Mad Hedge Biotech & Healthcare Letter

September 29, 2020

Fiat Lux

(WHY THE PANDEMIC ISN’T STOPPING ELI LILLY’S WINNING STREAK)

(LLY), (PFE), (MRNA), (AZN), (GILD), (INCY), (REGN), (NVO), (BIIB)

Mad Hedge Biotech & Healthcare Letter

September 29, 2020

Fiat Lux

(WHY THE PANDEMIC ISN’T STOPPING ELI LILLY’S WINNING STREAK)

(LLY), (PFE), (MRNA), (AZN), (GILD), (INCY), (REGN), (NVO), (BIIB)

Vaccine developers have taken center stage on Wall Street since the pandemic started, with companies like Pfizer (PFE), Moderna (MRNA), and AstraZeneca (AZN) enjoying soaring share prices for months now.

One of the primary reasons for this popularity is the US government’s Operation Warp Speed, which poured $11 billion into its chosen COVID-19 vaccine programs.

Realistically, the cold, hard truth is that a COVID-19 vaccine will not be the panacea for this deadly virus.

While the vaccine developers are rushing to complete their clinical trials, more people continue to die from COVID-19.

With almost a million deaths and over 30 million cases recorded to date, the need for treatments is more pressing than ever.

Among the companies working on COVID-19 treatments, one name has been quietly making headway: Eli Lilly (LLY).

So far, the company has two potential treatments that can cure COVID-19 patients.

One is its rheumatoid arthritis drug Olumiant, which the company developed with biotechnology firm Incyte (INCY).

Results showed that the treatment can lessen the days patients stay in hospitals when combined with Gilead Sciences’ (GILD) Remdesivir. Not only that, the combination also reduced the severity of the disease and allowed for less-intensive hospital care.

Once all the results have been tested and validated, Eli Lilly will seek an emergency authorization from the FDA.

Aside from Eli Lilly and Gilead Sciences, Pfizer is also working on a potential COVID-19 treatment. Although not much is known about the New York biopharmaceutical giant’s version of the antiviral drug, the target approval date is set in the second half of 2021.

Riding on the momentum of its successful Olumiant trials, Eli Lilly is working to extend its winning streak by being one of the first to develop a preventive COVID-19 treatment specifically designed for elderly patients.

Eli Lilly is developing the potent monoclonal antibody treatment, called LY-CoV555, with AbCellera. The Phase 3 trials conducted in nursing homes were launched in August and the company expects the results to be available by March 2021.

While using monoclonal antibody treatment is groundbreaking technology, Eli Lilly is not alone in the field.

The company faces considerable competition from other healthcare giants like AstraZeneca and Regeneron (REGN).

Nonetheless, the antibody market is massive enough for sharing, with this market estimated to rake in as much as $10 billion annually.

Conservatively speaking and assuming that Eli Lilly fails to attract major market share, there’s still a decent chance that the sales of LY-CoV555 can go beyond $1 billion every year starting 2022.

Outside its COVID-19 programs, Eli Lilly is a dominant player in the diabetes market, with Trulicity leading the charge along with up and coming products like Humalog, Jardiance, Basaglar, and Humulin.

The company is expected to attract at least 13.8% of the market share this year, ranking second only to Novo Nordisk (NVO) and its 30.7% hold of the sector.

In the second quarter earnings report this year, Trulicity sales showed a 20% year-over-year jump to reach $1.2 billion in that period.

This is an impressive performance as investors expect the diabetes drug to surpass its 2019 sales of $4.1 billion.

Although Trulicity delivers substantial sales, it is remarkable that Eli Lilly is not overly reliant on the drug.

In fact, the diabetes drug’s total revenue only accounts for less than one-fifth of the company’s overall sales.

To boost its presence in the diabetes market, Eli Lilly added another potential blockbuster in its pipeline: Tirzepatide.

This drug is projected to become “best-in-class for lowering glucose, weight loss, and cardiovascular risk.”

To date, Tirzepatide is undergoing Phase 3 trials to test it on diabetes, obesity, and heart disease. It is also queued in Phase 2 trials for the liver disease NASH.

The potential of Tirzepatide is hinged not only in being a diabetes drug but more importantly, as an obesity drug.

If successful, Tirzepatide is estimated to hit peak sales of $10 billion annually, with the number trailing by 2025 to record $3.7 billion.

Another potential moneymaker for Eli Lilly is Verzenio, which showed an impressive 56% increase in sales in the second quarter to contribute $208.6 million.

In a bid to expand its oncology pipeline, Eli Lilly is looking into adding a new indication for Verzenio as well.

The company recently released the promising results for the oral tablet as an early-stage breast cancer treatment.

If successful, this drug will be in direct competition against an industry leader, Pfizer’s Ibrance.

In terms of its neurology pipeline, Eli Lilly has also been active in developing its own Alzheimer’s program.

While most of the treatments are still in the early stages, the success of Biogen’s (BIIB) Aducanumab could provide a much-needed boost for Eli Lilly’s own Alzheimer’s candidates.

Eli Lilly offers an extensive product line that goes beyond its COVID-19 programs, underscoring the company’s resilience even during the pandemic.

After dominating in the diabetes sector, the company focused its efforts on becoming one of the top players in the oncology, immunology, and neurology fields.

Consequently, Eli Lilly has been consistent in posting first-rate earnings and revenue growth since 2017.

Eli Lilly markets treatments for life-threatening and chronic conditions, with the company owning the rights to products with consistently growing sales. It also has the ability to continuously boost its revenue stream thanks to its rich pipeline and strategic collaborations.

The COVID-19 pandemic may have negatively affected sectors of Eli Lilly’s business this year, but the company holds the qualities that make it a solid long-term investment.

Mad Hedge Biotech & Healthcare Letter

September 22, 2020

Fiat Lux

Featured Trade:

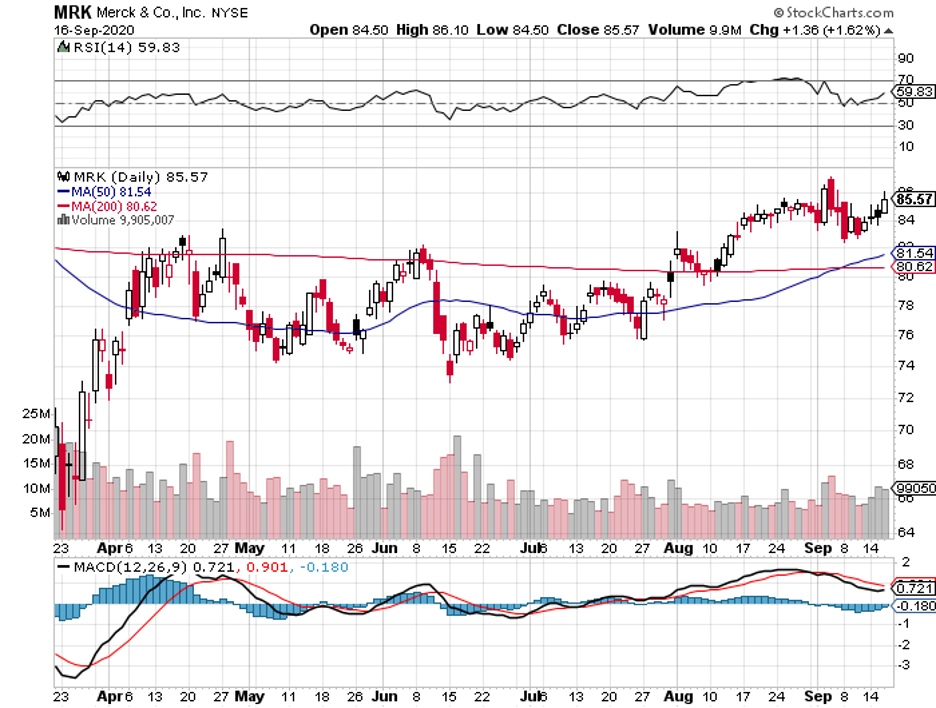

(WHY MERCK IS UNDER-APPRECIATED IN THE COVID-19 RACE)

(MRK), (PFE), (MRNA), (RHHBY), (REGN), (BMY), (GILD)

The excitement over the COVID-19 vaccine candidates has boosted the shares of the most widely reported companies like Pfizer (PFE) and Moderna (MRNA). Meanwhile, other developers have not received the same love from investors.

However, it looks like another COVID-19 vaccine player will be joining Pfizer and Moderna under the spotlight: Merck (MRK).

Merck recently announced that it is now ready to test its vaccine on humans. The trials will be conducted in Germany, and the company has been scouring government databases for viable volunteers.

Unlike Pfizer and Moderna, which are utilizing a novel technology that will need two vaccine doses to be fully effective, Merck is working on two different COVID-19 vaccine candidates designed to work with only a single dose.

This could offer Merck a clear advantage over its competitors.

Also, one of Merck’s candidates could be taken in oral form. This is another significant advantage since it would make the vaccine easier and more convenient to administer.

Merck’s vaccine candidates contain a destabilized version of the same virus that causes measles. This virus is then used to deliver the coronavirus’ spike protein to the patient’s immune system, which would trigger an immune response.

The goal is not only to create a vaccine that would offer protection using a single dose, but also utilizing an existing and reliable technology that can be readily scaled up for mass production.

Since we need to immunize roughly 7 billion across the globe, Merck’s plan to manufacture a single-dose vaccine would be more convenient instead of using multiple doses.

Overall, the COVID-19 vaccine market could reach $50 billion in revenue by 2030.

Apart from its vaccine candidate, Merck is also looking into an antiviral treatment for COVID-19 patients

If successful, this product would be competing against Gilead Sciences’ (GILD) Remdesivir. Just like one of its vaccines, Merck is also developing a treatment in oral form instead of a hospital infusion.

Merck’s Remdesivir alternative can reduce the severity of the COVID-19 by interrupting the virus’s capacity to replicate.

Unlike Gilead’s drug, which can only be used in severe cases, Merck’s candidate can be prescribed immediately after a patient is diagnosed with the disease.

This COVID-19 cure is set to begin its Phase 3 trial this September, with Merck is confident that it can manufacture millions of doses before 2020 ends.

Experts dubbed this drug as an “underappreciated COVID-19 treatment,” which is estimated to reach blockbuster status.

Aside from not getting enough credit for its COVID-19 efforts, Merck is also not receiving enough attention for its pipeline.

So far, the company holds the leading drug that boosts the immune system to fight off cancer: Keytruda. It also has one of the leading vaccine franchises in the world.

Keytruda can easily generate $14.5 billion in sales in 2020 alone, which represents a 30% jump from its 2019 performance. More importantly, the drug can reach $22 billion by 2025.

However, investors are worried over Merck’s dependence on the drug, which comprises 30% of its revenue. In fact, Wall Street keeps zeroing in on the 2028 patent expiration of Keytruda.

At the moment, Keytruda faces competitors like Roche Holding (RHHBY), Regeneron Pharmaceuticals (REGN), and Bristol Myers Squibb (BMY).

However, Merck is not the type to put all its eggs in a single basket.

The company is developing new products that can generate an additional $13 billion to $18 billion in sales annually.

Among these treatments is another potential immuno-oncology antibody, which has been sent to clinical trials this year. Merck also has a long-term HIV treatment queued for clinical studies.

One exciting drug candidate is ARQ531, which is a potential cancer therapy. This projected blockbuster was part of Merck’s $2.7 billion acquisition of ArQule in January.

Other than this acquisition, Merck also obtained the rights to several cancer treatments, which are hailed to be more effective than the conventional chemotherapy, thanks to its acquisitions of Astex Pharmaceuticals and Taiho Pharmaceuticals.

In terms of its vaccine franchise, this arm of the business is projected to generate $9 billion in annual sales in 2021, with the revenue steadily rising to $100 billion in the next several years.

In particular, Merck is looking into developing further its cervical cancer vaccine Gardasil. So far, this vaccine is estimated to generate roughly $3.9 billion in sales in 2020 and reach $5.5 in 2023.

The focus on boosting its vaccine franchise is a strategic move considering that vaccines are generally a durable business and are typically immune from any generic competition.

Although it is not one of the leading vaccine developers in the COVID-19 race, Merck has positioned itself as the leader in the cancer drug development sector and its distribution over at least the next decade.

I believe that Merck’s prudent business, strategic acquisitions, and exciting pipeline will gradually push the stock to the top.

In summary, I think that Merck is a good stock to buy. For those searching for a strong biopharmaceutical play at a reasonable price, this company should be on your shortlist.

Mad Hedge Biotech & Healthcare Letter

September 3, 2020

Fiat Lux

Featured Trade:

(BRACE YOURSELF FOR ANOTHER PANDEMIC)

(AMGN), (NVS), (CYTK), (GILD), (RHHBY), (LLY), (SNY), (REGN)

“Anything that can go wrong will go wrong.”

It looks like Murphy’s law is about to strike again this year. The number of COVID-19 cases has reached almost 15 million worldwide, with about 4 million found in the US alone. However, the pandemic isn’t showing signs of slowing down.

Now, another deadly virus described to manifest “all the essential hallmarks of a candidate pandemic virus” has been found.

Earlier this month, a team of scientists revealed that there’s a newly discovered influenza strain, which could be a variation of the H1N1 swine flu—the same virus that triggered a global pandemic back in 2009.

That health crisis infected roughly 61 million Americans and more than 700 million people across the globe.

Although there’s still no conclusive evidence, this H1N1 influenza strain also traces its origins in China.

We witnessed how the stock market plummeted as the COVID-19 pandemic broke out. It eventually bounced back, which provided us with insights on how to deal with this potential second deadly virus.

Taking into consideration the uncertainty caused by these health and financial crises, I no longer put all my energy on near-term investments.

Instead, I train my eyes on stable and strong stocks with attractive revenue potential.

One of the companies that meet my criteria is Amgen (AMGN).

Amid the coronavirus pandemonium, Amgen has been aggressive in keeping its stronghold, particularly in its key moneymakers.

The latest win for the company is against Novartis (NVS), which challenged Amgen’s patent rights on the blockbuster anti-inflammatory treatment Enbrel.

This patent victory secured exclusivity for the top-selling rheumatoid arthritis injection, which generated $5.1 billion in sales in 2019 and could rake in at least $4.5 billion in 2020, against low-priced copycats until 2029.

Although Amgen has been struggling with biosimilar competition in the past years, the company’s first quarter earnings reports indicate that things are turning around for them.

Amgen reported an 11% year-over-year increase in revenue for the first quarter of 2020 to reach $6.2 billion, with global product sales jumping by 12%, boosted by a remarkable 15% in volume growth.

The company’s free cash flow for the first quarter also went up to $2 billion compared to the $1.7 billion it recorded in the same period in 2019.

The spike in Amgen’s numbers could be attributed to the new products in its pipeline. Apart from Enbrel, there are several other moneymakers generating solid growth for the company.

An obvious game-changer is severe plaque psoriasis medication Otezla, which Amgen acquired from Celgene for $13.4 billion in November 2019.

In the first 3 months of 2020 alone, Otezla has already raked in $479 million in sales for Amgen.

Sales of high cholesterol drug Repatha jumped by 62%, hitting $229 million.

Meanwhile, osteoporosis treatment Evenity contributed $100 million thanks to its expansion in the US and Japanese markets.

With the improvement in its performance, Amgen reiterated its revenue forecast for 2020 of $25 billion to $25.6 billion, showing off a 9.4% gain compared to 2019.

Aside from its current roster, Amgen is also waiting for regulatory approvals on some of its products this year.

The company is hoping for good news from the FDA on its multiple myeloma drug Kyprolis in November and its Rituxan biosimilar candidate in December.

Its pipeline also features 20 late-stage studies, 15 of which are for expanded indications of the company’s already-approved products.

Next to Otezla, Amgen is eyeing another blockbuster following the Fast Track designation granted to heart failure drug Omecamtiv mecarbil.

The drug, which the company is working in collaboration with Cytokinetics (CYTK), is projected to reach a jaw-dropping valuation of roughly $16 billion by 2026.

If successful, Omecamtiv mecarbil could become a close competitor of Entresto, which raked in $569 million for Novartis in the first quarter of 2020 alone.

Meanwhile, Amgen is not only focused on harnessing its growth drivers. The biotechnology giant has been active in searching for COVID-19 treatment as well.

Following the lead of Gilead Sciences (GILD), which used an already approved drug Remdesivir to come up with a treatment, Amgen is also testing its newly acquired blockbuster Otezla.

In using an anti-inflammatory drug to treat COVID-19 patients, Amgen is taking a similar approach as other biotechnology giants like Roche (RHHBY) with Actemra, Eli Lilly (LLY) with Baricitinib, and Sanofi (SNY) and Regeneron (REGN) with Kevzara.

Amgen investors currently get $1.60 in quarterly dividend payments, receiving $6.40 annually. In comparison, shareholders received $1.45 in 2019, showing off a healthy 10% hike.

With a stock price of roughly $235, this puts the company’s dividend yield to somewhere above 2.7%.

This is better than the 2% of investors earn on average from the S&P 500, indicating that Amgen pays investors with an above-average yield. Over the past 5 years, Amgen has boosted its annual dividend by nearly 103%.

Overall, Amgen is a solid long-term investment with promising growth drivers out in the market and in its pipeline.

Another biotechnology company is cashing in on its COVID-19 vaccine efforts: CureVac (CVAC).

CureVac, which has a market capitalization of $9.9 billion, is hoping to follow the footsteps of Moderna (MRNA) and BioNTech (BNTX).

Earlier this year, both small-cap companies saw their value skyrocket, with Moderna now reporting a market capitalization of $27.3 billion while BioNTech is at $16.3 billion.

While the jump in their market capitalization is definitely newsworthy, what is even more impressive is that neither company has a product out in the market today. That is, up until the pandemic struck.

Now, CureVac is looking into raking in the same benefits from its own COVID-19 vaccine work.

Here is a snapshot of how well this stock is doing so far.

CureVac, which raised $213.13 million in its IPO, initially priced its shares at $16 each, started trading at $44 per share and ended the day at $55.90 per share.

The week after, CureVac shares started trading at $79.33 in the premarket hours of Monday, with the price expected to reach an all-time high of approximately $85 per share.

Aside from the Bill and Melinda Gates Foundation, CureVac also attracted backing for its COVID-19 vaccine candidates from the German government and GlaxoSmithKline (GSK). So far, the company has recorded $640 million in funding for its coronavirus program.

What we know about CureVac’s vaccine candidate is that it utilizes the same mRNA-based technology as Moderna and Pfizer (PFE).

While the newly minted biotechnology company is behind competitors, the results of their study are expected to be released by the next quarter.

Prior to prioritizing its COVID-19 vaccine work, CureVac has been focusing on developing cancer and rare disease treatments.

CureVac is also developing CV8102, which is a treatment that can target four different kinds of tumors.

Another frontrunner in its pipeline is CV7202, which is its rabies drug candidate. Its second-generation lipid nanoparticle (LNP) flu vaccine, called CV6301, is also a promising treatment.

Apart from CureVac, another small-cap biotechnology company has been competing against the COVID-19 vaccine frontrunners like AstraZeneca (AZN) and Johnson & Johnson (JNJ).

Earlier this month, Novavax (NVAX) announced the launch of the Phase 2B clinical trial of its COVID-19 vaccine.

The trial for the coronavirus vaccine, called NVX-CoV2373, is set in South Africa and is anticipated to not only provide the company with a larger group but also test the vaccine’s efficacy in an environment where the disease is currently surging.

Although Novavax is also behind the leaders, the level of transmission rate in South Africa, which accounts for half of the COVID-19 cases in Africa, is expected to provide the company a better chance of evaluating its candidate.

Other than that, Novavax has also secured manufacturing deals that can handle more than 2 billion doses.

Novavax has been working on a COVID-19 vaccine since February, with the company receiving $388 million in funding from the Coalition for Epidemic Preparedness Innovations.

By July, the company received a $1.6 billion investment from the US government courtesy of Trump’s Operation Warp Speed project.

If Novavax’s vaccine candidate earns approval, then the company could realistically expect over $10 billion in annual sales.

Riding the momentum, Novavax has also been working on a flu vaccine candidate, called NanoFlu, which can record as much as $1.7 billion in yearly sales.

With the current financial climate, the unprecedented demand for a vaccine will unsurprisingly drive the shares of companies like Novavax and CureVac even higher.

However, it is better to err on the side of caution when it comes to these ultra risky biotechnology companies.

The biotechnology industry has no shortage of investors on the lookout for stocks that can easily make them filthy rich. Although these high-profile stocks can definitely result in massive gains, there are still a number of critical caveats to bear in mind.

While waiting for the actual candidates to get launched, it is safer to bet on tested and proven businesses for now and perhaps dip your toe in the unfamiliar water currently dominated by these small-cap biotechnology companies.

Mad Hedge Biotech & Healthcare Letter

August 13, 2020

Fiat Lux

Featured Trade:

(HOW ROCHE’S STRATEGIC MOAT KEEPS IT AFLOAT)

(RHHBY), (MRK), (GILD), (LLY), (BPMC), (PFE), (JNJ), (ABBV), (NVS)

Moat is a concept that Warren Buffett's followers are well-acquainted with.

In a nutshell, it describes a company’s capacity to keep its competitive edge over its rivals. For the Oracle of Omaha, the safest bets are businesses with large moats because it indicates a strong ability to ward off competitors.

One company that has a particularly strong moat is Roche (RHHBY).

Roche has been at the forefront of the fight against the COVID-19 pandemic.

In mid-March, Roche became the first-ever commercial company to receive an FDA Emergency Use Authorization for its COVID-19 tests. What made this kit, called Cobas SARS-CoV-2 test, impressive is that the turnaround time of less than 4 hours was incredibly fast compared to others.

By April, Roche’s tests were already administered to roughly 4 million people, with some users paying as low as $5 for every test.

Following the success of its tests, Roche ventured into developing a COVID-19 cure.

While there’s still no conclusive data on its tests, Roche secured agreements with the European Commission to be one of the suppliers of the experimental COVID-19 drugs to any of the 27 EU members looking to buy for their constituents.

The deal involves Roche’s RoActemra. Meanwhile, the other supplier is Merck (MRK) with its Rebif.

Aside from that, Roche is also working alongside Gilead Sciences (GILD) in investigating whether Remdesivir could work better when combined with RoActemra.

The other drug undergoing similar compatibility tests with Remdesivir is Eli Lilly’s (LLY) Olumiant.

However, there remains a much bigger story for Roche outside its COVID-19 efforts.

Looking at the company’s first-quarter earnings report, Roche’s pharmaceutical arm generated over 80% of its total revenue for that period.

This is primarily thanks to its strong lineup of drugs, which recorded a 7% increase to reach roughly $13 billion in sales compared to the previous quarter. Overall, Roche recorded a 52.9% growth in its year-over-year quarterly earnings.

The key growth drivers of the company came from its oncology sector.

Leading the charge is bladder and urinary tract cancer treatment Tecentriq, followed by breast cancer drug Perjeta.

Roche’s efforts to expand the label of its blockbuster drug Tecentriq sets expectations for further growth as well.

To further boost its dominance in the oncology field, Roche recently signed an agreement with Blueprint Medicines (BPMC) to gain commercial rights to market thyroid and lung cancer treatment Pralsetinib outside the U.S., excluding Greater China.

This will allow Roche to directly compete with Eli Lilly’s newly gained blockbuster drug Rotovmo, which the company got from its $8 billion takeover of Loxo Oncology in 2019.

Apart from its oncology sector, Roche also saw promising results from other treatments like hemophilia medicine Hemlibra and multiple sclerosis treatment Ocrevus.

On top of Roche’s 37 approved treatments in the market today, the company is expected to submit regulatory findings for almost 20 products this year alone.

Meanwhile, Roche’s $4.3 billion acquisition of Spark Therapeutics in 2019 provided a much-need boost to the company’s gene therapy space.

Despite the uncertainties brought about by the pandemic, Roche’s shares still saw a 10.5% jump this year. In fact, the company increased its 2020 earnings estimate by 0.8% while it expects a 1.4% rise in 2021.

For context, Roche generated $61.5 billion in revenue in 2019 and raked in approximately $13.5 billion in profits. To date, the company pays its shareholders a dividend that yields close to 2.5%.

These reports highlight Roche’s financial stability and strength.

So far, Roche has been able to corner three of the major diseases today: cancer, hemophilia, and multiple sclerosis.

This makes the company one of the biggest names in the biotechnology and healthcare sector in terms of sales.

In fact, Roche is projected to be the No.1 in the field by 2026 with an annual revenue of $62 billion, achieving a compound rate of over 3.6% since its 2019 numbers.

Pfizer (PFE) is expected to land second place, with sales estimated to reach over $56 billion. The rest of the list includes companies poised to record more than $50 billion in sales, namely, Johnson & Johnson (JNJ), AbbVie (ABBV), and Novartis (NVS).

Mad Hedge Biotech & Healthcare Letter

August 4, 2020

Fiat Lux

Featured Trade:

(MERCK’S SLOW BUT STEADY COVID-19 HEADWAY)

(MRK), (GILD), (REGN), (AZN), (PFE), (MRNA), (ABBV), (BMY), (RHHBY)