Mad Hedge Biotech & Healthcare Letter

November 10, 2020

Fiat Lux

FEATURED TRADE:

(PFIZER ADDS EXCLAMATION POINT TO ITS DECLARATION OF INDEPENDENCE)

(PFE). (MRNA), (AZN), (JNJ), (MCK), (GSK), (MYL). (MRK), (BMY)

Mad Hedge Biotech & Healthcare Letter

November 10, 2020

Fiat Lux

FEATURED TRADE:

(PFIZER ADDS EXCLAMATION POINT TO ITS DECLARATION OF INDEPENDENCE)

(PFE). (MRNA), (AZN), (JNJ), (MCK), (GSK), (MYL). (MRK), (BMY)

When Operation Warp Speed was launched, the US government handpicked the most promising COVID-19 vaccine programs and offered them funding—an offer that was welcomed by all those selected except for one: Pfizer (PFE).

While COVID-19 vaccine frontrunners like Moderna (MRNA), AstraZeneca (AZN), and even Johnson & Johnson (JNJ) accepted financial assistance from the US government, Pfizer insisted on funding its own coronavirus program.

Now, Pfizer has taken another step to make it clear that it does not need any help.

In what could only be described as adding an exclamation point to its “declaration of independence” from the US government, Pfizer announced that it won’t use the country’s chosen distribution partner in delivering its COVID-19 vaccine.

For years, the US government has been using McKesson (MCK) to deliver drugs and other treatments.

In fact, this was the same company used by the Obama administration in 2009, when it distributed the H1N1 vaccine and medications.

This won’t be the case for Pfizer’s COVID-19 vaccine though.

According to the company, it has designed its own delivery system to ensure the proper and safe distribution of its product.

In October, Pfizer disclosed its distribution plans that centered on select sites in Michigan, Belgium, Wisconsin, and Germany.

Other than its goal to operate as independently from the US government as possible, one of the concerns of Pfizer is the sensitive nature of its COVID-19 vaccine.

The vaccine has to be kept at an ultra-cold temperature of minus 94 degrees Fahrenheit, which means that the shipments would require close monitoring.

What we know so far is that Pfizer has designed shipping containers that can maintain the temperature of the vaccine for 10 days.

In terms of monitoring, the company has developed a real-time GPS tracking system that will report any deviations in the set conditions.

All these are implemented to ensure that the COVID-19 vaccine does not lose potency before it reaches patients.

Looking at the other vaccine candidates, Moderna might also resort to this kind of distribution arrangement since its vaccine needs to be stored at negative 4 degrees Fahrenheit.

Outside its COVID-19 efforts, Pfizer has been aggressive in pruning its business divisions.

Since late 2019, Pfizer has been implementing strategies to eliminate its underperforming segments.

In August last year, the company forged a partnership with GlaxoSmithKline (GSK) to combine their consumer healthcare sectors.

This led to the formation of the GSK Consumer Healthcare, where Pfizer holds a 32% stake.

This year, Pfizer has been working on offloading its off-patent drug unit, Upjohn, and merging it with Mylan (MYL).

This deal should be finalized by the fourth quarter of 2020, with the merger offering Pfizer’s shareholders with roughly 57% of the new company, Viatris.

When this is completed, Pfizer would become a smaller and more focused biopharmaceutical company.

This means that the company can leverage its $202.27 billion market capitalization to move the needle more substantially in terms of its long-term prospects.

One of the key areas that Pfizer has been working towards becoming a powerhouse is oncology—a sector that has served as a major growth driver for the company for years.

Pfizer has a deep oncology portfolio comprising over 20 approved drugs marketed to different areas including breast cancer, lung cancer, and blood cancer.

However, none of its cancer drugs have managed to breach the $10 billion annual sales mark in this sector.

This is because Pfizer has no absolute mega-blockbuster in the oncology space like its competitors Merck (MRK) with Keytruda and Bristol-Myers Squibb (BMY) with Opdivo.

With the growing number of pipeline candidates in its cancer portfolio, Pfizer is expected to come up with a blockbuster by the fourth quarter this year or before the first half of 2021 ends.

Looking at Pfizer’s pipeline, there are 14 approvals anticipated from today through 2025 in the oncology segment alone.

One contender is its prostate cancer drug Xtandi. Another is a non-small cell lung cancer medication called Lorbrena.

In terms of its current product lineup, Pfizer’s biopharmaceutical operations continue to impress investors.

Despite not having a mega-blockbuster, it still has several top-selling drugs like Eliquis and Ibrance. Both showed 9% increase each in sales for the third quarter of 2020.

Taking all these into consideration, Pfizer is estimated to deliver solid growth in the next few years primarily thanks to its fast-developing oncology segment. This market is forecasted to experience an increase of $240 billion every year by 2023.

Overall, a successful COVID-19 program could provide a one-time earnings boost for Pfizer and a substantial earnings accretion in fiscal 2021.

However, this giant biopharmaceutical company’s extensive lineup of commercialized products and promising oncology pipeline mean that its revenue and share performance do not heavily depend on its coronavirus vaccine.

If Pfizer’s COVID-19 vaccine candidate fails, it won’t be a disaster for its shareholders, especially since the company’s shares do not seem to consider this program in its pricing.

In fact, Pfizer shares are looking inexpensive even without a successful COVID-19 vaccine candidate.

If it does turn out to be a success though, then Pfizer investors could enjoy some COVID-19 vaccine call option for free.

Mad Hedge Biotech & Healthcare Letter

October 1, 2020

Fiat Lux

FEATURED TRADE:

(IS AMGEN THE NEW CHAMPION OF THE BIOTECH WORLD)

(AMGN), (ABBV), (JNJ), (BMY)

Amgen (AMGN) grabbed headlines in August when it became the first biotechnology stock listed in the prestigious Dow Jones Industrial Average, offering mutual funds and exchange-traded funds that follow the index more access to the company’s shares.

With its share price worth $243.21, Amgen has been hailed responsible for roughly 1,600.20 Dow points – roughly 5.8% of its total.

Does this make Amgen the new champion of the biotechnology sector?

Although it has not explicitly declared that it is developing drugs mainly for older adults, Amgen’s pipeline notably focuses on the fast-rising senior population across the globe.

This is quite strategic considering that the world population of seniors is projected to double from the current number to reach more than 2 billion by 2050.

A noteworthy strategy it employed to expand its market share is cutting the prices of some of its most popular products.

For example, Amgen lowered the price of its heart disease treatment Repatha by as much as 60% in 2018. Since the drug has become one of the more affordable options in the market, making it more accessible to more users.

This led to a 20% rise in sales revenue by 2019, with Repatha expected to rake in a higher number in 2020 – a highly probable expectation considering the 32% climb it recorded in its second quarter earnings report this year. So far, Repatha has generated $200 million in sales in the second quarter.

Another notable drug that recorded a climb in sales is Evenity, which targets postmenopausal women with osteoporosis.

Evenity generated an impressive increase of $101 million compared to the $28 million it earned in the same period in 2019.

Despite its $142.08 billion market capitalization, Amgen is not immune to the effects of the pandemic.

For one, sales of arthritis drug Enbrel fell by 9% year over year to record only $1.2 billion while cancer therapy Neulasta showed a 28% decline to $593 million.

The drop in their performance was attributed to pricing pressure and biosimilar competition.

In addressing the issue, Amgen also ventured in creating a competitive and lucrative biosimilar portfolio.

So far, its biosimilar version of AbbVie’s (ABBV) best selling drug arthritis drug Humira has managed to rake in over $200 million in sales in 2019.

Two more oncology biosimilars, MVASI and KANJINTI, which were only launched in the US last year, generated $588 million in sales.

This year, Amgen will launch another potential biosimilar blockbuster called AVSOLA. This would be in direct competition with Johnson & Johnson’s (JNJ) antitumor treatment Revicade.

Outside these biosimilars, Amgen has over 50 clinical trials queued, which include more than 20 Phase 3 studies. Ultimately, the company’s goal is to displace all the deadweights in its current portfolio.

One of the most exciting products in Amgen’s pipeline right now is its heart failure drug Omecamtiv Mecarbil, which recently completed Phase 3 clinical trials.

With cardiovascular diseases identified as one of the leading causes of death worldwide, the success of Omecamtiv Mecarbil would translate into a strong foothold for Amgen in this huge market and a key growth driver in the long run.

Another blockbuster in Amgen’s portfolio is Otezla, which it acquired from its $13.4 billion deal with Celgene prior to its merger with Bristol Myers Squibb (BMY) in 2019.

Although Otezla has already been marketed as an adult arthritis and psoriasis treatment, Amgen has been working on expanding its indication to include Behcet's disease, pediatric psoriasis, and pediatric arthritis.

Even without the expanded indications, Otezla has been a hot seller for Amgen.

In fact, the pandemic did not stop it from reaching a 14% year over year revenue growth every quarter, with its second quarter earnings reaching $561 million.

Other than the expanded use to cover more age ranges in the arthritis and psoriasis sector, Amgen is also studying whether Otezla can be used as a COVID-19 treatment.

If these studies prove to be successful, then Amgen will easily make up the price of the Otezla purchase quicker than anticipated.

More importantly, it would be able to add another massive moneymaker in its already formidable anti-inflammation program. By the end of 2021, Amgen’s revenues would be considerably bigger.

Amgen’s second quarter earnings reports showed a respectable 6% rise in its year over year revenue, with the company generating $6.2 billion despite the ongoing health and financial crises.

Beyond its growth in the US market, Amgen has been busy with international expansion. To date, the company has established a key partnership with China’s BeiGene (BGNE).

It further strengthened its presence in Asia thanks to its acquisition of Japan’s Astellas Pharma earlier this year.

These moves are promising since China and Japan are the second and third biggest pharmaceutical markets in the world, and both countries are showing strong growth in their senior populations.

Needless to say, these partnerships would put Amgen in a strategic position to capture a share of that growth.

Investing in healthcare and biotechnology stocks has always been one of my go-to advice to people.

National healthcare spending is expected to increase at an average rate of 5.5% annually until 2027.

By then, the cost would reach a whopping $6 trillion, resulting in an estimated $1 in every $5 of the GDP getting allocated to healthcare spending within this decade.

Amgen is a blue chip biotechnology stock that has a presence in over 100 countries and develops groundbreaking treatments that can help people across the globe.

As a leading company in the healthcare and biotechnology industry, Amgen holds a strong position to leverage this growth to its advantage.

While the 2.48% trailing annual dividend yield is pretty average, Amgen also prides itself of consistently boosting its dividend every year since 2011.

It also engages in opportunistic share buybacks, so its investors have more ways to get rewarded.

Since Amgen stock shares are not exactly cheap right now, income-oriented investors should be on the lookout for a market crash and seize the opportunity to scoop up shares of this valuable biotechnology giant.

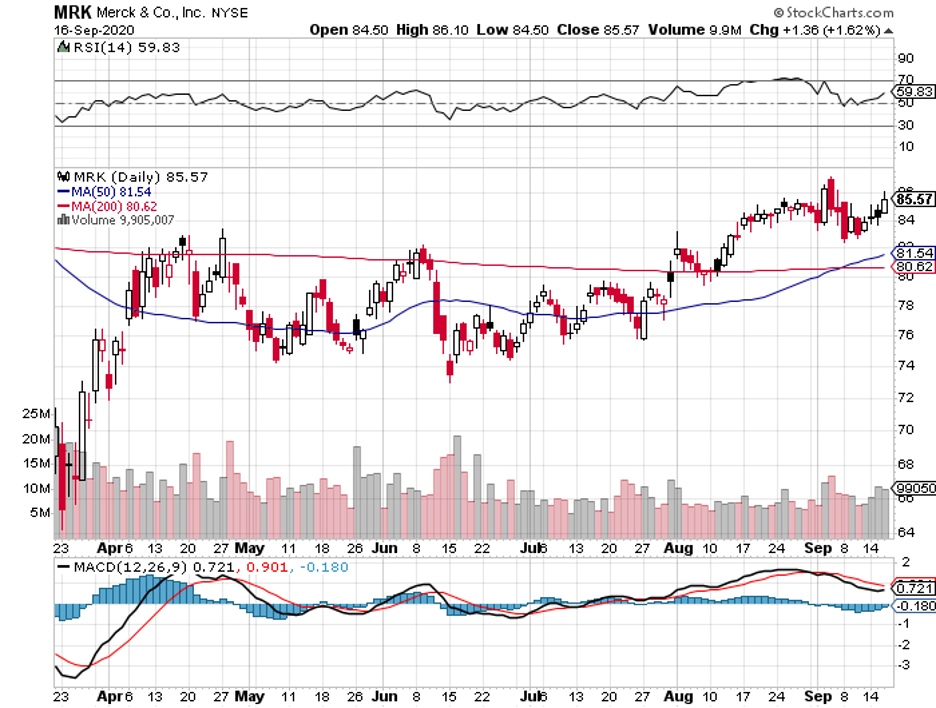

Mad Hedge Biotech & Healthcare Letter

September 22, 2020

Fiat Lux

Featured Trade:

(WHY MERCK IS UNDER-APPRECIATED IN THE COVID-19 RACE)

(MRK), (PFE), (MRNA), (RHHBY), (REGN), (BMY), (GILD)

The excitement over the COVID-19 vaccine candidates has boosted the shares of the most widely reported companies like Pfizer (PFE) and Moderna (MRNA). Meanwhile, other developers have not received the same love from investors.

However, it looks like another COVID-19 vaccine player will be joining Pfizer and Moderna under the spotlight: Merck (MRK).

Merck recently announced that it is now ready to test its vaccine on humans. The trials will be conducted in Germany, and the company has been scouring government databases for viable volunteers.

Unlike Pfizer and Moderna, which are utilizing a novel technology that will need two vaccine doses to be fully effective, Merck is working on two different COVID-19 vaccine candidates designed to work with only a single dose.

This could offer Merck a clear advantage over its competitors.

Also, one of Merck’s candidates could be taken in oral form. This is another significant advantage since it would make the vaccine easier and more convenient to administer.

Merck’s vaccine candidates contain a destabilized version of the same virus that causes measles. This virus is then used to deliver the coronavirus’ spike protein to the patient’s immune system, which would trigger an immune response.

The goal is not only to create a vaccine that would offer protection using a single dose, but also utilizing an existing and reliable technology that can be readily scaled up for mass production.

Since we need to immunize roughly 7 billion across the globe, Merck’s plan to manufacture a single-dose vaccine would be more convenient instead of using multiple doses.

Overall, the COVID-19 vaccine market could reach $50 billion in revenue by 2030.

Apart from its vaccine candidate, Merck is also looking into an antiviral treatment for COVID-19 patients

If successful, this product would be competing against Gilead Sciences’ (GILD) Remdesivir. Just like one of its vaccines, Merck is also developing a treatment in oral form instead of a hospital infusion.

Merck’s Remdesivir alternative can reduce the severity of the COVID-19 by interrupting the virus’s capacity to replicate.

Unlike Gilead’s drug, which can only be used in severe cases, Merck’s candidate can be prescribed immediately after a patient is diagnosed with the disease.

This COVID-19 cure is set to begin its Phase 3 trial this September, with Merck is confident that it can manufacture millions of doses before 2020 ends.

Experts dubbed this drug as an “underappreciated COVID-19 treatment,” which is estimated to reach blockbuster status.

Aside from not getting enough credit for its COVID-19 efforts, Merck is also not receiving enough attention for its pipeline.

So far, the company holds the leading drug that boosts the immune system to fight off cancer: Keytruda. It also has one of the leading vaccine franchises in the world.

Keytruda can easily generate $14.5 billion in sales in 2020 alone, which represents a 30% jump from its 2019 performance. More importantly, the drug can reach $22 billion by 2025.

However, investors are worried over Merck’s dependence on the drug, which comprises 30% of its revenue. In fact, Wall Street keeps zeroing in on the 2028 patent expiration of Keytruda.

At the moment, Keytruda faces competitors like Roche Holding (RHHBY), Regeneron Pharmaceuticals (REGN), and Bristol Myers Squibb (BMY).

However, Merck is not the type to put all its eggs in a single basket.

The company is developing new products that can generate an additional $13 billion to $18 billion in sales annually.

Among these treatments is another potential immuno-oncology antibody, which has been sent to clinical trials this year. Merck also has a long-term HIV treatment queued for clinical studies.

One exciting drug candidate is ARQ531, which is a potential cancer therapy. This projected blockbuster was part of Merck’s $2.7 billion acquisition of ArQule in January.

Other than this acquisition, Merck also obtained the rights to several cancer treatments, which are hailed to be more effective than the conventional chemotherapy, thanks to its acquisitions of Astex Pharmaceuticals and Taiho Pharmaceuticals.

In terms of its vaccine franchise, this arm of the business is projected to generate $9 billion in annual sales in 2021, with the revenue steadily rising to $100 billion in the next several years.

In particular, Merck is looking into developing further its cervical cancer vaccine Gardasil. So far, this vaccine is estimated to generate roughly $3.9 billion in sales in 2020 and reach $5.5 in 2023.

The focus on boosting its vaccine franchise is a strategic move considering that vaccines are generally a durable business and are typically immune from any generic competition.

Although it is not one of the leading vaccine developers in the COVID-19 race, Merck has positioned itself as the leader in the cancer drug development sector and its distribution over at least the next decade.

I believe that Merck’s prudent business, strategic acquisitions, and exciting pipeline will gradually push the stock to the top.

In summary, I think that Merck is a good stock to buy. For those searching for a strong biopharmaceutical play at a reasonable price, this company should be on your shortlist.

Mad Hedge Biotech & Healthcare Letter

August 27, 2020

Fiat Lux

Featured Trade:

(THE FUTURE OF GENE-EDITING TECHNOLOGY)

(CRSP), (VRTX), (BAYRY), (NTLA), (NVS), (EDIT), (BMY)

There are wise investments, and there are excellent investments.

CRISPR Therapeutics (CRSP) has been proving to qualify in the latter category.

In fact, the company is considered one of the best biotechnology stocks to own during these turbulent times. It is estimated to dominate the gene-editing therapy market, which will reach roughly $11.2 billion in worth by 2025.

Four years ago, CRISPR Therapeutics stock was trading at $14.09. Today, each share is worth $90.35.

This means that CRISPR Therapeutics biotechnology company has been trading for 540% more than its value since it went public in 2016.

This is a remarkable pace for a biotechnology stock, with CRISPR Therapeutics raking in $289 million in trailing 12-month revenue thanks to strategic collaborations.

It even has a decent $890 million stored in cash, with the company reporting a 16% profit margin despite not having any treatment or drug available in the market yet.

More importantly, CRISPR Therapeutics holds a novel position of being under absolutely zero pressure to push a product out the door.

Nonetheless, the investor confidence in CRISPR Therapeutics relies heavily on the company’s leading position in the groundbreaking world of gene-altering treatments.

Basically, the company specializes in creating and developing therapies for genetic diseases with either no cure available or require frequent transfusions.

Looking at the results of the recent tests on the company’s pipeline candidates, CRISPR Therapeutics is projected to transform into a household name in the next five to 10 years.

CRISPR Therapeutics has five cell therapy candidates in the clinical stage. Three of these target immuno-oncology, while the two are designed for genetic blood disorders like beta-thalassemia sickle cell disease.

Among the five, the most advanced is CRISPR Therapeutics’ collaborative work with Vertex Pharmaceuticals (VRTX) on beta-thalassemia therapy CTX001.

This candidate received a fast-track designation from the FDA, with CRISPR Therapeutics releasing promising preliminary results recently.

However, it is another Vertex collaboration drug that actually yielded CRISPR Therapeutics $25 million at the beginning of 2020.

The drug, which is developed to treat muscular dystrophy disorder, is expected to account for approximately $800 million in future milestone payments in the next few years.

Although the genetic blood disorder programs are raking in millions these days, CRISPR Therapeutics’ cancer treatment pipeline offers an even greater potential in terms of stable revenue streams.

The company is utilizing a gene-editing platform, called CRISPR/Cas9, to create “off the shelf” novel chimeric receptor (CAR) T-cells.

If successful, then CRISPR Therapeutics can use a single batch to treat a broad group of cancer patients.

This is groundbreaking because the typical way involves harvesting T-cells from the patients, tailor-fitting the therapies, then re-introducing the cells to the body.

With this technology, CRISPR Therapeutics can easily cover more markets and offer regular treatments for patients within shorter intervals.

That’s why it comes as no surprise that a major biotechnology player like Bayer (BAYR) reached out to the smaller company for a collaboration.

The CAR T-cell market is projected to hit $8.4 billion by 2027, with an estimated compound annual growth rate of roughly 15%.

Specifically, CRISPR Therapeutics expects this product to become a leader in the solid tumor cancer therapy space, pegged to reach $425 billion by 2027.

However, it is not only CRISPR Therapeutics that is widely known in the gene-editing sector.

To date, the company has two close competitors: Intellia Therapeutics (NTLA), which has a strategic partnership with Novartis (NVS), and Editas Medicine (EDIT), which is working alongside Bristol Myers-Squibb (BMY).

Both are also using the CRISPR/Cas9 technology to come up with treatments.

Although Intellia Therapeutics and Editas went public the same year as CRISPR Therapeutics, neither has performed quite as well.

For perspective, CRISPR Therapeutics currently has a market capitalization of $6.3 billion. In comparison, Intellia Therapeutics has $1.13 billion while Editas Medicine has $2.13 billion.

Keep in mind though that clinical-stage companies, particularly in the biotechnology sector, are inherently risky plays.

Among the companies in the space, CRISPR Therapeutics is emerging to be a solid bet not only from a cash perspective but also based on its strong pipeline and profitable collaborations.

Overall, CRISPR Therapeutics is still considered a high-risk option.

Hence, the safest way to invest is to build a carefully hedged portfolio filled with well-researched gene-editing stocks. This will minimize your risks and guarantee your exposure to the upside in case any of your chosen biotechnology companies makes it to the market with a groundbreaking therapy.

Mad Hedge Biotech & Healthcare Letter

August 4, 2020

Fiat Lux

Featured Trade:

(MERCK’S SLOW BUT STEADY COVID-19 HEADWAY)

(MRK), (GILD), (REGN), (AZN), (PFE), (MRNA), (ABBV), (BMY), (RHHBY)

Is it truly better late than never?

Merck has been decisively cautious in its approach of potential COVID-19 treatments and even more so when it comes to their vaccine candidates.

Recently though, the company has finally offered a glimpse of its progress.

The first promising update is Merck’s work on MK-4482, which is an antiviral candidate aimed at treating COVID-19 patients. Basically, this candidate works by preventing the SARS-CoV-2 from replicating.

The laboratory results showed that an increasing dose of MK-4482 can effectively halt the progress of the virus in a patient’s system.

Judging from the timeline followed up to this point, Merck plans to begin huge trials by September.

The MK-4482 is expected to compete with Gilead Sciences’ (GILD) Remdesivir, with the Merck candidate possibly edging out the latter.

This is because the SARS-CoV-2 tends to mutate, rendering Remdesivir less potent the next time it is administered to patients. In comparison, MK-4482 has demonstrated an ability to fight off the mutated versions of the virus.

MK-4482 also comes in tablet form, making it a preferable and more convenient option compared to Gilead’s intravenous infusion and even Regeneron’s (REGN) injectable antiviral cocktail REGN-COV2.

On the COVID-19 vaccine front, Merck has been working with Thermis Biosciences in developing a candidate based on a measles virus vector platform originally developed by the Institut Pasteur researchers.

However, this is not Merck’s only shot on goal.

The company is also collaborating with the International AIDS Vaccine Initiative to develop another vaccine candidate, V590.

The two are using the same platform that Merck created for its already approved Ebola vaccine. The goal is to start human testing by the third quarter of 2020.

Merck is also looking into offering a single-dose vaccine instead of the double dose shots its competitors are working on, with one of its candidates developed to be taken orally instead of via injectibles.

If they succeed, then Merck’s vaccines will be more accessible and convenient for a lot of patients.

Aside from developing V590, Merck plans to use the same approved technology to advance its other antivirals in its clinical testing pipeline.

In fact, Merck’s move to acquire Thermis Bioscience demonstrates the company’s resolve to focus on strengthening its vaccine program. The primary expectation for this newly formed partnership is to come out swinging and eventually win big on the COVID-19 vaccine race.

The victory will then serve as a springboard for a new and powerful revenue stream for Merck, which would serve to quiet the fears of the company’s investors fretting over the patent expiration of blockbuster drug Keytruda.

The impending loss of exclusivity for cancer treatment Keytruda has been hanging over Merck’s head for quite some time now.

Aside from the potential biosimilar competition, Keytruda has been facing stiff competition against biotechnology giants like Bristol Myers Squibb (BMY), Roche (RHHBY), and Regeneron.

Needless to say, fears over this have been overshadowing the company’s impressive internal pipeline – a reaction that pretty much mirrors the experience of AbbVie (ABBV) on the pending patent loss of its blockbuster Humira.

However, Merck has been working on products that could rake in an additional $13 billion to $18 billion to its sales every year.

The list includes immuno-oncology antibody candidates, additional vaccines, and even HIV treatments.

The company also has more than $40 billion on its balance sheet, putting it in a favorable position to acquire more companies or products that could bolster its franchise.

Since the pandemic broke out, Merck has lagged behind its COVID-19 rivals AstraZeneca (AZN), Pfizer (PFE), and Moderna (MRNA).

Looking at its progress and future plans though, it looks like the company has set out to achieve a tortoise over the hare victory particularly in the COVID-19 vaccine race.

With incredible uncertainty hovering over the rest of 2020, it is only natural to seek stocks for an all-weather portfolio.

While there are many factors to consider, looking at businesses that allocated sensibly to capital expenditures and R&D is definitely a great way to start.

Merck’s strategic partnerships with companies like Thermis Biosciences, Taiho Pharmaceuticals, and Astex Pharmaceuticals also play significant roles in this aspect.

Although Merck has not provided a particularly strong performance so far this year, this biotechnology and health care giant is poised to stage a strong comeback when the dust settles.