Mad Hedge Technology Alerts!

Being a stone’s throw away from the pulse of Silicon Valley, I have been showered with acute insights to which I otherwise would be oblivious.

This finely developed acumen is vital to keep my head above water and offer insights unfounded in any other newsletter.

The margins of victory and failure are becoming finer with each passing day, and that goes tenfold for the hyper-cutthroat trading world where each investor fights daily for his crust of bread.

The same thin margins apply for the tech industry whose prodigious march to profits has dwarfed any other industry.

Its far-reaching effects has brought forth social change unparallel to any other time in history.

The Mad Hedge Technology Letter has chronicled the messenger platforms rolled out by public companies such as Facebook and Snapchat, and their lust for profit extraction from every corner of the globe.

But there is another war going on in one nearby corner outside of our social lives I have yet to touch upon that will have profound consequences.

Enter the office.

The battle for hegemony in the workplace to evangelize a supreme workplace app is a big deal.

The office is where most semi-sober, semi-sane adults make a living, and where they allocate the lion’s share of sunlight hours before they mosey on home.

Slack, a workspace messenger app, has become the dominant way to communicate with professionals using collaborative messaging services, and offering integration with all legitimate apps that workers leverage to get work done.

After another round of fundraising, the company is now valued at more than $7 billion.

The $7.1 billion price tag is $2 billion more than the price only last September when Masayoshi Son’s SoftBank dipped its toes in to the tune of $250 million.

Overall, the company has at least 41 investors to its name.

This latest $427 million capital injection was led by Dragoneer Investment Group and General Atlantic, both private equity groups on the forefront of investing in transformative Silicon Valley firms.

Employees’ appetite for enterprise software has mushroomed in recent times, highlighting the dire need for progressive workplace apps liaising with other major productivity applications.

The smooth display interface and ease of use has spawned a monumental rush inside offices to adopt this sleek looking app called Slack.

Competition is coming with Microsoft and Facebook intent on disrupting Slack’s newfound success in the workspace area.

Slack is one of the most popular apps distributed by start-up companies and the numbers back it up.

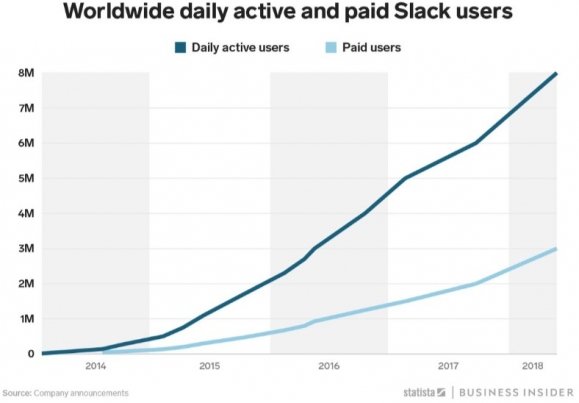

The company has blown by 8 million daily active users (DAU).

Considering Slack only had 1 million users three years ago makes this feat even more impressive.

Of the 8 million (DAU)s, 3 million are paid subscribers.

Slack follows the freemium model such as other tech firms like Spotify, which lure customers in for free and allow access to its platform.

The free users are the biggest source of converts to its paid reoccurring subscription revenue.

Slack proves its worth by enhancing each product iteration based on diligent analyzation of customer feedback.

A no-brainer for many firms, but you would be surprised how many companies forgo this critical source of data.

Slack streamlines the process of communicating with work buddies.

No matter what industry or specialization with which you grapple, Slack makes it easy to share information over its platform.

In fact, Slack is an acronym for “searchable log of all communication and knowledge.”

Workplace portals can be initiated right away around projects or assignments, and the sense of team bred through this innovative communication channel offers the impetus for coworkers to contribute immediately.

Speed is money in tech land, and Slack gives a reason for coworkers to shun emails all together.

Being a customer-centric workplace app, any malfunctions in the harmony of its operations are met with instant patches of fixes so workers can carry out their time-sensitive tasks.

Other advanced functions aiding workers is the advanced search function allowing users to search for messages that were sent days, weeks, months, or even years ago.

Slack messages accommodate the trend for replying using a hoard of emoji’s, which has become a standard response as the emoji has taken a life of its own in the business world.

It has been found through surveys that emojis are a more effective way to respond to messages that need a blunt opinion.

Millennials are the tech-savvy generation that christened emojis as a normalized way of communication, and they are Slack’s target audience.

Another function allows users to type short code into its interface, triggering the software to remind users of a task and at a specific date and time.

Fastcompany.com smartly described Slack as “a virtual mash-up of the conference room and water cooler, with a pinch of corner office chit-chat.”

Slack is known for uber-productivity.

And if it’s something that a top-quality worker should harness such as referencing, enhancing, prioritizing, delegating, sharing, or creating - the app facilitates these traits seamlessly.

Slack certainly will boost the productivity of your team’s performance once the team gets a hang of its tools.

The emphasis of enterprise collaboration will continue as more work teams band together remotely.

This app perfectly captures functionality and meets the needs from companies where all users are online and live in different time zones.

If Slack continues evolving at its current speed, it could shortly wipe out emails.

Emails are a legacy type of communicative tool for companies, and its outdated interface is ripe for disruption.

Gmail’s disciples must have noticed that the past few iterations of Gmail have looked more and more like Slack, as it steals from other workplace app functions to upgrade its own workplace services.

All of this explains why Slack has been adding 2 million users per year and still has enormous potential for further disruption and growth.

Most early-stage companies are massive cash burners.

Reports from Didi Chuxing, the Chinese ride-sharing firm that bought out Uber in China, exposed the double-edged sword of being an up-and-coming tech firm.

Growth is often put up on a pedestal with profits relegated to the sidelines.

Even though Didi Chuxing is the dominant player in China, the exorbitant subsidies dished out to scarce drivers have devoured cash flow metrics.

Didi Chuxing has lost an astonishing $580 million in the first six months of 2018.

Slack is cash-flow positive.

An extraordinary accomplishment for an industry littered with firms exercising their industry right to spoon feed excuses of indulgent losses until their IPO day.

Even more impressive, Slack is only 5 years old and has already signed up more than 70,000 workgroup teams for its platform.

Slack has avoided even talking about going public, and this is bad news for retail investors hoping to get in on the action.

The carnage that tech firms have faced in front of Congress and in the press have budding tech firms rethinking if it’s worth opening themselves up to such torturous criticism.

Mark Zuckerberg is now the whipping boy on Capitol Hill.

Why risk it when bountiful funds await through venture capitalist coffers chomping at the bit to pay a premium for the latest hot tech company?

Elon Musk’s personal meltdown does not help either.

Sadly, it will be years before Slack chooses to go public - and most likely when the business becomes ex-growth.

Yes, it’s unfair to the average Joe, but life is unfair.

Money talks and as Slack feeds back its fresh capital into energizing its product, the valuation will rise to epic heights along with its DAU numbers.

If your office isn’t using Slack yet, it will soon.

Or…it’s probably not a modern place to work.

To visit its official website and sign up for free, please click here.

________________________________________________________________________________________________

Quote of the Day

“You should learn from your competitor, but never copy. Copy and you die,” – said Alibaba cofounder Jack Ma.

Mad Hedge Technology Letter

September 10, 2018

Fiat Lux

Featured Trade:

(GOOGLE’S BREAKFAST OF ROTTEN EGGS),

(TWTR), (FB), (GOOGL), (MSFT), (AMZN)

In a recent interview Google CEO Sundar Pichai admitted he is “not a morning person” and maybe that was his argument for skipping out on the grilling that his contemporaries Facebook (FB) COO Sheryl Sandberg and CEO of Twitter (TWTR) Jack Dorsey received in front of Congress.

Or maybe Pichai managed to down a rotten egg that morning when eating his favorite staple breakfast “omelet with toast," because his decision to abort his date with Congress was a shocking error of judgment for a CEO that has had a flair for controversy lately.

With the whole world watching, the empty chair with a simple name tag with Google plastered over it represents the arrogance and excesses of Silicon Valley all mixed into one incongruous mixture.

This rookie move will open a can of worms for the company made famous by its search algorithm that dominates the developed world.

Google will have a target on its back going forward while creating a massive public relations backlash for a company that must fiercely defend its ad-laden profit engine going forward.

Instead of taking it on the chin like Facebook and Twitter, Google has voluntarily veered into a sticky situation, and all to avoid a few stomach wrenching questions from Congress.

How did this all happen?

In the beginning of June, Google decided to scrap its relationship with the U.S. Department of Defense.

Project Maven, as it was known, provided Google’s artificial intelligence (A.I.) technology to systematically analyze drone footage for the U.S. government.

Pichai chose to avoid renewing the contract, and Google Cloud CEO Diane Greene agreed it was a black eye for the company that applied its own technology to conspire against damaging human life.

Throwing fat on the fire, Pichai followed up by dismantling Project Maven and giving the thumbs up for code-name Dragonfly. This was a secret project aimed at the mainland Chinese market and rolling out a censored version of Google’s search engine by altering its construction of unique search algorithms for a mainland Chinese audience.

This incensed the higher-ups on Capitol Hill, as this move was largely viewed as pandering toward the Chinese communist government for monetary purposes at an uber-sensitive time between the two powerhouse nations, which remain mired in a tumultuous trade war.

The timing couldn’t be worse for Pichai.

Dragonfly is already in beta mode and could be rolled out in the near future. However, I see it as dead on arrival, because there is no hope that Google can penetrate the fortress that is the Chinese business world.

Naturally, Google employees were dismayed and shocked by these startling revelations.

Pichai’s conspicuous no-show was in part driven by the potential wrath he would have faced by these recent reckless decisions that seemed to put the American government’s interests below the Chinese communist government.

The circus was there for everyone to see.

Sheryl Sandberg put on her bravest face.

It was obvious she had rehearsed every word to the utmost precision while Dorsey vehemently guarded his brainchild with honesty and zeal.

The testimonies made social media look perceivably criminal with a congressman even hinting the reason they aren’t allowed to do business in China was mainly a business model issue, and more specifically a legal issue.

Another congressman from West Virginia suggested Facebook’s Instagram was the source of the opioid epidemic ripping apart his state.

The only thing getting ripped apart during the intense grilling was Sheryl Sandberg’s well-practiced smile.

Dorsey and Sandberg were visibly uncomfortable with the line of questioning and rightly so.

Google would have looked worse if it showed up. But it managed to look 10 times worse than that by stonewalling the government’s invitation.

In a recent Pew Survey, data revealed 44% of youth between 18 to 29 last year deleted Facebook on their mobile phones.

Facebook is already a legacy platform in the throes of disruption cannibalized by its own asset - Instagram.

Instagram will be the sole survivor of Facebook by taking out Facebook itself, and that is bearish for overall business.

And that is if social media can hang on that long before it’s taken down by the hawks circling above in Washington.

When Facebook’s Cambridge Analytica scandal broke, the government was at sixes and sevens at attempting to figure out what on earth was going on behind the smoke and mirrors of the big data theatrics.

CEO Mark Zuckerberg was let off the hook with questions he wriggled out of, and Facebook shares powered on unabated.

This time it’s different.

Regulation is an imminent threat to social media revenues and could hurt earnings this quarter.

Investors need to migrate to higher tide, meaning Amazon (AMZN) and Microsoft (MSFT), because the waves still aren’t yet reaching those levels.

Amazon and Microsoft need to send a thank you note to Alphabet for screwing the pooch.

The administration has felt it convenient to barrage Silicon Valley to solidify the Republican base, and this tactic has resonated with the administration’s diehards.

A smorgasbord of FANG-bashing was the recipe to this madness. But now sights will be zoned in on dismantling Google, and Microsoft and Amazon will benefit from avoiding nasty, gut-churning headlines that turn up in the form of Twitter blitzkrieg.

Yes, Sheryl Sandberg, Facebook was “too slow” to react to foreign interference in the elections. But it is more accurate to characterize the battle social media faces against outside nefarious forces as impossible.

It is impossible for these social media platforms to police themselves while policing the whole world.

The incessant whack-a-mole scenario is the best-case outcome for the self-policing prospects of social media.

Once social media algorithms figure out how to stopgap one method of circumvention, the bad actors will move on to a more advanced way to manipulate the algorithmic police.

What does this mean for social media?

Costs are going up and will seep into profit margins.

Highlighting the upward trend of rising expenses for social media platforms is the daily cost of keeping CEO Mark Zuckerberg safe.

And remember, he lives in Palo Alto, California, one of the safest places on planet earth with a medium household income of $137,000.

In 2017, Facebook divvied up $7.3 million for Zuckerberg’s security detail and costs associated to it.

In 2018, shareholders approved a $10 million security package to keep Facebook’s head honcho safe. This underscored the ballooning risk of leading this controversial technology forum littered with conflict of interests, and on the verge of potentially perverting western democracy.

By the end of 2018, Facebook will increase its security division from 10,000 employees to 20,000.

And that is just the beginning.

Facebook’s security division is the fastest-growing division of fresh hires at Facebook.

Before Facebook and Twitter can ring in the profits, they face an exorbitant war against foreign “bot armies” intent on muddying the free flow of accurate information on domestic shores that target individuals deemed unaligned to the foreign actor’s interests.

There will be collateral damage and lots of it.

This does not sound like an easy road to profits, and it is not.

As midterm elections creep closer and closer, Facebook and Twitter must confront elevated headline risk, and any trading day could see shares wacked with a 10% haircut.

Following the government question-and-answer period, Twitter and Facebook will be designing a new resistance to stymie villainous foreign infiltration.

Ultimately, spending the bulk of employees’ work days realigning their business models to protect democracy, instead of creating new growth drivers, is not bullish for the stock price.

It is hard to breed much confidence in social media stock’s long-term narrative after listening to Dorsey and Sandberg speak.

They kept touching on needing help from government intelligence sources to aid them in catching the miscreants.

It makes sense to gradually nationalize social media platforms to unite the disconnect between social media’s war against foreign forces and the intelligence communities war against them.

It is clear hackers are exploiting the dislocation in cohesiveness between the cracks in social media and government intelligence.

But if that ever happens, it would be the end of Facebook and Twitter as we know it, as normal users would be averse to providing free content on a government-enabled platform as well as a strong blow to democracy itself.

It all makes sense now why Dorsey and Sandberg gave the answers they gave.

Their answers were akin to a faint plea for help while appearing contrite, hoping to persuade Congress to give them more time to figure it out.

This thinly veiled attempt to elongate the profit-making process and find a solution for a problem with no solution could end badly for these two companies.

Migrate to higher quality tech names in the short-term.

The resilient American economy powers on with the heavy lifting done by Silicon Valley albeit it with fewer lifters.

If social media stocks can get through the midterm elections unscathed, there is a trade on the table for these beleaguered companies rounding out a tumultuous year.

But getting to that point will be volatile, as this group of stocks have a rocky road ahead of them for the rest of the year.

I’m Not A Morning Person

________________________________________________________________________________________________

Quote of the Day

“I'm not a regular smoker of weed. Almost never,” – said CEO of Tesla Elon Musk on The Joe Rogan Experience podcast.