Mad Hedge Technology Alerts!

Datadog's (DDOG) platform enables IT professionals to simultaneously monitor the performance of multiple servers, databases, cloud services, applications, and mobile apps through unified dashboards.

That unified view makes it easier to diagnose problems while saving time and money.

What do these tools specifically do?

They monitor and offer analytics for information technology (IT) and DevOps teams that can be used to determine performance metrics as well as event monitoring for infrastructure and cloud services.

Every CEO I talk to tells me that the accuracy and fluidity of their data procurement is one thing they prioritize above other sets of challenges in technology.

Muddying and underutilizing these tools is really a death knell for any executive in Silicon Valley, and buying the best tools money makes is where Datadog comes into play.

The user interface includes customizable dashboards which can show graphs composed of multiple data sources in real-time. Datadog can also send users notifications of performance issues on any set metric, such as compute rates.

Some of its other features providing immense value are shooting out alerts based on critical issues, broad support for over 250 product integrations, and automatization of collecting and analyzing logs as well as latency and error rates.

Simply put on the financial side of the numbers, Datadog is in the sweet spot of growth, and their last Q2 earnings report validated that.

The quarter was stronger than expected with existing customers, as well as strong new customer sales.

Relative strength revealed itself across product lines and across customer segments.

For a quick review of the quarter, revenue was $234 million, an increase of 67% year over year and 18% quarter over quarter and above the high end of management’s guidance range.

Customers continue to pursue cloud migrations which is a global business trend.

Expansion with existing customers means rapidly standardizing with Datadog to consolidate observability tool vendors.

The stickiness of Datadog’s business is quickly becoming an x-factor with 75% of customers using two or more products, up from 68% a year ago.

Additionally, 28% of customers are now using four or more products, which is up from 15% last year.

These companies rely on Datadog log management as the platform across the organization to find the root cause of issues.

Significant increase in usage of existing products was used to better understand good performance in production.

Datadog has also upsold several massive European e-commerce companies that were using multiple commercial observability tools, and one of their 2021 strategic initiatives was to consolidate and reduce costs by standardizing Datadog to satisfy while improving their team's collaboration and communication.

The company is investing as aggressively as it can to stay ahead of the game.

Accelerating the investment in R&D is helped partly through a few acquisitions to take advantage of the opportunity across observability and security.

Another sub-sector screaming for Datadog penetration is real-time business intelligence (BI), and that will be the next sphere to be attacked by creating products that can easily integrate into their platform.

In terms of the impact on the go-to-market, management is now inclined to push the sell side of the security products more aggressively.

It hasn't happened yet, and they simply weren’t doing enough before.

Those products are just barely reaching the addressable audience it needs to, but it's something that is in the short-term pipeline.

In the long-term, they are making progress in breaking down silos between DevOps and security teams.

This foray will provide opportunities to democratize data and help customers increase visibility and manage complexity.

The world is transforming digitally so the overall market and the size of the infrastructure that will have to be monitored is likely a lot bigger than what had to be monitored five years ago.

There is just a lot more ground to cover in terms of those market penetration. So, how much can Datadog cover with infrastructure monitoring?

That’s really the main crux of piling resources into new acquisitions and the creation of new products.

In parallel to that, it's a field that is still evolving, right?

The name of the game in the cloud is that there are ways to innovate and new ways of running workloads.

Datadog has already seen that story play out multiple times and they continue to improve on their iterations with each version.

Remaining performance obligations, or RPO, was $583 million, up 103% year over year, driven by strong sales activity and increased contract duration.

A company's Remaining Performance Obligation (RPO) represents the total future performance obligations arising from contractual relationships. More specifically, RPO is the sum of the invoiced amount and the future amounts not yet invoiced for a contract with a customer.

The increase in contract duration was driven by a higher mix of annual and multi-year commitments relative to the year-ago quarter. As a reminder, multiyear commitments are billed annually, and they do not incentivize our sales force toward multiyear deals.

In terms of product resiliency and stickiness — it’s there for Datadog based on the numbers I just trotted out.

The projected third quarter still signals elevated growth — forecasting revenues of 60% year-over-year growth at the midpoint.

Essentially, the company's landscape hasn't changed, and the focus is still mostly greenfield, new environments, teams that are going to start small with DDOG and are going to grow until they standardize with them for just about everything they do.

Datadog calls this their "land and expand" model — wherein it locks in a customer with a single product to cross-sell additional ones.

The issue I have with Datadog is not the spectacular structural tailwinds and accelerating growth metrics of the company, but the pricey valuation of the stock.

Don’t get me wrong, I would love to own this company myself, it really is the glue that holds the data together for many big corporations, an important cog in the wheel, and a service that cannot be shortchanged for a tech CEO.

But I would be doing a disservice to my readers to recommend deploying capital at these prices — the stock is up over 400% in the past 2 years which is why the stock is expensive today especially for a company that is a net-loss maker.

However, this does mean the stock can’t grind up higher, but I believe the more advantageous risk-reward scenario would be to wait for a big sell-off in DDOG if searching for a meaningful profit or finding other opportunities until this one becomes cheaper.

If it simply runs away from us, we will just migrate to the next tech opportunity.

Mad Hedge Technology Letter

September 3, 2021

Fiat Lux

Featured Trade:

(TWITTER MAKING MOVES TO BOOST EARNINGS)

(TWTR)

When one looks at the 7 billion people in the world who don't use Twitter yet, and then looks at the 300 million who are in the United States, Twitter obviously has ample runway to add whole groups of people who look just like those that use the service today, whether they're in the US or in other parts of the world.

When one considers the product roadmap, it's right-sized to help all of them to get better usage out of Twitter.

The top of the marketing funnel continues to be robust and consistent and gives Twitter confidence that people can find what they're looking for and feel safe being a part of the conversation.

That’s a lot of what these new Twitter features are about and I do believe these changes signal a new wave of earnings’ success on the short-term horizon.

Let’s roll through them.

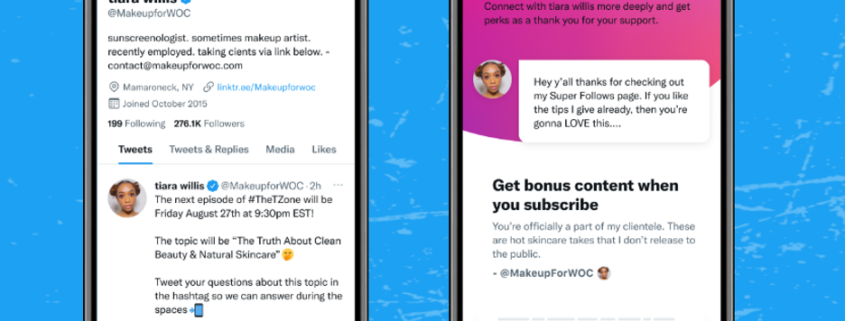

Twitter users who purchase a subscription, known as Super Followers, will receive a public badge that is highlighted under their name whenever they interact with the creator who they are paying a subscription to. That gives the creator an opportunity to pay more attention to subscribers if they wish.

The feature — which is currently only available to a limited group of US and Canada users on Apple devices — lets Twitter users charge others $2.99, $4.99, or $9.99 per month to follow them.

Twitter users who offer super follows will get a special pink badge on their profiles. They will be able to keep up to 97% of super follow revenue up to $50,000 after fees, then up to 80% past that mark.

Only users who have at least 10,000 followers, have used the site for at least three months and have posted at least 25 tweets over the past 30 days will be eligible to charge a toll for their tweets, according to Twitter’s rules.

The news comes as various online platforms like Patreon, Substack and OnlyFans compete to offer internet users ways to make money from the content they create.

Creating Super Follows content is for anyone who brings their unique perspectives and personalities to Twitter to drive the public conversation, including activists, journalists, musicians, content curators, writers, and so on.

Twitter said it would launch a safety feature that allows users to temporarily block accounts for seven days for using harmful language or sending uninvited replies.

Putting in new privacy-related features aimed at giving users greater control over their follower lists and who can see their posts and likes, an effort to make people more comfortable interacting and sharing on the social network.

Among features being considered is the ability to edit follower lists, and a tool to archive old tweets so that they’re no longer visible to others after a specific amount of time designated by the user.

All of these improvements to the inner workings of the platform set the stage for Twitter to dive straight into Bitcoin as the currency of choice.

Why?

If the Internet has a native currency, a global currency, Twitter is able to move faster with products such as Super Follows, e-commerce, Subscription, Tip Jar and we can reach every single person on the planet because of that and sort of going down a market by market approach.

If everyone is using Bitcoin, transactions get easier instead of dealing with dollars, rubles, pesos, and liras and getting a whole division to manage these odds and ends.

Ultimately, Daily Active Users (DAU) has been remarkably consistent and healthy in every geography.

In the US as news cycles come and go, as habits evolve hopefully, people are still merging their pre-pandemic habits with their new habits.

For many people, that means that they're new on Twitter and they're sorting out all kinds of different things that have changed in their lives.

I believe that plays out positively for Twitter in the form of accelerating revenue, increasing earnings, and a larger moat around their unique business which is increasing its scarcity value.

I am highly bullish on Twitter in the short and long term and deploying capital through dollar cost averaging would be a great way to play this.

Buying Twitter today at $64 would make sense.