No Fed Action Disappoints QE Bulls

It?s always nice when intelligent people agree with you. That was my feeling after the Federal Reserve gave notice today that it was downgrading its forecast of US economic growth for 2012 from 2.6% to 2.15%. That is a major step down from the 3% and higher predictions they were hanging on to earlier.

The news came in the written statement that followed the Fed?s somewhat disappointing decision today. As I expected, there will no QE3. The Fed needs to keep dry powder in case we get another market crash, possibly as early as this summer. Operation ?twist? was renewed for another year, but wasn?t extended to include mortgage backed securities. It was about as conservative of a conclusion one could have expected from the Fed, given the rapidly deteriorating economic data flow that I chronicle daily in these pages.

It brings the August panel of respected central bankers in line with my own 2% expectation, which I have been posting since January. Here?s a good rule of thumb from a four decade long Fed watcher: they are always behind the curve, sometimes way behind, often by a year or more.

The problem for you is that 2% is not my forecast anymore. As of today, I am ratcheting it down to 1.5%. Without a QE3 it is really hard to see where additional growth is going to come from this year. US corporations are producing record profits and sitting on mountains of cash, so they have absolutely no incentive to stick their necks out whatsoever. Additional government spending is hamstrung by an election year and a gridlocked congress.

Virtually the entire international arena is slowing, in some cases dramatically so. China is about to bust through the bottom of its target growth range at 7%, down from 13% a few years ago. Tsunami reconstruction spending in Japan has just about run its course. Europe is clearly in a major recession. Even powerhouse, Germany, is shrinking from 2% growth to 1% because of weakness in its major export markets.

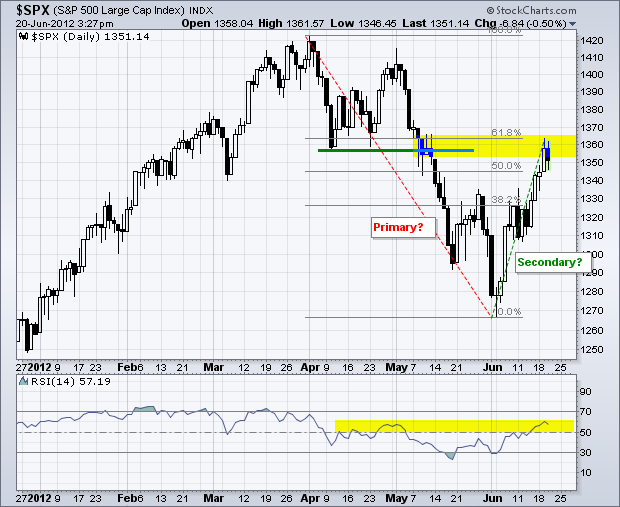

The market implications of this lower growth rate are many. It means that the recent 100 point rally in the S&P 500 was built on so much hot air and false hope. It was never driven by more than a round of furious short covering and profit taking. Let the permabulls enjoy a few more days of summer, possibly taking the index as high as 1,400 by month end.

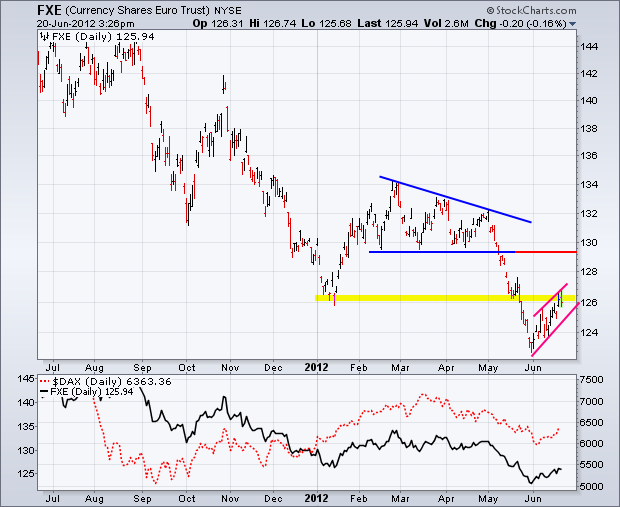

It also means that another round of pain for the Euro (FXE) (EUO) is not far off. The best case for Treasury bonds (TLT) is that they churn sideways until the next Fed meeting in six weeks. In the worst case, the spike up to challenge the old highs, taking yields up to 1.42% for the ten year once more.

The lows for the year haven?t been put in yet, but they are about to. Before, we had a 4% GDP stock market and a 2% GDP economy. Now we have a 4% GDP stock market and a 1.5% GDP real economy. Watch out below. The only question is whether 1,250 in the (SPX) holds this time, or whether we have to plumb the depths of 1,200 before the penance is paid for our hubris.

Sorry Guys, No QE3 Today