Global Market Comments

January 4, 2013

Featured Trades: (LUNCH WITH THE TREASURY SECRETARY)

Global Market Comments

January 4, 2013

Featured Trades: (LUNCH WITH THE TREASURY SECRETARY)

When I wake up at 4:30 am each morning to check the overnight markets and review the opening salvo of incoming emails, I often have trouble focusing in my groggy state. So I had to blink twice when the first message in my inbox politely inquired if I had time to meet the Secretary of the Treasury in Palo Alto for lunch that day, apologizing for the short notice.

Tim Geithner was in San Francisco for a day to meet with a small group of venture capitalists and other business leaders. I can?t say who else was invited. Suffice it to say that I was the only one without an NYSE or NASDAQ listing.

When I greeted the lithe, athletic, but diminutive Treasury Secretary, I could see the six secret service agents in the room visibly tense up. At 6?4? I towered over him, but he shook my hand firmly. I knew he was an avid surfer, and asked if he had stowed his board on Air Force One so he could shoot ?Steamer Lane? in nearby Santa Cruz after the meeting. He laughed, confessing that he rode the waves in a less than adequate fashion.

Geithner succinctly laid out the administration?s position on a wide range of financial and economic issues. The economy is now healing, has been growing for 20 months, but conditions were still very tough, especially if you were in construction, real estate, or small banks. Private sector investment grew 20% in H1, but then slowed down to 10% in H2. Exports are strong.

The economy is undergoing some difficult, but necessary changes. The crisis was caused by excessive debt levels, the adjustment of which is now mostly behind us. The savings rate has soared from below 0% before the crisis to 4%-6% today. The debt burden is falling. Still, further measures are required.

Geithner thrilled his audience by proposing a permanent investment tax credit for domestic R & D. On top of that, he wants to add a one year tax credit for capital investment. It was music to the ears of those present, who were primarily engaged in the business of starting new companies. He would also eliminate tax preferences that encouraged companies to build plants overseas. At the very least, the playing field should be level.

Stepped up spending on infrastructure is a big priority, which has suffered from decades of neglect and under investment. The US is not a country with unlimited resources, and this is where the taxpayer gets the highest return on money spent. He also highlighted the urgency to extend tax cuts for the bottom 98% of the working population. The country entered the crisis with an unsustainable fiscal situation, and this would help address that.

Geithner says that the US would not engage in a debasement of its currency. It is very important that our counterparties believe that we will fulfill our long term obligations. The US benefits from the dollar being used as a reserve currency, and there will be no non-dollar reserve currency in our lifetimes.

The Dodd-Frank bill was an essential reform, as a huge financial industry had grown up outside the existing rules. Banks needed bigger shock absorbers. Governments do a very bad job at picking industries to protect, which only supports the weak at the expense of consumers.

Geithner said that by any measure, the Chinese Yuan was undervalued, and that was unfair to all of the country?s trading partners. Although this was enabling China to reap short-term benefits, long term it meant that the US was setting its monetary policy. A flexible exchange rate would give China economic independence and soften the impact of imported inflation. When asked what exchange rate he would be happy with, he would only say ?HIGHER?.

The 49-year-old Geithner has devoted much of his life to public service. He spent his childhood abroad while his father was a micro finance administrator for the Ford Foundation, growing up in Zimbabwe, Indonesia, and India, and finally graduating from high school in Bangkok. He did his undergrad at Dartmouth, and obtained a master?s in Asian studies at Johns Hopkins, where he gained fluency in Chinese and Japanese. I first met Tim myself two decades ago, when he was a low level Treasury attach? at the Tokyo embassy who spoke the local language flawlessly. After that, his rise was meteoric, from Undersecretary of the Treasury for International Affairs, to President of the New York Fed, to his current gig.

Geithner put on quite the performance. No matter what the question, he was able to caste it in the context of its historical background, the lead up over the past two decades, the current policy response, and parallels with other major and minor countries. We jumped from the Japanese stagnation, to the Swedish banking crisis in the early nineties, to Indonesia?s explosion of hyperinflation in the sixties, to the Mexican debt crisis, all within a minute. His canned answers to standard question rolled effortlessly off his tongue, while original problems delivered an intensity of thought one rarely sees.

Before he left, I pulled out all the cash in my wallet and pointed out to Geithner that while I had bills signed by previous Treasury Secretaries Larry Summers, Paul O?Neil, and Robert Rubin, I lacked one with his illegible scrawl. Did he have any which he could exchange with me? He sheepishly admitted that while such bills existed, they we being held back from circulation until the Treasury?s existing stockpile of Hank Paulson bills ran out, in order to deliver taxpayers good value for money. I would only see his bills once the economy recovers and the growth of M1 starts to accelerate. That is truly an answer one would expect from the 75th Treasury Secretary.

Quote of the Day

?If You?ve lived long enough on Wall Street, you know that we shoot out wounded and eat our young,? said Brad Hintz, an analyst with Sandford Bernstein.

As a potentially profitable opportunity presents itself, John will send you an alert with specific trade information as to what should be bought, when to buy it, and at what price. Read more

As a potentially profitable opportunity presents itself, John will send you an alert with specific trade information as to what should be bought, when to buy it, and at what price. Read more

Global Market Comments

January 3, 2013

SPECIAL FOREIGN CURRENCY ISSUE

Featured Trades:

(LONG TERM DOLLAR TREND),

(FXA), (FXC), (BNZ), (CYB), (FXE)

(THE COMING COLLAPSE OF THE YEN),

(THE BIG MAC INDEX), (MCD

CurrencyShares Australian Dollar Trust

CurrencyShares Canadian Dollar Trust

WisdomTree Dreyfus New Zealand Dollar

WisdomTree Dreyfus Chinese Yuan

CurrencyShares Euro Trust

Any trader will tell you the trend is your friend and the overwhelming direction for the US dollar for the last 220 years has been down.

Our first Treasury Secretary, Alexander Hamilton, found himself constantly embroiled in sex scandals. Take a ten-dollar bill out of your wallet and you?re looking at a world class horndog, a swordsman of the first order. When he wasn?t fighting scandalous accusations in the press and the courts, he spent much of his six years in office orchestrating a rescue of our new currency, the US dollar.

Winning the Revolutionary War bankrupted the young United States, draining it of resources and leaving it with huge debts. Hamilton settled many of these by giving creditors notes exchangeable for then worthless Indian land west of the Appalachians. As soon as the ink was dry on these promissory notes, they traded in the secondary market for as low as 25% of face value, beginning a centuries long government tradition of stiffing its lenders, a practice that continues to this day. My unfortunate ancestors took him up on his offer, the end result being that I am now writing this letter to you from California?and am part Indian.

It all ended in tears for Hamilton, who, misjudging former Vice President Aaron Burr?s intentions in a New Jersey duel, ended up with a bullet in his back that severed his spinal cord. Cheney, eat your heart out.

Since Bloomberg machines weren?t around in 1790, we have to rely on alternative valuation measures for the dollar then, like purchasing power parity, and the value of goods priced in gold. A chart of this data shows an undeniable permanent downtrend, which greatly accelerates after 1933 when FDR banned private ownership of gold and devalued the dollar.

Today, going short the currency of the world?s largest borrower, running the greatest trade and current account deficits in history, with a diminishing long term growth rate is a no brainer. But once it became every hedge fund trader?s free lunch and positions became so lopsided against the buck, a reversal was inevitable. We seem to be solidly in one of those periodic corrections, which began six month ago, and could continue for months or years.

The euro has its own particular problems, with the cost of a generous social safety net sending EC budget deficits careening. Use this strength in the greenback to scale into core long positions in the currencies of countries that are major commodity exporters, boast rising trade and current account surpluses, and possess small consuming populations. I?m talking about the Canadian dollar (FXC), the Australian dollar (FXA), and the New Zealand dollar (BNZ), all of which will eventually hit parity with the greenback. Think of these as emerging markets where they speak English, best played through the local currencies.

For a sleeper, buy the Chinese Yuan ETF (CYB) for your back book. A major revaluation by the Middle Kingdom is just a matter of time.

I?m sure that if Alexander Hamilton were alive today, he would counsel our modern Treasury Secretary, Tim Geithner, to talk the dollar up, but to do everything he could to undermine the buck behind the scenes, thus over time depreciating our national debt down to nothing through a stealth devaluation. Given Geithner?s performance so far, I?d say he studied his history well. Hamilton must be smiling from the grave.

?Oh, how I despise the yen, let me count the ways.? I?m sure Shakespeare would have come up with a line of iambic pentameter similar to this if he were a foreign exchange trader. I firmly believe that a short position in the yen should be at the core of any hedged portfolio for the next decade. To remind you why you hate the Japanese currency, I?ll refresh your memory with this short list:

* With the world?s weakest major economy, Japan is certain to be the last country to raise interest rates.

* This is inciting big hedge funds to borrow yen and sell it to finance longs in every other corner of the financial markets.

* Japan has the world?s worst demographic outlook that assures its problems will only get worse. They?re not making Japanese any more.

* The sovereign debt crisis in Europe is prompting investors to scan the horizon for the next troubled country. With gross debt approaching 200% of GDP, or 100% when you net out inter agency crossholdings, Japan is at the top of the list.

* The Japanese long bond market, with a yield of 0.1.2%, is a disaster waiting to happen.

* You have two willing co-conspirators in this trade, the Ministry of Finance and the Bank of Japan, who will move Mount Fuji if they must to get the yen down and bail out the country?s beleaguered exporters.

When the big turn inevitably comes, we?re going to ?100, then ?120, then ?150. That works out to a price of $40 for the (YCS), which last traded at $16.35. But it might take a few years to get there. The Japanese government has some on my side with this trade, not that this is any great comfort. Four intervention attempts have so been able to weaken the Japanese currency only for a few nanoseconds.

If you think this is extreme, let me remind you that when I first went to Japan in the early seventies, the yen was trading at ?305, and had just been revalued from the Peace Treaty Dodge line rate of ?360. To me the ?84 I see on my screen today is unbelievable. That would then give you a neat 15-year double top.

It's All Over For the Yen

It's All Over For the Yen

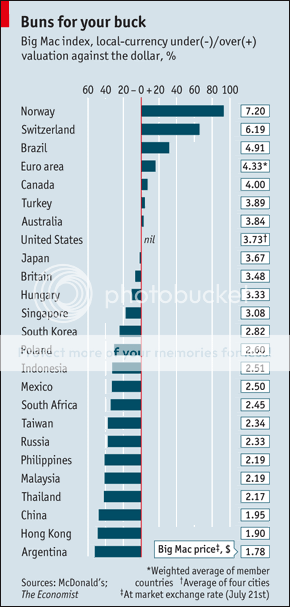

My former employer, The Economist, once the ever tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its ?Big Mac? index of international currency valuations (click here for the link).

Although initially launched as a joke three decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success. The index counts the cost of McDonald?s (MCD) fat and sodium packed premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss Franc, the Brazilian Real and the Euro are overvalued, while the Hong Kong Dollar, the Chinese Yuan and the Thai Baht are cheap. I couldn?t agree more with many of these conclusions. It?s as if the august weekly publication was tapping The Diary of the Mad Hedge Fund Trader for ideas. I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my ass. Better to use it as an economic forecasting tool, than a speedy lunch.

The Big Mac in Yen is Definitely Not a Buy

?At some point in 2013, knuckles are going to be turning white and we?ll see whatever rabbits Ben Bernanke is going to have to pull out of his hat?, said David Rosenberg of Gluskin, Sheff in Associates