Mad Hedge Biotech and Healthcare Letter

May 6, 2025

Fiat Lux

Featured Trade:

(AN OLD, BORING DOG WITH NEW TRICKS)

(GSK)

Mad Hedge Biotech and Healthcare Letter

May 6, 2025

Fiat Lux

Featured Trade:

(AN OLD, BORING DOG WITH NEW TRICKS)

(GSK)

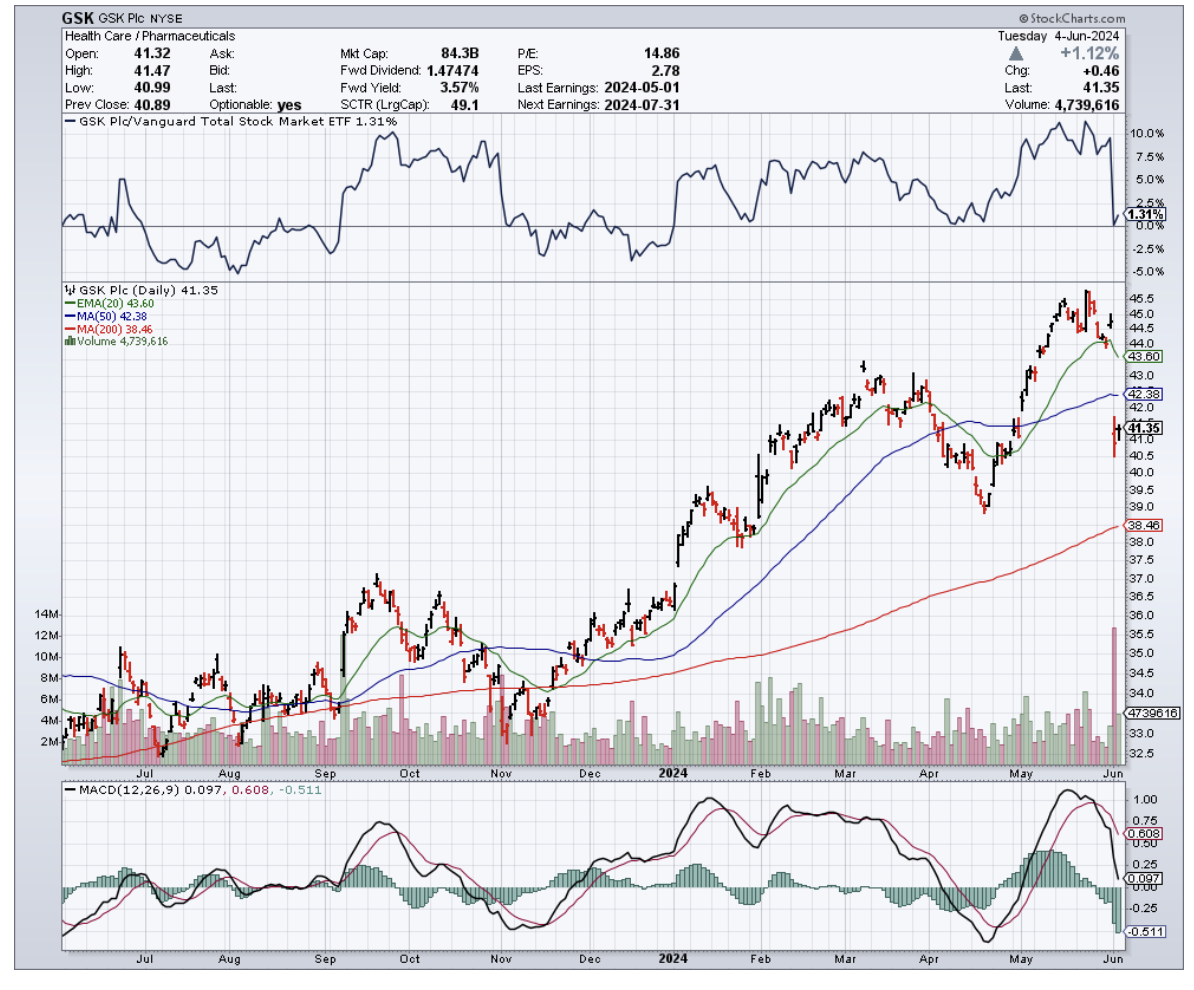

GSK (GSK) isn’t the name that makes your inbox light up or your broker call in a frenzy. No breaking news banner, no meme-stock frenzy. Just a 15% YTD climb while the rest of the healthcare sector stayed in bed.

It’s the kind of move that doesn’t come with fanfare — but it does make you sit up and ask, wait a minute, what’s going on here?

I was at a biotech conference in Basel once, back when I was helping Swiss Bank sort out its Japanese equity derivatives book. Sitting across from me was a pharma strategist with a pension for skepticism and a wine list habit to match. We were trading war stories about the market’s favorite pastime: chasing biotech rocket ships.

He shook his head and said, "The flash fades. The cash sticks." I laughed, nodded, and promptly forgot about it. But seeing GSK quietly tack on 15% YTD while the rest of the healthcare sector has been napping? That line just came roaring back.

That stuck with me. GSK — the British pharma mainstay formerly known as GlaxoSmithKline — isn’t anyone’s idea of a moonshot. No one’s quitting their day job because of a GSK short squeeze. But what it lacks in fireworks, it makes up for in fundamentals, and frankly, that’s more useful in a market like this one.

Let’s get right into it: Q1 2025 numbers just dropped, and they did not disappoint. Revenue was up 4% year-over-year, and earnings per share beat analyst expectations by a comfortable 15.6%. Not the kind of thing that gets retail investors frothing, but real, tangible outperformance in a quarter when much of the healthcare sector has been flatlining.

GSK’s guidance for the year calls for 3–5% revenue growth and 6–8% EPS growth. These aren't blockbuster figures, but they’re dependable. And in a year where the S&P 500 has had more mood swings than a caffeinated options trader, boring might just be beautiful.

Now let’s talk valuation. GSK’s forward non-GAAP price-to-earnings ratio is currently sitting at 8.8x. That’s well below its five-year average of 12.3x, which implies around 40% upside if the market decides to re-rate the stock closer to historical norms.

Even if it doesn’t, that low P/E means you’re not paying up for growth that may or may not materialize. You're buying earnings now, and at a discount.

The dividend doesn’t hurt either. At 4.4%, it’s comfortably above the sector median of 1.6%. And this isn’t a fly-by-night payout either. GSK has shelled out dividends for 23 straight years, with a payout ratio of just 19%.

There’s also the buyback angle. Management has approved $1.33 billion in repurchases for Q2 2025, which is roughly 3.4% of the company’s market cap. That’s not nothing, and it signals a level of confidence from inside the house that’s worth noting.

Of course, it’s not all sunshine and roses. GSK expects its long-term revenue growth to slow post-2026, projecting a CAGR of 3.5% through 2031. That’s down from the 7% they’re targeting through 2026.

Some might see that as a red flag. I see it as realism. Pharma is cyclical. Patent cliffs are real. And growth eventually slows — even in biotech land.

But margins tell another story. GSK’s core operating margin hit 33.7% in Q1, already above their 2026 target of 31%. If that holds, or improves, the impact on profit leverage over the next couple of years could be meaningful.

In plain English: they’re squeezing more out of every pound they earn.

On a longer timeline, the math still works. Assuming steady margins and modest revenue expansion, GSK’s forward P/E could drop to 6.7x by 2031. At that level, it’s almost unreasonably cheap for a company still growing, still paying a dividend, and still buying back its own stock.

In the late 1990s, I was running one of the first global hedge funds with exposure to Japanese equity derivatives — a market that made GSK look like a thrill ride. What I learned back then was that patience, paired with a good entry point, often beats flash and momentum.

GSK right now feels a lot like that. Quietly undervalued. Misunderstood. But building.

No one’s getting rich overnight with this stock. But if you get a dip, it’s worth stepping into. Not for drama. Not for headlines. But for the sort of predictable, well-capitalized earnings stream that keeps the portfolio steady when the rest of the market forgets what a balance sheet looks like.

Mad Hedge Biotech and Healthcare Letter

February 20, 2025

Fiat Lux

Featured Trade:

(PORTFOLIO MANAGEMENT DURING PAIN MANAGEMENT)

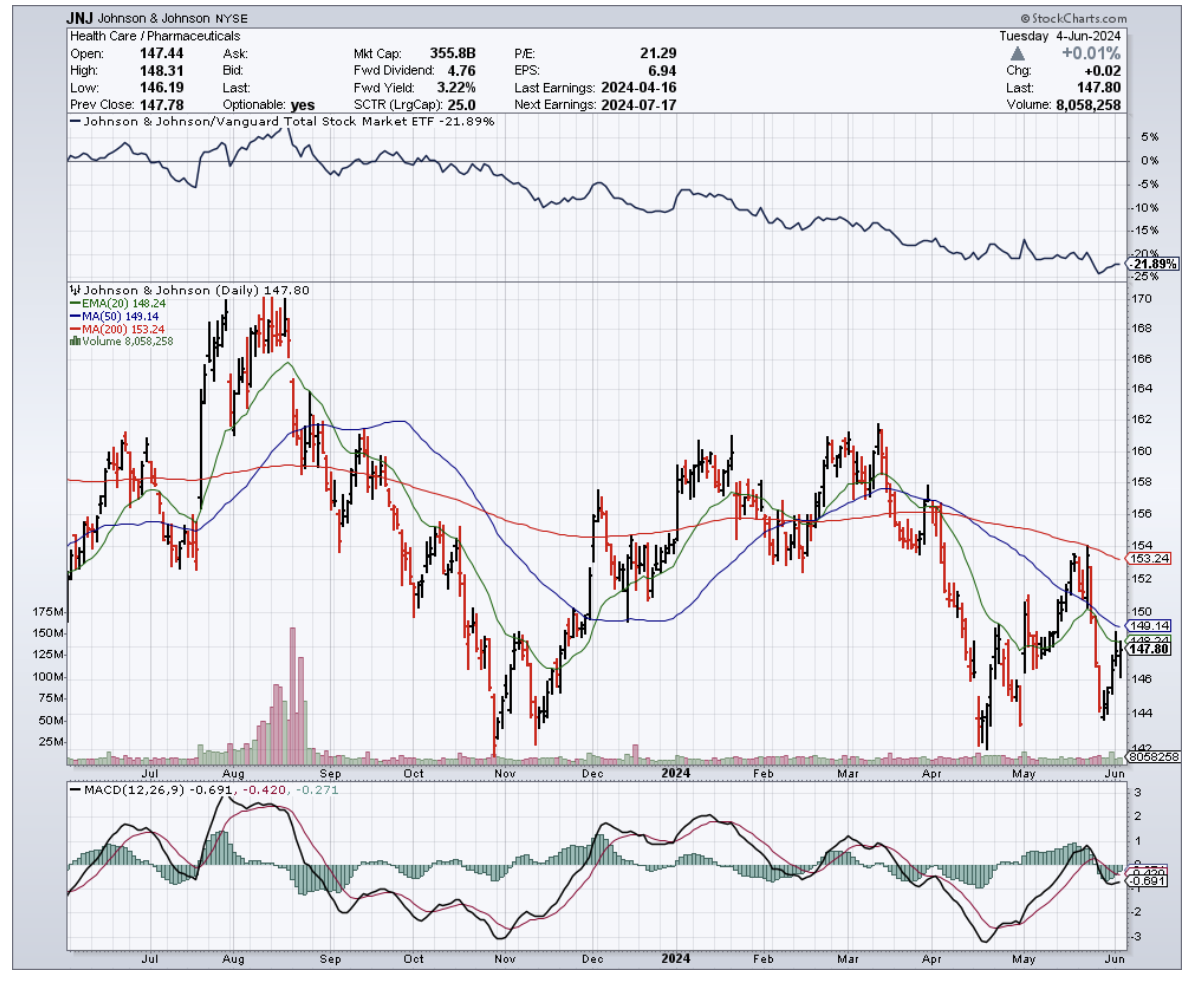

(VRTX), (DSNKY), (AZN), (GILD), (SNY), (GSK), (JNJ), (BMY), (LLY)

Mad Hedge Biotech and Healthcare Letter

July 16, 2024

Fiat Lux

Featured Trade:

(SMALL GIANTS RISING)

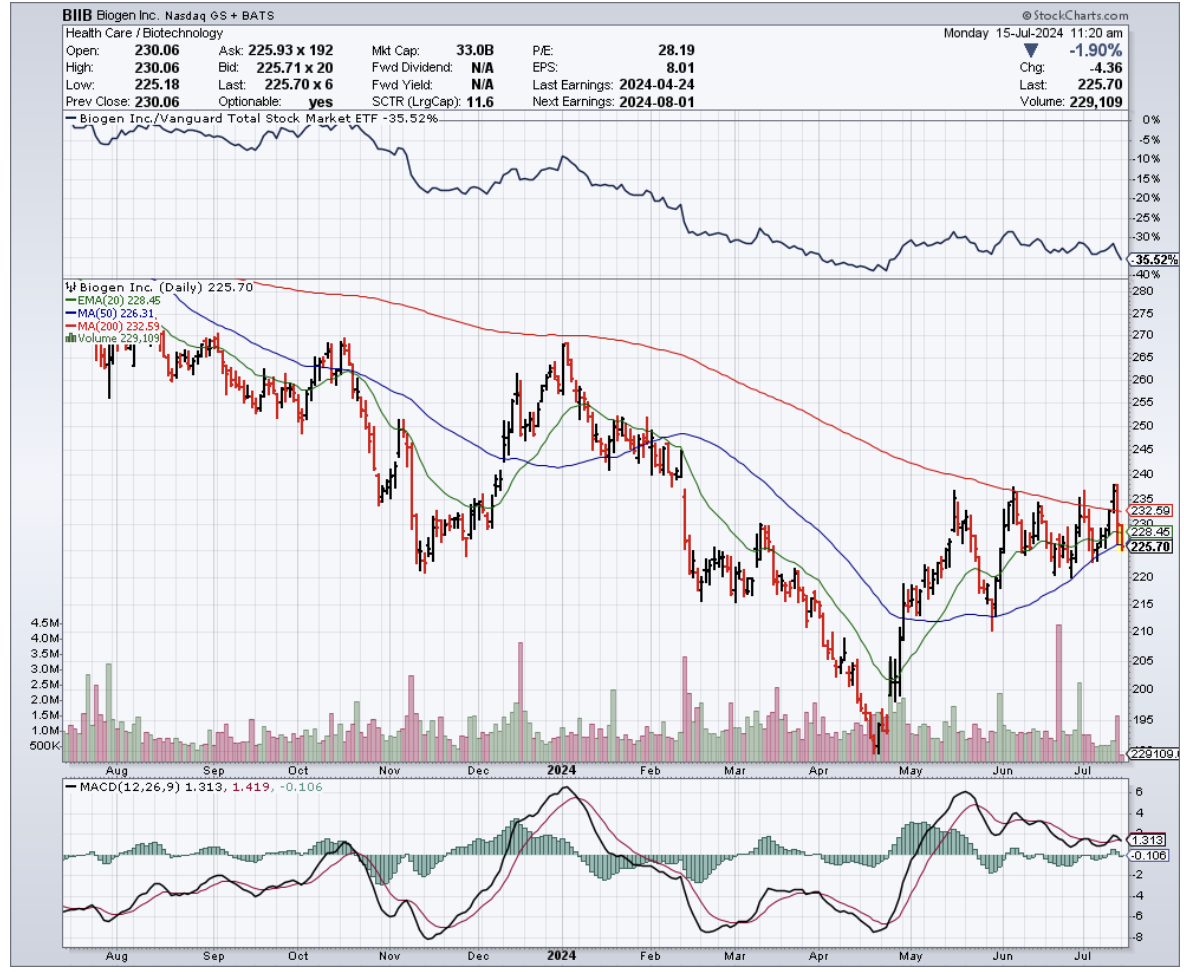

(GMAB), (OPHLY), (VRTX), (INCY), (BIIB), (AHKSY), (ALNY), (ARGX), (BGNE), (MRNA), (NBIX), (BNTX), (IPSEY), (CTLT), (NVO), (LLY), (JNJ), (GILD), (ABBV), (MRK), (SNY), (BMY), (GSK)

Remember when David took down Goliath? Well, history's repeating itself in the biotech arena, and this time, David's got deep pockets and a Ph.D.

Since April, I've been watching a trend on the so-called "next-generation" players in biotech and healthcare world. It reminds me of the massive changes I witnessed in Asian markets back in the '70s.

Over the past months, companies like Genmab (GMAB), Ono Pharmaceutical (OPHLY), Vertex (VRTX), Incyte (INCY), Biogen (BIIB), and Asahi Kasei (AHKSY) have been making waves that would impress even the most seasoned surfer. And these next-gen dealmakers aren't just dipping their toes in the M&A pool - they're doing cannonballs.

With cash reserves that would make Scrooge McDuck blush, these companies are overturning industry norms, already joining the prestigious $100 billion market cap club. At this celebration, the champagne flows freely.

So, what’s the play here?

With IPOs cooling down like day-old coffee, companies eyeing public debuts are now ripe targets for acquisition, more tempting than a juicy peach.

This fresh class of biotechs, unphased by the FTC's scrutiny that acts like kryptonite to pharma giants, are acting more like rocket fuel for these agile consolidators.

They slide through regulatory gaps faster than a greased pig at a county fair, grabbing six out of ten biopharma M&A deals in the second quarter alone. They’re not just taking a slice of the pie—they’re rewriting the recipe.

And if we're talking about firepower? These newcomers boast an average of $3.8 billion in pro forma adjusted cash, which isn't just walking-around money — that's "buy a small country" money.

But don't think for a second that this cash is just sitting pretty in their coffers. These upstarts are putting their money where their mouth is.

Take Incyte, for instance. They flexed their financial muscle with a $2 billion buyback in May 2024, sending a clear message to the market: "We're here to play, and we're playing to win."

And that's just the tip of the iceberg. The industry as a whole is lounging on a cool $1.5 trillion. That's enough liquidity to stretch the imagination — perhaps even to purchase a small planet. Mars, anyone? Elon might give us a discount.

But this financial might isn't just about buying power – it's about survival. As I said before, Big Pharma is teetering on a patent cliff that threatens to erode their revenue streams. To stay competitive, they're scrambling to replenish their pipelines, acquiring promising assets and gobbling up innovative technologies with the voracity of Pac-Man on steroids. And it's not just the usual suspects making moves.

This sense of urgency has created a fertile ground for an emerging cohort of aggressive dealmakers. Companies like Alnylam (ALNY), argenx (ARGX), BeiGene (BGNE), Moderna (MRNA), Neurocrine Biosciences (NBIX), BioNTech (BNTX), and Ipsen (IPSEY) are biting off more than the market expected them to chew, and they're coming to the table hungry.

And these companies aren't just nibbling around the edges. They're making bold moves, acquiring cutting-edge biotech firms with promising pipelines. We're talking oncology, epilepsy, kidney diseases, cardiovascular plays – it's like someone turned a medical textbook into a shopping catalog.

In fact, even the big boys are flexing their muscles.

Novo Holdings (NVO) dropped a jaw-dropping $16.5 billion on Catalent (CTLT). That's not even for a drug - it's for manufacturing. Talk about betting on the picks and shovels in this biotech gold rush.

Eli Lilly (LLY) just plunked down $3.2 billion on Morphic Therapeutic (MORF), betting big on inflammation, immunity, and oncology.

Johnson & Johnson's (JNJ) been on a shopping spree, too, snagging Numab's Yellow Jersey for $1.25 billion and Proteologix for $850 million. Both plays in inflammation and immunity - clearly, they've found their sweet spot.

Biogen's not twiddling its thumbs either, striking a deal with HI-Bio worth up to $1.8 billion.

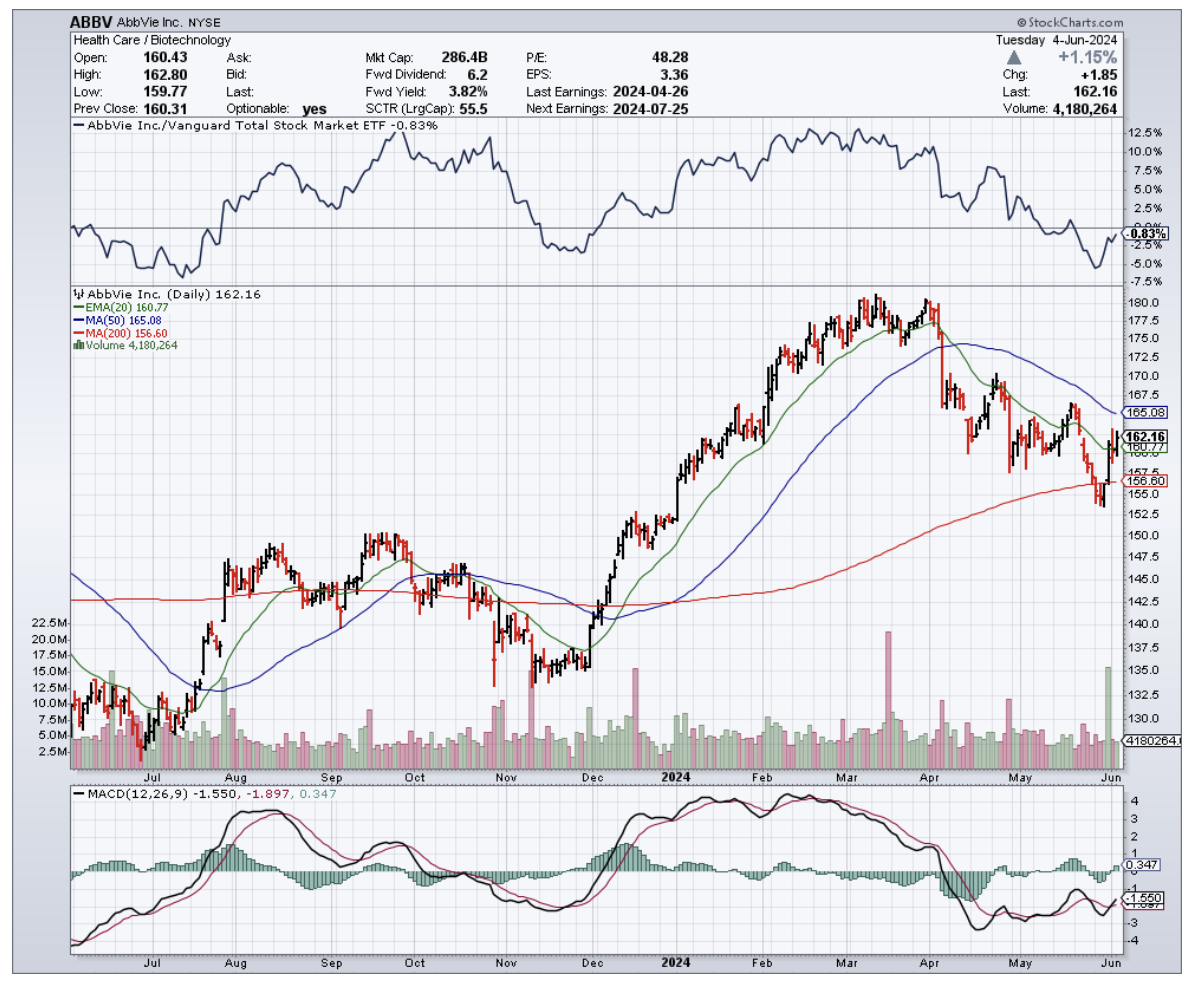

Not to be outdone, Gilead (GILD) shook hands with CymaBay Therapeutics to the tune of $4.3 billion. Even AbbVie (ABBV), playing it cooler, still dropped a cool $250 million on Celsius.

Meanwhile, Merck's (MRK) set its sights on EyeBio for up to $3 billion, focusing on ophthalmology.

Sanofi (SNY), Bristol Myers Squibb (BMY), GSK (GSK) - they're all in, placing their chips on everything from rare diseases to generics to asthma. Clearly, the Big Pharma giants are also trying to keep up with this shift.

As the biotech field evolves, watching these underdogs will be like watching history in the making — where today's Davids become tomorrow's Goliaths. I suggest you keep a close eye on the names above. Adding them to your portfolio would mean you’re not just watching the giants rise — you’ll be a part of the story.

Mad Hedge Biotech and Healthcare Letter

June 11, 2024

Fiat Lux

Featured Trade:

(THE CAPITAL CURE)

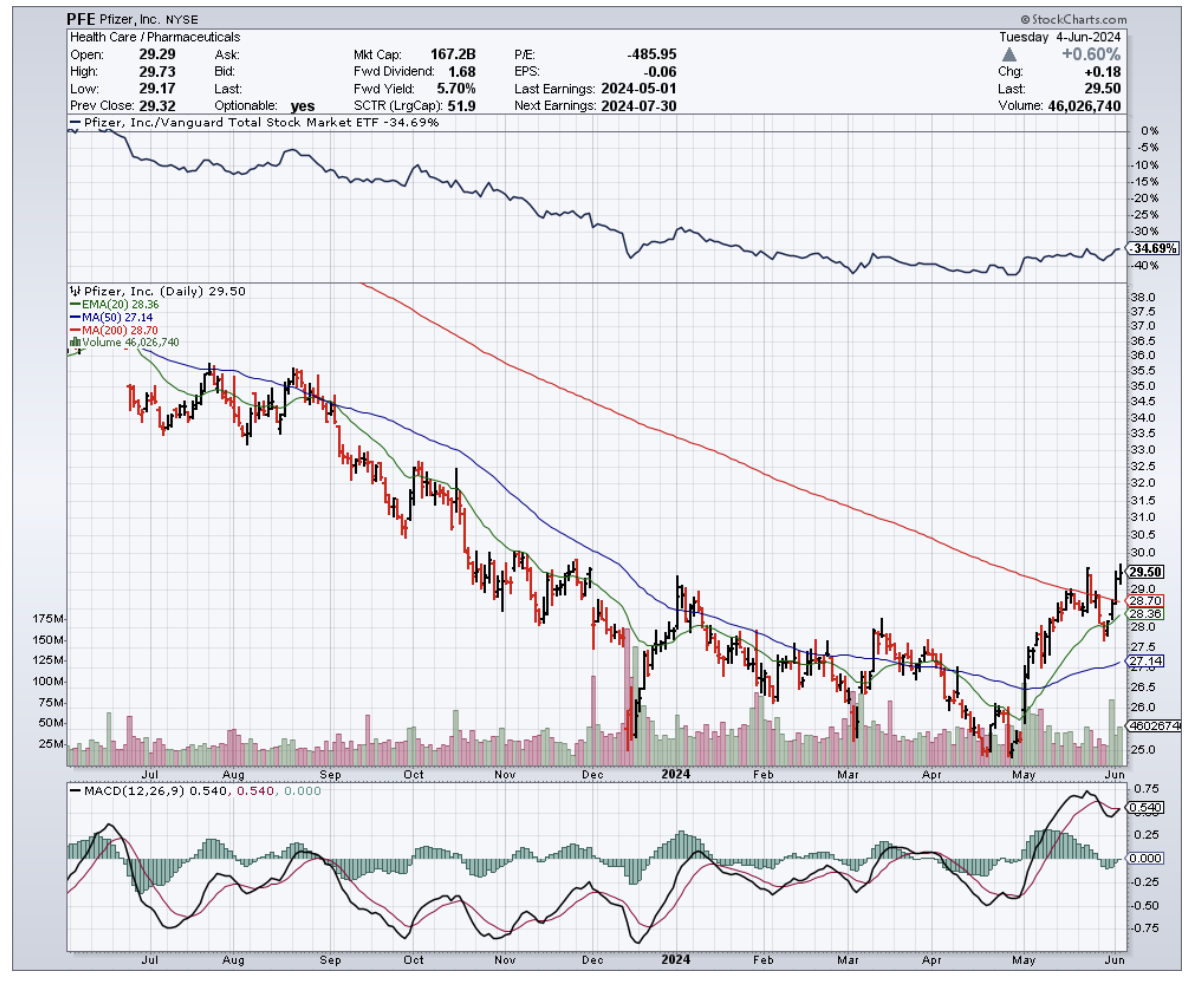

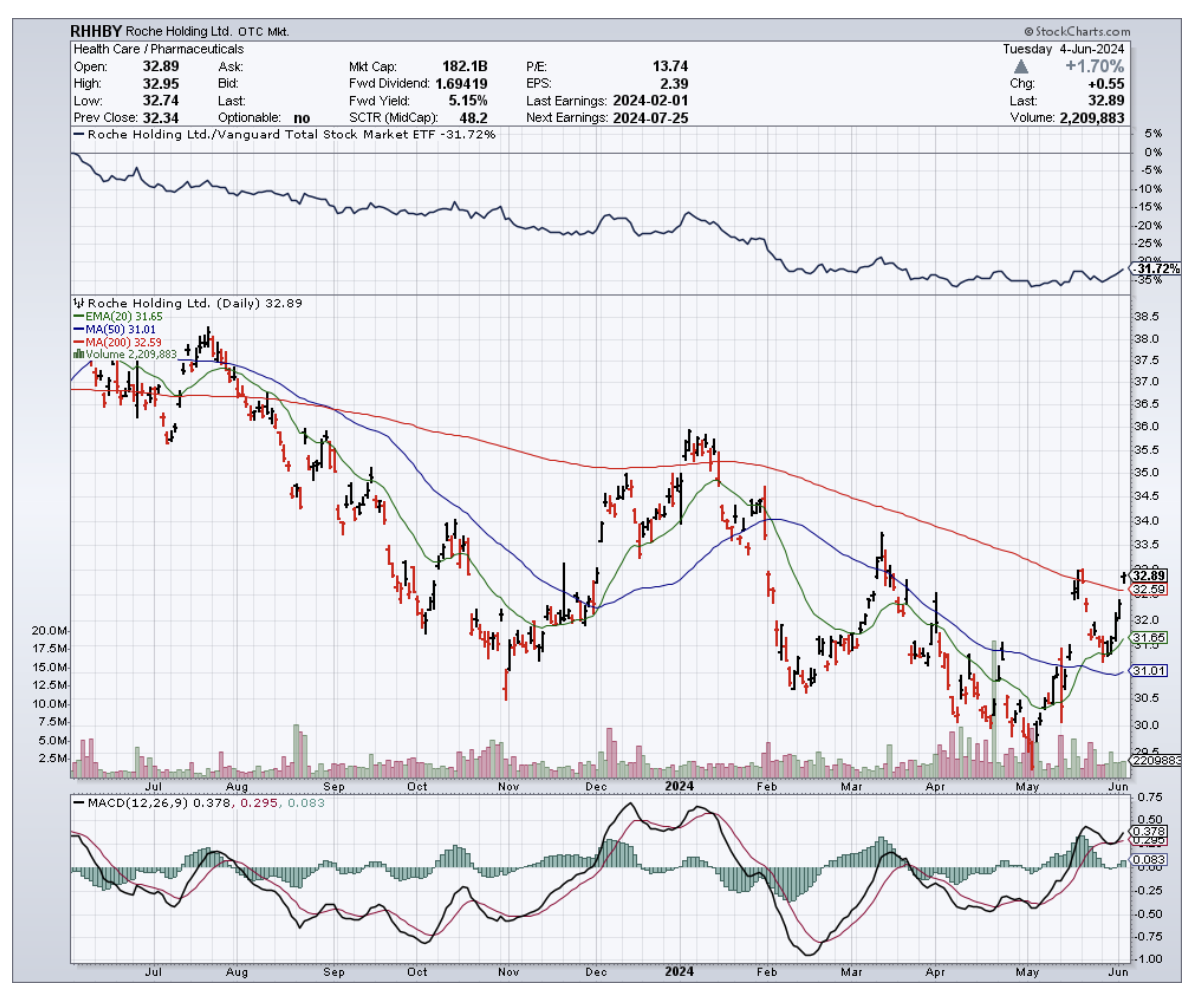

(ABBV), (MRK), (PFE), (RHHBY), (JNJ), (AZN), (GSK), (MRNA), (BNTX), (CRSP), (NTLA), (BEAM), (TPTX), (ZNTL), (MRTX), (BPMC), (MGNX), (TYRA), (SPRT), (VRTX), (FOLD), (RARE), (CRBU)

Imagine you're the CEO of a major pharmaceutical company. You've got blockbuster drugs that are raking in billions, a cushy corner office, and a corporate jet at your disposal. Life is good.

But then, you look at the calendar and realize that your patents are about to expire. Suddenly, that jet feels more like a crop duster, and your corner office starts to feel like a broom closet.

That's the reality facing Big Pharma right now. These pharma big shots are sweating bullets over losing their golden geese like AbbVie's (ABBV) Humira and Merck's (MRK) Keytruda.

That’s roughly $300 billion in products about to get kicked to the curb.

But these guys didn't get to the top by sitting on their hands. They've got a war chest of $1 trillion, and they're not afraid to use it.

Major pharmaceutical giants like Pfizer (PFE), Roche (RHHBY), Johnson & Johnson (JNJ), AstraZeneca (AZN), and GlaxoSmithKline (GSK) are about to go on the mother of all shopping sprees.

Why the rush? Because they're staring down the barrel of a patent cliff that's going to make the Grand Canyon look like a pothole.

We're talking $198 billion worth of branded drugs going off the patent cliff between 2021 and 2025. That's a gut-wrenching 56% jump from the last five years.

But don't think for a second that they're just going to sit back and watch their profits go up in smoke. No sir, they're on the hunt for the next big thing, and they've got their sights set on some juicy targets – and biotech is at the top of their list.

Leading the biotech charge are mRNA pioneers Moderna (MRNA) and BioNTech (BNTX), each sitting on a gold mine of potential blockbusters taking on everything from flu to cancer vaccines.

Underdogs like CRISPR (CRSP) biotech stars Intellia (NTLA) and Beam Therapeutics (BEAM) are also squarely in Big Pharma's acquisition crosshairs for their cutting-edge work in genetic disease treatments.

But beyond the headliners, don't overlook the sleeper hits that could catalyze the next big boom.

Oncology, in particular, is a prime hunting ground, accounting for 37% of pharma M&A deal value in 2023 as the $392 billion global cancer drug market continues to boom.

Companies like Turning Point Therapeutics (TPTX) and Zentalis Pharmaceuticals (ZNTL), with their promising targeted therapies for various solid tumors, are particularly attractive prospects.

Mirati Therapeutics (MRTX), focused on KRAS inhibitors, and Blueprint Medicines (BPMC), specializing in precision therapies, have also caught the eye of big pharma with their innovative approaches.

Additionally, companies with late-stage assets like MacroGenics (MGNX), Mereo BioPharma (MREO), and Tyra Biosciences (TYRA) could offer promising near-term revenue opportunities for acquiring companies looking to bolster their oncology portfolios.

Close behind are rare disease treatments, snagging 16% of new drug approvals and 9 of the top 100 deals last year in this $262 billion market ripe for more growth.

This lucrative sector has captivated pharma giants, who see potential in companies like Sarepta Therapeutics (SRPT) and Vertex Pharmaceuticals (VRTX), leaders in rare disease therapies with strong financial performance and consistent growth.

Aside from these, smaller biotechs like Amicus Therapeutics (FOLD) and Ultragenyx Pharmaceutical (RARE), focused on developing innovative therapies for a range of rare diseases, are attracting attention for their potential to address unmet medical needs and deliver substantial returns on investment.

But the real wild card everyone wants a piece of is cell and gene therapies. This medical Wild West is projected to explode to $66.8 billion by 2030, with the FDA already greenlighting 6 cutting-edge therapies like next-gen CAR-T treatments from Caribou Biosciences (CRBU) in 2023 alone.

Notably, the buying frenzy is very much already underway. In fact, 2023 saw the biggest biotech M&A spree in a decade, with a staggering $122.2 billion changing hands as the FDA approved 50% more new therapies.

Pharma mega-mergers also hit $135.5 billion as firms raced to reload pipelines.

Interestingly, these deals are only the tip of the iceberg. As Wall Street predicts, with record-smashing deals, sky-high demand, and new approvals surging, "biotech's got plenty of reasons to be cautiously optimistic."

Especially if interest rates finally cooperate, throwing gasoline on the M&A bonfire and making biotech the belle of the ball as soon as late 2024.

So keep your eyes peeled and your powder dry. I suggest you add these innovative biotech names to your watchlist, and you might just discover the next blockbuster drug or breakthrough therapy that could reshape medicine – and deliver explosive returns in the process.

Mad Hedge Biotech and Healthcare Letter

April 11, 2024

Fiat Lux

Featured Trade:

(BELLY BUSTERS)

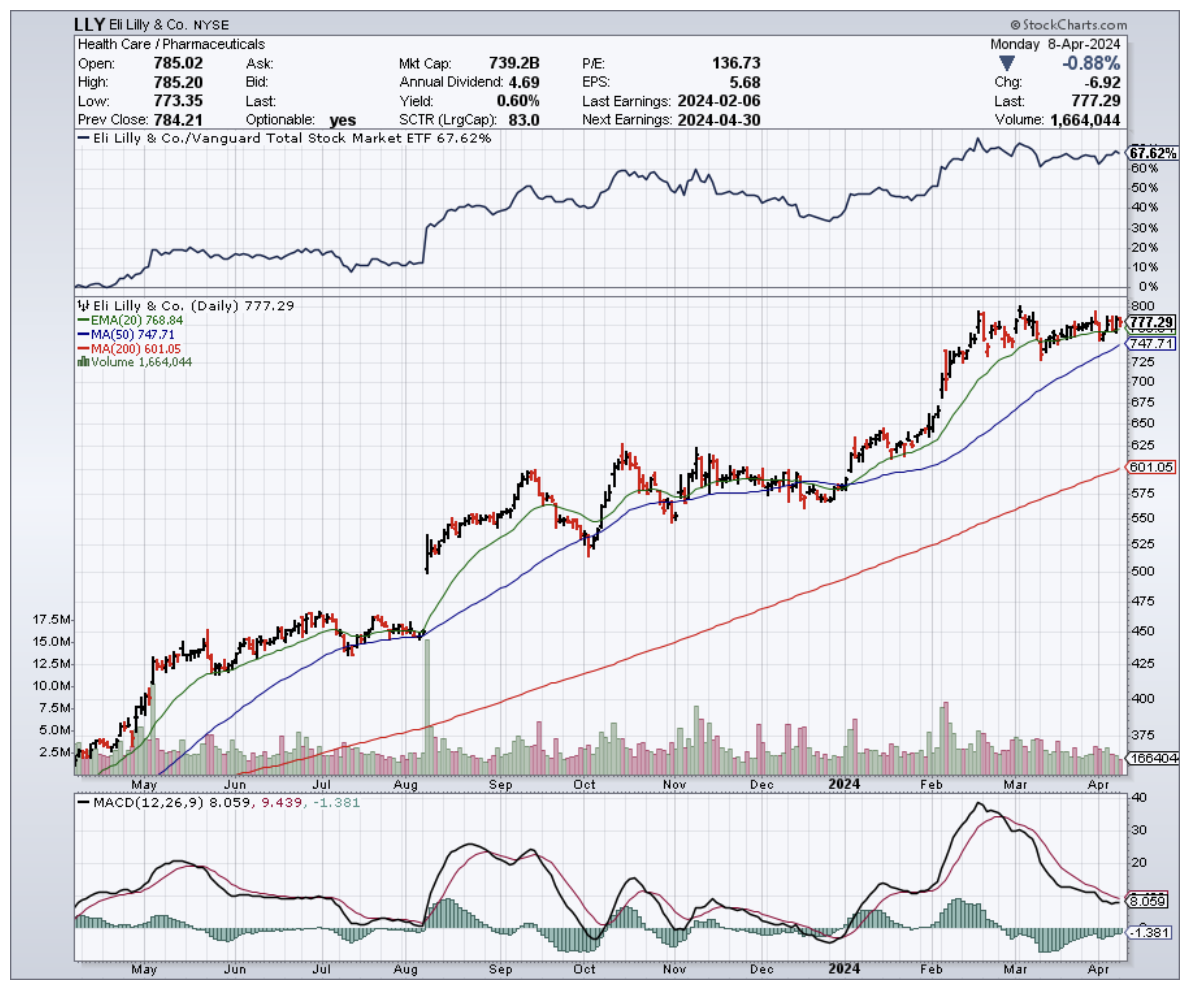

(NVO), (LLY), (JNJ), (AMGN), (RHHBY), (GSK), (VKTX)

Did you know that more Americans are now trying to lose weight than trying to quit smoking? That's a staggering shift, and it has a lot to do with the buzz around those new obesity drugs.

Novo Nordisk (NVO) got the ball rolling in 2021 when they received the green light to market their diabetes drug, Ozempic, as a weight loss miracle called Wegovy.

Not to be outdone, Eli Lilly (LLY) swooped in the fall of 2023 with Mounjaro – also a diabetes drug, sold as Zepbound – that got the FDA nod for weight loss, too.

Then, the whole pharma world, it seems, has started to go all-out on obesity, flooding the market with a whole new generation of weight loss drugs.

To date, there are 124 obesity meds in the works – a mix of 61 Phase 1 hopefuls, 47 in Phase 2, eight in Phase 3, and eight already greeting patients.

Remember that whole fen-phen disaster back in the 90s? That left a bad taste in everyone's mouth when it comes to weight loss drugs.

But things are different this time. These new obesity meds, especially those from Novo Nordisk and Lilly, are a game-changer. They're blowing those old weight loss pills out of the water.

It's not about fitting into those skinny jeans anymore (though that's a nice bonus). The focus is on health.

And while Novo Nordisk and Eli Lilly might be the big names in the obesity drug game, they've got competition. There's a whole crew of pharma companies jumping on the bandwagon, like Currax Pharmaceuticals, Roche (RHHBY), GlaxoSmithKline (GSK) – you get the picture.

But here's the really wild part about these drugs like Mounjaro and Wegovy, which use GLP-1 (Glucagon-like peptide-1) compounds to treat diabetes: They kinda stumbled onto their weight loss powers by accident.

Turns out, while they were busy helping diabetes patients, boom, patients started shedding pounds. Talk about a happy side effect.

As expected, this has created excitement in the market. Now, usually in the drug world, it's baby steps forward. A little better here, a bit less nausea there... yawn.

But with eight of these drugs already in the late stages of development (Phase 3), expect even more surprises as potential breakthroughs could bypass traditional drug trial phases for a faster route to market.

Frankly, I'm shocked at the number of new mystery drugs suddenly popping up in early testing. Even those old-school Big Pharma players are jumping in: AstraZeneca (AZN), Novartis (NVS), Amgen (AMGN), and, heck, even Johnson & Johnson (JNJ) – everyone wants a slice of the obesity pie.

Now, this whole obesity meds craze reminds me of what happened with those PD-1 drugs in cancer treatment.

One good result, and suddenly everyone was scrambling to get their version to market. But like in a reality TV show, not everyone makes it to the finale.

But what's the endgame in this obesity market expansion? Not 124 contenders, that's for sure.

Even right now, with everything in its early stages, you can already see which candidates have the potential. The competition's going to get fierce, and only the strongest drugs will survive.

Viking Therapeutics (VKTX), for example, has a dual GLP-1 and GIP agonist showing serious promise. After just 13 weeks, patients lost an average of 14.7% of their weight.

This data, released in February, proves Viking’s not just chasing the big pharma players; they're running right alongside them.

Now, over at Novo and Lilly, the pace hasn’t slowed down one bit either. Wegovy, which is Novo's contender in the ring, just got a nod in March for something a bit bigger than weight loss.

It’s been approved to tackle some serious heavyweights — cardiovascular deaths, heart attacks, and strokes in adults dealing with obesity or who are overweight. It's like getting a one-two punch for health.

As for Eli Lilly? They’ve been making some noise with tirzepatide, especially around metabolic dysfunction-associated steatohepatitis, or MASH for short.

They’ve got results showing that 74% of adults who were either overweight or obese managed to kick MASH to the curb without any increase in liver scarring after sticking with the treatment for 52 weeks.

Sadly, the biggest roadblock isn't the science, it's the money. It’s not just about making these drugs. It’s about getting them into the hands of those who need them most.

The current scene? A bit of a heartbreaker.

Most US insurance companies are drawing the line at covering Wegovy or Zepbound for obesity. This leaves a hefty bill on the table, putting these potentially life-altering treatments out of reach for many.

Think about it – the people who could benefit the most, maybe those on Medicaid or living paycheck to paycheck, are staring at a closed door. And let’s not even get started on Medicare, which, as of now, can’t even touch these drugs.

It’s a strange paradox, isn’t it? The very treatments that could lift the weight of obesity off society’s shoulders are dangling just out of reach for many.

So, now, the burning question isn’t so much about whether these treatments can make shareholders and companies do a happy dance. It’s more about where we’re heading.

Think about cancer treatment – the sickest patients get the cutting-edge drugs first. What would that even look like in obesity?

Will all these 124 experimental options help level the playing field, finally forcing insurers to step up? Only time will tell.

As of now, the obesity treatment field is going through a revolution. While the market faces challenges like accessibility, I suggest you closely monitor the progress of key players like Novo Nordisk and Eli Lilly.

Consider smaller, innovative companies, such as Viking Therapeutics, for potential high-risk, high-reward investments as well.

Mad Hedge Biotech and Healthcare Letter

March 21, 2024

Fiat Lux

Featured Trade:

(THE COMEBACK STORY WE'RE ALL HERE FOR)

(PFE), (GSK), (LON)