Yesterday, I provided to you the evidence that oil may never again reach a triple digit price click here for ?Oil: It?s Different This Time? .

Today I am going to tell you what will replace it.

Sony Corp. (SNE) invented the lithium ion battery in 1991 to power its high end consumer electronics products. It is now looking like that was a discovery on par with Bell Labs? invention of the transistor in 1947 and Intel?s creation of the microprocessor in 1971, although no one knew it at the time.

Until then, battery technology was essentially unchanged since the first one was invented by Alessandro Volta in 1800 and Gaston Plante upgraded it to the lead acid version in 1859. That is the same battery that today starts your conventional gasoline powered car every morning.

The Sony breakthrough proved the springboard for a revolution in battery power. It has fed into cheaper and ever more powerful iPhones, electric cars, and even large scale utilities.

In 1995, the equivalent of today?s iPhone 6 battery cost $20. Today it can be had for $1.40 if you buy in bulk, which Apple does by the shipload. That?s a cost reduction of a mind blowing 93%.

Electric car batteries have seen prices plunge from $1,000/kilowatt in 2009 to only $200 today.

Tesla (TSLA) expects that price to drop to $150 when its $6 billion new ?gigafactory? comes online in Sparks, Nevada next year. The facility will produce cookie cutter off the shelf batteries made under contract by Japan?s Panasonic (Matsushita).

That will pave the way for the Tesla 3 in 2018, a low end $35,000 vehicle with a 200-mile range that will take over the global car market.

If you took existing battery technologies and applied them as widely as possible, it would have the effect of reducing American oil consumption from 22 to 18 million barrels a day. That?s what the oil market seems to be telling us, with prices at a 13-year low at $26 a barrel.

Improve battery capabilities just a little bit more and that oil consumption drops by half very quickly.

Both national and state governments are doing everything they can to make that happen.

The US is taking the lead here and now has a commanding technology lead over the rest of the world (I can?t believe the Germans fell so far behind on this one).

In 2009, President Obama chipped in $2.4 billion for battery and electric car development as part of his $787 billion stimulus package. He got a lot of bang for the buck.

So far, I have been the beneficiary of not one, but two $7,500 federal tax credits for my purchase of my Nissan Leaf and Tesla S-1. The Feds also chipped in another $13,000 for my new solar roof panels.

A reader told me yesterday that Sweden will ban the sales of gasoline and diesel powered vehicles from 2030. Japan wants electric and hybrids to account for half of its new car sales by 2020.

California has been the most ambitious, investing to obtain 50% of its power from alternative sources by 2030. Some 450,000 homes here already have solar panels, and these are not even counted in the equation.

Solar and wind are already taking over in much of Europe on a nonsubsidized, cost competitive basis.

At the current rate of improvement, electric cars will be cheaper than gasoline powered ones in only a few years. By 2030, a ten-pound battery in your glove compartment (glove box to you in London) will be able to take your car 300 miles. The cost of energy will essentially be free.

And guess what?

In a year, I will be able to use my solar panels to charge my 85-kilowatt Tesla battery during the day and then use it to power my home at night. That is enough juice to keep the lights on for three nights. Then, I will be totally off the grid, with utility bills of zero.

Tesla has denied it has such a program, but there is nothing to stop a third party from coming in and providing the service. All it would require is an app and 30 minutes worth of wiring.

To say this will change the geopolitical landscape would be a huge understatement. The one liner here is that oil consumers will benefit enormously, while the producers will get destroyed. I?m talking Armageddon, mass starvation levels of destruction.

In the Middle East, some 1 billion people with the world?s highest birth rates will lose their entire source of income.

Russia, which sees half its revenues come from oil, will cease to be a factor on the international stage, and may even undergo a third revolution. Take oil away, and all they have left is hacking.

Norwegians will have to start paying for their social services instead of getting them for free.

Venezuela, which couldn?t make it at $100 a barrel, will implode, destabilizing Latin America.

It going to be an interesting decade for we geopolitical commentators.

Further improvements in battery power per dollar will change the US economy beyond all recognition. This will be a big win for the 90% of the economy that consumes energy and an existential crisis for the 10% that produce it.

Public utilities will have to change their business models from power producers to distributors.

No less an authority than former Energy Secretary Dr. Steven Chu (another Berkeley grad) has warned the industry that they must change or get ?Fedexed?, much the same way that overnight delivery replaced the US Post Office.

US oil majors will suffer some very tough times, but won?t disappear. My bet has always been that they will buy the entire alternatives industry the second it becomes profitable.

After all, they are not in the oil business, but in the profit making business, and they certainly have the cash and the management and engineering expertise to pull this off. Exxon (XOM) will turn green out of necessity.

As is always the case, there are very few publicly listed stock plays in a brand new emerging technology like the battery sector. Many of the early stage entrants have already filed for bankruptcy and had their assets taken over for pennies.

It?s a business you want to be in because Citibank expects that giant grid scale batteries alone will be a $400 billion a year market by 2030.

When I visit friends at the oil majors in Houston, I chide them to be kind to that Birkenstock wearing long haired visitor.

He may be their future boss.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/John-Thomas-Tesla.jpg330317DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2016-02-11 01:07:212016-02-11 01:07:21The Battery In Your Future

Featured Trade: (OIL: IS IT DIFFERENT THIS TIME?) (USO), (LINE), (CHK), (FCX), (KOL), (THE BIPOLAR ECONOMY), (AAPL), (INTC), (ORCL), (CAT), (IBM), (TESTIMONIAL)

United States Oil (USO) Linn Energy, LLC (LINE) Chesapeake Energy Corporation (CHK) Freeport-McMoRan Inc. (FCX) Market Vectors Coal ETF (KOL) Apple Inc. (AAPL) Intel Corporation (INTC) Oracle Corporation (ORCL) Caterpillar Inc. (CAT)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-02-10 01:09:452016-02-10 01:09:45February 10, 2016

A reader emailed me yesterday to tell me that while visiting his daughter at a college in North Carolina, he refilled his rental car with gas for $1.39 a gallon.

So I got the idea that something really big is going on here that no one is yet seeing. I processed the possibilities in my snowshoe up to the 10,000-foot level above Lake Tahoe last night.

By the way, the view of the snow covered High Sierras under the moonlight was incredible.

For decades, I have dismissed the hopes of my environmentalist friends that alternatives will soon replace oil (USO) as our principal source of energy.

I have long agreed with the views of my fracking buddies in the Texas Barnett Shale that it will be decades before wind, solar, and biodiesel make any appreciable dent in our energy makeup.

It took 150 years to build our energy infrastructure, and you don?t replace that overnight. The current weakness in oil prices is a simple repeat of a predictable cycle that has continued for a century and a half. In a couple years, Texas tea will be posting triple digits once again.

I always thought that oil had one more super spike left in it. After that, it will fade into history, reduced to limited applications, like making plastics and asphalt, probably sometime in the 2030?s.

The price for a barrel of oil should then vaporize to $5.

But given the price action for energy and all other commodities I?m starting to wonder if this time I?m wrong.

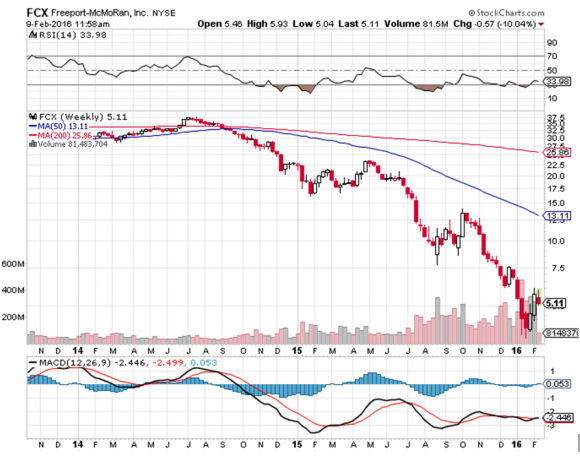

I have watched with utter amazement while Freeport McMoRan (FCX) plunged from $38 to $3. I was gob smacked to see Linn Energy (LINE), admittedly a leveraged play, crater from $32 to 30 cents.

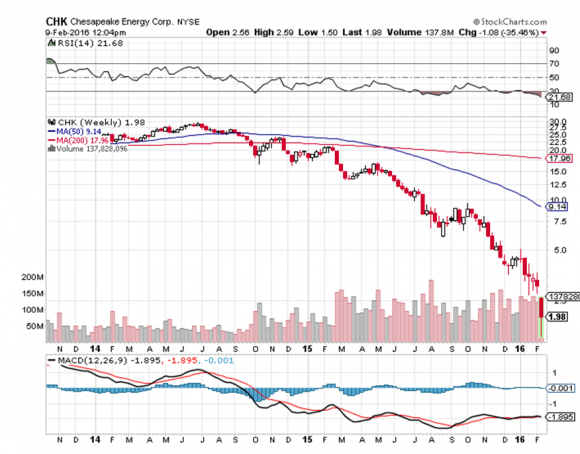

And I was totally befuddled to see gas major Chesapeake Energy (CHK) implode from $65 to $1.

Has the world gone mad?

When the data don?t match your view, it?s time to change your view.

Maybe there won?t be another spike in oil prices. Could its disappearance from the modern industrialized economy have already begun?

That would certainly explain a lot of the recent eye-popping price action in the markets. In five short years oil has dropped 82%. It did this while global GDP grew by 20% and auto sales, and therefore gasoline demand, has been booming.

Of course, you could just call all of this a big giant reversion to the mean.

Over the past 150 years, the average, inflation adjusted price of oil has been $35 a barrel. The price for gasoline has been $2.25 a gallon, exactly where it was in 1932, and where it now is in much of the country.

I know all of these numbers because I once did a study to see if oil prices are rigged (conclusion: they are). How can the price of a commodity stay the same for 150 years?

Wait, the naysayers announce. Things don?t happen that fast.

But they do, my friends, they do, especially in energy.

Until 1849, my ancestors were the largest producers of whale oil on Nantucket Island. (Our family name,? Coffin, was mentioned in ?Moby Dick? seven times, and was a focus of the just released film, ?In the Heart of the Sea.?)

Then this stuff called petroleum came along, wrested from the ground with new technology by men like Drake and Rockefeller. The whale oil market crashed, dropping in price by 90%, and virtually disappeared in two years.

My relatives were wiped out and moved to San Francisco, which they already knew from their whaling days, and where gold had just been found.

A half-century later, this thing called an ?automobile? came along meant to replace the ubiquitous horse and buggy. People laughed. It was loud, noisy, smelly, inefficient, and expensive. Only the rich could afford them.

You had to go to a drug store to buy high priced fuel in one-gallon tins. And it scared the horses. England passed a national automobile speed limit of 5 miles per hour, as cars were considered dangerous.

Then huge oil discoveries were made in Texas and California (watch ?There Will Be Blood?), the Hughes drill bit came along, and gasoline prices fell sharply. Suddenly cars were everywhere. The horse population declined from 100 million to only 1 million today.

All of this is a long-winded, history packed way of saving ?This time it may be different?.

I have on my desktop a Trade Alert already written up to buy the (USO) May, 2016 $9 calls. Today, they traded at $1.00. I?m just waiting for another melt down in oil to take a low risk punt on the long side.

If we rocket back up to $100, as many are predicting, these calls will be worth a fortune. But you know what, oil may only peak out at $44 this time. The trade will still make money, but not as much as in past cycles.

So, you better think hard about loading up on too many oil stocks at these distressed levels. Look what has already happened to the coal industry (KOL), which has essentially gone bankrupt.

You could well be buying into the buggy whip industry circa 1900.

There?s Got to Be a Better Way to Make a Living

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Heart-of-the-Sea-e1455051681747.jpg224400DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2016-02-10 01:08:472016-02-10 01:08:47Oil: Is It Different This Time?

Anyone would be forgiven for thinking that the stock market has become bipolar.

According to the Commerce Department?s Bureau of Economic Analysis, the answer is that corporate profits accounts for only a small part of the economy.

Using the income method of calculating GDP, corporate profits account for only 15% of the reported GDP figure. The remaining components are doing poorly, or are too small to have much of an impact.

Wages and salaries are in a three decade long decline. Interest and investment income is falling, because of the ultra low level of interest rates. Farm incomes are up, but are a tiny proportion of the total. Income from non-farm unincorporated business, mostly small business, is unimpressive.

It gets more complicated than that.

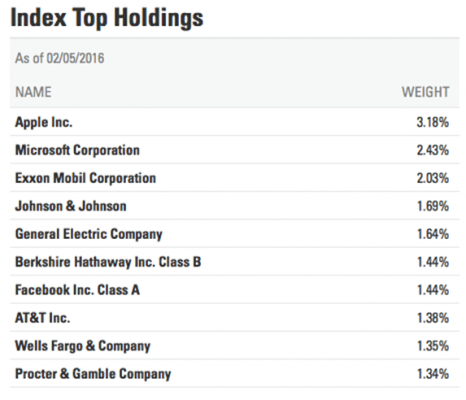

A disproportionate share of corporate profits is being earned overseas. So multinationals with a big foreign presence, like Apple (AAPL), Intel (INTC), Oracle (ORCL), Caterpillar (CAT), and IBM (IBM), have the most rapidly growing profits and pay the least amount in taxes.

They really get to have their cake, and eat it too. Many of their business activities are contributing to foreign GDP?s, like China?s, more than they are here. Those with large domestic businesses, like retailers, earn less, but pay more in tax, as they lack the offshore entities in which to park them.

The message here is to not put all your faith in the headlines, but to look at the numbers behind the numbers. Those who bought in anticipation of good corporate profits last month, got those earnings, and then got slaughtered in the marketplace.

Caveat emptor. Buyer beware.

What?s In the S&P 500?

Has the Market Become Bipolar?

https://www.madhedgefundtrader.com/wp-content/uploads/2015/09/bipolar-masks-e1455046648141.jpg287400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-02-10 01:07:452016-02-10 01:07:45The Bipolar Economy

I?m sitting here at my Lake Tahoe lakefront mansion watching the Dow Average open down 700 points from its Friday intraday high.

It is one of those perfect, picture postcard days, with a blue sky and cobalt lake. The fields outside are covered with snow crystals sparkling in the sunshine.

After the close, I?m going to have to shovel off my outside decks to keep the weight of the ice from collapsing them.

Those (SPY) April $182 puts are looking pretty good this morning, up 50%. They?re hedging all of my remaining long side positions.

In these heart stopping trading conditions it is more important for me to teach you how to avoid doing the wrong thing than pursuing the right thing.

I am therefore going to reiterate my 13 Rules for Trading in 2016. Tape them to the top of your computer monitor, commit them to memory, and maintain iron discipline.

They will save your wealth, if not your health. Here they are:

1) Dump all hubris, pretentions, and stubbornness. It will only cost you money.

2) The market is always right, even if all the prices appear wrong.

3) Only buy the puke outs and sell the euphoria. Do anything in the middle, and you will get whipsawed.

4) Outright calls and puts are offering a far better risk/reward right now than vertical bull and bear call and put spreads, which have a built in short volatility element. It is also better to buy stocks and ETF?s outright with a tight stop loss. This won?t last forever.

5) If you do trade spreads, you can no longer run them into expiration. If you have a nice profit take it, don?t hang on to the last 30 basis points, even if it means paying more commission. The world could end three times, and then recover three times, before the monthly expiration date rolls around.

6) Tighten up your stop loss limits. Not losing money is the key to winning in this market. There is nothing worse than having to dig yourself out of a hole. Don?t run hemorrhaging losses, like the (TBT) from $57.56 down to $37. It will get easy again some day.

7) Buy every foreign crisis and sell every recovery. It really makes no difference to assets here in the US.

8) Several asset classes are becoming untradeable for long periods (bonds, oil, ags). Stay away and stick to the asset classes that are working (stocks and gold).

9) Keep positions small enough to sleep well at night. The doubled volatility will make up for your reduced risk. This is not the time to get greedy and bet the ranch.

10) Turn off the TV and just look at your screens and data. Public entertainers have no idea what the market is going to do, especially if their last job was sports reporting. Their job is to get you to watch the adds for General Motors and TD Ameritrade.

11) As the bull market in stocks enters its seventh year, too many traders, analysts, and strategists have become complacent. You are going to have to work for your crust of bread this year. This is an earnings, technology, and cash flow driven bull, not a QE driven momentum one.

12) It is clear that more money was allocated to high frequency traders this year. That is driving the new, breakneck volatility, increasing stop outs. A sneeze now generates a 500-point intraday move.

13) It is no accident these tempestuous conditions are occurring in an election year. Some $8 billion will be spent on media convincing you how terrible this are.

Better change your password from 12345 to DKFGGIDKFOKBJGELXPEVJBKDLKFBBJFCJCKVLBKGTY69!, and hope that the 69 doesn?t give you away.

Only The Meanest and Toughest are Prospering in This Market

https://www.madhedgefundtrader.com/wp-content/uploads/2014/03/John-Thomas1-e1421097493926.jpg355400DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2016-02-09 01:08:472016-02-09 01:08:47The 13 New Trading Rules for 2016

I spent an evening with Lester Brown, president of the Earth Policy Institute and a winner of the coveted MacArthur Prize, for some long-term thinking about the environment and its investment implications.

Global warming is causing the melting of ice sheets in Greenland and Antarctica, glaciers in the Himalayas, and the Sierra snowpack.

Water tables are falling and fossil aquifers are depleting. In the coming decades this will cause severe shortages of fresh water that could lead to crop failures in India and China, where one billion people depend on mountain runoff to irrigate crops.

California, which delivers 80% of America?s vegetables, is currently suffering one of the worst droughts in history, sending food prices through the roof.?

My preference for local champagne and strawberries just got more expensive.

The fresh water inputs in one person?s food and materials consumption works out to some 2,000 liters a day. That is no typo.

As a result, all food prices will rise over the long term. To head off the greatest threat to the global food supply in human history, we need to cut carbon emissions by 80% before 2020, not 2050, as was discussed in Copenhagen.

This can only be accomplished by redefining food and the environment as national security issue and launching a wartime mobilization.

These difficult goals are achievable. Enough sunlight hits the earth in a day to power the global economy for 27 years. Texas alone has more than 20 gigawatts of wind power operating, under construction, or planned, enough to take 5% of our 250 coal fired power plants offline.

Electricity demand could be cut by 90% purely through greater efficiencies, like switching from incandescent bulbs to LED?s.

Europe could get its entire 300 gigawatt power supply from solar plants in North Africa at current market prices.

Cars powered by wind generated electricity would bring fuel costs down to an equivalent 75 cents a gallon, as electric motors are three times more efficient than internal combustion engines.

While Brown?s predictions are a little extreme for many, they mesh perfectly with my own long term bullish cases for food and water plays. Take another look at the food sector ETF?s, (DBA) and (MOO), and the water space ETF?s (PHO) and (FIW).

https://www.madhedgefundtrader.com/wp-content/uploads/2014/04/Waterfall-e1440505746456.jpg264400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-02-09 01:07:342016-02-09 01:07:34An Environmental Activist?s Take on the Markets

Featured Trade: (THE GREAT AMERICAN ROT IS ENDING), (SPY), (TLT), (FXY), (FXE), (USO)

SPDR S&P 500 ETF (SPY) iShares 20+ Year Treasury Bond (TLT) CurrencyShares Japanese Yen ETF (FXY) CurrencyShares Euro ETF (FXE) United States Oil (USO)

Those of a certain age can?t help but remember that things for the US went to hell in a hand basket after 1963.

That?s when President John F. Kennedy was assassinated, heralding decades of turmoil. Race riots exploded everywhere. The Vietnam War ramped up out of control, taking 60,000 lives, and destroying the nation?s finances. Nixon took the US off the gold standard.

When people complain about our challenges now, I laugh to my self and think this is nothing compared to that unfortunate decade.

Two oil shocks and hyper inflation followed. We reached a low point when Revolutionary Guards seized American hostages in Tehran in 1979.

We received a respite after 1982 with the rollback of a century?s worth of regulation during the Reagan years. But a borrowing binge sent the national debt soaring, from $1 trillion to $18 trillion. An 18-year bull market in stocks ensued. The United States share of global GDP continued to fade.

Basking in the decisive victories of WWII, the Greatest Generation saw their country account for 50% of global GDP, the largest in history, except, perhaps, for the Roman Empire. After that, our share of global business activity began a long steady decline. Today, we are hovering around 22%.

Hitch hiking around Europe in 1968 and 1969 with a backpack and a dog-eared copy of Europe on $5 a Day, I traded in a dollar for five French francs, four Deutschmarks, three Swiss francs, and 0.40 British pounds.

When I first landed in Japan in 1974, there were Y305 yen to the dollar. Even after a strong year, the greenback is still down by 75% against these currencies, except for sterling. How things have changed.

We now live in a world where the US suddenly has the strongest economy, currency and stock market in the world. Are these leading indicators of better things to come?

Is the Great American Rot finally ending? Is everything that has gone wrong with the United States over the past half century reversing?

The national finances are hinting as much. Over the last four years, the federal budget deficit has been shrinking at the fastest rate in history, from $1.4 trillion to only $483 million.

If the economy continues to grow at its present modest 2.5% rate, we should be in balance by 2018. Then the national debt, which will peak at around $18 trillion, will start to shrink for the first time in 20 years.

And since chronic deflation has crashed borrowing costs precipitously, the cost of maintaining this debt has dramatically declined.

A country with high economic growth, no inflation, generationally low energy costs, a strong currency, overwhelming technology superiority, a strong military and political stability is always a fantastic investment opportunity.

It certainly is compared to the highly deflationary, weak currency, technologically lagging major economies abroad.

You spend a lifetime looking for these as a researcher, and only come up with a handful. Perhaps this is what financial markets have been trying to tell us all along.

It certainly is what foreign investors have been telling us for years, who have been moving capital into the US as fast as they can (click here for ?The New Offshore Center: America?).

It gets even better. These ideal conditions are only the lead up to my roaring twenties scenario (click here for ?Get Ready for the Coming Golden Age?), when over saving, under consuming baby boomers enter a mass extinction, and a gale force demographic headwind veers to a tailwind.

That opens the way for the country to return to a consistent 4% GDP growth, with modest inflation and higher interest rates.

Which leads us all to the great screaming question of the moment: Why is the US stock market trading so poorly this year? If the long term prospects for companies are so great, why have shares suddenly started performing feebly?

Not only has it gone nowhere for three months, market volatility has doubled, making life for all of us dull, mean and brutish.

There are a few short-term answers to this conundrum.

There is no doubt that the Euro and the yen have fallen so sharply against the greenback that it is hurting the earnings of multinationals when translated back to dollars.

This has cut S&P 500 earnings forecasts for the year. And these days, everyone is a multinational, including the Diary of a Mad Hedge Fund Trader, where one third of our subscribers live abroad.

Another short-term factor is the complete collapse of the price of oil. Again, it happened so fast, and was so unexpected, that it too is having a sudden deleterious influence of broader S&P earnings.

Go no further than oil giant Chevron, which just announced a big drop in earnings and a massive cut in its capital spending budget for 2016.

The final nail in the Q4 coffin has been bank earnings, which all took big hits in trading revenues. Virtually all were taken short by the huge, one-way rally in bond prices in recent months and the collapse of interest rates.

This happens when panicky customers come in and lift the banks? inventories, and trading desks have to spend the rest of the day, week and month trying to get them back at a loss.

I have seen this happen too many times. This is why the industry always trades at such low multiples.

With no leadership from the biggest sectors of the market, financials and energy, and with the horsemen of technology and biotech vastly overbought, it doesn?t leave the nimble stock picker with too many choices.

The end result is a stock market that goes nowhere, but with a lot of volatility. Sound familiar?

Fortunately, there is a happy ending to this story. Eventually, all of the short-term factors will disappear. Oil prices and bond yields will go back up. The dollar will moderate. Corporate earnings growth will return to the 10% neighborhood. And stocks will reach new highs.

But it could take a while to digest all of this. This is a lot of red meat to take in all at one time. If the market grinds sideways in a 15% range all year, and then breaks out to the upside once again for a 5% annual gain, most investors would consider this a win.

Once again, index investors will beat the pants off of hedge fund managers, as they have for the past seven years.

In the meantime, I doubt the stock indexes will drop more than 6% % from here, with the (SPY) at $189, and we have already seen a 6% hair cut from last year?s peak.?

Knock a tenth off a 16.5 X forward earnings multiple with zero inflation, cheap energy, ultra low interest rates and hyper accelerating technology, and all of a sudden, stocks look pretty cheap again.

As the super sleuth, Sherlock Homes used to say, ?When you have eliminated the impossible, whatever remains, however improbable, must be the truth?.

It?s All Elementary

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Holmes-Watson.jpg308394Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-02-08 01:06:502016-02-08 01:06:50The Great American Rot is Ending

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.