Featured Trade: (FRIDAY, MAY 15 SAN FRANCISCO STRATEGY LUNCHEON) (THE BIG MILESTONE FOR SOLAR), (TAN), (SCTY), (SPWR), (FSLR), (THE CHINA VIEW FROM 30,000 FEET), (FXI), (BABA), (DBC), (DYY), (DBA), (PHO), (TESTIMONIAL)

Guggenheim Solar ETF (TAN) SolarCity Corporation (SCTY) SunPower Corporation (SPWR) First Solar, Inc. (FSLR) iShares China Large-Cap (FXI) Alibaba Group Holding Limited (BABA) PowerShares DB Commodity Tracking ETF (DBC) DB Commodity Double Long ETN (DYY) PowerShares DB Agriculture ETF (DBA) PowerShares Water Resources ETF (PHO)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-04-06 10:03:362015-04-06 10:03:36April 6, 2015

I am writing this to you from a dive boat headed for the Molokini Crater off the coast of Maui in Hawaii. The rolling of the boat makes typing challenging, so please excuse me for more than the usual number of typos.

In the distance farmers are burning off their harvested cane fields, creating giant plumes of smoke, a practice banned in the continental US decades ago.

A pod of dolphins are racing the bow of the boat and humpback whales are blowing their spouts on the horizon. Periodically, the boat scares up a school of flying fish going airborne to find safety.

Life is good.

Another thing I have noticed cruising off the Maui leeward coast is that almost every building has solar roof panels. Of course, the incentive here is huge, as costly imported fuel for power plants makes electricity in Hawaii 20%-50% more expensive than it is on the mainland.

By now, you probably are sick to death of my banging on about the fantastic investment opportunities in the solar industry. But I am not recommending the sector because I wear Birkenstocks, eat organic bean sprouts and recycle even my vegetable waste. Putting money into solar now also makes solid business sense.

Did I also mention that it prevents millions of tons of carbon from entering the atmosphere, or about 5 tons per household per year?

With the stocks expected to rise by ten times over the next decade, you better get ready for more abuse. The solar industry is about to cross an epochal, sea changing benchmark.

Thanks in part to heavy competition from China, South Korea and Japan, the cost of solar panels has collapsed by 75% over the past four years.

Indeed, Chinese flooding of the US market with cheap imported panels almost wiped out every American producer. If you don?t believe me, then check out the long-term stock charts.

More importantly, the cost of industrial, utility sized solar power plants has fallen by 50%.

Only four years ago, large solar power plants made economic sense only after heavy government subsidies were included. They were all part of a ?stimulate the economy and save the world? philosophy demanded by the global economic collapse.

Now we are about to attain the Holy Grail: solar that is profitable on a stand-alone basis.

Don?t get me wrong. Subsidies are nice, as the oil and gas industry well know. I have been sidling up to the trough myself lately with my own solar projects (more on that in a future research piece). But subsidies are no longer the lifeblood of the business.

The economics of solar roof installations are now so compelling, that they are going up everywhere across the country. In fact, everyone on my street has one except me.

That is because the technology, which I keep close track of, is evolving so quickly that it has paid to wait. I did the same when I skipped six track tapes and waited for eight tracks ones, ignored Betamax in favor of VHS, and passed on Windows 1 (which always froze), but soaked up Windows 2.

A solar installation now also protects you from the hefty price increases that will be demanded by your local utility to pay for long overdue infrastructure upgrades.

I am also holding out for the best possible deal (you know me). With one Tesla Model S in the garage, and a Model X on order, I also happen to be one of the largest residential electric power consumers in the state. So, we?re not talking small beer here.

This is starting to have a sizeable impact on the American electricity market. A reader who works for Southern California Edison (SCE/PF) has told me that the cumulative effect of millions of home silicon roof panels is now so great that the traditional daily afternoon power demand spike is starting to disappear.

Even Saudi Arabia is building solar plants now, and they have access to nearly unlimited crude at a mere $5 a barrel.

The Spanish engineering company TSK has just signed a contract with Dubai to build a sizeable, state of the art 100-megawatt photovoltaic plant. The production costs there will work out to just $5.85 a kilowatt hour.

For oil to be competitive with this capital cost, the price would have to stay under $50 a barrel for the next 20 years. Technological advances on stream will make solar competitive at $20 a barrel in a year or two. This explains why some $2.7 billion worth of solar contracts with the Middle East are currently in negotiation.

Oil poor states are rushing even faster to the solar panacea. Jordan is planning to obtain 20% of its power from alternative sources by 2020, while Egypt has set a more ambitious 20% target. Morocco, which I will be visiting this summer, is the most aggressive, with an impressive 42% goal.

All of the means dramatically falling costs and soaring revenue for the solar companies. That sounds like a great business plan to me.

The usual suspects here include First Solar (FSLR), at $11 billion, the largest capitalized behemoth in the industry, and the master of thin film technology. Their power plant near Las Vegas is a sight to behold from the air.

There is Solar City (SCTY), Elon Musk?s highly competitive entry in the field, which will be able to draw from Tesla?s massive $6 billion giga factory in Reno, Nevada.

Sunpower (SPWR) is the Rolls Royce of the solar industry, producing the highest efficiency rated 340-watt panels (thanks to the pure copper substrate), which I will soon be installing in my own home. Love that biochemistry degree!

You could also go risk averse and buy all of them through the Guggenheim Solar ETF (TAN).

The key here is the price of oil, which has unnecessarily dragged down the shares of solar companies over the past nine months. Once it bottoms, if it has not already done so, it will be off to the races.

While your big cap oil majors might add on 40% in value in any recovery, the solars could be in for a tenfold return.

Back to me whale watching. Thar she blows!

Busy Thinking Great Thoughts

https://www.madhedgefundtrader.com/wp-content/uploads/2015/04/Molokini-Crater-e1428328695311.jpg268400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-04-06 10:00:322015-04-06 10:00:32The Big Milestone for Solar

Featured Trade: (FRIDAY, APRIL 17 INCLINE VILLAGE, NEVADA STRATEGY LUNCHEON) (AN UPGRADE FOR THE TESLA SUPERCHARGER NETWORK), (TSLA), (NOTICE TO MILITARY SUBSCRIBERS)

Tesla Motors, Inc. (TSLA)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-04-02 01:06:132015-04-02 01:06:13April 2, 2015

I am writing this to you from Terminal 3 at San Francisco airport, awaiting my flight to Honolulu, Hawaii.

The pilot strides by quickly and purposefully, and I?m wondering if I should stop him for a brief pilot to pilot chat.

How are you feeling? Are you satisfied with your life?

Are you feeling depressed at all?

Hey, did you hear the one about the chicken that crossed the road...?

Two guys walk into a bar, and there?s a duck sitting on a barstool...?

Did you know that the three most often told lies are ?the check is in the mail?, ?I?ll get back to you? and ??

A Protestant, a Catholic and a Jew are sitting next to each other when the engine fails?

My kids quickly talk me out of the idea. They convince me that if I did make it to Hawaii, I probably would only get as far as the Federal Detention Facility in Honolulu. This must be the only family in the world where the kids have to ask the dad to exercise discretion.

But I digress.

No, this is not some kind of April Fool.

You would think that homebuilders would be the worst place in the world to invest right after the biggest bond bull market in history is ending, and interest rates are going to rise.

Not so.

In fact, homebuilders are the current number one pick of Bill Miller, the legendary stock picker at fund manager Legg Mason. He argues strongly that it will be the easiest place to make money in the market for the rest of the decade, with the stocks doubling or more from current levels.

I like the sound of this.

Bill argues that there is a 500,000-unit deficit in homebuilding industry capacity compared to market demand. It trades at a 25% discount to the S&P 500 earnings multiple of 17X. He expects profit growth to run at a 20% annual rate for the next 3-5 years.

And let?s face it. The data out of the real estate industry in February was nothing less that blockbuster. February new home sales were up a red hot 7.8% and January was revised up to a smoking 4%. February pending home sales clocked 6.1% and 12% year on year.

When you see an entire data range catch fire like this, it becomes highly convincing.

This rocketing demand is occurring in the face of shrinking supply. There are now only 1.8 million existing homes on the market in the United States, a 4.6 month supply, close to an historic low. Real estate agents are clamoring for new supply, but the builders are taking their own sweet time.

After a quiescent 2014, home prices in America have started to rise once again.

You would think that anyone going into the homebuilders just as interest rates are starting to increase has a hole in their head. But look at the correlation between rates and homebuilder share prices, and the opposite is true.

When prices began their meteoric rise last year, culminating in an eye popping 1.62% yield on ten year Treasury bonds (TLT) in January, homebuilder stocks looked liked they had Montezuma?s revenge.

Now that rates have backed off, and the Fed has been rattling its saber for more interest rate rises (goodbye ?patience?), the sector has been on fire.

The reason is that the Fed will raise rates only if they see inflation coming. This would be fantastic news for the entire real estate industry, the most reliable inflation hedge out there for the individual investor.

Having your inventory appreciate in value through no effort of your own is also about the best thing that can happen to any developer.

The key to understanding these stocks is that this is not you father?s real estate industry.

Absolutely no one competes for market share anymore. Companies are constructing only enough homes they are certain to sell at high margins. They?re also getting cagier on land acquisition costs.

Hence the shortage.

Look no further than Lennar (LEN). At the top of the last housing cycle in 2005, they built 53,000 houses. In 2015, they will construct only 25,000, but will earn a far greater profit margin on them.

Those firms that reached for market share with leverage were wiped out by the great cleansing of the 2008 crash, or were taken over for pennies on the dollar.

Mind you, the industry still has major challenges. The entry-level buyer is missing in action, as millions of students buckle under crushing debt loads. Some 10% of all homeowners representing 5.4 million units are still underwater on their mortgages, blocking trade ups.

These factors alone explained the market?s and the homebuilder shares lack of sizzle in 2014.

But longer term, the outlook is fantastic.

My ?Golden Age? scenario for the 2020?s makes the homebuilders an absolute sweet spot to be in. A demographic shortfall will make workers scarce, lead to rising wages, and at long last bring a return of inflation. It is a perfect storm for rising home prices.

Could the market already be starting to discount the great things to come in the next decade?

In addition to (LEN), the usual suspects in this sector include Pulte Homes (PHM), KB Homes (KBH), the old Kaufman & Broad (who sold out right at the top) and DR Horton (DHI). You can also contemplate the Real Estate iShares ETF (IYR).

Coming Soon to a Neighborhood Near You

https://www.madhedgefundtrader.com/wp-content/uploads/2015/03/Home-with-Chart-e1427821248483.jpg280400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-04-01 01:03:462015-04-01 01:03:46Get Ready to Load the Boat with Homebuilders

I?ll let you in on my top secret investment strategy that has brought me blockbuster results over the past six years.

Listen to the Wharton Business School?s professor, Jeremy Siegel.

The good doctor has been unremittingly bullish year in and year out, nearly pegging the stock index performance annually.

So, when he says that the Dow Average is going to rise to 20,000 by the end of 2015, that?s good enough for me. In fact Siegel thinks that at current price earnings multiple of 17 times, the bull market has years to run.

It would not be until we hit nosebleed levels of 25X or 30X earnings that he would get worried. And the current ultra low level of interest might even make these high multiple numbers justifiable.

So for the foreseeable future, we are going to see long periods of tedious range trading, followed by frenetic rounds of buying, once the market decides that it is time to discount the next rise in corporate earnings.

We happen to be in one of those range-trading periods right now, which my partner, Mad Day Trader Jim Parker, thinks could last all the way until September.

Actually, it is a little more complicated than that.

There is good reason for the stock market to go to sleep over the next two weeks.

Do you hear that great sucking sound? That is the noise of 170 million tax payers writing checks to the US Internal Revenue Service.

Foreign readers may not realize this, but tax payments are due in the United States on April 15 every year. I would ask for your sympathy, but I know all of you pay far more in taxes than we do. I know, because I used to pay them myself when I lived abroad for 23 years.

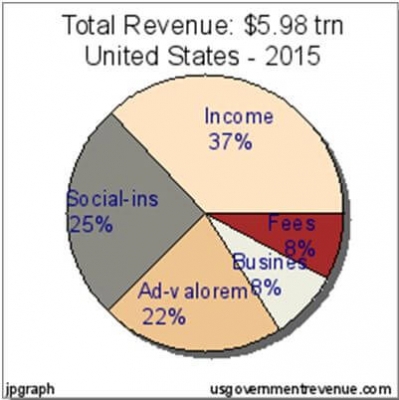

Of the $6 trillion in revenues from all sources due to Uncle Sam in 2015, 37%, or $2.2 trillion will come in the form of individual income taxes. That is a big hit for the financial system. That means for the next two weeks there won?t be any extra money lying around to put into the stock market.

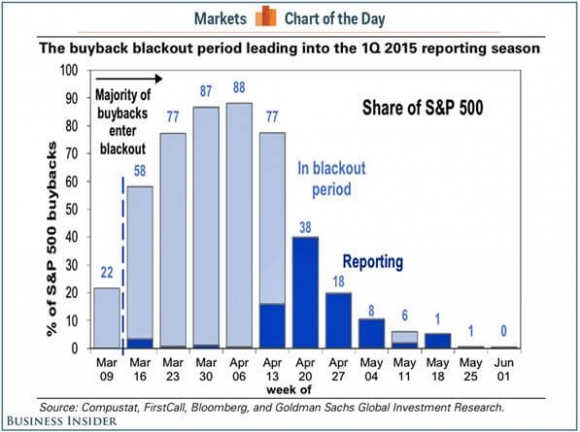

There is another reason why the stock indexes are stagnating here. The Q1, 2015 corporate earnings reporting season kicks off when Alcoa (AA) reports on April 8, or in six trading days. Until then, we are in the quiet period, and companies are not allowed the buy back their own stock.

This is a big deal, since companies buying back their own shares have provided major support for the stock market for many years. Possibly a quarter of all the net cash flow pouring into stocks since 2009 has come from this source.

Take it away, even for a short period, and the most bullish thing the market can do is move sideways, which is exactly what it has been doing for the past two months.

What happens when the tax payment deadline passes and the quiet period ends? Stocks take off like a bat out of hell. That will take us to the spring interim peak.

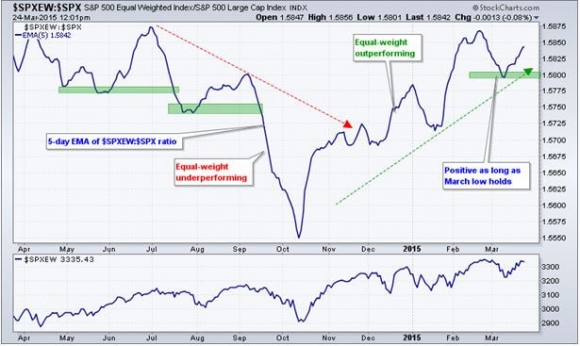

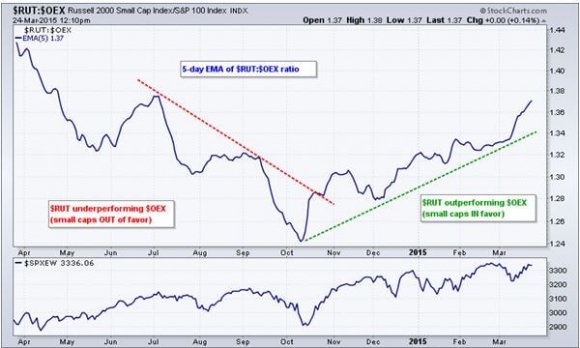

This is why I strapped on three new ?RISK ON? positions last Friday, longs in the Russell 2000 (IWM) and Goldman Sachs (GS) and a short in the euro (FXE).

https://www.madhedgefundtrader.com/wp-content/uploads/2015/03/Shhhh-e1427748076919.jpg300400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-03-31 01:04:342015-03-31 01:04:34Entering the Quiet Time

Come join me for lunch at the Mad Hedge Fund Trader?s Global Strategy Update, which I will be conducting in Honolulu, Hawaii on Friday, April 3, 2015. An excellent meal will be followed by a wide-ranging discussion and an extended question and answer period.

I?ll be giving you my up to date view on stocks, bonds, currencies, commodities, precious metals and real estate. And to keep you in suspense, I?ll be throwing a few surprises out there too. Tickets are available for $208.

I?ll be arriving at 11:30 and leaving late in case anyone wants to have a one on one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at the premier hotel on Waikiki Beach, Honolulu on the island of Oahu. The precise location will be emailed with your purchase confirmation.

As I am unlikely to make it down to Australia and New Zealand this winter, I urge my many followers there who are chock a block with frequent flier points to make the trip up to the balmy Hawaiian Islands to attend the lunch. So should readers in Alaska, British Columbia, Washington state, and Oregon. There are plenty of other things to do there besides listening to the dulcet tones of John Thomas speak.

You can?t lose by renting a car and spending a day driving around the island to experience the lush, fragrant jungle and gigantic crashing waves at Waimea Bay. Pineapple plantations offer an enticing lunch stop.

A visit to the USS Missouri at Pearl Harbor, the site of Japan?s surrender ending WWII, is a must see for history buffs. You can still see the dent in the hull from a crashing Kamikaze plane.

I always try to squeeze in a workout by climbing to the top of Diamond Peak. The surfing instructors at Waikiki Beach are always ready to tune up your skills. A trip to the Polynesian Cultural Center will set you up with dancing natives in grass skirts and a pig roasted on a spit.

While in America?s 50th state, I?ll be renewing my interisland flying skills, renting a plane to fly to Maui, Kauai, and the Big Island. Flying there is so dangerous that the state requires mainland pilots to obtain a special amendment to their licenses, which I have had for the last 40 years.

Among the many challenges there are erupting volcanoes, unbelievable wind shear, sudden tropical thunderstorms and enormous waves that threaten to hit your plane on takeoff and bend your propellers forward. If you crash on Mt. Haleakala, the Park Service will charge you (or your estate) for carting down the wreckage.

And the slightest miscalculation in fuel consumption will find you drifting back to Australia in a life raft, Unbroken style. Don?t worry, they closed the leper colony on Molokai a few years ago.

It?s all worth it just to see the torrential waterfalls cascading off the southern cliffs of Molokai, to catch a pod of migrating humpback whales, or witness one of those amazing tropical sunsets.

I look forward to meeting you, and thank you for supporting my research. To purchase tickets for the luncheons, please go to my online store.

?

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Hula-Dancer.jpg261393Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-03-30 09:58:002015-03-30 09:58:00Last Chance to Attend Friday April 3 Honolulu, Hawaii Global Strategy Luncheon

It?s time to take profits on CytRx Corp., but only if you are a trader. The shares that I first recommended in June, 2014 have just tacked on a healthy 40% over the last three weeks.

However, if you are an investor, hang on. I believe that the biotech boom in the US is only just getting started. The sector should grow from 1% to 20% of US stock market capitalization over the next decade. All major diseases will get cured.

Yes, we will live forever.

CytRx Corp?s cutting edge technology will enable it to continue rising that tsunami.

If there is one complaint about the Diary of a Mad Hedge Fund Trader, it is that I am too short term in my orientation. My response is that this is the only way you can obtain a 163% trading return in 4 ? years.

I can skim off the cream when others can?t.

There is a reason why we are the only investment newsletter that publishes our performance on a daily basis. Basically, all our competitors lose money for their readers. It?s a lot like those Japanese restaurants that display plastic models of their food in the front window, which are inedible.

Still, I like to throw readers ten baggers when I find them. Long-term followers get that warm and fuzzy feeling when I mention Baidu (BIDU) ($12 to $190), Cheniere Energy (LNG) ($5 to $68), Molycorp ($12 to $80), and Tesla (TSLA) ($16 to $260) for a good reason.

Well, I found another ten bagger, one you can just buy and forget about for the next three to five years. I discovered this jewel at the SALT conference in Las Vegas last year organized by my friend, Anthony Scaramucci (click here for ?The Report on the 6th Annual Skybridge Alternatives (SALT) Conference).

At the keynote dinner, I randomly picked a table near the stage. One of the couple next to me wore a UCLA pin where she graduated, prompting a discussion of the Golden Age of Bruin basketball and the salad days of legends John Wooden and Bill Walton (four perfect 30-0 seasons and an 88 game winning streak!).

I casually mentioned I was there as a cancer researcher and DNA scientist during the early 1970?s and graduated in biochemistry. The ears perked up, and the dam broke.

The gentleman I was dining with turned out to be the CEO of CytRx Corp. (CYTR) a revolutionary innovator in the chemotherapy field. Through a top secret, patented chemical reaction, their chemists can add an acid sensitive linker molecule to pre existing generic chemotherapy drug.

That enables the drug to only kill the cancer cells and not the rest of you as well, eliminating side effects, and permitting a substantial ramping up of the dosage. I worked out the chemistry in my mind, and quickly figured out that it would work.

The net effect is to install a turbocharger on existing drugs, greatly enhancing their curative effects. That means lower doses that can cure, with no side effects.

Stage three trials will be completed by 2016, when the company expects full FDA approval. The company has $125 million in cash and no debt.

I lost a wife to cancer 12 years ago, and received a crash update on the state of the science since then. I have been following it ever since, awaiting my turn.

If CytRx is able to pass the FDA gauntlet, then they have found the Holy Grail.

To learn more about the company and obtain the details, please visit their website at http://www.cytrx.com.

Curing of cancer during the 2020?s is a major part of my Golden Age scenario for the coming decade (click here for Here Comes the Next Golden Age).

The kicker here is that there is not just one, but hundreds of companies developing ground-breaking treatments that will come out in the years ahead, many of them located just across the bridge from me. This should collapse the cost of health care for the government, and the rest of us as well.

Remember that buying the shares of a drug company before final approval is always a crapshoot. That last time I did this was with Genentech?s (DNA) Avastin, because I was dating the senior researcher there at the time (tall, long legs, blue eyes, brilliant).

The shares doubled the day they got the green light, and Bank of America flipped from a ?SELL? to a ?BUY? recommendation for the stock on top of a $30 move, tail between legs. That was good.

As we parted ways, the CEO even pushed over his desert, from which his doctor forbade him for health reasons. I gobbled that up as well.

Is CytRx (CYTR) Another Ten Bagger?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/JT-with-Tesla-e1427723768460.jpg227400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-03-30 09:57:002015-03-30 09:57:00Take Profits on CytRx Corp. (CYTR)

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.