When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-08-05 13:05:232024-08-05 13:05:23Trade Alert - (CAT) August 5, 2024 - STOP LOSS - SELL

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

U.S. Markets turned down sharply last Friday after the July nonfarm payroll revealed the highest unemployment rate since 2021, catching many by surprise.(If you had read my Monday, July 29 newsletter last week, you would have already known we were in a Wave 4 down period and would have been aware of the targets).Many stocks were absolutely battered, including Intel.No sector was left untouched.Yields fell, and the TLT rallied strongly.But you knew all this was about to happen – you had been forewarned.

The US dollar depreciated against all major currencies, with particularly steep declines against traditionally risk-off currencies like the Swiss franc (CHF) and the Japanese yen (JPY).In response to this data, markets are now pricing in steep rate cuts – as many as 150 basis points – from the Federal Reserve by year’s end.( I said earlier in the year that the slowdown in the economy would show up in the second half of the year and steamroll its way through the economy like a ball falling down a hill, gathering momentum as it fell, and this is exactly what is showing up in the data now – the economy is slowing faster than most realize, and the Fed is where it was when it went to raise rates -slow to the party - and will now be expected to act aggressively.)

All Aussies will be watching the Reserve Bank on Tuesday.No change is expected, but many are hoping for a rate cut.

Economic data points from China, including the trade balance and inflation figures, will give some insight into an economy that is still struggling post-pandemic.

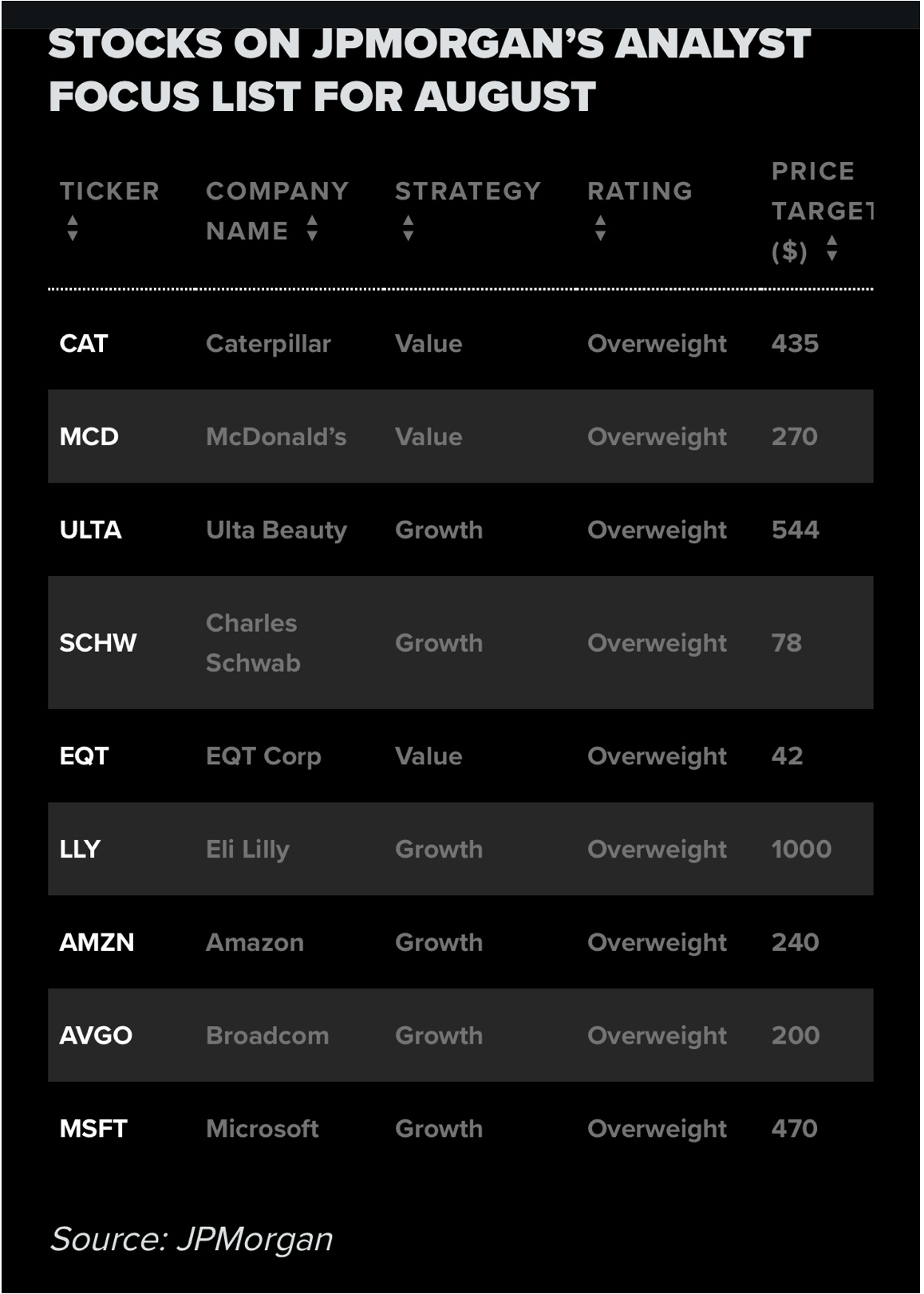

I am not suggesting you buy any of the stocks listed above at this time.I am merely showing you what the bank is focused on.We hold three of these stocks in our portfolio:Caterpillar, Amazon and Microsoft.

Earnings: Costco Wholesale, Warner Bros, Discovery, Occidental Petroleum, Ralph Lauren, CVS Health, Hilton Worldwide Holdings, Walt Disney Company

Thursday, August 8

8:30 a.m. Continuing Jobless Claims (07/27)

8:30 a.m. Initial Claims (08/03)

10 a.m. Wholesale Inventories final (June)

9:30 p.m. China Inflation Rate

Previous: 0.2%

Forecast: 0.3%

Earnings:Gilead Sciences, Akamai Technologies, Take-Two Interactive Software, News Corp, Paramount Global, Expedia Group, Martin Marietta Materials, Eli Lilly

Friday, August 9

8:30 a.m. Canada Unemployment Rate

Previous: 6.4%

Forecast: 6.4%

MARKET UPDATE

S&P 500

Correction sell-off in progress.Support zone = between 5,265 – 4,950.Sustained break of 4,950 would probably see a much deeper sell-off toward the late 4,500’s.

GOLD

If gold can hold $2,350 area, the metal could advance to the mid $2,500’s.A break of the latter level would see gold rallying toward the $2,650 zone.However, if gold does fall below the $2,300 area, we could see a fall toward $2,260 or even $2,200.

BITCOIN

As I write this Post Sunday after/evening, I am watching the price action of Bitcoin, which is now sitting at $54,190.00. There is strong support at the $50k level, and at the $40k level.

PSYCHOLOGY CORNER

Herd Behaviour

This occurs when investors follow the actions of the majority, often leading to trends and bubbles.Herd behaviour can result in significant swings as large groups of investors buy or sell simultaneously.

Exploiting Herd Behaviour

By understanding how herd behaviour drives market movements, investors can position themselves to benefit from the irrational actions of the crowd.For example, contrarian investors often buy when others are selling and sell when others are buying.

QI CORNER

AUSTRALIAN CORNER

It’s the Olympics, so we must celebrate our athletes’ achievements.

Australian, Saya Sakakibara, wins the gold medal in BMX and dedicated it to her brother.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-08-05 10:38:052024-08-05 10:38:05Trade Alert - (AMZN) August 5, 2024 - STOP LOSS - SELL

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-08-05 10:20:042024-08-05 10:20:04Trade Alert - (BRK/B) August 5, 2024 - STOP LOSS - SELL

(MARKET OUTLOOK FOR THE WEEK AHEAD or DID JAY POWELL BLOW IT?) and CHASING EARNEST HEMINGWAY),

($VIX), (INTC), (CCI), (TLT), (COPX), (BHP), (USO) (NVDA), (SLV), (FXY), (CAT), (IWM), (IBKR), (AMZN), (GLD), (BRK/B), (DE)

I am writing this to you from the first-class lounge at Warsaw Airport for LOT Airlines, the national air carrier of Poland. Every seat is full and the air conditioning is broken so the air is stifling.

The guy sitting next to me is shopping for a new tattoo on his iPhone as if he had space for another one.

There is all the day-old Polish food you can eat, but everything is full of garlic, not a great idea in a packed lounge of people waiting to get on to packed airplanes. The Internet doesn’t work, and I had to hack into another airline’s router to send out my trade alerts. They’re doing noisy construction next door. I’m here because my LOT flight to Lithuania is five hours late.

Oh, and the Dow is down 1,000 points.

Oh, the joys of international travel! I wish you weren’t here.

Which raises the important question of the day.

Did Jay Powell blow it?

Did he and his cohorts at the Federal Reserve hold off on interest rate cuts unnecessarily long, so long that he triggered a recession? That is certainly what the stock market thinks today, where it is to sell first and ask questions later.

When the Fed governor says he might cut interest rates that means “SELL” to a trader when the Headline Employment Rate is on an undeniable trend to a year high of 4.3%.

So, how is Jay to atone for his sins?

Cut rates sooner, faster, and by more. Instead of 0.5% in cuts by yearend, we instead are looking at 1.50%. He certainly has the dry powder to do it with. A 5.25% overnight rate against a 3.0% YOY inflation rate that is falling?

Who is Jay kidding?

It may take a couple of weeks for markets to figure all this out. Wash out all the stale Big Tech leveraged longs and we could get there pretty quickly. The 30% Volatility Index ($VIX) on Friday was certainly pretty convincing. That is known in the trade as a “1% event”, with a move in ($VIX) from $12 to $30 in two days only occurring 1% of the time.

Just be happy you didn’t own Intel (INTC), down 50% on the week. I (and therefore you) never bought into the (INTC) recovery story because I think the CEO is a con man. Andy Grove is rolling over in his grave.

In the meantime, anyone who loaded the boat with interest rate-sensitive stocks is looking just fine, thank you very much. Look no further than the (TLT), which hit an impressive $98, a one-year high.

Those who hovered up the dozen or so (TLT) calls spreads and long-term LEAPS I recommended during this time are sitting pretty. Has anyone looked at the (CCI) lately, where I put out a LEAPS as recently as in June at $95? It’s now at $115.50!

And the game has only just begun. This could go on for years.

Although few realize it, we actually suffered a global financial crisis last week. The metals like copper (COPX), and iron ore (BHP) have been waving a red flag for three months. Oil prices (USO) matched a new low for the year, already the worst-performing asset class of 2024, despite getting massive support from multiple wars in the Middle East. A near-instant move in ten-year US Treasury yields to 3.79% says that a recession is already here.

What you are seeing worldwide is known in the business as a “de-grossing,” where everyone shrinks their trading books all at once. The proof of this is the explosive 15% move in the Japanese yen (FXY).

For the past 30 years, hedge funds have been financing their positions through selling short the yen, which yielded zero, and investing the proceeds anywhere in the world into anything with a positive return. They then leveraged this position times ten or more. The Bank of Japan’s move to raise interest rates by a mere 25 basis points ended this game.

Another signal this was all about a “de-grossing” is that assets that should be rocketing on falling interest rates, like gold (GLD) and silver (SLV), actually fell. These declines will end once sanity returns to the markets, which should be soon.

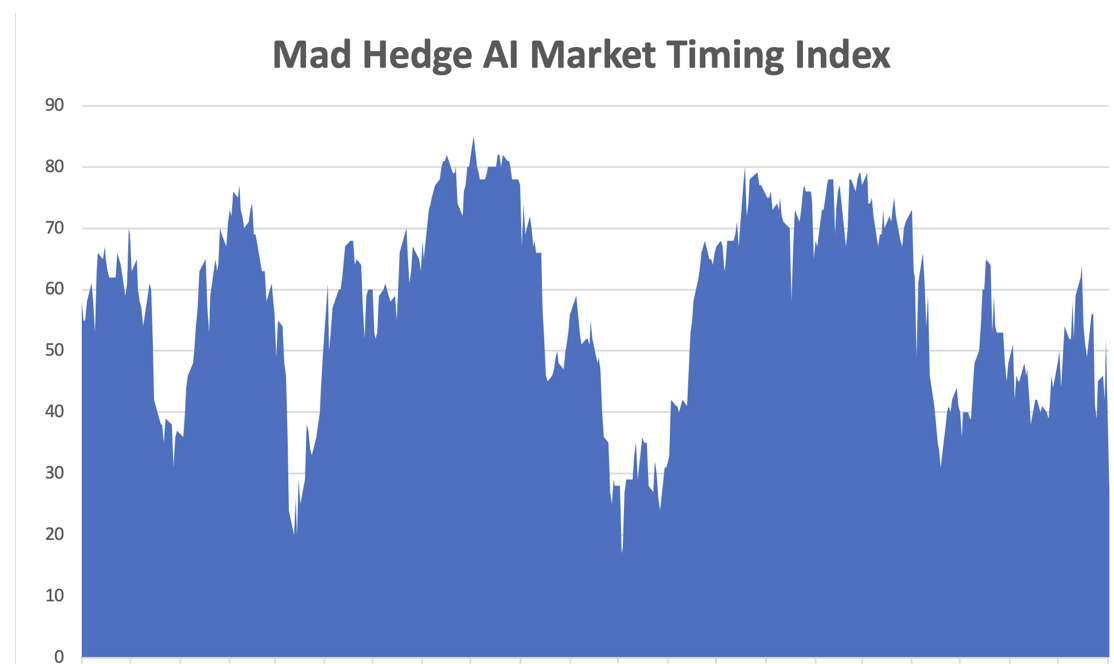

The swan song for all of this frenetic activity is that some great trading and investment opportunities are setting up. But I’ll wait until the last trader throws up on their shoes before pulling the trigger. My Mad Hedge AI Market Timing Index now at 20 says we are already there.

So will you.

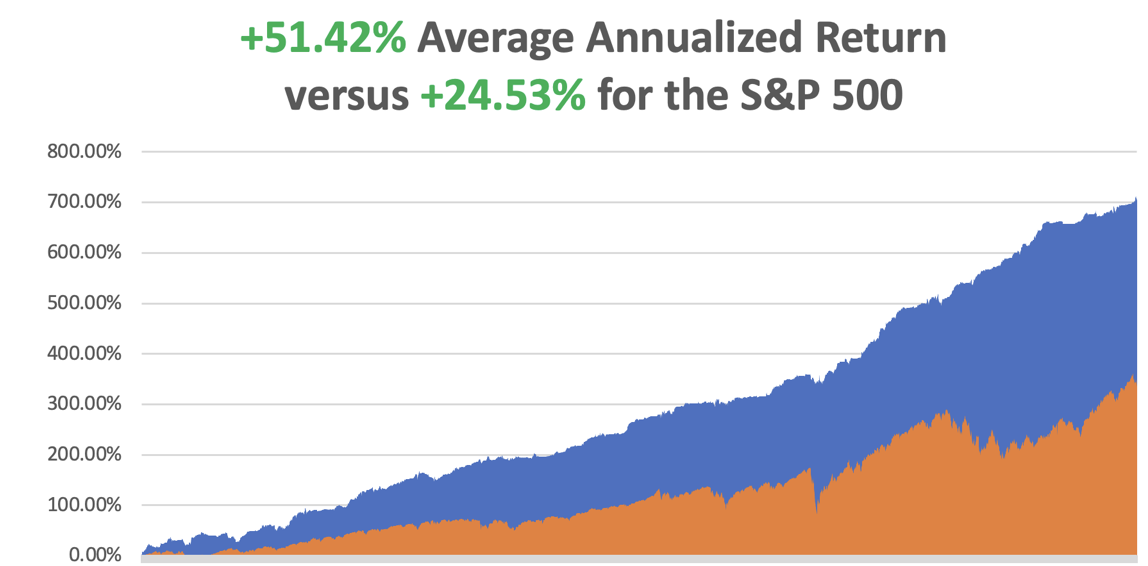

In July, we ended up a stratospheric +10.92%. So far in August, we are down by -4.83%. My 2024 year-to-date performance is at +26.11%.The S&P 500 (SPY) is up +9.43%so far in 2024. My trailing one-year return reached +42.49. That brings my 16-year total return to +702.74.My average annualized return has recovered to +51.42%.

I used the market collapse to take profit in my shorts in (NVDA). I am still short (TSLA). I came out of a long in (SLV) when it started to wobble at support, a move that days proved too soon.

I added a new long in interest-sensitive (CAT). The Friday meltdown stopped me out of (IWM) and (IBKR). It’s easier to dig yourself out of a small hole than a big one.

I also used the meltdown in big tech to add a very deep in-the-money long (AMZN), taking advantage of the extremely high implied volatilities.

This is in addition to existing longs in (GLD), (BRK/B), (DE), and which I will likely run into the August 16 option expiration.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 44 of 56 trades have been profitable so far in 2024, and several of those losses were really break-even. That is a success rate of 78.57%.

Try beating that anywhere.

Market Prices in 50 Point Basis Cut for September, job growth in the U.S. cratered and the unemployment rate inched higher. Nonfarm payrolls grew by just 114,000 and below the estimate of 185,000. The unemployment rate edged higher to 4.3% setting the stage for rates to be cut earlier than expected.

Weekly Jobless Claims Jump 14,000 to 249,000, a one-year high. The report from the Labor Department on Thursday also showed the number of people on jobless rolls swelling in mid-July to the highest level since late 2021. It could fan fears of a rapid labor market deterioration, which surfaced last month when data showed the unemployment rate rose to a 2-1/2-year high of 4.1% in June.

Bank of Japan Raises Rates for only the Second Time in 17 Years, up 25 basis points to 0.25%. The Japanese yen caught on fire as massive short positions were covered. The BOJ also halved monthly bond buying to ¥3 trillion in Q1 2026. Five-year bond yields hit a 15-year high at 0.665%. The world’s most despised currency, down 40% in three years, just caught a bid. Buy (FXY) on dips.

Fed Leaves Rates Unchanged at 23-Year High but indicated that the September rate cut is in the mail. Recent economic data has pointed toward inflation data falling back toward the central bank’s 2% target, while the unemployment rate has crept up above 4%. The Fed said in its policy statement Wednesday that it is attentive to risks on “both sides of its dual mandate,” which is maximum employment and stable prices.

Pending Home Sales Rocket 4.8% in June, versus 1.0% expected. The rise in housing inventory is beginning to lead to more contract signings. Multiple offers are less intense, and buyers are in a more favorable position. The Pending Home Sales Index (PHS), a leading indicator of housing activity, measures housing contract activity and is based on signed real estate contracts for existing single-family homes, condos, and co-ops.

Europe’s Economy Grew at a 0.3% Rate in Q2, far begin that of the 2.8% rate in the US. Germany in recession was a big drag. Germany, the euro zone’s biggest economy, unexpectedly posted a 0.1% contraction in the second quarter. It is amazing how strong the US is with its export markets so weak.

Homeowners Insurance Premiums Rocket by 21%, last year. Experts say a rise in severe weather largely contributed to the increase, but it’s hard to tell how insurers are factoring climate risk into the cost of policies. Some insurers have pulled out of certain areas completely, making state-sanctioned options a necessity. That’s only a Band-Aid as climate change can easily bankrupt any individual state, even California. Many in Florida now only buy fire insurance because storm insurance is now priced out of reach.

Microsoft (MSFT) Bombs, with an earnings and revenue beat, but with a slight shortfall in their Azure cloud business. Revenue from Azure, Microsoft’s main growth engine in recent years, rose 29% in the fiscal fourth quarter, compared with a 31% jump in the previous period. About 8 percentage points of the increase in the recent period was attributable to AI, up from 7 percentage points in the prior quarter. When you’re priced for perfection and come in less than perfect it's worth a 7% share price drop. Avoid big tech until it bottoms.

Tesla Recalls 1.8 Million Cars Over Hood Latch. Tesla claims a warning can be done with an overnight software upgrade. An unlatched hood could fully open and obstruct the driver's view, raising the risk of a crash, the National Highway Traffic Safety Administration (NHTSA) said. Thank goodness I sold short Tesla twice this month.

Janet Yellen Says $3 Trillion Annually is needed to shift to a low-carbon global economy, far more than we have currently budgeted for. On the other hand, it also offers the greatest investment opportunity of the century. We’ve had several alternative energy booms over the past decade, provided you got out on time.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, August 5 at 8:30 AM EST, the ISM Services PMI is out. On Tuesday, August 6 at 9:30 AM, the Balance of Trade ispublished.

On Wednesday, August 7 at 8:30 PM, the new Mortgage Data is printed.

On Thursday, August 8 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, August 9 at 2:00 PM, the Baker Hughes Rig Count is printed.

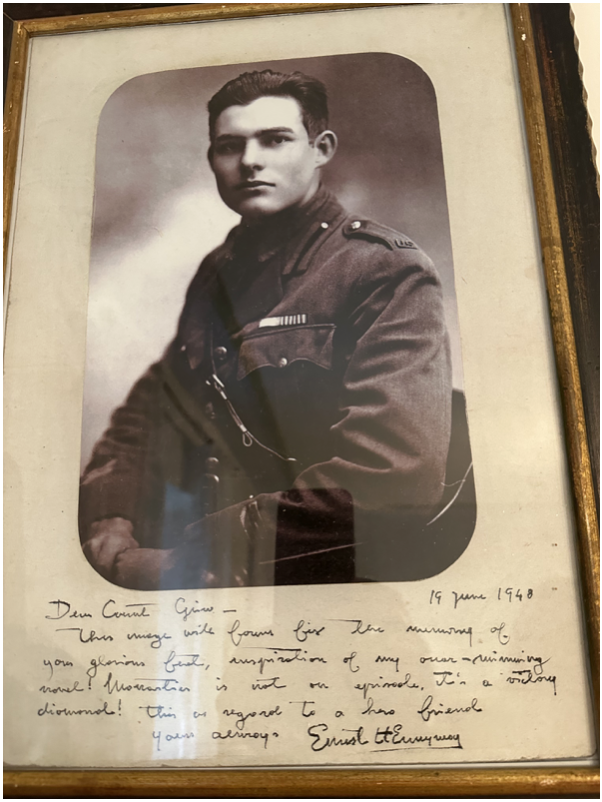

As for me, I received calls from six readers last week saying I remind them of Ernest Hemingway. This, no doubt, was the result of Ken Burns’ excellent documentary about the Nobel Prize-winning writer on PBS last week.

It is no accident.

My grandfather drove for the Italian Red Cross on the Alpine front during WWI, where Hemingway got his start, so we had a connection right there.

Since I read Hemingway’s books in my mid-teens I decided I wanted to be him and became a war correspondent. In those days, you traveled by ship a lot, leaving ample time to finish off his complete work.

I visited his homes in Key West, Cuba, and Ketchum Idaho.

I used to stay in the Hemingway Suite at the Ritz Hotel on Place Vendome in Paris where he lived during WWII. I had drinks at the Hemingway Bar downstairs where war correspondent Ernest shot a German colonel in the face at point-blank range. I still have the ashtrays.

Harry’s Bar in Venice, a Hemingway favorite, was a regular stopping-off point for me. I have those ashtrays too.

I even dated his granddaughter from his first wife, Hadley, the movie star Mariel Hemingway, before she got married, and when she was also being pursued by Robert de Niro and Woody Allen. Some genes skip generations and she was a dead ringer for her grandfather. She was the only Playboy centerfold I ever went out with. We still keep in touch.

So, I’ll spend the weekend watching Farewell to Arms….again, after I finish my writing.

Oh, and if you visit the Ritz Hotel today, you’ll find the ashtrays are now glued to the tables.

As for last summer, I stayed in the Hemingway Suite at the Hotel Post in Cortina d’Ampezzo Italy where he stayed in the late 1940’s to finish a book. Maybe some inspiration will run off on me.

Hemingway’s Living Room in Cuba, Untouched Since 1960

Earnest in 1918

Typing at Hemingway’s Typewriter in Italy from the 1940s

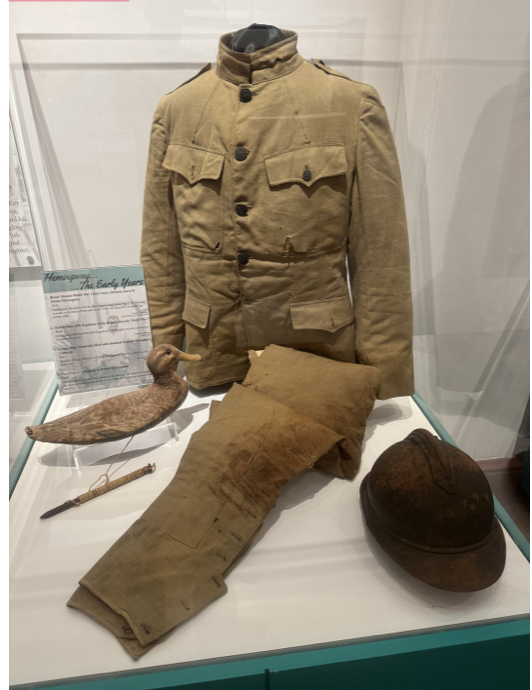

The Red Cross Uniform Hemingway Wore when He was Blown Up in 1917

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/08/Earnest.png802602april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-08-05 09:02:432024-08-05 14:00:30The Market Outlook for the Week Ahead, or Did Jay Powell Blow It?

'Paper money is made of cotton, and I'm long cotton. One reason I'm long cotton is because Dr. Bernanke is out there running the printing presses as fast as he can', said noted commodity bull and former George Soros partner, Jim Rogers.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2024-08-05 09:00:342024-08-05 14:00:11August 5, 2024 - Quote of the Day

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.