Mad Hedge Biotech & Healthcare Letter

December 22, 2020

Fiat Lux

FEATURED TRADE:

THE MOST FAMOUS CANCER STOCK YOU’VE NEVER HEARD OF

(TRIL), (NVAX), (PFE), (IMMU), (SHOP), (GILD), (ABBV)

Mad Hedge Biotech & Healthcare Letter

December 22, 2020

Fiat Lux

FEATURED TRADE:

THE MOST FAMOUS CANCER STOCK YOU’VE NEVER HEARD OF

(TRIL), (NVAX), (PFE), (IMMU), (SHOP), (GILD), (ABBV)

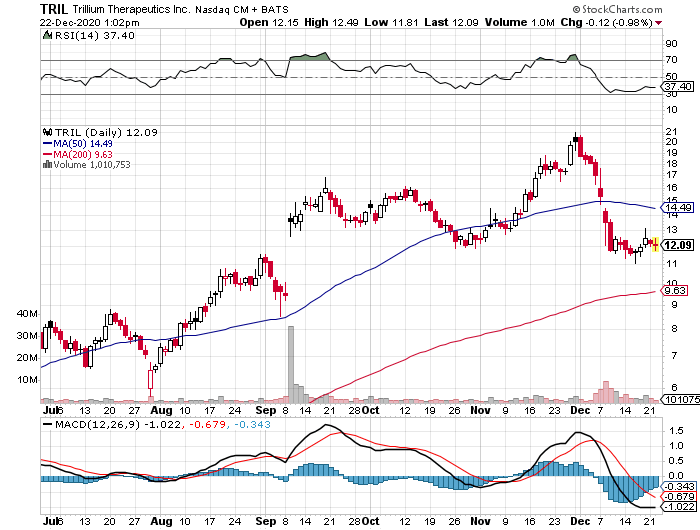

Biotechnology stocks have proven time and time again to be excellent growth vehicles for risk-tolerant investors.

Underscoring this claim are companies like COVID-19 vaccine frontrunner Novavax (NVAX), which generated jaw-dropping returns on capital for their investors within an impressively short period.

Now, another biotechnology stock is showing telltale signs of following their footsteps: Trillium Therapeutics (TRIL).

Trillium’s story is a familiar one in the biotechnology industry.

Trading only in the penny stock range back in 2019, the company’s share price practically quadrupled since the start of 2020.

Taking into consideration that this meteoric rise actually happened while COVID-19 was blasting the world to smithereens, it’s hardly surprising that this news didn’t receive much media attention.

Trillium’s shares are currently up by an astounding 1,260% -- and the company still has so much room to grow from here.

For context, Trillium had a market capitalization of $7 million in November 2019. This number skyrocketed to $1.3 billion since its shift to cancer technology.

Although a lot of factors came into play, the key turning point for Trillium was when the company decided to go all-in on its cancer programs.

Ultimately, Trillium’s goal is to challenge chemotherapy.

The move to shutter its lead programs on tumor treatments and instead focus on developing cancer-fighting technology was the gamble of a lifetime for the company.

This gutsy move impressed investors, and Trillium was never the same since then.

Today, Trillium is the No. 1 stock on Canada’s S&P/TSX Composite Index, overtaking its previous leader e-commerce giant Shopify (SHOP) by almost 10-fold.

In the US, Trillium shares rank as the No. 4 best-performing company on the Nasdaq Composite Index.

While its epic stock market rally may have some investors feeling left out, all signs point to further gains in the future even for those who missed the initial boom.

Among the major capitalists of this biotechnology company is giant biopharmaceutical company and COVID-19 vaccine leader Pfizer (PFE), which invested $25 million in Trillium’s common stock.

While this equity stake may seem small in relation to Pfizer’s $212.16 billion market capitalization, this initial show of confidence is hailed as a prelude to an even bigger investment in the future.

So far, the most exciting cancer treatments in Trillium’s pipeline are TTI-621 and TTI-622.

These programs are in the same class of emerging cancer technologies, called CD47-based therapies, that prompted Gilead Sciences’ (GILD) $4.9 billion acquisition of Forty Seven, Inc. in April this year.

Aside from Gilead, AbbVie (ABBV) has also been reported to have invested a huge sum in this technology.

In simplest terms, CD47-based therapies can bypass the “don’t eat me signal” put up by some cancer cells in an effort to evade immune detection.

Thus far, both TTI-621 and TTI-622 have been showing promising results. Trillium recently announced that it will increase the dosage in these programs.

While Trillium leaders have not been specific in terms of being open to an acquisition, their recent statements indicate that they are not completely opposed to one.

It’s either that or a partnership with a company as big or even bigger than Pfizer.

As with all the biotechnology stocks, however, there will always be a risk.

For Trillium, the most evident one is competition.

While it’s true that the company has been recognized as the leader in the CD47 arena, more and more competitors are entering the immuno-oncology space.

Right now, the most obvious rival is Gilead, which added Immunomedics (IMMU) to its arsenal via a $21 billion acquisition deal.

Given the sheer amount of money that Gilead has been spending to practically corner the immuno-oncology market, it’s to be expected that more biopharmaceutical titans will enter the fray.

This is one of the reasons Trillium has been tagged as a prime candidate for a massive acquisition deal soon. So far, Pfizer is considered the most probable suitor.

Despite its astonishing performance this year, Trillium’s market capitalization still remains within the small-cap territory. That’s to be expected since its lead assets are still undergoing trials.

Considering that it is an early-stage biotechnology stock, Trillium does not have much in terms of income.

However, the company does have enough cash to last for a while. At the moment, it has $130 million cash.

With its total expenses of $38.8 million in 2019, I say this could offer the company more than three years of breathing room financially.

But it would be shocking if Trillium’s value won’t enter the large-cap territory (higher than $10 billion) if and when the company’s high-value assets reach the late-stage studies.

The fact that it’s also an attractive acquisition candidate offers incredible incentive to its investors.

Simply put, Trillium’s stock could get as much as 1,000% gain over the coming two to three years, making it an ideal investment for risk-tolerant investors.

Mad Hedge Biotech & Healthcare Letter

December 1, 2020

Fiat Lux

FEATURED TRADE:

(BET LIKE WARREN BUFFETT)

(MRK), (BRK.A), (AAPL), (JPM), (GILD), (PFE), (ABBV)

Warren Buffett’s moves via Berkshire Hathaway (BRK.A) showed some telling signs this third quarter.

For one, the Oracle of Omaha has surprisingly trimmed his holdings in Apple (AAPL) and even JPMorgan Chase (JPM).

Another telltale sign that change is coming can be seen in his positions in biopharmaceutical titans.

Let’s take a closer look at one of the three biggest biopharma investments of Berkshire to date: Merck.

While the New Jersey-based pharmaceutical titan has not been as widely reported as its counterparts in the COVID-19 race, Merck has actually been working on a promising coronavirus program.

In fact, the company is part of the first five COVID-19 programs included in Donald Trump’s Operation Warp Speed.

Just last week, the company added another promising COVID-19 treatment to its pipeline via the $425 million cash acquisition of Oncolmmune—a move that would give Merck access to the privately-owned company’s COVID-19 treatment, called CD24Fc.

If successful, CD24Fc will be a powerful treatment for mild to severe cases of COVID-19.

To date, only Gilead Sciences’ (GILD) Veklury has received FDA approval and even that treatment failed to address all the health concerns.

In comparison, CD24Fc is expected to undergo a smooth sailing journey from clinical trials to its market launch in 2021.

Meanwhile, Merck may have another ace in the hole with its COVID-19 program.

While the company is already months behind the frontrunners, Merck has a competitive advantage over the COVID-19 vaccine candidates submitted by Pfizer (PFE), Moderna (MRNA), and even AstraZeneca (AZN).

Its experimental COVID-19 vaccine does not require any freezing.

This means that unlike the candidates of Pfizer and Moderna, Merck’s vaccine does not need ultra-special handling and transportation.

On top of that significant advantage, Merck has been working with the nonprofit organization International AIDS Vaccine Initiative to develop a COVID-19 vaccine that only requires a single dose.

In contrast, the leading candidates today require two shots of their vaccines to become effective.

Apart from betting big on its COVID-19 program, Merck is also upping the stakes in its oncology pipeline.

Its recent move is the $2.75 billion acquisition of VelosBio—a partnership that adds another potent arrow to Merck’s already powerful quiver of cancer drugs.

This deal with VelosBio provides Merck with access to cancer treatments under development. Most of these home in on the deadly cancer cells but manage to spare the patients from several horrible side effects.

Prior to this, Merck shelled out $1 billion to gain an equity stake in Seagen (SGEN). The deal also grants Merck access to an extensive antibody drugs pipeline.

Aside from its oncology-related acquisitions—all of which have been home runs for its investors—Merck’s existing cancer pipeline has been consistent moneymakers.

Apart from lung cancer treatment Keytruda, which generated a whopping $11.9 billion in sales in 2019 alone, Merck has a virtually unbeatable arsenal against cancer.

In fact, its thyroid cancer drug Lenvima, which was initially approved for thyroid cancer in 2015, already expanded its indications to cover renal cell carcinoma and potentially even melanoma, endometrial cancer, NSCLC, and bladder cancer.

This could bring Keytruda-like success for Merck in the future.

Aside from Merck, Warren Buffett also invested in biopharmaceutical titans Pfizer and AbbVie.

As of September, Berkshire Hathaway holds 3.7 million Pfizer shares, 21.3 million AbbVie shares, and 22.4 million Merck shares.

These moves are especially noteworthy since the company has not owned any of these biopharma giants at the end of June.

Looking at the profile of these companies, there is no obvious connection or theme.

As discussed, Merck is heavily investing in its oncology pipeline.

AbbVie has been busy diversifying and building a pipeline independent from its megablockbuster Humira.

In fact, this biopharmaceutical giant has delved into dermatology with its massive acquisition of Allergan, aka the Botox-maker.

Meanwhile, Pfizer has been in the news thanks to its COVID-19 vaccine.

Aside from its coronavirus program, Pfizer has been focused on completing the merger between its Upjohn unit and generic drugmaker Mylan (MYL) to form a new company, called Viatris.

Analyzing all three closely though, one thing becomes clear: They are trading off their all-time highs and have been doing it for the entire 2020.

Do you know what that means?

Warren Buffett has been bargain shopping.

Mad Hedge Biotech & Healthcare Letter

October 29, 2020

Fiat Lux

FEATURED TRADE:

ROCHE ENTERS COVID-19 FIGHT IN STYLE

(RHHBY), (REGN), (GILD), (MRK), (ALNY), (IONS)

Roche (RHHBY) is making quite an entrance in the COVID-19 antiviral treatment race, forking out $350 million in cash to gain rest-of-the-world rights to a promising new drug created by Massachusetts-based biotech company Atea Pharmaceuticals.

This is an exciting development because the partnership between the two companies holds incredible promise in the search for a COVID-19 cure.

In May, Atea Pharmaceuticals essentially dropped all its projects and rebranded itself as a COVID-19 fighter, attracting a stunning $215 million in its venture round.

Among the marquee names that invested in this 7-year-old biotechnology company are Bain Capital and RA Capital.

Going back to its work with Roche, the $350 million cash is expected to fund the ongoing clinical trials of Atea’s very own COVID-19 antiviral treatment called AT-527.

So far, the candidate is in its Phase 2 trial and slated to start global trials or Phase 3 by early 2021.

Apart from being a potential COVID-19 treatment, AT-527 is also under development as a Hepatitis C medication.

In terms of where AT-527 stands in the COVID-19 treatment race, this drug belongs to the same class as Gilead Sciences’ (GILD) Remdesivir and Merck’s experimental candidate with Ridgeback Biotherapeutics called MK-4482.

Like Remdesivir and MK-4482, Roche’s AT-527 is designed to inhibit the replication of SARS-CoV-2, the virus that causes COVID-19.

Unlike Remdesivir though, which is only available through intravenous infusion, AT-527 is an oral drug, making it a more convenient option.

This isn’t the first time that Roche’s COVID-19 efforts came under the spotlight.

Earlier this month, its COVID-19 work with Regeneron (REGN), called REGN-COV2, has been dubbed as a leading candidate in the race because of the high-profile patient who used it: President Donald Trump.

This partnership with Regeneron is expected to ramp up the manufacturing process by at least 3 and a half times compared to their individual capacities.

Outside its COVID-19 efforts, Roche has proven to be a good long-term investment.

Admittedly, the company’s third-quarter report missed the mark by 4% due to aggressive biosimilar competition. However, Roche’s pipeline of newer products has been growing nicely.

Because of biosimilar competition, sales of cancer and immuno-oncology treatments like Avastin fell by 30%, Rituxan slipped by 33%, and Herceptin dropped by 38%.

However, the performance of Roche’s new drug lineup showed promising results, with sales of these products showing off a 32% growth in the third quarter of 2020.

For example, sales of multiple sclerosis drug Ocrevus rose by 37%, while revenue from cancer treatments like Perjeta climbed 17%, Kadycla rose by 33%, and Tecentriq jumped by 49%. Meanwhile, sales of hemophilia medication Hemlibra increased by 57% .

All in all, the hits and misses cancelled out each other this quarter.

Despite the disappointment in these results, Roche stood by its full fiscal year guidance.

This is a strong indicator that the company sees a brighter fourth quarter. Overall, Roche remains in good shape.

Tecentriq has been expanding to cater to other indications such as liver cancer and even some immuno-oncology applications.

Hemlibra continues to outperform its peers, holding on to 25% of the US market share for Hemophilia-A. Even Ocrevus has been outperforming others.

Regarding pipeline developments, Roche has been pouring resources for the trials of NASH drug candidate Crovalimab, which is now in Phase 3.

The acquisition of Inflazome in September and Enterprise Therapeutics in October indicate that Roche is looking to expand in the cystic fibrosis space as well.

Its recently inked agreement with Dyno Therapeutics also signals its plans to work on gene therapies, making itself a potential threat to the likes of biotechnology companies Alnylam (ALNY) and Ionis (IONS).

Looking at everything it has done and has yet to offer, I believe that Roche shares are undervalued at below the high $40s.

This company has a healthy lineup and promising R&D strategies combined with the capacity to buy high-potential assets.

I can see the company generating mid-single-digit cash flow growth on a long-term basis, and I even expect additional improvements to the dividend.

Given the returns you can get from Roche, I can say that this stock is very much worth consideration for any investor interested in quality growth.

Mad Hedge Biotech & Healthcare Letter

October 20, 2020

Fiat Lux

FEATURED TRADE:

THE MOST FAMOUS CANCER STOCK YOU’VE NEVER HEARD OF

(TRIL), (NVAX), (PFE), (IMMU), (SHOP), (GILD), (ABBV)

Biotechnology stocks have proven time and time again to be excellent growth vehicles for risk-tolerant investors.

Underscoring this claim are companies like COVID-19 vaccine frontrunner Novavax (NVAX), which generated jaw-dropping returns on capital for their investors within an impressively short period.

Now, another biotechnology stock is showing telltale signs of following their footsteps: Trillium Therapeutics (TRIL).

Trillium’s story is a familiar one in the biotechnology industry.

Trading only in the penny stock range back in 2019, the company’s share price practically quadrupled since the start of 2020.

Taking into consideration that this meteoric rise actually happened while COVID-19 was blasting the world to smithereens, it’s hardly surprising that this news didn’t receive much media attention.

Trillium’s shares are currently up by an astounding 1,260% -- and the company still has so much room to grow from here.

For context, Trillium had a market capitalization of $7 million in November 2019. This number skyrocketed to $1.3 billion since its shift to cancer technology.

Although a lot of factors came into play, the key turning point for Trillium was when the company decided to go all-in on its cancer programs.

Ultimately, Trillium’s goal is to challenge chemotherapy.

The move to shutter its lead programs on tumor treatments and instead focus on developing cancer-fighting technology was the gamble of a lifetime for the company.

This gutsy move impressed investors, and Trillium was never the same since then.

Today, Trillium is the No. 1 stock on Canada’s S&P/TSX Composite Index, overtaking its previous leader e-commerce giant Shopify (SHOP) by almost 10-fold.

In the US, Trillium shares rank as the No. 4 best-performing company on the Nasdaq Composite Index.

While its epic stock market rally may have some investors feeling left out, all signs point to further gains in the future even for those who missed the initial boom.

Among the major capitalists of this biotechnology company is giant biopharmaceutical company and COVID-19 vaccine leader Pfizer (PFE), which invested $25 million in Trillium’s common stock.

While this equity stake may seem small in relation to Pfizer’s $212.16 billion market capitalization, this initial show of confidence is hailed as a prelude to an even bigger investment in the future.

So far, the most exciting cancer treatments in Trillium’s pipeline are TTI-621 and TTI-622.

These programs are in the same class of emerging cancer technologies, called CD47-based therapies, that prompted Gilead Sciences’ (GILD) $4.9 billion acquisition of Forty Seven, Inc. in April this year.

Aside from Gilead, AbbVie (ABBV) has also been reported to have invested a huge sum in this technology.

In simplest terms, CD47-based therapies can bypass the “don’t eat me signal” put up by some cancer cells in an effort to evade immune detection.

Thus far, both TTI-621 and TTI-622 have been showing promising results. Trillium recently announced that it will increase the dosage in these programs.

While Trillium leaders have not been specific in terms of being open to an acquisition, their recent statements indicate that they are not completely opposed to one.

It’s either that or a partnership with a company as big or even bigger than Pfizer.

As with all the biotechnology stocks, however, there will always be a risk.

For Trillium, the most evident one is competition.

While it’s true that the company has been recognized as the leader in the CD47 arena, more and more competitors are entering the immuno-oncology space.

Right now, the most obvious rival is Gilead, which added Immunomedics (IMMU) to its arsenal via a $21 billion acquisition deal.

Given the sheer amount of money that Gilead has been spending to practically corner the immuno-oncology market, it’s to be expected that more biopharmaceutical titans will enter the fray.

This is one of the reasons Trillium has been tagged as a prime candidate for a massive acquisition deal soon. So far, Pfizer is considered the most probable suitor.

Despite its astonishing performance this year, Trillium’s market capitalization still remains within the small-cap territory. That’s to be expected since its lead assets are still undergoing trials.

Considering that it is an early-stage biotechnology stock, Trillium does not have much in terms of income.

However, the company does have enough cash to last for a while. At the moment, it has $130 million cash.

With its total expenses of $38.8 million in 2019, I say this could offer the company more than three years of breathing room financially.

But it would be shocking if Trillium’s value won’t enter the large-cap territory (higher than $10 billion) if and when the company’s high-value assets reach the late-stage studies.

The fact that it’s also an attractive acquisition candidate offers incredible incentive to its investors.

Simply put, Trillium’s stock could get as much as 1,000% gain over the coming two to three years, making it an ideal investment for risk-tolerant investors.

Mad Hedge Biotech & Healthcare Letter

October 8, 2020

Fiat Lux

FEATURED TRADE:

(CAN REGENERON TRUMP OTHER COVID-19 RIVALS?)

(REGN), (GILD), (SNY), (JNJ), (MRK)

If the experimental COVID-19 treatment of Regeneron Pharmaceuticals (REGN) is good enough for the US president, then this stock should be given more attention not only by the media but also by investors.

One of the biggest stories this October is that President Donald Trump got infected with COVID.

The bigger story for the stock market though is his choice of treatment.

According to his medical team, Trump was given Regeneron’s antibody cocktail, called REGN-COV2, which was actually developed based on the same technology used in the company’s experimental Ebola treatment.

Although REGN-COV2 is still in the trial phase, reports that Trump already beat COVID just three days since his diagnosis are doing wonders for the stock.

Apart from REGN-COV2, Trump also received Gilead Sciences’ (GILD) Remdisivir as well as dexamethasone, a common generic steroid he once touted as a “miracle COVID-19 cure.”

The president was given aspirin and famotidine, which is more widely known as Johnson & Johnson (JNJ) and Merck’s (MRK) Pepcid.

On top of these, he took zinc, Vitamin D, and two immune-boosting supplements.

Compared to how far Gilead’s Remdesivir has gone in terms of offering treatment to COVID-19 patients with severe symptoms, Regeneron’s candidate is nowhere near the finish line.

Among all these drugs, however, Regeneron enjoyed the most advantage, with its stocks rising to roughly 5% since the announcement. Gilead also experienced a boost from the news, with a 3% jump.

What does this mean for investors?

Well, this news triggered aggressive buying of Regeneron shares. As expected, the unusually heavy volume pushed the stock price up.

While it would be tempting to join the market mob in buying a hot stock in the hopes of it getting even hotter, you might want to consider switching gears instead.

Hot stocks that dominate the news tend to cool and end up sliding at some point.

Rather than buying Regeneron stock right now, think about buying its bullish call options.

Options are always cheaper than their associated stock, which means you’ll be less at risk if something happens that lowers the stock price.

Even if the stock continues to advance, investing in options will still ensure that you get a nice return.

After all, each options contract represents 100 shares of stock.

To date, Regeneron’s stock is up 7.2% at $605.

That means you should buy bullish November $600 call options for roughly $40 with the expectation that REGN-COV2 gets approved—or at least stays as a strong contender until the next earnings report.

Since Regeneron released its 2019 third-quarter earnings report on November 5, it’s reasonable to assume that the company will follow the same timeline for 2020.

Therefore, setting the expiration to November ensures that you cover its third-quarter earnings report this year.

Aside from that, you’ll have enough time to gauge the success of REGN-COV2 and how the results will affect the stock price.

If the company’s share price reaches $665 at the expiration date, which is its peak price in the past 52 weeks, the call would be worth $65. If it hits $700, then the call will be worth $100.

For context, Regeneron stock has been anywhere between $279.22 and $664.64 in the past 52 weeks.

If REGN-COV2 gains approval, its projected 2021 sales could reach $1.8 billion. Meanwhile, its 2022 sales could hit $2.4 billion, with a decline to $1.7 billion by 2023.

Outside its COVID-19 efforts, the company has a promising portfolio to keep investors interested.

Regeneron’s annual revenue for its marketed drugs has been consistently climbing since 2012, with the biotechnology company’s earnings beating estimates in the last four quarters.

At the moment, the company has over 30 programs in its pipeline, 9 of which are in Phase 3, ensuring that its portfolio still has so much room for growth.

At the height of the pandemic, Regeneron maintained its stellar balance sheet in the second quarter.

One of its top-selling drugs is atopic dermatitis medication Dupixent, which it developed with Sanofi (SNY), with $770 million in sales for that period alone.

Looking at the drug’s track record, Dupixent is projected to rake in $6.3 billion in sales in 2021.

However, the top performer in the second quarter is eye injection Eylea, which contributed $1.1 billion in sales.

Meanwhile, skin cancer treatment Libtayo generated $63 million and cardiovascular disease drug Praluent raked in $47 million.

Regeneron also finished the second quarter with $943 million in net cash flow, which is a massive jump from the $188 million it reported in the same period in 2019.

On top of Regeneron raking in huge rewards for ’s COVID-19 treatment if approved, the company also has other promising products in its portfolio—ones that can still sway investors in their favor regardless of REGN-COV2’s future.