Global Market Comments

March 18, 2026

Fiat Lux

Featured Trade:

(JOIN ME ON CUNARD'S QUEEN MARY 2 FOR MY JUNE 19 TRANSATLANTIC SEMINAR AT SEA LUNCHEON)

Global Market Comments

March 18, 2026

Fiat Lux

Featured Trade:

(JOIN ME ON CUNARD'S QUEEN MARY 2 FOR MY JUNE 19 TRANSATLANTIC SEMINAR AT SEA LUNCHEON)

"The things that affect the investment world so profoundly are the things that were not foreseen. If they could be foreseen ... anticipated and adjusted to and factored into prices, they wouldn't have that cataclysmic effect," said legendary investor Howard Marks of Oaktree Capital.

In 1987, I was drinking whisky in a Ginza bar with a senior trader from one of Japan's largest brokerages. He was celebrating. His firm's stock had just hit a new all-time high, trading at a valuation that made even the most optimistic analysts uncomfortable.

I asked him what justified the premium. He swirled his glass and said, simply, "reputation." I've never forgotten that answer. Not because he was wrong, exactly, but because he wasn't entirely right either. Sometimes a premium is justified. Sometimes it isn't.

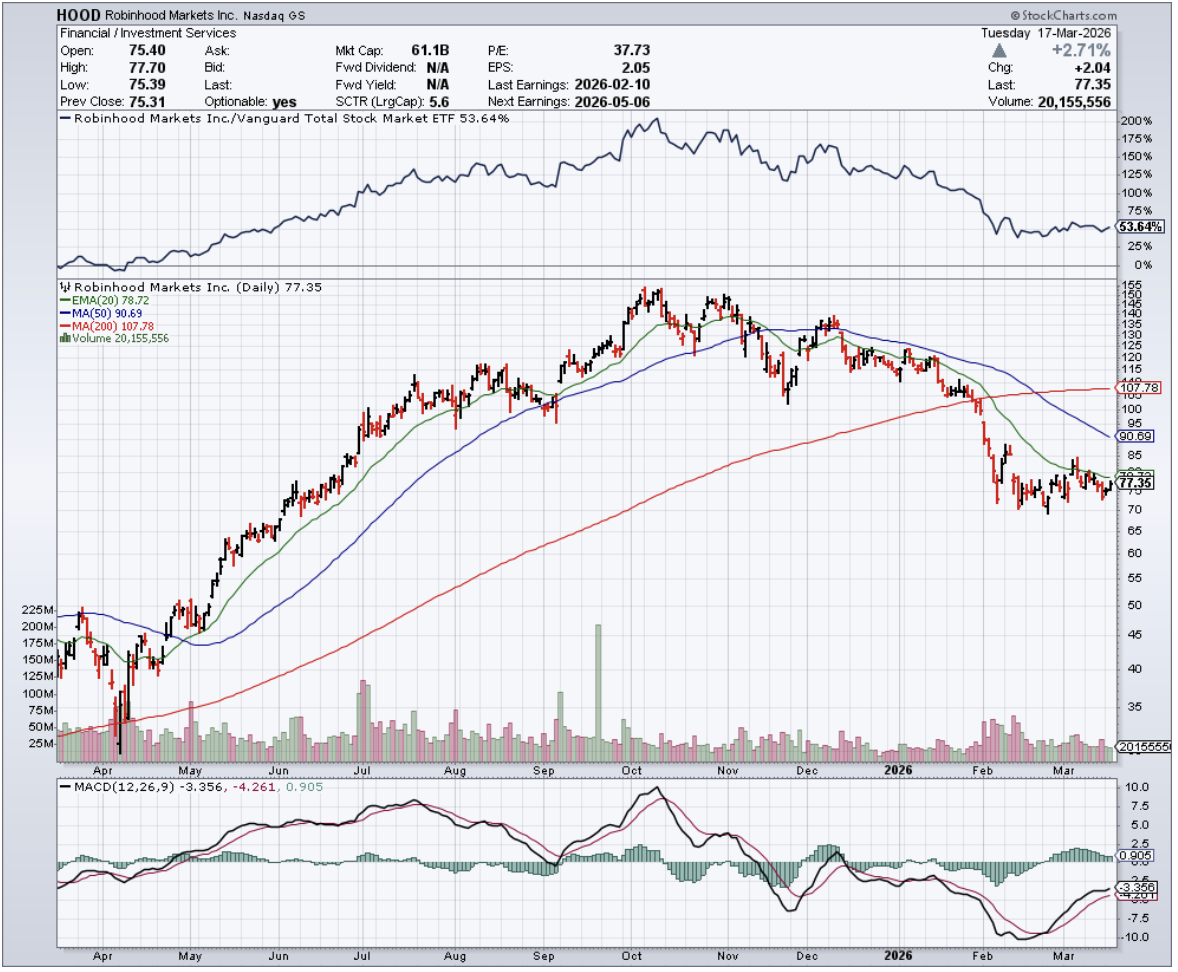

Right now, the same question is worth asking about Coinbase (COIN) and Robinhood (HOOD).

Both companies are legitimate ways to play the ongoing institutionalization of crypto. Both will benefit when Bitcoin (BTC) regains momentum. The sector itself is not in question here.

What’s worth examining carefully is what you are paying for each, and whether the gap between them reflects a genuine difference in business quality or simply a difference in name recognition.

Start with the similarities, because they are more significant than most investors appreciate.

Both companies derive the majority of their revenues from transaction fees that surge in crypto bull markets and compress when sentiment turns.

Both are actively diversifying away from that cyclicality.

Both face identical regulatory headwinds and competitive pressures from exchanges operating with far lower cost structures.

In a genuine crypto winter, neither balance sheet emerges unscathed. The risk profiles are, in practical terms, closer than the valuations suggest.

Coinbase trades at roughly 51x forward earnings. Robinhood trades at 29x. That 75% premium deserves scrutiny in either direction.

The case for Coinbase's premium is valid.

COIN has quietly become the dominant institutional custodian for the Bitcoin and Ethereum (ETH) spot ETFs - a recurring, relationship-driven revenue stream that carries genuine stickiness.

Its subscription and services division generated $727 million in Q4 2025, encompassing stablecoin income, blockchain rewards, and custody fees.

The institutional transaction revenue adds another layer of predictability that a purely retail-facing broker cannot replicate. These are structural advantages, not marketing talking points.

The honest counterpoint is that Coinbase's defensive revenues are somewhat less defensive than the label implies.

Stablecoin income, blockchain rewards, and custody fees all maintain meaningful correlation to the broader crypto cycle.

When the market cooled through 2025, total Coinbase revenue swung significantly quarter to quarter despite the diversified revenue presentation. The subscription line smooths the volatility at the edges without eliminating it at the core.

Investors pricing COIN as though the institutional franchise insulates it from crypto sentiment are likely getting ahead of themselves.

Robinhood's story is quieter, but the numbers are interesting.

Equities, options, RIA assets, and subscription services now contribute as meaningfully to HOOD's top line as crypto transaction fees - a genuine diversification that the market has been slow to fully credit.

In Q4 2025, crypto transaction revenue fell 18% sequentially, and total net revenue still grew 27% year over year.

Expenses grew more slowly than revenue. Margins expanded. Consensus has HOOD growing revenue 28% over the next twelve months against COIN's 9%, and for 2026, the divergence widens further - HOOD at 21% growth against Coinbase at negative 14%.

One additional data point worth noting involves shareholder economics.

Coinbase's stock-based compensation creates a meaningful spread between its GAAP and non-GAAP earnings. The forward GAAP P/E sits at 48x against the non-GAAP 32.8x.

Robinhood's equivalent spread runs from 32x to 26.7x. Neither figure is disqualifying, but the difference in dilution trajectory is worth factoring into any long-term hold thesis.

So, where does that leave those trying to allocate intelligently across this space?

Coinbase offers institutional credibility, a maturing custody franchise, and exposure to stablecoin infrastructure that could prove enormously valuable as crypto payments scale.

Robinhood offers superior near-term growth, expanding margins, and a diversification story that is already showing up in the reported numbers rather than future slide decks.

The premium separating them is either a fair reflection of Coinbase's structural moat or an overhang waiting to compress - and reasonable people are currently sitting on both sides of that argument.

My old friend from the Ginza bar was right that reputation matters. What he never quite resolved, nursing that whisky, was exactly how much it should cost.

Global Market Comments

March 17, 2026

Fiat Lux

Featured Trade:

(HOW TO HANDLE THE FRIDAY, MARCH 20, OPTIONS EXPIRATION),

(SPY), (RTX), (BA), (CAT), (GLD)