of your average laptop

Powered by the Nvidia GB10 Superchip and based on the NVIDIA Grace Blackwell architecture, this supercomputer can run AI models with up to 200 billion parameters.

The crazy part? You can link two units to handle 405B parameter models.

From this perspective, OpenAI's GPT-4o is around 200B parameters while Grok-1 by xAI has 314B parameters.

Jensen Huang is single-handedly bringing data center-class AI computing to individual users.

(IN 2024, THE TRADITIONAL SANTA RALLY DIDN’T APPEAR, SO WHAT DOES 2025 AND BEYOND LOOK LIKE?)

January 6, 2025

Hello everyone

Happy New Year!Wishing you all good things for 2025.

I’m back on deck for a new year.I hope you are all well-rested and ready for another year navigating the markets.

So, what can we expect for 2025?

In Australia, economists indicate that 2025 offers no solutions to the economic problems of the past year.However, we can expect an easing of interest rates and inflation.

China’s sluggish economy has the potential to weigh down Australia.

US President-elect Donald Trump will be inaugurated for a second term later in January, with the full extent of his promised tariffs a key factor for the economic outlook.

He’s pledged the mass deportations of migrant workers and a huge reduction in government regulation of different industries.

For the economy, the biggest impact will likely be from tariffs imposed on goods from foreign countries, including steep taxes on Mexico, Canada, and China.

It is yet unknown whether Trump will follow through on the announced rate of tariffs on these countries.

(DOGE) leader Elon Musk could trim the fat in government departments, making the system work more efficiently.

Unemployment begins to rise in 2025.

Interest rates are finally cut in Australia in the first half of the year.

In the last two decades, in Australia, migration increased to about 60 percent of growth in an average year and natural increases were the other proportion – about 40 percent.

Migration is now up to 83 percent of our growth … so, record population increases in Australia.

Demographer, Mark McCrindle, believes Australia’s population could reach 50 million by the 2050’s.

He also points out, that Australia is not keeping up with a heightened population demand on critical infrastructure such as housing.

McCrindle argues that the “population growth is greater than the built environment growth and that’s really what’s driving the housing affordability challenges, that demand is exceeding supply.”

So, as you can imagine, no relief yet on Australia’s housing crisis.(It is a similar story in the U.S.)

People will continue to move to regional areas away from the big cities – Sydney & Melbourne – to look for affordable living options with flexible working conditions.

Globally, McCrindle predicts the population will grow as high as 10 billion by the 2080’s, before stabilizing.He said the world was already experiencing increased rates of population contraction – meaning fewer people are being born annually – and this trend was likely to continue.

We will continue to see technological innovations.AI technology is on our doorstep, but Australians appear to be slow to take up new technologies.An attitude of distrust seems to be an issue.The AI “big brother” lens is not palatable for everyone.Nevertheless, AI will no doubt increase efficiency and cut costs in many sectors & industries, which will likely be passed on to the consumer. The chip industry and the main heavyweights will continue to do well as demand will not go away.Quantum computing is not far away.

Geopolitical conflicts have been increasing in intensity in the last few years.Strategic Analysis Australia founder, Michael Shoebridge, argues there is a credible scenario “There could be a global war this decade and that can be because of the rise of nationalism we’re seeing, particularly in places like Russia and China.”

Shoebridge comments that just like before World War I, the world in 2025 is witnessing a “revolution in warfare” with newly innovated weaponry, and leaders like Russian President Vladimir Putin, Chinese President Xi Jinping, and the United States president-elect Donald Trump blindly moving closer to a full-scale war.

S&P500

2024 was a stellar year for stocks, but in 2025 Equities may pause for a period this year before another major rally takes place.

Over a period of 6-9 months, the S&P500 could possibly fall towards $4,800, or even lower, but will then rally in the final part of the year.2026 and 2027 could be good years for the market.

If the markets do take the bear path, FANG stocks could fall 20% or more.

Of course, these predictions depend, somewhat, on what Donald Trump actually does when he enters the White House.If nothing changes, then a rally could well take place, and stocks could rise into nosebleed territory.Time will tell.

PRECIOUS METALS

Gold and silver will remain financial safe havens.As confidence in fiat currencies erodes amidst economic instability, gold, silver, and cryptocurrencies are emerging as pillars of financial security.With geopolitical tensions rising, central banks hoarding reserves, and inflation fears mounting, many analysts project gold could rally toward $3,500 per ounce – and possibly higher.Unlike fiat money, gold isn’t tied to the whims of governments or central banks, making it a trusted store of value during crises.

I see gold and silver continuing to range in the first instance this year and then, possibly, gradually moving lower towards $2,400 and even $2,200 is possible.In the second half of the year, we could see a rally towards $3,000.Late last year I suggested selling calls on gold and silver stocks.At the moment this is still a good play.

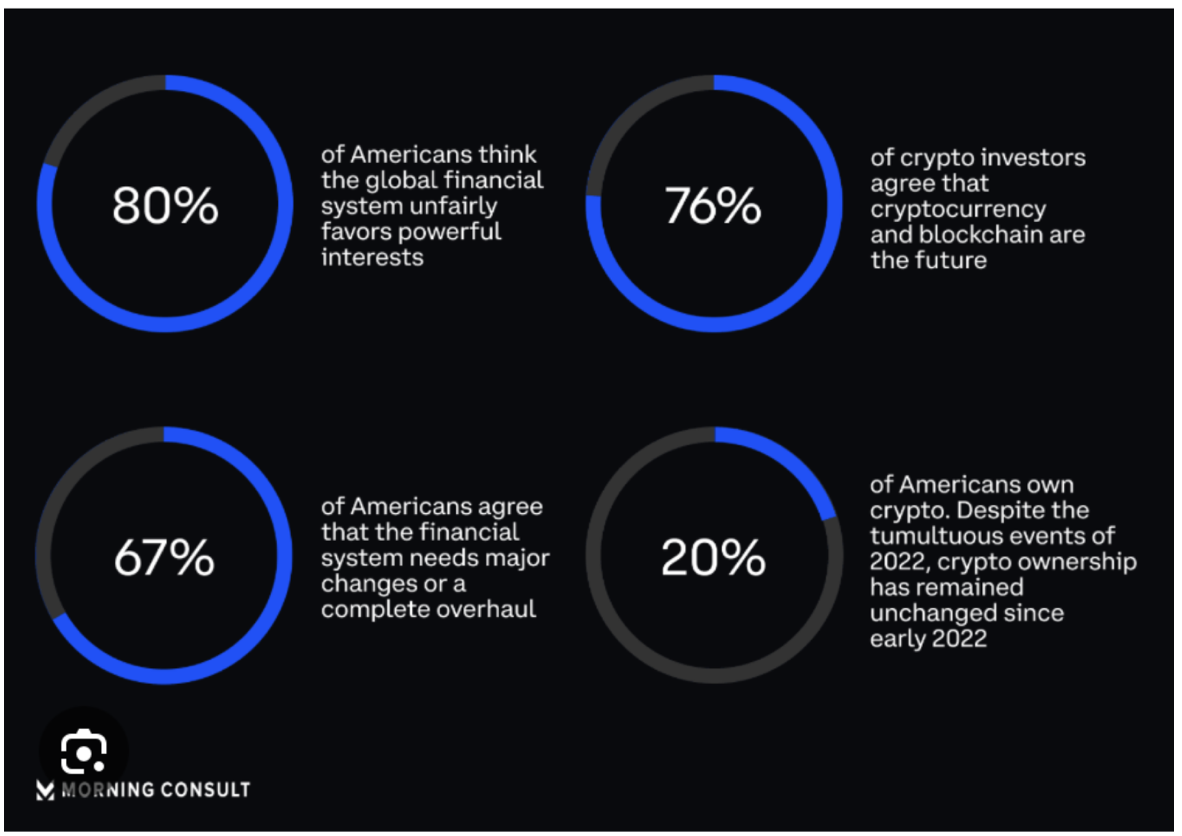

THE CRYPTO REVOLUTION

Crypto should shine this year.The election of Donald Trump has shaken up the markets, particularly in the cryptocurrency space.His administration has swiftly installed crypto-friendly leaders in key positions, including Vice President JD Vance, National Security Advisor Michael Waltz, Commerce Secretary Howard Lutnick, Treasury Secretary Scott Bessent, SEC Chairman Paul Atkins, FDIC Chair Jelena McWilliams, Dept of Govt Efficiency (DOGE) leader Elon Mush, and HHS Secretary RFK Jr., who has become the face of the MAHA (Make America Healthy Again) movement. These appointments signal the end of anti-crypto policies while positioning Bitcoin and other digital assets as strategic components of the U.S. economy.

Bitcoin is expected to rally well this year.With increasing institutional adoption, corporate treasuries diversifying into Bitcoin, and even nation-states taking on board the idea, Bitcoin could easily reach $150,000 and beyond this year.Some are even predicting $250,000 by December.

Why is this happening now?

Many factors:

Greater regulatory clarity, the launch of Bitcoin exchange-traded products (ETPs), and institutional players continuing to pour large amounts of capital into Bitcoin.These developments not only seem to set Bitcoin’s position as a store of value but signal that it’s well on its way to becoming a dominant force in the global economy.

Bitcoin isn’t the only crypto that will rally this year.Investors and/or traders should also be looking at Ethereum.This coin has a valuable ecosystem of decentralized applications (d’Apps) and smart contracts.The introduction of Ethereum 2.0, which promises faster transactions and a more energy-efficient proof-of-stake mechanism, combined with Ethereum’s role at the heart of decentralized finance (DeFi), may well incentivise mass adoption.With more institutions and businesses adopting Ethereum-based platforms, the token could rally strongly, riding the wave of growing trust in blockchain technology.There is potential for Ethereum to rally towards $8000.

Another coin that could have a bright future is Ripple.Some experts are predicting that XRP could hit $10 in 2025. Faster, cheaper transactions offer banks and corporations a more efficient way to process payments across borders, making it a preferred choice for many in the financial world.Further igniting its popularity is the endorsement by high-profile figures like Elon Musk, who recently mentioned XRP in the context of his support for decentralized technologies. Musk’s influence could boost XRP’s visibility and attract new investors and institutional partners.As blockchain technology continues to reshape the global financial landscape, Ripple’s XRP could become the backbone of cross-border payments, setting its place as a key player in the future of global finance.

Utility coins, too, are gaining acceptance and popularity.These coins go beyond mere speculations, offering real-world value by supporting initiatives and candidates committed to preserving liberty and individual rights.For example, USA Unity Coin (UUC) empowers Americans to back pro-freedom political leaders while participating in a decentralized financial ecosystem.Coins like UUC are providing a unique opportunity to drive change.UUC, in particular, is on a mission to safeguard the principles of freedom in the digital age.

ENERGY

Energy was one of the worst-performing sectors last year.Will it be the same this year?Much depends on supply and demand, and the ongoing conflicts around the world.

Geopolitical risks threaten investment, environmental regulations, and infrastructure.

In 2025 oil prices could keep ranging for a period before the market finds a low and a bullish move begins.

Hold on to traditional energy stocks like (XOM)Exon Mobil, (CVX) Chevron, and (OXY)Occidental Petroleum.They should do well in the future.

By 2030, the use of renewables will probably increase by over 430%.Nuclear energy and hydroelectricity will expand by 54.5% and 48.5% respectively.

So, nuclear energy stocks should definitely be on your list.Look at (CCJ) Cameco Corp. (VST) Vistra Energy (a good buy now- scale in), (CEG) Constellation Energy, (SMR) Nu-Scale Power Corporation (A good buy now –scale in)

Santa didn’t deliver at the close of 2024

In contrast to what had been a very strong 2024 performance, the year ended without any fanfare at all.The S&P500 rose more than 23% last year but ran out of puff at year's end.Does the absence of a Santa rally mean a lacklustre market or a period of underperformance lies ahead for stocks?Some analysts believe the returns may not be as robust as in years when we did enjoy a Santa rally. On average then, we can expect around a 6.5% return.At any rate, January usually sets the tone for the rest of the year, so we need to take note and see what markets are telling us.History reminds us that when January is positive, the S&P500 averages a 6.9% gain on a six-month forward basis.When it’s negative, the index falls 0.6%.

The December jobs report is released this Friday.And with inflation data released later this month, we could get a much clearer picture of the path of interest rates going forward.A slowdown in job growth is expected.This week will be a good test for the dollar, with employment statistics and Fed speeches.

WEEK AHEAD CALENDAR

Monday Jan. 6

9:45 a.m. PMI Composite final (December)

9:45 a.m. S&P PMI Services final (December)

10:00 a.m. Durable Orders final (November)

10:00 a.m. Factory Orders (November)

Tuesday Jan.7

8:30 a.m. Trade Balance (November)

10:00 a.m. ISM Services PMI (December)

10:00 a.m. JOLTS Job Openings (November)

9:00 a.m. Euro Area Inflation Rate

Previous:2.2%

Forecast: 2.4%

Wednesday Jan. 8

8:15 a.m. ADP Employment Survey (December)

8:30 a.m. Jobless Claims (week ending 12/28)

2:00 p.m. FOMC Minutes

3:00 p.m. Consumer Credit (November)

Thursday Jan 9

10:00 a.m. Wholesale Inventories final (November)

NYSE is closed to mourn the death of President Jimmy Carter.

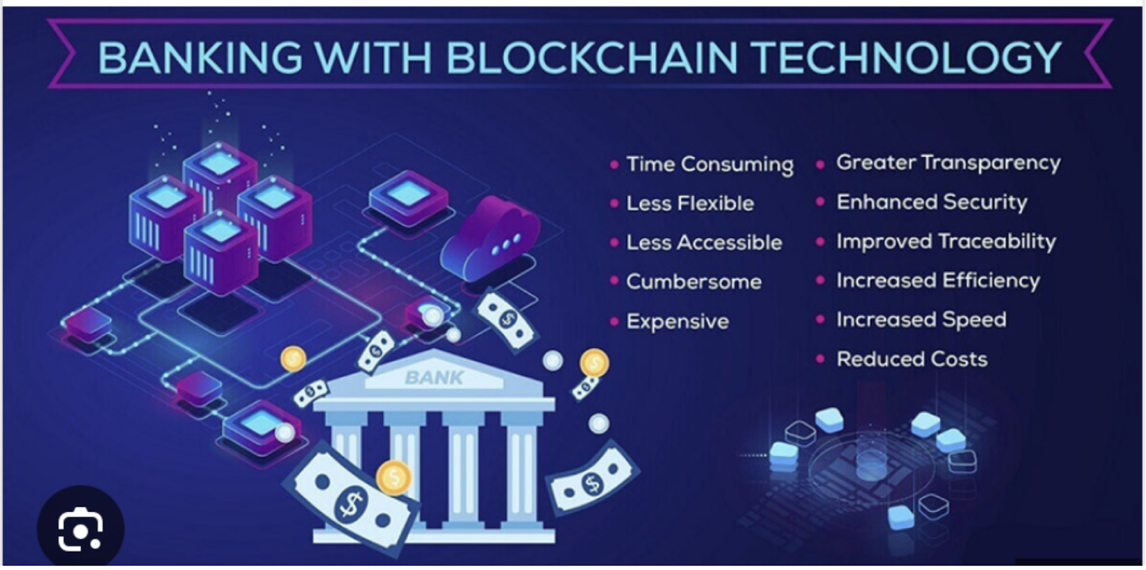

(THE GLOBAL FINANCIAL SYSTEM COULD BE REVOLUTIONIZED WITHIN THE NEXT DECADE)

January 3, 2025

Hello everyone,

In the NYSE, investors make upwards of 1 billion trades per day. Many of those trades appear to happen in milliseconds, except when you investigate further, that’s not the reality.

Trades on Wall Street take days to settle, and lots of people to make them happen. Take market makers, for example. They are the middlemen handling all those trades on Wall Street, and the top 5% of market makers handle nearly 30% of all trades. The fact is these intermediaries help with volatility, but they create a gap between buyers and sellers in the markets, and there are a lot of gaps in the financial system (which are beyond our control.)

Have you ever noticed how long some bank transfers take?

Some of the big banks think they may have a solution. JP Morgan, Citibank, and Goldman Sachs want to push the financial system into the next generation and to do that, they need to borrow a tool from crypto – blockchain. Presently all large-scale global financial infrastructure is highly warehoused or functions through different silos. In other words, money moves on one set of rails, assets move on a different set of rails. They operate independently, and information cannot be shared because of system limitations.

But being able to move money 24/7 365 is what we are moving towards.

These banks believe it could become a 5 trillion-dollar industry. In other words, we could see 5 trillion in combined tokenized asset-trading volume by 2030.

Why do these big banks think blockchain can turbo-charge the financial system?

Wall Street still operates in T+2. Trade + two days. That’s how long it takes for the standard securities settlement – for cash and assets to change hands. So, for instance, if you sell some stock on Tuesday, the cash won’t hit your bank until Friday.

Electronic trading and modern payment processing have accelerated the global financial system to move assets much faster. You don’t have to be an investment banker to feel the lag in the financial system. ACH transfers, credit card refunds, and all kinds of money that move in our economy take time to go from one person to another. Part of the slowness is how many steps and people are involved. On Wall Street, for example, brokers help set up a transaction, and they can charge a commission. Then market makers connect brokers to the assets they are trying to buy or sell. They charge a fee, too, on the difference or spread of the asking price of an asset and what someone is willing to pay. Very large transactions will need to go through even more steps for security and fraud prevention.

Some big banks are hoping that tokenization on blockchains can streamline the process of trading assets and maybe make it cheaper. It would revolutionize and rewrite financial market infrastructure.

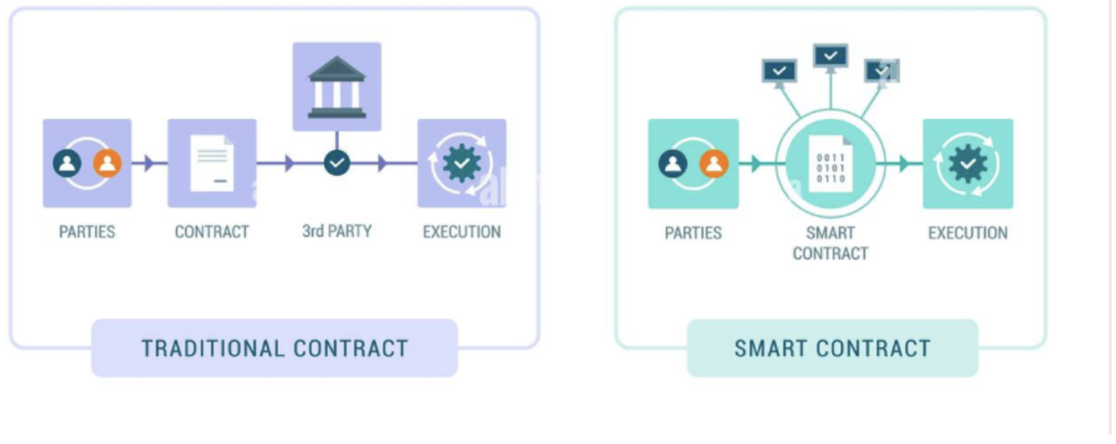

To understand how tokenization works, we need to talk about ownership in the digital era. Right now, it’s hard to transfer ownership of real-world items over the web.

We all know that you can buy a car through an online marketplace, but the title that proves your ownership of this car only arrives in the mail a few weeks later. Inefficient in the modern world, wouldn’t you say? In the hope of bringing ownership online, developers are creating tokens that represent real-world items. You can do this with any kind of asset: stocks, bonds, or a token that could represent ownership of a building or a car. Banks backing this believe that it may create new investments altogether, and that’s why they are putting their money behind it. For example, JPMorgan has Onyx, a blockchain platform they launched in 2020. In the short time since then, it’s handled 700 billion in short-term loans through its private blockchain. JPMorgan describes it as a “killer app” for the future of finance. Larry Fink, the CEO of BlackRock, called digital asset innovation and tokenization the next generation for markets.

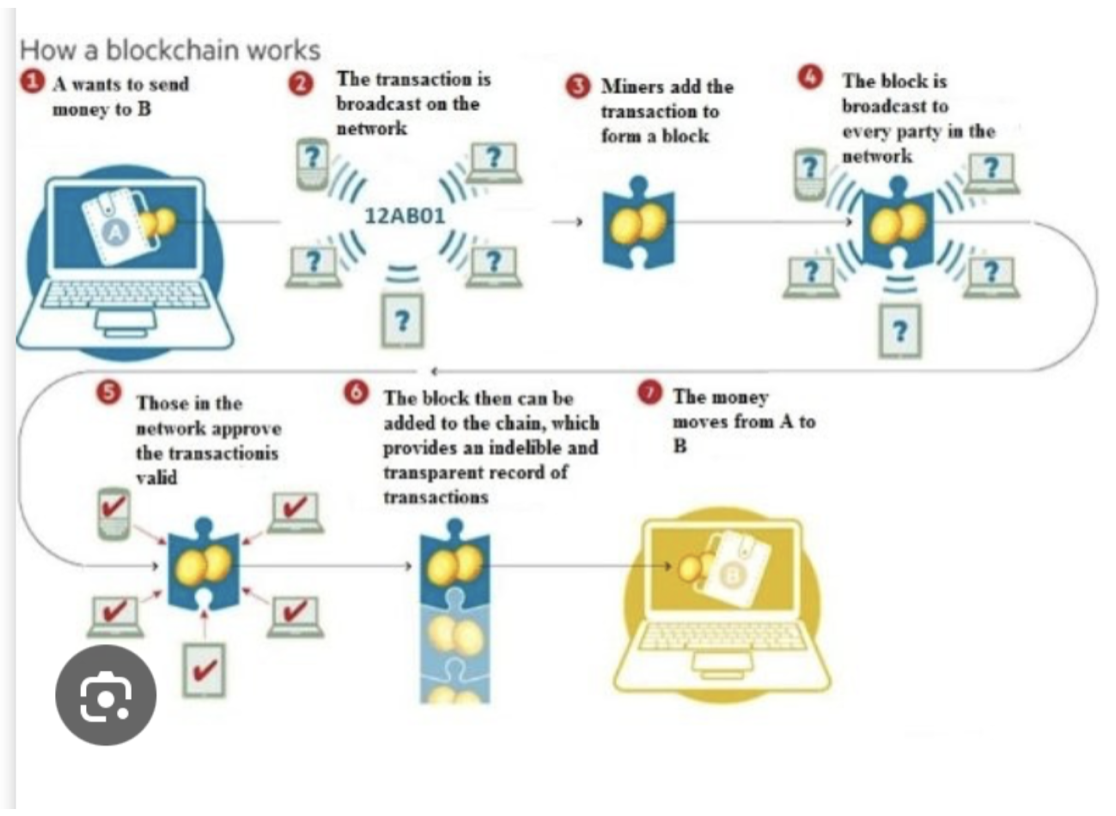

A blockchain is basically a database of all the transactions. There are many copies of the database, which helps to keep it secure. Each block is cryptographically signed so that any tampering is immediately evident. Additionally, you have a consensus mechanism to control how you update that database.

If technology provides you with the capability to use one rail line to transfer value, assets, and information, a lot of the inefficiencies and friction that exist in the regular financial infrastructure start to disappear.

Blockchains are meant to be transparent, cutting down the need for intermediaries that could charge fees or the need for extra due diligence. Proponents say it could enable P2P transactions across many parts of the economy.

In addition, this technology would allow for brand new forms of ownership, like splitting, fractionalizing ownership of property through real estate tokens, or tokenized deposits in bank accounts to allow for quick transfer of money between people using P2P transactions.

The IMF said in February that tokenising stocks and bonds could cut trading costs but requires the money paying for those assets to be tokenised as well, which would lead banks to make tokenised cheque accounts for faster payments.

The global financial system is one of the most regulated systems in the world and making any changes will be slow going. There will be a gradual movement forward in small steps.

Citibank has recently introduced Citi Token Services, which is a new blockchain-based service that will transform how institutional clients deposit and trade assets. In the evolving world of blockchains and smart contracts, Citibank has enhanced its products and services, including digital money, trade, securities, custody, asset servicing, and collateral mobility.

(THE HOUSING CRISIS IN YOUR FUTURE IS BROUGHT TO YOU BY CLIMATE CHANGE)

December 30, 2024

Hello everyone,

Most of us know about the changing climate. But few of us realize the implications of these changes on housing over the next 30 years and beyond.

We know about interest rates and the cost of housing, but what about the relationship between climate and the cost of housing?

It’s another crisis which is going to spread its tentacles worldwide. No country will escape.

Dave Burt, CEO of investment research firm DeltaTerra Capital, believes an overlooked and unpriced climate risk could see a repeat of a financial crisis in housing, albeit on a smaller scale in relation to the 2008 crisis. But still, it’s a damaging real threat to exposed communities.

Dave Burt was among the few skeptics who recognized the housing market was on the brink of collapse in 2007. He helped two of the protagonists of Michael Lewis’ bestselling book “The Big Short” bet against the mortgage market in the lead-up to the 2008 global financial crisis. As it turned out, they were right and were estimated to have made millions.

Now, Burt believes an overlooked climate risk could see history repeating itself.

Burt argues that DeltaTerra Capital’s research suggests that 20% of U.S. homes have “meaningful exposure” to a mispricing issue because of flood risk. If realized, he warned the fallout could resemble the extraordinary correction seen during the global financial crisis.

Even though he says that it could be a quarter the size and magnitude of the GFC, it still would be very damaging to exposed communities. Burt argues that there are cracks starting to appear in terms of the cost of insurance. Think about Hurricane Ian in Florida, for instance. The recovery here was an issue, particularly because this storm surge exposed a flood insurance nightmare for homeowners. We can also think about the people in Lismore, Australia, where the residents have endured about three major floods in 18 months. Some residents have left, never to return. Others have offered their house to the market for around 200k. The only way people will be able to live in these areas again is if the houses are built on stilts, if the community is relocated, or if major feats of engineering are undertaken to protect the town.

I would argue that most people do not lose a lot of sleep over the climate crisis in relation to their portfolio. But, a recent study has warned the U.S. housing market could be overvalued by around $200 billion due to unpriced flood risks.

This analysis was published in mid-February in the journal Nature Climate Change. Authored by researchers from the Environmental Defence Fund, the First Street Foundation, and the U.S. Federal Reserve, among others, the study modeled property-level changes in flood risk across the U.S. over the next three decades and warned that low-income households were particularly vulnerable to home value devaluation.

Jeremy Porter, head of climate implications at the First Street Foundation, said it is a huge concern because climate risk is not being priced into the housing market. He goes on to say that the costs now or the valuation of homes don’t consider the realization of that actual flood risk, and that’s not taking into account that there seems to be a huge amount of overvaluation attached to properties across the country.

Insufficient climate risk information when purchasing a home poses a significant financial hazard, as households could lose a large proportion of their property value overnight.

Eventually, Burt argues, there is going to be some sort of national tipping point where there is some type of bubble that bursts.

Presently, the study said that nearly 15 million U.S. properties face a 1% annual likelihood of flooding, with expected annual damages to residential properties forecast to exceed $32 billion.

In addition, the research also warned the increasing frequency and severity of flooding amid the deepening climate emergency could see the number of U.S. properties exposed to flooding increase by 11% and average annual losses jump by at least 26% by 2050.

The vacuum in climate-related information when purchasing property needs to be addressed. People need to understand what the climate-related costs are going to look like and rethink their property location if they cannot meet those costs.

Lower-income property owners are most at risk, and this, in turn, has the potential to widen the wealth gap in the U.S. and exacerbate inequality.

How will local government tax revenues be affected?

They could be hit quite badly, as the total for municipalities typically relies heavily on property taxes. Having that tied to a physical asset that is exposed to climate change introduces a lot of risk to the stability of that revenue stream, according to DeltaTerra Capital research.

This is not just a domestic issue. It is a problem for countries worldwide. And it morphs into a humanitarian crisis when you start looking at the issue through a global lens.

Munich Re, the world’s largest reinsurance company, observed steep economic losses in 2022 as the climate crisis drove more extreme weather events, such as Hurricane Ian in the U.S. and apocalyptic flooding in Pakistan. Reinsurance refers to insurance for insurance companies.

It estimated that these losses amounted to $270 billion last year, of which around $120 billion was covered by insurance. The insured loss total continues a trend of high losses in recent years.

Someone must pay in the end. Whether insured or uninsured, it becomes an increasing economic burden.

So, before you purchase your next property, consider the climate cost also.

Be safe and enjoy time with family and/or friends.

Cheers,

Jacque

“The world is reaching the tipping point beyond which climate change may become irreversible. If this happens, we risk denying present and future generations the right to a healthy and sustainable planet – the whole of humanity stands to lose.” - Kofi Annan, Former Secretary-General of the UN.

(THE LONG-TERM INFLATION TARGET MAY BE 2%, BUT THE REALITY WILL LIKELY BE QUITE DIFFERENT)

December 27, 2024

Hello everyone

The era of stable inflation is over.

Yes, the Fed might get inflation down to close to 2%, but I believe they will struggle to keep it there.

Let’s check out the reasons why here.

First, demographics.

The U.S. and other Western industrial countries – even China – are facing declining populations that will result in a persistent shortage of labour. Tight labour markets in turn will keep upward pressure on wages as businesses compete for workers.

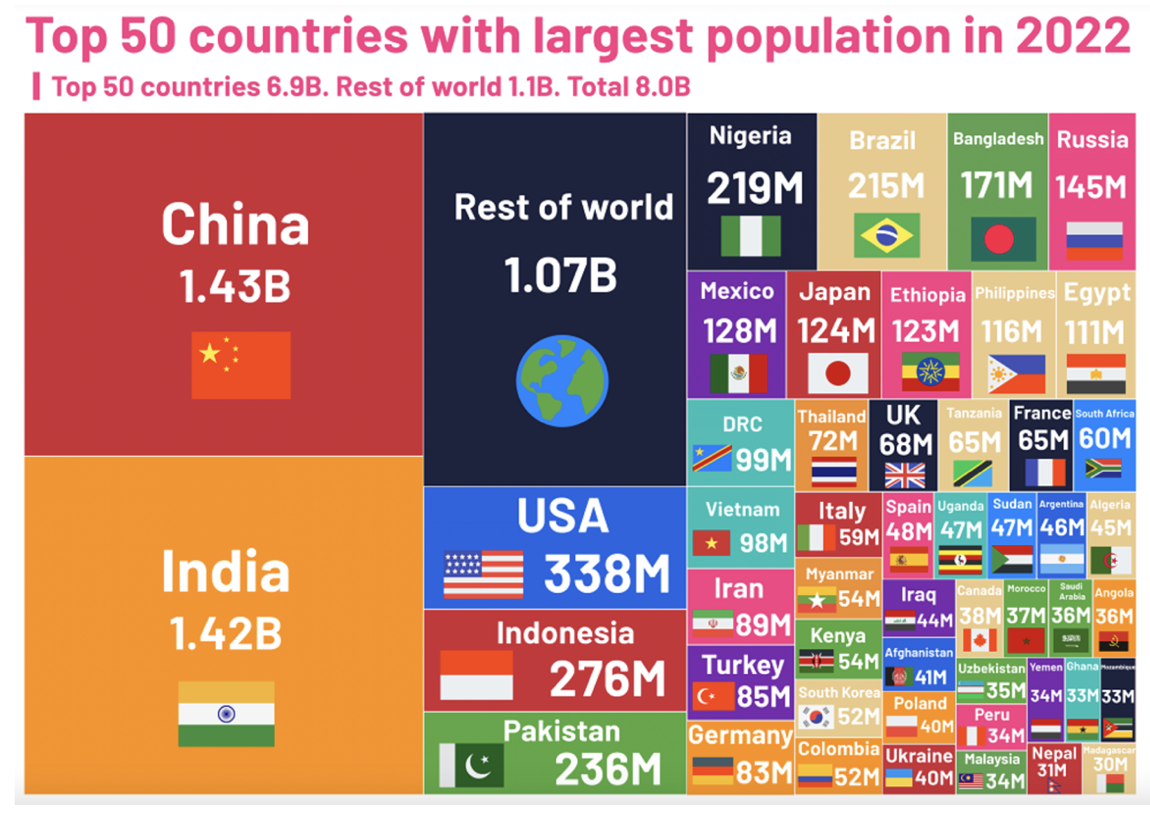

AND THESE ARE THE TOP 50 COUNTRIES WITH THE LARGEST POPULATION IN 2050.

And then there is the era of global free trade, which is taking a backseat to security concerns in the wake of the Russian war on Ukraine and Western tensions with China after the pandemic. Any tensions between the U.S. and China tend to be costly.

The growing government deficit – does anyone really think about this and its consequences? – is also fuel for inflation. The U.S. has been running trillion-dollar deficits since the pandemic and the national debt is expected to continue to grow by leaps and bounds.

The importance of greening the economy is a concept we all appear to accept. But this is another potential inflation accelerator. And what about the implications here? The U.S. would need to spend trillions of dollars to modernize its electric grid and feed the insatiable appetite of emerging technologies such as artificial intelligence. Lots of older, valuable assets such as coal-or gas-fired could also get stranded.

2% inflation has gone by the wayside for the long term? We’re probably looking at a 3% inflation world.

The only way to get to 2% long term would be to drive up unemployment and collapse the economy. Hands up who thinks the Fed is going to do that?

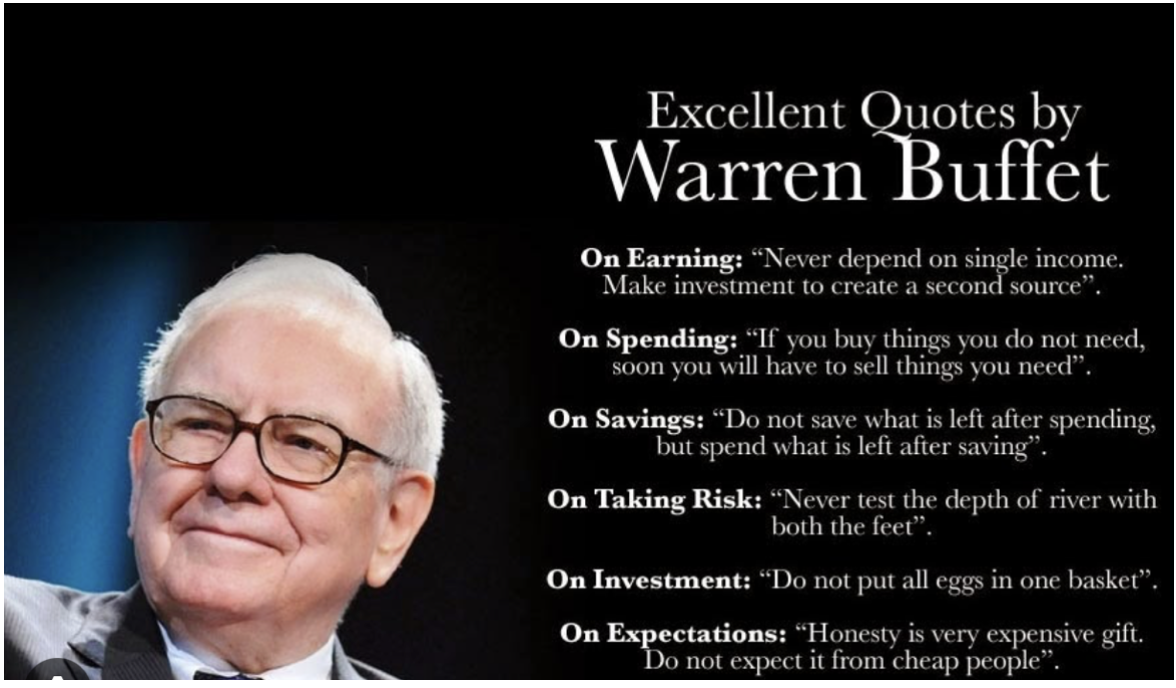

I want to sink into your psyche today some investing advice by Buffett. You would do well to write these on a piece of paper and stick that on the wall above your computer or your desk and read it every day.

We might know the hard and fast rules of investing, but life has a habit of tipping the scales sometimes, where we temporarily lose our balance and are not thinking clearly, and these are the times we sometimes slip up in our ability to stick to the plan and the rules.

So, let’s jump into those tips.

1. Design a broad portfolio. The goal of the non-professional investor is not to pick winners – but rather own a cross-section of businesses that, in the aggregate, are bound to do well. This is why Buffett always advises investors to invest in a low-cost S&P 500 index fund, which will achieve this goal. He suggests checking out Vanguard. Interestingly, Buffett revealed 10 years ago that he would direct 10% of the cash to go into short-term government bonds and 90% to a low-cost S&P500 index fund.

2. Steer clear of the financial salesperson. Professional money managers and advisors (on Wall Street or indeed anywhere) are incentivized to recommend various securities. The fact is that they rarely beat the market. Buffett’s words here: “You just have to recognize you’re dealing with an industry where it pays to be a great salesperson…There’s a lot more money in selling than in managing…if you look to the essence of investment management.” (I learned this lesson the hard way and am now very wary). And please note that more than 95% of financial newsletters are rubbish, written by people with no investing experience.

3. You don’t need to be a Math genius. Buffett says you don’t need to excel at technical analysis or mathematical calculations to find great stocks. Buffett comments that “if you need to use a computer or a calculator to make the calculation, you shouldn’t buy it” (the stock).

4. When you buy a stock, you own part of the business. Buffett only buys something when he grasps the intrinsic value of an asset or the discounted value today of the cash that a business generates in the future.

5. Market action is largely driven by emotions. Fear and greed should guide investors on when to buy and sell. Buy when there is fear and sell when there is greed. Simple as that. (For long-term investors, just average in and stick the investment in the bottom compartment of your cupboard). Buffett reminds us of the fact that math and a high IQ don’t necessarily help. So, leave the ego boxed up if you topped your class in Math – it may get in the way here... Buffett’s words: “Higher mathematics may be dangerous, and it will lead you down pathways that are better left untrod.” He goes on to remind us that “we do not sit with spreadsheets…we just see something that obviously is better than anything else around, that we understand. And then we act.”

6. After a loss, move on. Look forward. No extra detail is needed here.

7. Steer clear of declining businesses. When Buffett started on his investing journey, he used to buy cheap, failing businesses that he called “cigar butts.” But that strategy is not beneficial in the long run. Real money is going to be made by being in growing businesses, and that’s where the focus should be. Buffett is now known for seeking out wonderful businesses that he could buy at fair prices. He transformed Berkshire Hathaway from a small, failing textile mill into a near-$800 billion multifaceted juggernaut.

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.