Mad Hedge Technology Alerts!

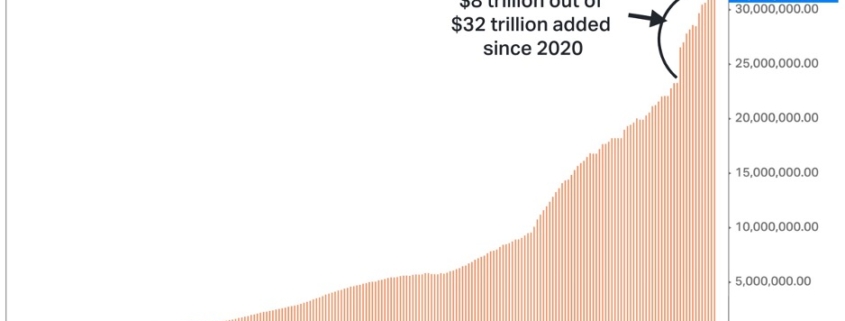

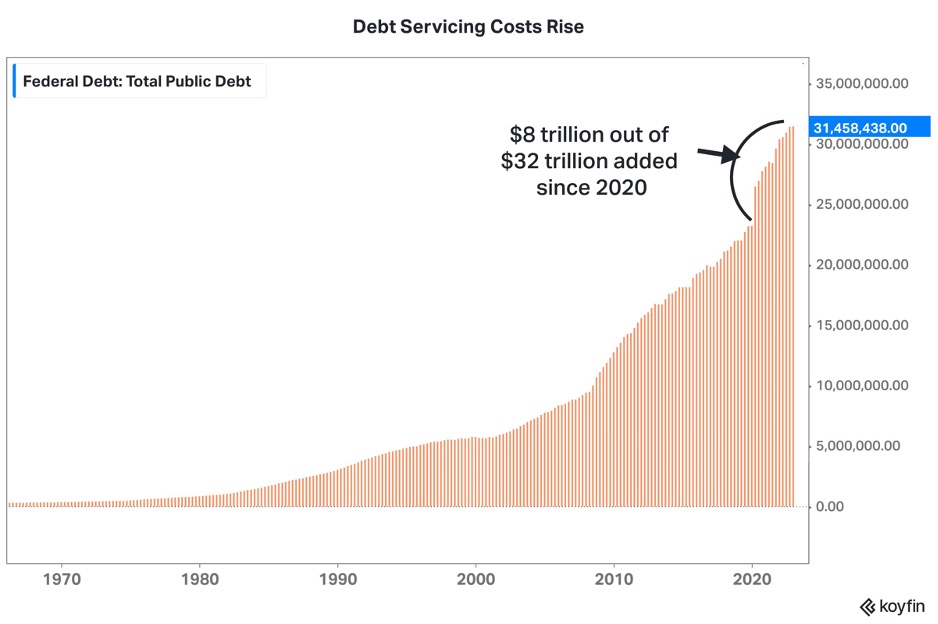

Fitch Ratings’ decision to strip the US of its AAA credit ranking to AA+ sets the stage for inflation to come roaring back, and tech stocks to underperform in the short term.

Why?

The downgrade risks bond yields blowing out, which in turn will potentially cause the U.S.’s interest payments on the debt to shift substantially higher.

That is exactly what investors don’t want to hear, in particular concerning technology stocks.

Tech stocks, along with U.S. housing prices, are most susceptible and sensitive to interest rate shocks and this could be a doozy.

The smaller the tech company is, the more reliant they are on initial debt funding to develop the company.

Big tech will be more insulated from this chaos because they are the equivalent of the reams of home buyers that purchased homes at a sub-3% interest rate that is fixed for 30 years.

As long as revenue is growing okay-ish, big tech will be fine, and the latest earnings reports have proved that with big tech’s unimpressive single-digit growth.

It’s nothing special but good enough for the times.

The booming federal deficits are the heart of the bear case for Treasuries and, even more poignant, the massive federal mismanagement of the country, no matter which political party has been in charge.

Take for instance, over 20 years and 3 presidents, a certain country would spend over $10 trillion in Afghanistan and the result is replacing the Taliban with the Taliban.

Many would say that wad of federal money probably wasn’t worth the paltry result.

Now, what we finally have is a real-life example of the consequences of government underperformance.

The U.S. economy is the most vibrant, productive, and profitable economy in the world.

Free market capitalism has catapulted the U.S. to build the largest and most successful tech industry in the world that is the envy of the rich world.

Now, exploding bond yields move to the fore as the largest risk for technology stocks.

The downgrade also means that Fed Chair Jerome Powell and the Central Bank will have a harder time pivoting when they want to because yields could spike and could have another dose of inflation to fight against.

The downgrade could invite a horde of algo traders and hedge fund pros to pile into the short-bond trade because where there is smoke, there is fire.

In the short term, don’t expect the 30-year US treasury yield to hit 10% which was the case in 1987.

However, a turn for the ugly and yields surpassing last year’s 4.35% is just in sign after this last melt up.

The stage could be set for the 30-year to reset at higher increments between 5%-6% with no relief in sight.

This sort of level is highly prohibitive to tech stocks in the short term, therefore, I would believe a repricing would need to take place to balance itself out.

In all honestly, tech needs a break and this appears as if it is the trigger to cool down tech stocks which have been on a pulsating trend to the upside in 2023.

Ultimately, I would describe the downgrade as inevitable. The rising (and accelerating) deficit begs the question of fiscal amateurism.

Congress has been behaving as if unlimited dollar binge spending has no consequence.

Furthermore, we can kiss smaller tech companies tapping the debt market goodbye.

Conditions keep tightening in tech and it’s becoming harder to thread the needle for the unknown quantity.

I would stick with investments in known quantities with strong balance sheets, as they will perform better in a spiking bond yield scenario.

Reload the ammo to buy the dip on those guys.

U.S. Congress is now on call to reign in the massive fiscal deficits or face yet another downgrade and even higher interest payments on federal bonds.

That would be materially negative for tech stocks in the medium term.

Mad Hedge Technology Letter

August 4, 2023

Fiat Lux

Featured Trade:

(SELF-DRIVING CARS ARE HERE)

(TSLA), (FSD)

Isn’t it interesting that self-driving cars and the software that launched this phenomenon are not required to pass a driving test, yet humans are?

I am here today to challenge the basic premise that software backed by artificial intelligence can drive a car better than a human.

Take left turns without a traffic light:

Artificial intelligence has consistently failed to successfully complete this standard objective.

This somewhat riskier driving maneuver must take into account drivers on the other side of the road, which humans can do, but the back-tested data in the self-driving software cannot predict external variables that could come into play.

This is why the software malfunctions on a left turn when a bird defecates on the windshield believing it’s an accident worthy of a full stop and yes a full stop right in the middle of oncoming traffic.

These types of poor decisions occur more often than you think with this “cutting-edge” technology.

The truth is that self-driving car technology has been very slow to develop.

Elon Musk has been talking about Tesla's Full Self-Driving technology for years. In 2016, the CEO said that Tesla's driver-assist feature Autopilot will be able to drive better than a human in two to three years.

He also said that by 2018, it would be possible to remotely summon a Tesla (TSLA) across the country.

In 2019, he said that Tesla could have a fleet of a million robotaxis by the end of 2020 if the company pumped out hundreds of thousands of FSD cars.

FSD is currently under investigation by the federal government in 2023.

Twenty years on from the start, no real product to show for except many unintended road deaths and rich Silicon Valley software engineers that peddle this false theory that software is better at driving than humans.

What’s the current situation today?

100% self-driving technology amounts to little more than a bunch of glorified tech demos. FSD isn’t the real deal.

In demos, you see what the creators want you to see, and they control for things that they'd rather you didn't.

To an AI, a slight change could be catastrophic. After all, how is it supposed to know what an appropriate response to a slight or sudden change is when it doesn’t understand everything it’s looking at?

How will it handle when the weather goes from sunny to hail, or when there’s deer in the headlights at the edge of the road?

It is unequivocally wrong to believe that software is better at real-time driving than a human, and therefore this industry will never mushroom into what investors think it might.

Self-driving cars are a 2-ton weapon ready to kill pedestrians, cyclists, and little kids.

The interesting thing to look for is whether these venture capitalists and investors double down on failed technology and pull strings to get this circus on public roads with the rest of us.

It’s entirely possible that this could happen in limited areas like the states of Arizona and California.

At the very minimum, if all 50 states do green-light such technology, we will need to wait another 15 or 20 years.

It’s not as imminent as Elon Musk tells us.

Don’t believe self-driving is the secret sauce that will be the next leg in revenue for Silicon Valley.

The benefits of this are not coming any time soon.

Outdoing the smartphone is proving to be almost impossible. Who would have known that the smartphone would have such staying power and longevity?

Tech is still utterly reliant on smartphone revenue until someone can supplant it and package it nicely in a consumer-friendly way. The road to that type of achievement is littered with good intentions.

ANOTHER LONG WHILE FOR SELF-DRIVING TO HIT THE MASSES