Mad Hedge Technology Alerts!

One of the forgotten risks of AI is the energy capacity situation in the United States.

Many people forget that AI will require immense energy with a hoard of energy-guzzling data centers to facilitate the next tech revolution.

Many consumers have come to realize how the cost of energy has skyrocketed lately and no doubt the interest rates cut next year might turbocharge commodity prices around the globe.

There is an increasingly real chance that Silicon Valley might not be able to afford AI simply because the costs of energy will deem the AI concept unworthy.

Green energy hasn’t developed as fast as many experts once thought and the United States is still very much dependent on fossil fuels to facilitate tech and business in general.

A pressing question that is popping up is whether the United States can deliver the energy capacity that AI chips demand.

The question is hard to dissect because the situation is always changing.

Numbers need to make sense just like how builders build when they think they can sell their houses and apartment for a profit to the end buyer.

The military conflict in Eastern Europe has forced German manufacturing to deindustrialize because producing without that cheap Russian energy is loss-worthy. AI could follow a similar pattern.

The data grid will become strained but by how much is the next most important matter.

A ChatGPT query, on average, requires almost 10 times as much electricity to process as a Google search does.

The rise of generative AI coincides with a heightening of other factors increasing energy demand, from the electrification of transportation and infrastructure to the on-shoring of US manufacturing. Adding yet another acute demand: AI systems need power all the time.

Critics of AI fanaticism point to potential wastefulness and this could end up morphing into a government regulatory quagmire like so many industries that are overburdened by government agency overreach.

If in the case, the energy demands spiral out of control with everyone going the AI route with every country building AI data centers, the exploding costs will mean that tech won’t be able to profit from AI as quick as it wants.

Many analysts are already raising the flag as to whether all these billions poured into AI investments will really pan out or not. AI isn’t free to produce but shares of it are priced as such.

Much of this hot money is migrating into companies that haven’t proven anything or never even turned a profit, look at OpenAI, it started out as a non-profit.

The issue I have is that generative AI is priced to have zero pushback of its revenue trajectory and I do believe that is wrong.

When there is a pullback, it will be deep and sharp even if not long.

I believe that would be a healthy event for AI because the stock shares of AI have gone parabolic when there isn’t much meaningful follow-through to the underlying business models.

On top of that, generative AI is programmed to be ultra-left-leaning on the social spectrum which could cause conflict down the road.

In short, ride up the momentum until the wave crashes, but watch out for the canary in the coal mine which will bring attention to a deep dip in AI shares.

Mad Hedge Technology Letter

July 3, 2024

Fiat Lux

Featured Trade:

(SHOULD I INVEST IN AI CHIPS OR AI SERVERS?)

(SMCI), (NVDA), (DELL)

The AI server market is booming and so are the AI chip markets.

I’ll talk about 2 prestigious companies right in the mix of things.

For long-term portfolios, it’s essential to not miss out on these supercharge growth companies.

I just don’t think that average investors will be able to make up the performance if they miss the boat of these 2 companies. The law of large numbers will just put you too far behind.

All the hot new money is going into AI which adds to the momentum of the share price trajectories.

Even the old money, after not being convinced by Bitcoin, is starting to come around to AI partly because most of the companies involved in AI are publicly listed companies on the New York Stock Exchange.

It makes it a lot easier when the source of exponential growth isn’t on some alternative exchange in some alternate currency in some backwater jurisdiction.

With a few clicks and moving a few dollars here and there, investors can be part of the AI future whether it be in AI chips or AI servers like the companies I am about to talk about.

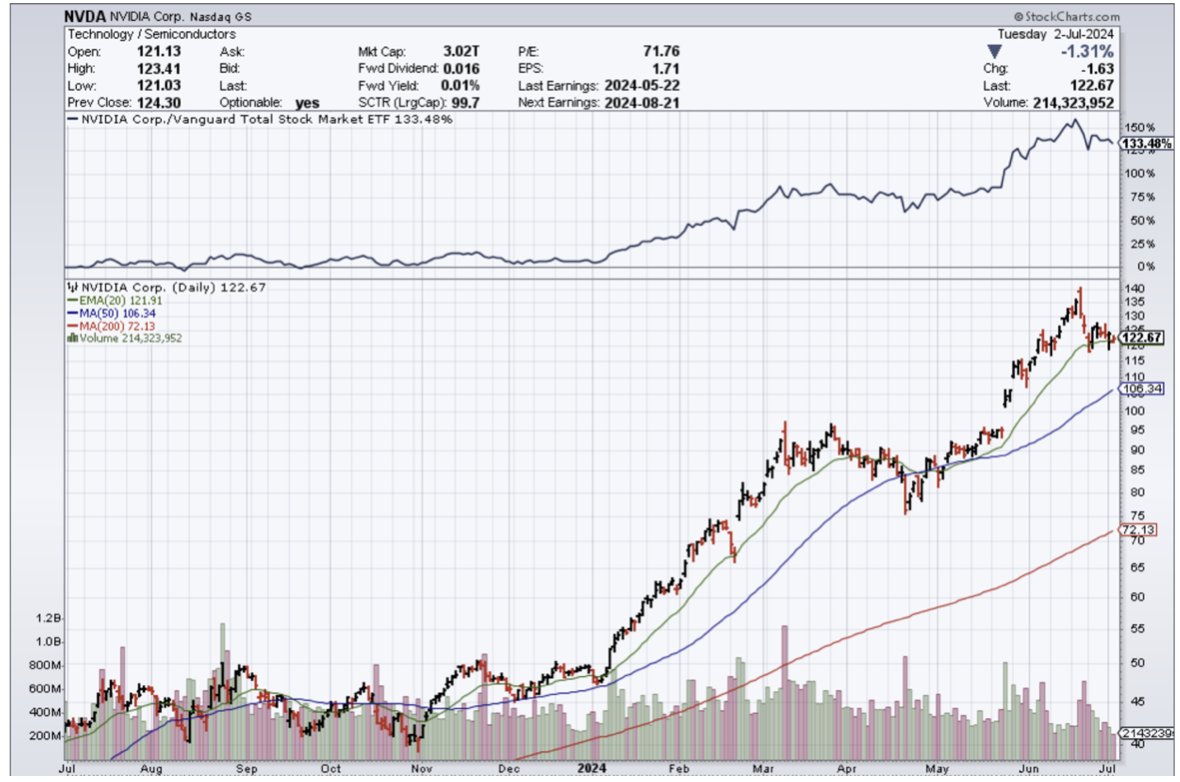

What up with Nvidia?

Nvidia (NVDA) dominates an impressive 94% of the AI chip market. It’s basically a monopoly or close to it.

Revenue is rising a stunning 262% year over year.

Even more interesting, emerging growth avenues in the nascent AI market indicate that Nvidia could end up doing even better than that.

For instance, governments are also betting the ranch on AI and this stable source of revenue will highly likely grow substantially for the foreseeable future.

Nvidia's customer base is diversifying beyond the major cloud infrastructure providers that have been deploying its chips in large numbers to train and deploy AI models.

Spending on AI chips is expected to grow more than 10-fold over the next decade, generating $341 billion in revenue in 2033 compared to $23 billion last year.

Nvidia should remain the Tom Brady of AI stocks as the race to develop AI applications by companies and governments alike has created a secular growth opportunity.

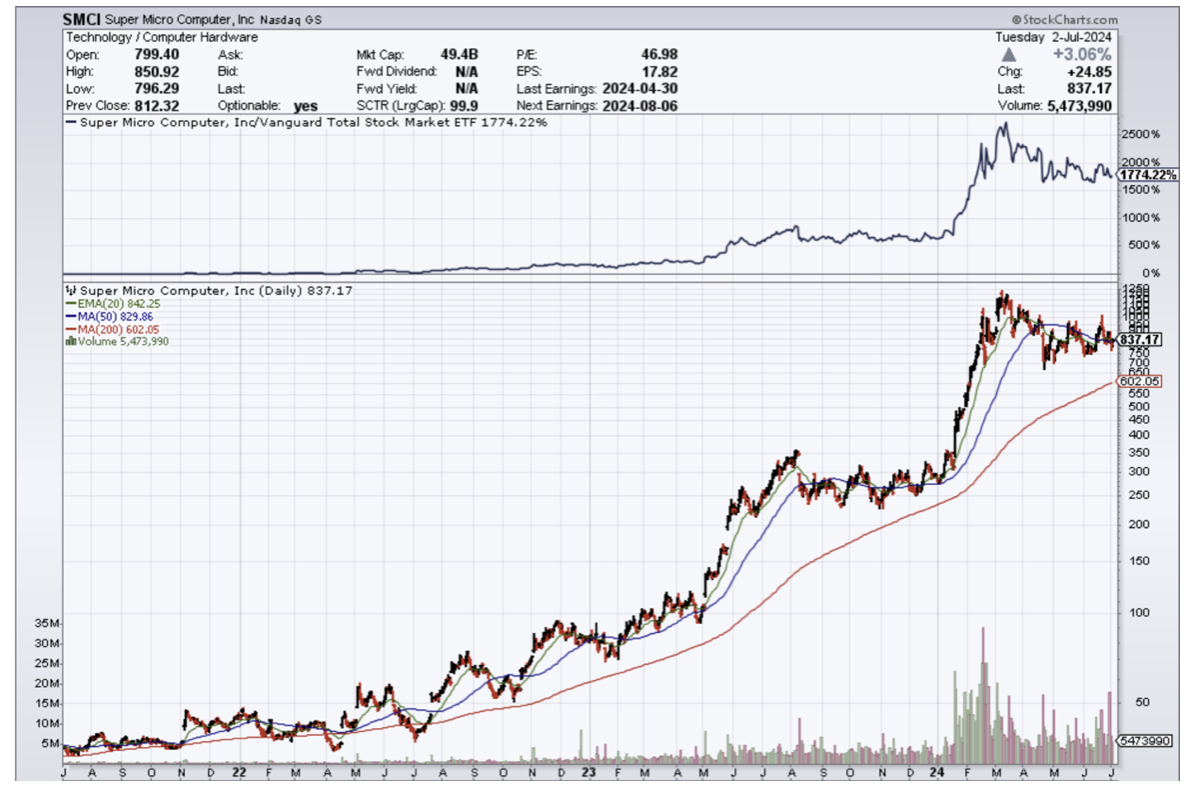

What about Super Micro Computer?

Supermicro's future prospects are attached to some extent with that of Nvidia’s.

Data center operators require server rack solutions of the type that Supermicro sells to mount the processors sold by Nvidia and other chipmakers.

Revenue jumped 200% year over year and Supermicro isn't all that far behind Nvidia when it comes to how AI has supercharged its fortunes.

I expect its top line to nearly double over the next couple of years.

Demand for AI servers is expected to expand at a compound annual rate of 25% through 2029.

Supermicro is growing at a faster pace than the AI server market right now. As it turns out, its growth is faster than that of more established companies such as Dell.

How to invest?

Supermicro is cheaper than Nvidia and Nvidia’s run-up to a more than $3 trillion market valuation has got to scare some people with sticker shock.

People with a time advantage of more than a few years should invest in Super Micro, whereas investors looking for that quick sugar high should buy the dips in Nvidia.

In short, anyone under the age of 40 and many years in front of them should invest long-term in Super Micro at a market cap of $50 billion. With Nvidia, I could easily see its market cap climbing to $4 trillion soon, but a wicked pullback would mean its market cap going from $4 to $3 trillion.

Either way, these are two tech firms with great prospects in the current and future.