Global Market Comments

April 3, 2013

Fiat Lux

Featured Trade:

(APRIL 19 CHICAGO STRATEGY LUNCHEON),

(PULLING THE RIPCORD ON UNITED), (UAL),

(EASTER AT INCLINE VILLAGE)

United Continental Holdings, Inc. (UAL)

Global Market Comments

April 3, 2013

Fiat Lux

Featured Trade:

(APRIL 19 CHICAGO STRATEGY LUNCHEON),

(PULLING THE RIPCORD ON UNITED), (UAL),

(EASTER AT INCLINE VILLAGE)

United Continental Holdings, Inc. (UAL)

Come join me for lunch for the Mad Hedge Fund Trader?s Global Strategy Update, which I will be conducting in Chicago on Friday, April 19. A three-course lunch will be followed by a PowerPoint presentation and an extended question and answer period.

I?ll be giving you my up to date view on stocks, bonds, foreign currencies, commodities, precious metals, and real estate. And to keep you in suspense, I?ll be throwing a few surprises out there too. Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week. Tickets are available for $199.

I?ll be arriving an hour early and leaving late in case anyone wants to have a one on one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at a downtown Chicago venue on Monroe Street that will be emailed with your purchase confirmation.

I look forward to meeting you, and thank you for supporting my research. To purchase tickets for the luncheons, please go to my online store.

Delta announces that revenues grew by only 2% in the last quarter, so of course, they trash United Continental Group (UAL), taking it down 11% from the recent high.? As a former pilot myself, I always allow an extra safety margin separating me from a catastrophic event. This time it came in handy, my deep out-of-the-money call spread limiting my losses to a handful of basis points.

Have no doubt this position will expire in the money. But the share price has crossed that line in the sand of the upper strike price on the call spread. Prudent risk control demands that I bail. I am still up 30% in 2013. There is no point in blowing it on a crappy airline that doesn?t even give you free peanuts back in coach anymore. Or so I heard.

The one mitigating factor here is that those who also strapped on the United Continental Holdings (UAL) April, 2013 $34-$36 bear put spread at $1.76 will now almost certainly take in 68 basis points in profit by running it to the maximum $2 value, cutting the loss on the call spread by half. Such is the value of the hedge. If I had gone with a full 10% weighting on the short side, I would have had the luxury of running both positions into expiration.

After sending you 30 consecutive winning trade alerts, it was just a matter of time before one of these bites you back. Notice that the higher prices go, the more often this will happen. Markets get dizzy, squirrely, and punch drunk at high altitude, no doubt from the shortage of oxygen in the form of fresh new cash flows. Let this be a shot across your bow, that we are entering dangerous, even uncharted territory.

Notice also that we lost money an individual name while the main market continued to ascend. That is the double-edged sword of picking a single sector or company. A one off news event can send your prices spilling while everyone else is laughing all their way to the bank. This happened to me last year with Apple (AAPL). You get double the profit with individual option spreads, but with double the risk. Live by the sword, die by the sword.

It has definitely been a tough year for ski bums, massage therapists, and black jack dealers at Incline Village, Nevada. After getting a prodigious eight feet of snow over one weekend at Christmas, there has been nary a flake since then. Hats off to the Diamond Peak ski resort for trucking down enough snow from the higher elevations to keep the bunny slope running.

However, the real estate business is another kettle of fish. After a six-year hiatus, business is now booming in the High Sierras, as it is throughout the West. Until December, my real estate agent had only sold one house since 2007, and that to me, a nice little foreclosure deal where I picked up a beachfront estate for pennies on the dollar. Since then she has sold six residences, half to Chinese buyers for cash, and has another three in escrow. I guess when it rains, it pours.

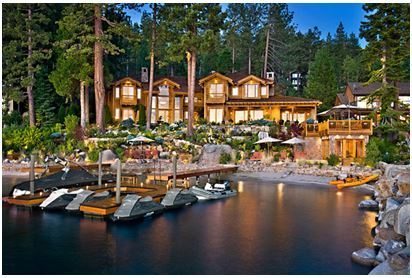

I was surprised to learn that my neighbor, Oracle mogul, Larry Ellison, has placed on the market his nearby Glenbrook compound for $28.5 million. The property includes a six bedroom, eight bathroom 9,242 square foot main house on 2.6 acres, with 230 feet of frontage on the east shore of Lake Tahoe (click here for the listing).

I guess his existing 7.6 acre estate with 420 feet of beachfront next door is enough. Larry has been accumulating ultra high-end properties all over the world for the past two decades, more than he could ever possibly live in. Who knew these were investments, and not conspicuous consumption? This is the first time I have ever seen Larry sell anything. Is this a tell?

You can?t swing a dead cat in Incline Village without hitting a billionaire, so the public events are incredibly well funded. Junk bond king, Michael Milliken, pays for the Fourth of July fireworks, as the celebration falls on his birthday. On Sunday, the ski slopes were amply planted with plastic eggs, some containing candy, others, free lift tickets. Even the pet hospital here is better equipped than most public hospitals.

So I knew the Easter egg hunt would not disappoint. Perhaps, the eggs contained real gold coins. I have to tell you that it was a total blast wading through 500 hyped up children. Click here for the video of the event and hit the ?PLAY? arrow, if for no other reason than to admire the spectacular Lake Tahoe scenery.

Global Market Comments

April 2, 2013

Fiat Lux

Featured Trade:

(APRIL 12 SAN FRANCISCO STRATEGY LUNCHEON),

(THE US DOMINANCE IN HIGHER EDUCATION),

(AN EVENING WITH JAMES BAKER III),

(THE CORN CRASH CONTINUES),

(CORN), (WEAT), (SOYB), (DBA)

Teucrium Corn (CORN)

Teucrium Wheat (WEAT)

Teucrium Soybean (SOYB)

PowerShares DB Agriculture (DBA)

Come join me for lunch at the Mad Hedge Fund Trader?s Global Strategy Update, which I will be conducting in San Francisco on Friday, April 12, 2013. An excellent meal will be followed by a wide-ranging discussion and an extended question and answer period.

I?ll be giving you my up to date view on stocks, bonds, currencies, commodities, precious metals, and real estate. And to keep you in suspense, I?ll be throwing a few surprises out there too. Tickets are available for $189.

I?ll be arriving at 11:00 and leaving late in case anyone wants to have a one on one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at a private club in downtown San Francisco near Union Square that will be emailed with your purchase confirmation.

I look forward to meeting you, and thank you for supporting my research. To purchase tickets for the luncheons, please go to my online store.

I spent the weekend attending a graduation in Washington State, a stone?s throw from where the 2010 Winter Olympics were held. While sitting through the tedious reading of 550 names, and listening to the wailing bagpipes, I did several calculations on the back of the commencement program.

I came to some startling conclusions. Higher education has grown into a gigantic industry, with a massively positive impact on America?s balance of payments, generating an impact on the world far beyond the dollar amounts involved. There are 671,616 foreign students in the US (90,000 from China alone) paying an average out-of-state tuition of $25,000 each, creating a staggering $16.8 billion of payments a year.

On a pro rata basis, that amounts to a serious part of our total surplus in services in 2011 of $188 billion, not far behind financial services (click here for the Bureau of Economic Analysis site). A fortunate few, backed by endowed chairs and buildings built by wealthy and eager parents, land places at prestigious Universities like Harvard, Princeton, Yale, and the University of California at Berkeley. The overwhelming majority, however, enroll in the provinces in a thousand rural state universities and junior colleges that most of us have never heard of.

The windfall has enabled once sleepy little schools to build themselves into world class institutions of higher learning with 30,000 or more students, boasting state of the art facilities, much to the joy of local residents and state education officials. Furthermore, this dominance of education industry is steadily Americanizing the global establishment.

I can?t tell you how many times over the decades I have run into the Persian Gulf sovereign fund manager who went to Florida State, the Asian CEO who attended Cal State Hayward, or the African finance minister who fondly recalled rooting for the Kansas State Wildcats.

Those who constantly bemoan the impending fall of the Great American Empire can take heart by merely looking inland at these impressive degree factories. It also might give them an explanation of why the dollar is so strong in the face of absolute gigantic and perennial trade deficits.

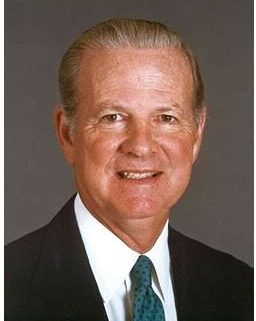

?We have 3,500 nuclear weapons left over from the cold war we don?t need, they take 20 seconds to re-aim, we?re not afraid to use them. And by the way, they?re already aimed at you.? That is the approach James Baker III thinks America should take with Iran, Ronald Reagan?s Chief of Staff and Secretary of the Treasury and George H.W. Bush?s Secretary of State.

At the same time we should be talking to the regime in Tehran, while doing everything we can to support the reformers, tighten sanctions, and enlist Europe?s help. Baker does not see a military solution in Iran, even though their potential to create instability in the region is enormous. This was one of dozens of amazing insights I gained chatting with the wily Texas lawyer during an evening in San Francisco.

Baker is happy to take on the ?America Bashers?, pointing out that the US still plays a dominant role in the UN, NATO, the IMF, and the World Bank. It accounts for 25% of global GDP, and its military is unmatched. The US spread globalization, and the spectacular growth of China and India is largely the result of open American trade policies, raising standards of living globally.

But the US can?t take its leadership role for granted. The biggest threats to American dominance are the runaway borrowing and entitlements. US debt to GDP will soar to over 100% in the near future, the highest level since WWII. This is unsustainable, is certain to bring a return of inflation, and unless dealt with, will lead to a long term American decline on the world stage.

Massive trade and capital flow imbalances also have to be addressed. The 82-year-old ex-Marine, who confesses to being the only Treasury Secretary in history who never took an economics class, believes that the advantageous rates that the government now borrows at are not set in stone.

Baker is the man who engineered an end to the cold war with a whimper, and not a bang. He thinks that ?even our power has its limits,? and that there is a risk of strategic overreach.? With the US politically evenly divided, Congress has degenerated from debating teams into execution squads, and consensus is impossible. The media are partly to blame, especially bloggers who propagate wild conspiracy theories, as confrontation sells better than accommodation.

Regarding the financial crisis, we need to end ?too big to fail? and embark on re-regulation, not strangulation. All in all, it was a fascinating few hours spent with a piece of living history who still maintains his excellent contacts in the diplomatic and intelligence communities.

Pit traders of the ags are bruised, battered, and broken, in the wake of Thursday?s US Department of Agriculture crop report showing that there is a whole lot more food out there than anyone imagined possible.

Corn was the real shocker. It has long been a nostrum in the ag markets that high prices cure high prices, and that is exactly what is happening now. In the wake of last summer?s spectacular drought induced shortages, which saw corn prices nearly double, farmers rushed to expanding plantings in 2013. The government expects that some 97.3 million acres will be sown this year, the most since the Dust Bowl days of 1936.

The government agency boosted estimates of stockpiles nearly 10%, from 5 to 5.4 billion bushels. Demand from ethanol makers has collapsed as they have priced themselves out of the market, leading to the closure of nearly 10% of the country?s fermenting facilities. Purchases by ranchers as feedstuff for cattle have been weak. These are enormous upward revisions. Prices took a 10%, limit move down on Friday, and are taking another dive today.

Even though the numbers were not as dramatic for the other grains, their prices suffered as well. Some of the new corn is being grown at the expense of soybeans, which saw a small decline in plantings. But prices took a dump anyway. Wheat (WEAT) has amazingly dropped below the summer, 2012 lows. The ag ETF (DBA), which includes the machinery and fertilizer companies, has performed the worst of all, and is threatening a new three year low. Virtually the entire 2012 ag bubble has been given back.

The long term bull case for food could not be more compelling (click here for ?Is Food the New Distressed Asset??). The world is producing people faster than the food to feed them. The global population is expected to rise from 7 to 9 billion by 2050. Half of that increase will happen in countries that are unable to feed themselves, like the Middle East.

Food consumption in the US isn?t dropping anytime soon. According to Yahoo data, ?Plus sized swimsuits? searches were up 530% in March.

There is also a huge emerging market play here. Rising standards of living mean better diets. Better food requires more calories and water to grow. To raise one pound of beef, you need 2,200 gallons of fresh water. It is true that if everyone in China eats one extra egg a day, the entire continent of Africa has to starve.

I have been ignoring the ags since last summer, when, if you didn?t get in during the first week, you missed the entire drought play. Since then I dipped in on the short side in corn, playing the slow unwinding of the price bubble.

With this collapse, the long side is now, at last, back on the table. Let the current selloff shake itself out. Then, take a look at some long plays in case the global warming trade returns this summer. Nine of the ten past years have been the hottest in history. Why should this year be any different? If Texas governor, Rick Perry, says something isn?t happening with the environment, you can pretty much count that it is.

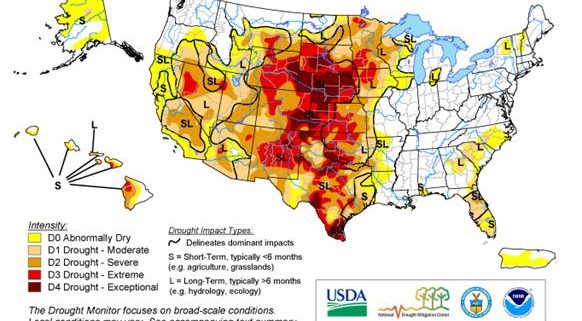

If you have any doubts, take a look at the latest drought monitor map below, which shows long-term arid conditions persisting in most of the Midwest.

Come join me for lunch at the Mad Hedge Fund Trader?s Global Strategy Update, which I will be conducting in Las Vegas, Nevada on Wednesday, May 8, 2013. An excellent meal will be followed by a wide-ranging discussion and an extended question and answer period.

I?ll be giving you my up to date view on stocks, bonds, currencies, commodities, precious metals, and real estate. I will also explain how I have been able to deliver a blowout 40% return since the November, 2012 market bottom. And to keep you in suspense, I?ll be throwing a few surprises out there too. Tickets are available for $179.

I?ll be arriving at 11:00 and leaving late in case anyone wants to have a one on one discussion, or just sit around and chew the fat about the financial markets. The PowerPoint presentation will be emailed to you three days before the event.

The lunch will be held at a major Las Vegas hotel on the Strip, the details will be emailed with your purchase confirmation. Please make your own hotel reservations, as business there is booming.

I look forward to meeting you, and thank you for supporting my research. To purchase tickets for the luncheons, please go to my online store.