Global Market Comments

November 4, 2022

Fiat Lux

Featured Trade:

(NOVEMBER 2 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (LLY), (TSLA), (GOOG), (GOOGL), (JPM), (BAC), (C), (BRK), (V), (TQQQ), (CCJ), (BLK), (PHO), (GLD), (SLV), (UUP)

Global Market Comments

November 4, 2022

Fiat Lux

Featured Trade:

(NOVEMBER 2 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (LLY), (TSLA), (GOOG), (GOOGL), (JPM), (BAC), (C), (BRK), (V), (TQQQ), (CCJ), (BLK), (PHO), (GLD), (SLV), (UUP)

Below please find subscribers’ Q&A for the November 2 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: The country is running out of diesel fuel this month. Should I be stocking up on food?

A: No, any shortages of any fuel type are all deliberately engineered by the refiners to get higher fuel prices and will go away soon. I think there was a major effort to get energy prices up before the election. If that's the case, then look for a major decline after the election. The US has an energy glut. We are a net energy exporter. We’re supplying enormous amounts of natural gas to Europe right now, and natural gas is close to a one-year low. Shortages are not the problem, intentions are. And this is the problem with the whole energy industry, and the reason I'm not investing in it. Any moves up are short-term. And the industry's goal is to keep prices as high as possible for the next few years while demand goes to zero for their biggest selling products, like gasoline. I would be very wary about doing anything in the energy industry here, as you could get gigantic moves one way or the other with no warning.

Q Is the SPDR S&P 500 ETF (SPY) put spread, correct?

A: Yes, we had the November $400-$410 vertical bear put spread, which we just sold for a nice profit.

Q: I missed the LEAPS on J.P. Morgan (JPM) which has already doubled in value since last month, will we get another shot to buy?

A: Well you will get another shot to buy especially if another major selloff develops, but we’re not going down to the old October lows in the financial sector. I believe that a major long-term bull move has started in financials and other sectors, like healthcare. You won’t get the October lows, but you might get close to them.

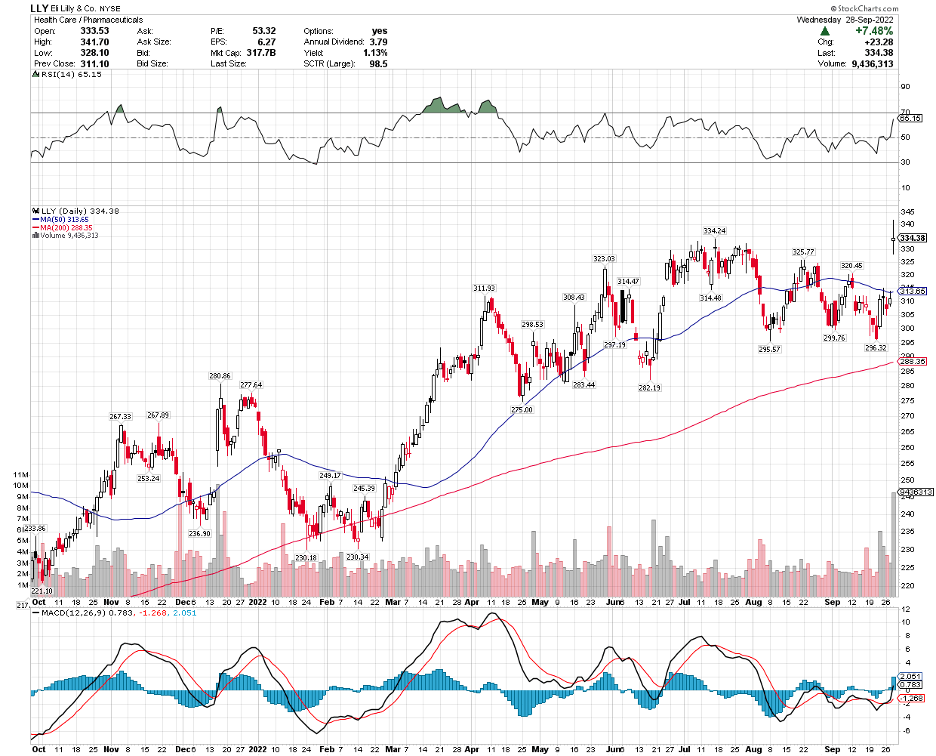

Q: I’m waiting for a dip to get into Eli Lilly (LLY), but there are no dips.

A: Buy a little bit every day and you’ll get a nice average in a rising market. By the way, I just added Eli Lilly to my Mad Hedge long-term model portfolio, which you received on Thursday.

Q: Any thoughts about the conclusion of the Twitter deal and how it will affect tech and social media?

A: So far all of the indications are terrible. Advertisers have been canceling left and right, hate speech is up 500%, and Elon Musk personally responded to the Pelosi assassination attempt by trotting out a bunch of conspiracy theories for the sole purpose of raising traffic and not bringing light to the issue. All indications are bad, but I've been with Elon Musk on several startups in the last 25 years and they always look like they’re going bust in the beginning. It’s not even a public stock anymore and it shouldn’t be affecting Tesla (TSLA) prices either, which is still growing 50% a year, but it is.

Q: In terms of food commodities for 2023, where are prices headed?

A: Up. Not only do you have the war in Ukraine boosting wheat, soybean, and sunflower prices, but every year, global warming is going to take an increasing toll on the food supply. I know last summer when it hit 121 degrees in the Central Valley, huge amounts of crops were lost due to heat. They were literally cooked on the vine. We now have a tomato shortage and people can’t make pasta sauce because the tomatoes were all destroyed by the heat. That’s going to become an increasingly common issue in the future as temperatures rise as fast as they have been.

Q: Do I trade options in Alphabet (GOOG) or Alphabet (GOOGL)?

A: The one with the L is the holding company, the one without the L is the advertising company and the stock movements are really identical over the long term, so there really isn’t much differentiation there.

Q: Why can’t inflation be brought down by increasing the supply of all goods?

A: Because the companies won’t make them. The companies these days very carefully manage output to keep prices as high as possible. It’s not only the energy industry that does that but also all industries. So those in the manufacturing sector don’t have an interest in lowering their prices—they want high prices. If they see the prices fall, they will cut back supply.

Q: What do you think about growth plays?

A: As long as interest rates are rising, growth will lag and value will lead, and that has been clear as day for the last month. This is why we have an overwhelming value tilt to our model portfolio and our recent trade alerts. They’ve all been banks—JP Morgan (JPM), Bank of America (BAC), Citigroup (C), plus Berkshire Hathaway (BRK) and Visa (V) and virtually nothing in tech.

Q: I don’t know how to execute spread trades in options so how do I take advantage of your service?

A: Every trade alert we send out has a link to a video that shows you exactly how to do the trade. I have to admit, I’m not as young as I was when I made the videos, but they’re still valid.

Q: Is the US housing market about to crash?

A: There is a shortage of 10 million houses in the US, with the Millennials trying to buy them. If you sell your house now, you may not be able to buy another one without your mortgage going from 2.75% to 7.75%—that tends to dissuade a lot of potential selling. We also have this massive demographic wave of 85 million millennials trying to buy homes from 65 million gen x-ers. That creates a shortage of 20 million right there. That's why rents are going up at a tremendous rate, and that's why house prices have barely fallen despite the highest interest rates in 20 years.

Q: If we get good news from the Fed, should we invest in 3X ETFs such as the ProShares UltraPro QQQ (TQQQ)?

A: No, I never invest in 3X ETFs, because they are structured to screw the investor for the benefit of the issuer. These reset at the close every day, so do 2 Xs and not more. If you're not making enough money on the 2Xs, maybe you should consider another line of business.

Q: Do you think BlackRock Corporate High Yield Fund (HYT) will show the pain of slights because of their green positioning?

A: No I don’t, if anything green investing is going to accelerate as the entire economy goes green. And you’ll notice even the oil companies in their advertising are trying to paint themselves as green. They are really wolves in sheep’s clothing. They’ll never be green, but they’ll pretend to be green to cover up the fact that they just doubled the cost of gasoline.

Q: Where do you find the yield on Blackrock?

A: Just go to Yahoo Finance, type in (BLK), and it will show the yield right there under the product description. That’s recalculated by algorithms constantly, depending on the price.

Q: Do you like Cameco (CCJ)?

A: Yes, for the long term. Nuclear reactors have been given an extra five years of life worldwide thanks to the Russian invasion of Ukraine. Even Japan is opening theirs.

Q: Should I short the US dollar (UUP) here?

A: The answer is definitely maybe. I would look for the dollar to try to take one more run at the highs. If that fails, we could be beginning a 10-year bear market in the dollar, and bull market in the Japanese yen, Australian dollar, British pound, and euro. This could be the next big trade.

Q: What is your outlook on Real Estate Investment Trusts (REITs) now?

A: I think it looks great. REITs are now commonly yielding 10%. The worst-case scenario on interest rates has been priced in—buying a REIT is essentially the same thing as buying a treasury bond, but with twice the leverage, because they have commercial credits and not government credits. We’ll be doing a lot more work on REITS. We also have tons of research on REITS from 12 years ago, the last time interest rates spiked. I'll go in and see who’s still around, and I'll be putting out some research on it.

Q: How do you see the price development of gold (GLD)?

A: Lower—the charts are saying overwhelmingly lower. Gold has no place in a rising interest rate world. At least silver (SLV) has solar panel demand.

Q: Do you have any fear of Korea going into IT?

A: Yes, they will always occupy the low end of mass manufacturing, and you can see that in the cellphone area; Samsung actually sells more phones than Apple, but they’re cheaper phones with lower-end lagging technology, and that’s the way it’s always going to be. They make practically no money on these.

Q: When can we get some more trade alerts?

A: We are dead in the middle of my market timing index, so it says do nothing. I’m looking for either a big move down or big move up to get back into the market. This is a terrible environment to chase trades when you're trading, so I'm going to wait for the market to come to me.

Q: What about water as an investment? The Invesco Water Resources ETF (PHO)?

A: Long term I like it. There’s a chronic shortage of fresh water developing all over the world, and we, by the way, need major upgrades of a lot of water systems in the US, as we saw in Jackson, MS, and Flint, MI.

Q: Will REITs perform as well as buying rental properties over the next 10 to 20 years?

A: Yes, rental properties should do very well, as long as you’re not buying any city that has rent control. I have some rental properties in SF and dealing with rent control is a total nightmare, you’re basically waiting for your tenants to die before you raise the rent. I don’t think they have that in Nevada. But in Las Vegas, you have the other issue that is water. I think the shortage of water will start to drag on real estate prices in Las Vegas.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log on to www.madhedgefundtrader.com go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

It’s Been a Tough Market

Global Market Comments

November 3, 2022

Fiat Lux

Featured Trade:

(LONG TERM PORTFOLIO UPDATE)

(BMY), (AMGN), (CRSP), (LLY), (EEM), (BABA),

(GOOGL), (AAPL), (AMZN), (SQ), (TBT), (JNK), (JPM),

(BAC), (MS), (GS), (FXA), (FXC), (SLV)

Mad Hedge Biotech and Healthcare Letter

November 1, 2022

Fiat Lux

Featured Trade:

(BARGAIN DEAL FOR A QUALITY STOCK)

(ABBV), (ABT), (RGNX), (JNJ), (MRK), (GILD), (AMGN), (LLY), (BMY), (PFE)

Uncertainty. That’s the prevalent sentiment in the investment community these days.

Investors have been hesitant to buy stocks because they believe the bear market isn’t over yet.

Moreover, investors are anxious over the possibility that the stocks will keep falling as issues like higher inflation continue to hound the market.

However, it’s critical to remember that although today’s situation is challenging, it’s only temporary. This means that businesses with solid track records and promising prospects still make excellent buys.

One of the companies outperforming the market this year but which has fallen out of investors’ favor recently, is AbbVie (ABBV).

AbbVie stock has been declining in value lately following an underwhelming third-quarter earnings report. On top of that, the looming patent expiration of its top-selling drug Humira remains a significant concern among investors.

While the Humira situation is clearly not good news for the company, the reality is that AbbVie has impressively preserved the medication’s exclusivity for almost a decade longer than initially expected. Plus, the company has been boosting Humira pricing every year to cope with the declining revenues in the EU, where it already lost patent protection in 2018.

Hence, it’s acceptable for Humira’s chapter in AbbVie’s story to end. After all, the drug has given the company so much. It has been primarily responsible for the more than 325% climb in the company’s share price since 2012 when AbbVie was spun out of Abbott Laboratories (ABT).

Nonetheless, Humira’s impending patent loss doesn’t mean that AbbVie will simply abandon its roots.

The company has since developed potential successors of Humira, namely, Skyrizi and Rinvoq.

So far, the two auto-immune drugs have delivered promising results and are on track to keep the company in tip-top shape in its post-Humira era.

These newer immunology drugs are showing impressive growth potential, with Rinvoq recording a 56% increase in revenue in the third quarter of 2022 and Skyrizi revenue soaring by 85%.

Both are also on track to beat Humira’s peak sales, with joint peak sales from Skyrizi and Rinvoq initially estimated to reach roughly $15 billion.

However, recent revenue reports show that the two could surpass the estimate and completely eclipse Humira’s more than $20 billion annual return.

Obviously, AbbVie would require more than its immunology segment if it plans to sustain a good top and bottom-line growth trajectory.

Other than the more than 10 neuroscience, hematology, immunology, and oncology candidates in its pipeline, which are projected to be ready for market launches in the three to five years, AbbVie has been diving into the aesthetics and eye care markets.

Its eye care program, specifically RGX-314, which is currently being developed in partnership with Regenxbio (RGNX), is an interesting wildcard. For context, the eye care segments for wet and dry advanced macular degeneration are roughly worth over $10 billion to $20 billion annually.

With its Humira chapter closing, AbbVie could be ushering in a new era where products from its Allergan acquisition take the lead.

For example, its Botox franchise consistently delivers impressive results. Even its Botox for migraine line has been recording double-digit revenue growth in the third quarter, indicating gains in AbbVie’s neuroscience segment.

As for the aesthetic indications of Botox, this particular portfolio could be a key driver in the company’s future growth.

Aside from Botox, AbbVie also gained access to the widely used dermal filler Juvederm. With the facial aesthetics industry pegged to experience a compound annual growth rate yearly at 14%, the market is estimated to hit $15.2 billion by 2028.

This trend of AbbVie dominating the market is likely to continue as the company is confident that competitors would be unable to develop biosimilars of Botox. That means its Botox line could keep adding to its top-line growth for an extended period.

Overall, AbbVie is a solid bet among the “Big 8” in the pharmaceutical world, which includes Johnson & Johnson (JNJ), Merck (MRK), Gilead Sciences (GILD), Amgen (AMGN), Eli Lilly (LLY), Bristol Myers Squibb (BMY), and Pfizer (PFE).

Moreover, this is an excellent time to hunt for deals as several quality stocks continue to decline, affected negatively partly by the momentum of the broader market. Among stocks to consider, AbbVie should be at the top of your list.

Mad Hedge Biotech and Healthcare Letter

October 13, 2022

Fiat Lux

Featured Trade:

(A SAFE BET IN A VOLATILE MARKET)

(AMGN), (NVO), (LLY)

The biotechnology and healthcare industry is fraught with risk. However, it’s also brimming with opportunities.

On the one hand, a new drug takes years of clinical research. On top of that, the average cost to bring each product to the market reached $1 billion between 2009 and 2018.

On the other hand, the chosen few that receive the green light from the FDA more often than not deliver on their promise to become blockbusters, raking in sales of over $1 billion every year.

This arguably justifies the risks that come with the industry.

Amgen (AMGN) has become the recent embodiment of this promise. Despite the volatility of the market in the past months, the company remains a strong player thanks to several factors that could bolster its share price.

In particular, Amgen investors are looking forward to potential gains courtesy of the pipeline of drugs slated for market release over the medium term.

The most exciting among them is its obesity drug AMG 133.

The positive data from AMG 133’s unveiling had experts excited over the drug, with many expecting it to become a multi-billion dollar revenue stream for Amgen.

As expected, Amgen will be facing stiff competition in this market, specifically between 2025 and 2030.

To date, investors have been closely monitoring the obesity segment, with two companies clearly leading the charge: Novo Nordisk (NVO) and Eli Lilly (LLY).

Novo Nordisk markets Wegovy, which is a shot that targets obesity by zeroing in on the glucagon-like peptide receptor, or GLP-1. This is also the same target for many diabetes treatments.

Meanwhile, Eli Lilly is working to integrate obesity as part of the conditions treated by its recently approved diabetes drug Mounjaro. Like Wegovy, this drug also targets GLP-1.

What makes it more potent is that it also targets glucose-dependent insulinotropic polypeptides or GIP. Both GLP-1 and GIP are hormones linked to blood sugar control.

What makes AMG 133 different from other approved and experimental treatments for obesity is that it blocks not only a particular hormone but also a specific protein involved in controlling blood sugar.

While it targets GLP-1, Amgen’s candidate works on a gut protein linked to digestion, called the gastric inhibitory polypeptide receptor, or GIPR.

The obesity market is a lucrative space since the medical world now categorizes obesity as a type of chronic illness instead of a mere consequence of lifestyle choices.

That is, obesity drugs are on the cusp of entering the mainstream primary health care system.

An apparent precedent for this opportunity is the high blood pressure sector, initially a nascent segment in the 1980s and eventually skyrocketed to a $30 billion industry by the 1990s.

In 2022, the obesity market is estimated to be worth $2.4 billion. By 2030, this space is projected to reach $54 billion.

That places all competitors in the same space, Amgen, Eli Lilly, and Novo Nordisk, in excellent positions. In fact, Novo Nordisk has been dealing with shortages of Wegovy due to rising demand.

While any upgrade or downgrade prompted by a single drug’s potential, or even multiple treatments’ potential, is exciting, it should be taken with a grain of salt.

The biotechnology and healthcare industry is continuously in flux, and any company in the sector is one major failed trial or one rival’s success away from facing trouble. Simply put, they tend to be volatile.

Amgen is not an exception to this harsh truth despite the company’s solid obesity prospects and impressive portfolio and pipeline. That means investors expecting an immediate payout following the recent developments might get disappointed.

Nonetheless, it’s also vital to remember that biotechnology and healthcare stocks tend to deliver better results than the broader market even amid the economic turmoil.

These companies seem to operate and function outside typical economic cycles, providing investors with dependable performance when most businesses are struggling.

Amgen is one of the biggest biotechnology companies in the world. It has been one of the pioneers in this segment since the 1980s. It’s also a part of the prestigious Dow 30 list of companies.

Moreover, it has a massive and diversified product portfolio, with nine treatments that individually generate more than $1 billion in sales annually.

These drugs are not only huge sellers, but also offer wide margins because of the existing restrictive and high barriers to entering the biotech world.

Hence, this enables Amgen to enjoy a remarkable pricing power and autonomy over its products while still growing its top line at a steady pace.

If you’re looking for a conservative and attractive long-term investment, then buying Amgen when the price drops wouldn’t be a bad bet.

Mad Hedge Biotech and Healthcare Letter

September 29, 2022

Fiat Lux

Featured Trade:

(TAKING ON THE WEIGHT OF THE WORLD)

(LLY), (NVO)

This is not your run-of-the-mill weight-loss story.

The number of obese American adults has climbed from 13% to 43% in the last 60 years. That’s approximately 100 million individuals in the United States alone.

The average American male currently weighs about 200 pounds, up from 166 back in 1960, while the average female is at 171 pounds, up from 140.

Obesity, or just being overweight, has several ripple effects. This carries the risk of diabetes, cardiovascular issues, and even cancer. It can also interfere with a person’s work, sleep, and other day-to-day activities.

Many factors have been studied as potential reasons behind obesity, but it has become very clear that solving the epidemic would need more than simply diet and exercise.

Taking on this challenge are Eli Lilly (LLY) and Novo Nordisk (NVO), competitors that came up with a promising drug, known as incretins, to hopefully solve the issue.

Amid all the dietary fads, supplements, and exercise trends we’ve seen, we are on the cusp of finally getting safe and effective drugs for this condition.

We can go as far as claiming that these could very well be our best hope in the fight against obesity. This epidemic has been threatening the way of life of over 100 million Americans and roughly half a billion people globally.

Nobody has ever witnessed the weight loss offered by this new category of drugs, called incretins.

Scientific research has enabled people to shed over 20% of their weight. Needless to say, incretins could become the top-selling drugs in the history of the pharmaceutical industry.

For context, a drug is tagged as a “blockbuster” when it manages to record $1 billion in sales annually. To date, the top-selling drug worldwide is Humira from AbbVie (ABBV), with roughly $20 billion in yearly sales.

If each obese American sought treatment (and given the projected prices of these drugs) the yearly sales for incretins would hit at least a trillion dollars.

Obviously, insurers would refuse to pay these sums, which is why studies have been conducted to show how these drugs could effectively prevent critical conditions like diabetes and heart disease. That is, it will be considered a maintenance drug.

Marketing incretins as treatments for diabetes and obesity could rake in $50 billion to $60 billion in sales over the next decade. As of the moment, the market is dominated by a duopoly of Eli Lilly and Novo Nordisk.

Recently, Eli Lilly gained much attention after its diabetes drug Mounjaro received FDA approval. While the product was given the green light earlier in 2022, the company has also become more aggressive in marketing it as an anti-obesity treatment.

When it goes to market, Mounjaro is expected to go head-to-head against Novo Nordic’s Wegovy. Both target basically the same market, but Eli Lilly’s candidate showed better results.

According to Eli Lilly, patients given the highest dosage of Mounjaro recorded an average weight loss of 22.5% over roughly 18 months.

In terms of sales potential, Wegovy reached $183 million in the first quarter of 2022. With Eli Lilly hot on its heels, investors should expect a slide in Novo Nordisk’s sales for this product.

When Mounjaro was initially released, it was expected to reach peak sales of $15.4 billion. However, the drug’s effectivity and potential to address weight loss boosted predictions to $25 billion.

The reason for the increase in confidence in Eli Lilly’s drug is pretty simple. Offering treatment to 1.6 million Americans yearly would generate $20 billion in sales in the US alone—which only comprises 2% of the estimated population of obese individuals in the country.

Either way, it’s a massive market. Dominating a small portion would already move the needle for any biopharmaceutical company. Hence, I recommend you buy the dip for these companies aiming to solve the obesity epidemic.

Mad Hedge Biotech and Healthcare Letter

September 27, 2022

Fiat Lux

Featured Trade:

(LAST CHANCE AT SALVATION)

(BIIB), (ESALY), (RHHBY), (LLY), (NVS), (AMGN), (REGN), (BMY), (ABBV), (MRK), (PFE)