Global Market Comments

October 16, 2018

Fiat Lux

Featured Trade:

(WHY COAL IS A SHORT),

(KOL), (BHP), (UNG),

(TESTIMONIAL)

Global Market Comments

October 16, 2018

Fiat Lux

Featured Trade:

(WHY COAL IS A SHORT),

(KOL), (BHP), (UNG),

(TESTIMONIAL)

What has been one of the top performing asset classes since the beginning of 2016?

Is it Apple (AAPL), Amazon (AMZN), gold (GLD), oil (USO), or collectible French postage stamps?

If you said “Coal,” you win the kewpie doll.

In fact, the 19thcentury energy source was one of the best investments you could have made over the past three years.

Indeed, the Van Eck Coal ETF (KOL) has picked up an eye-popping 210% since it printed its $5 low the first week of 2016.

Google (GOOG) eat your heart out.

You might give credit to the president for the meteoric move, thanks to policies so overwhelmingly helpful to the industry that they brought tears to the eyes of the owners of coal mining companies.

But you’d be wrong again.

Most of the move took place before the election.

As a result, I have recently been deluged from readers asking if it is time to buy this prehistoric energy source.

My answer is no, not ever, and not even with Donald Trump’s money.

However, my answer relies more on basic market dynamics rather than any environmental sympathies I might have.

You can blame China.

The Beijing government is manipulating its domestic coal industry to prevent them from defaulting on hundreds of billions of dollars with of loans to local banks.

So, it has cut back the number of days the industry can operate from 330 to 276 days a year.

What happens when you restrict supply and increase demand? Prices go through the roof as they have done smartly.

It gets better.

The Middle Kingdom was hit with rainstorms of biblical proportions, flooding many mines and forcing them to close many mines. The sushi hit the fan.

That forced major consumers, the big steel producers, and electric power plants to resort to the international spot market, or the “seaborne market” to cover shortages to avoid shutting down themselves.

Who is the world’s largest supplier to the seaborne market?

That would be BHP Billiton (BHP), the largest capitalized company in Australia, which has seen its shares appreciate by 144% since 2016 bottom.

I have been following coal for 45 years ever since I was the coal correspondent for the Australian Financial Review during the 1970’s.

I had to write a mind-numbing five pieces a week on coal (the AFR was a daily). So it’s safe to say that I know which end of a lump of coal to hold upward.

For a start, you never want to invest in an asset that is dependent on government fiat for rising prices. They can change their minds at any time. The loans in question could get paid off.

And you can count on the world market to suddenly find new supplies whenever a commodity price doubles.

Remember the Rare Earths bubble where we were active players?

After a hyperbolic bubble, prices fell by 90%. Rare earth turned out to be not so rare. Only the cheap labor to extract them free of environmental regulation was.

So you can count on the current coal bubble to deflate eventually. The perfect storm is about to run in reverse.

That leaves us with the long-term fundamentals of coal which are bleak, to say the least.

China is far and away the world’s largest coal consumer at 49%, followed by the US at 11%. This is why China is also the world’s largest producer of greenhouse gases.

China is making every effort to reduce reliance on these cheapest form of energy, thanks to the blinding, choking smog alerts besetting its largest cities.

It is only still using coal because with an economy growing at 6.6% a year plus, it has to rely on every energy form just to keep the lights only. Power brownouts can lead to political instability.

Coal consumption in the US has been in a death spiral for years falling from 50% to 33% of electric power generation over the past decade.

That led to the bankruptcy of several of its largest players such as Arch Coal (ACI) and Peabody Energy (BTU).

The collapse of natural gas prices to $2/btu made a cleaner burning alternative cost-competitive. And gas lacks the nitrous and sulfur oxides and particulate pollution prevalent in coal.

Read the prospectus of any electric power companies and you will find them besieged by lawsuits from consumers claiming that the coal they burned caused their asthma and cancers. Utility companies would love to be rid of it.

And then there’s solar energy.

California governor Jerry Brown has signed the nation’s toughest climate legislation, mandating that all power come from alternative sources by 2030.

On several days this year, alternatives already accounted for 100% of the state’s total power production.

While ambitious, the target is viewed as doable. Solar energy, which now accounts for 5% of the state’s power output, will do the heavy lifting.

Many other states are expected to follow suit. No room for coal here.

The United Kingdom has already taken this path as have many other nations.

It says a lot that a country that ran a coal-based economy for 300 years announces the closing of its last mine which it did a few years ago. It will replace the power output with alternatives.

Having lived in England during the violent miner’s strikes during the early 1980s, it was quite a revelation.

So the writing is on the wall. Another major producer, Anglo American (NGLB.BE) sold two major mines in Australia.

Coal is clearly an energy source whose time has clearly come and gone. So, will the price of coal. The next recession, which may only be a year off, could well drive the entire industry into bankruptcy.

If I warned them once, I warned them 1,000 times!

The Australian dollar (FXA) is going to fall.

That?s why I cautioned my Aussie friends to sell their homes, get the money the hell out of the country, and pay for their overseas vacations in advance.

As long as it is a de facto colony of China, the fortunes of the Land Down Under are completely tied to economic prospects there.

It is almost a waste of time looking at the Reserve Bank of Australia?s data releases. They have become a deep lagging, and really irrelevant indicators. You are better off going to the source, and that is in Beijing.

And therein lies the problem.

It is highly unlikely that the government in China has any idea what their economy is actually doing. Sure, they pump out the usual figures on a reliable basis like clockwork. These are educated guesses, at best.

Even in a perfect world, collecting numbers from 1.3 billion participants is a hopeless task. The US is unable to do these with any real accuracy, and we have one quarter of their population and vastly superior technology.

For what it is worth, Chinese President Xi Jinping has promised that his country?s GDP growth will not fall below a 6.5% annual rate for the next five years. At this pace, China is still creating more economic activity that any other country in the world.

Which leaves us nothing else to rely on but commodity prices to look at, far an away Australia?s largest earner. These are suggesting that the worst has yet to come.

Virtually the entire asset class hit new six year lows yesterday. I had to go to the weekly charts to see how ugly things really are.

Australia?s largest exports are iron ore (26%, or $68.2 billion worth), coal (KOL) (16%), gold (GLD) (8.1%), and petroleum (USO) (5.7%). When the world?s largest consumer of these slows down, so does demand for these commodities.

BHP Billiton Ltd. (BHP), the largest producer of iron ore, has seen its shares plunge 57% from last year?s high.

But wait! It gets worse.

I have written at length about the transition of China from an industrial to a services based economy. You would expect this, as the Middle Kingdom has virtually no commodity resources of its own, but lots of smart people.

In a nutshell, they wish they had America?s economy. Where services now account for a staggering 68% of all economic activity.

This is why China?s future lies with Alibaba (BABA), Baidu (BIDU), and JD.com (JD). It does NOT lie with its steel factories and coalmines, which by the way, recently announced layoffs of 100,000, the largest in history.

To learn more about the structural remaking of China, please click here for ?End of the Commodities Super Cycle?.

There is one bright spot to mention. Australia is making a transition to a services based economy of its own. Tourism is rocketing, as is the influx of flight capital from the Middle Kingdom.

Walk the streets of Brisbane these days, and you are overwhelmed by the abundance of Asians coming here to learn English, attain a high education, or start a new business. When I came here 40 years ago, they were virtually absent.

How low is low?

It doesn?t help that the governor of the Reserve Bank of Australia, Australia?s central bank, Glenn Stevens, despises his nation?s currency.

He has used every rally this year to talk down the Aussie, threatening interest rate cuts and quantitative easing.

The hope is that a deep discount currency will allow the exporters to maintain some pricing edge on the commodities front.

The market chatter is that the Aussie will take a run as low as $0.55, the 2008-09 Great Recession low.

Whether we actually get that far or not is a coin toss.

And will even $0.55 below enough for Glenn Stevens?

After the market closes every night, I usually don a 60 pound backpack and climb the 2,000 foot mountain in my back yard.

To pass the time, I listen to audio books on financial and historical topics, about 200 a year (I?ve really got President Grover Cleveland nailed!). That?s if the howling packs of coyotes don?t bother me too much.

I also engage in mental calisthenics, engaging in complex mathematical calculations. How many grains of sand would you have to pile up to reach from the earth to the moon? How many matchsticks to circle the earth?

For last night?s exercise, I decided to quantify the impact of this year?s oil price crash on the global economy.

The world is currently consuming about 92 million barrels a day of Texas tea, or 33.6 billion barrels a year. In May, at the $107.50 high, that much oil cost $3.6 trillion. At today?s $53.60 low you could buy that quantity of oil for a bargain $1.8 trillion.

Buy a barrel of crude, and you get one for free!

This means that $1.8 trillion has suddenly been taken out of the pockets of oil producers, and put into the pockets of oil consumers. Over the medium term, this is fantastic news for oil consumers. But for the short term, things could get very scary.

$1.8 trillion is a lot of money. If you had that amount in hundred dollar bills, it would rise to 180 million inches, 15 million feet, or 2,840 miles, or 1.2% of the way to the moon (another mental exercise).

The global financial system cannot move this amount of money around on short notice without causing some pretty severe disruptions.

For a start, there is suddenly a lot less demand for dollars with which to buy oil. This has triggered short covering rallies in the long beleaguered Japanese Yen (FXY) and the Euro (FXE), which are just now backing off of long downtrends. The fundamentals for these currencies are still dire. But the short term trend now appears to be an upward one.

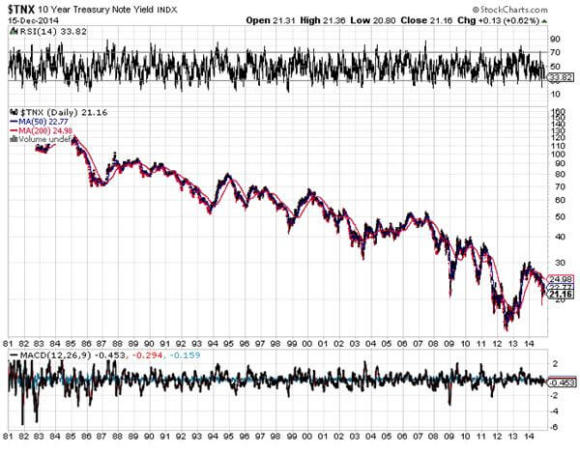

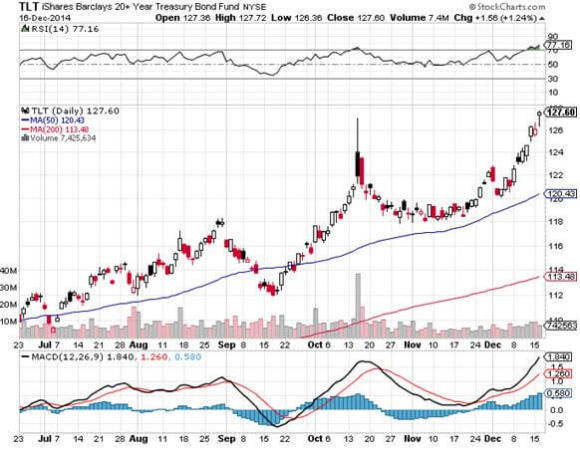

The US Federal Reserve certainly sees the oil crash as an enormously deflationary event. The use of energy is so widespread that it feeds into the cost of everything. That firmly takes the chance of any interest rate rise off the table for 2015. The Treasury bond market (TLT) has figured this out and launched on a monster rally.

Traders are also afraid that the disinflationary disease will spread, so they have been taking down the price of virtually all other hard commodities as well, like coal (KOL), iron ore (BHP), and copper (CU). For more depth on this, see yesterday?s piece on ?The End of the Commodity Super Cycle?.

The precipitous fall in energy investments everywhere will be felt principally in the 15 US states involved in energy production (Texas, Oklahoma, Louisiana, and North Dakota, etc.). So, the consumers in the other 35 states should be thrilled.

However, the plunge in energy stocks is getting so severe, that it is dragging down everything else with it. ALL shares are effectively oil shares right now. In fact, all asset classes are now moving tic for tic with the price of oil.

Throw on top of that the systemic risk presented by the ongoing collapse of the Russian economy. The Ruble has now fallen a staggering 70% in six months, and there is panic buying of everything going on in Moscow stores. The means that the dollar denominated debt owed by local firms has just risen by 70%. Any foreign banks holding this debt are now probably regretting ever watching the film, Dr. Zhivago.

Russian interest rates were just skyrocketed from 10.50% to 17%. The Russian stock market (RSX) is the world?s worst performing bourse this year. How do you spell ?depression? in the Cyrillic alphabet?

And guess what the new Russian currency is?

IPhone 6.0?s, of which Apple is now totally sold out in Alexander Putin?s domain!

Thankfully, this is more of a European than an American problem. But nobody likes systemic risks, especially going into illiquid yearend trading conditions. It?s a classic case of being careful what you wish for.

Of the $1.8 trillion today, about $430 billion is shifting between American pockets. That amounts to a hefty 2.5% of GDP.

Money spent on oil is burned. However, money spent by newly enriched consumers has a multiplier effect. Spend a dollar at Wal-Mart, and the company has to hire more workers, who then have more money to spend, and so on. So a shifting of funds of this magnitude will probably add 1% to U.S. economic growth next year.

Unfortunately, we will lose a piece of this from the obvious slowdown in housing. Deflation means that home prices will stagnate, or even fall. This is a major portion of the US economy which, for the most part, has been missing in action for most of this recovery.

Ultimately, cheap energy as far as the eye can see is a key element of my ?Golden Age? scenario for the 2020?s (click here for ?Get Ready for the Coming Golden Age? ).

But you may have to get there by riding a roller coaster first.

Oil at $53?

Oil at $53?

When the Trade Alerts quit working. I stop sending them out. That?s my trading strategy right now. It?s as simple as that.

So when I received a dozen emails this morning asking if it is time to double up on Linn Energy (LINE), I shot back ?Not yet!? There is no point until oil puts in a convincing bottom, and that may be 2015 business.

Traders have been watching in complete awe the rapid decent the price of Linn Energy, which is emerging as the most despised asset of 2014, after commodity producer Russia (RSX).

But it is becoming increasingly apparent that the collapse of prices for the many commodities is part of a much larger, longer-term macro trend.

(LINN) is doing the best impersonation of a company going chapter 11 I have ever seen, without actually going through with it. Only last Thursday, it paid out a dividend, which at today?s low, works out to a mind numbing 30% yield.

I tried calling the company, but they aren?t picking up, as they are inundated with inquires from investors. Search the Internet, and you find absolutely nothing. What you do find are the following reasons not to buy Linn Energy today:

1) Falling oil revenue is causing Venezuela to go bankrupt.

2) Large layoffs have started in the US oil industry.

3) The Houston real estate industry has gone zero bid.

4) Midwestern banks are either calling in oil patch loans, or not renewing them.

5) Hedge Funds have gone catatonic, their hands tied until new investor funds come in during the New Year.

6) Every oil storage facility in the world is now filled to the brim, including many of the largest tankers.

Let me tell you how insanely cheap (LINN) has gotten. In 2009, when the financial system was imploding and the global economy was thought to be entering a prolonged Great Depression, oil dropped to $30, and (LINN) to $7.50. Today, the US economy is booming, interest rates are scraping the bottom, employment is at an eight year high, and (LINE) hit $9.70, down $70 in six months.

Go figure.

My colleague, Mad Day Trader, Jim Parker, says this could all end on Thursday, when the front month oil futures contract expires. It could.

It isn?t just the oil that is hurting. So are the rest of the precious and semi precious metals (SLV), (PPLT), (PALL), base metals (CU), (BHP), oil (USO), and food (CORN), (WEAT), (SOYB), (DBA).

Many senior hedge fund managers are now implementing strategies assuming that the commodity super cycle, which ran like a horse with the bit between its teeth for ten years, is over, done, and kaput.

Former George Soros partner, hedge fund legend Paul Tudor Jones, has been leading the intellectual charge since last year for this concept. Many major funds have joined him.

Launching at the end of 2001, when gold, silver, copper, iron ore, and other base metals, hit bottom after a 21 year bear market, it is looking like the sector reached a multi decade peak in 2011.

Commodities have long been a leading source of profits for investors of every persuasion. During the 1970?s, when president Richard Nixon took the US off of the gold standard and inflation soared into double digits, commodities were everybody?s best friend. Then, Federal Reserve governor, Paul Volker, killed them off en masse by raising the federal funds rate up to a nosebleed 18.5%.

Commodities died a long slow and painful death. I joined Morgan Stanley about that time with the mandate to build an international equities business from scratch. In those days, the most commonly traded foreign securities were gold stocks. For years, I watched long-suffering clients buy every dip until they no longer ceased to exist.

The managing director responsible for covering the copper industry was steadily moved to ever smaller offices, first near the elevators, then the men?s room, and finally out of the building completely. He retired early when the industry consolidated into just two companies, and there was no one left to cover. It was heartbreaking to watch. Warning: we could be in for a repeat.

After two decades of downsizing, rationalization, and bankruptcies, the supply of most commodities shrank to a shadow of its former self by 2000. Then, China suddenly showed up as a voracious consumer of everything. It was off to the races, and hedge fund managers were sent scurrying to look up long forgotten ticker symbols and futures contracts.

By then commodities promoters, especially the gold bugs, had become a pretty scruffy lot. They would show up at conferences with dirt under their fingernails, wearing threadbare shirts and suits that looked like they came from the Salvation Army. As prices steadily rose, the Brioni suits started making appearances, followed by Turnbull & Asser shirts and Gucci loafers.

There was a crucial aspect of the bull case for commodities that made it particularly compelling. While you can simply create more stocks and bonds by running a printing press, or these days, creating digital entries on excel spreadsheets, that is definitely not the case with commodities. To discover deposits, raise the capital, get permits and licenses, pay the bribes, build the infrastructure, and dig the mines and pits for most commodities, takes 5-15 years.

So while demand may soar, supply comes on at a snail pace. Because these markets were so illiquid, a 1% rise in demand would easily crease price hikes of 50%, 100%, and more. That is exactly what happened. Gold soared from $250 to $1,922. This is what a hedge fund manager will tell us is the perfect asymmetric trade. Silver rocketed from $2 to $50. Copper leapt from 80 cents a pound to $4.50. Everyone instantly became commodities experts. An underweight position in the sector left most managers in the dust.

Some 14 years later and now what are we seeing? Many of the gigantic projects that started showing up on drawing boards in 2001 are coming on stream. In the meantime, slowing economic growth in China means their appetite has become less than endless.

Supply and demand fell out of balance. The infinitesimal change in demand that delivered red-hot price gains in the 2000?s is now producing equally impressive price declines. And therein lies the problem. Click here for my piece on the mothballing of brand new Australian iron ore projects, ?BHP Cuts Bode Ill for the Global Economy?.

But this time it may be different. In my discussions with the senior Chinese leadership over the years, there has been one recurring theme. They would love to have America?s service economy.

I always tell them that they have a real beef with their ancient ancestors. When they migrated out of Africa 50,000 years ago, they stopped moving the people exactly where the natural resources aren?t. If they had only continued a little farther across the Bering Straights to North America, they would be drowning in resources, as we are in the US.

By upgrading their economy from a manufacturing, to a services based economy, the Chinese will substantially change the makeup of their GDP growth. Added value will come in the form of intellectual capital, which creates patents, trademarks, copyrights, and brands. The raw material is brainpower, which China already has plenty of.

There will no longer be any need to import massive amounts of commodities from abroad. If I am right, this would explain why prices for many commodities have fallen further that a Middle Kingdom economy growing at a 7.5% annual rate would suggest. This is the heart of the argument that the commodities super cycle is over.

If so, the implications for global assets prices are huge. It is great news for equities, especially for big commod

ity importing countries like the US, Japan, and Europe. This may be why we are seeing such straight line, one way moves up in global equity markets this year.

It is very bad news for commodity exporting countries, like Australia, South America, and the Middle East. This is why a large short position in the Australian dollar is a core position in Tudor-Jones? portfolio. Take a look at the chart for Aussie against the US dollar (FXA) since 2013, and it looks like it has come down with a severe case of Montezuma?s revenge.

The Aussie could hit 80 cents, and eventually 75 cents to the greenback before the crying ends. Australians better pay for their foreign vacations fast before prices go through the roof. It also explains why the route has carried on across such a broad, seemingly unconnected range of commodities.

In the end, my friend at Morgan Stanley had the last laugh.

When the commodity super cycle began, there was almost no one around still working who knew the industry as he did. He was hired by a big hedge fund and earned a $25 million performance bonus in the first year out. And he ended up with the biggest damn office in the whole company, a corner one with a spectacular view of midtown Manhattan.

He is now retired for good, working on his short game at Pebble Beach.

Good for you, John.