Mad Hedge Biotech and Healthcare Letter

December 26, 2024

Fiat Lux

Featured Trade:

(PHASE 2 OR NOT PHASE 2: THAT'S NOT EVEN A QUESTION IN 2025)

(LLY), (NVO)

Mad Hedge Biotech and Healthcare Letter

December 26, 2024

Fiat Lux

Featured Trade:

(PHASE 2 OR NOT PHASE 2: THAT'S NOT EVEN A QUESTION IN 2025)

(LLY), (NVO)

I had dinner with a veteran biotech investor at San Francisco's Waterbar earlier this month, watching the Bay Bridge lights while discussing what's coming for biotech in 2025.

"The game is changing," he said, picking at his salmon. "It's not about platform promises anymore. Show me the Phase 2 data, or don't show up at all."

He's nailed what I've been seeing in my recent travels through the biotech corridors of Boston, San Diego, and Basel. The days of throwing money at shiny new platforms are ending.

That means that by 2025, we'll see venture capital concentrate in fewer but larger deals, especially in companies with solid Phase 2 data.

Let me break down what this means for our portfolio next year. First, North America will dominate in advanced biologics and AI-driven drug discovery. I've toured enough labs recently to see that our capabilities in these areas are leaving others in the dust.

Europe's doubling down on sustainable manufacturing and rare diseases - smart move given their regulatory environment. Asia? They're positioning to own generics and biologics manufacturing, with India making particularly interesting moves in antibody-drug conjugates.

The money's following these regional specialties. If you're investing in biotech companies that don't align with their region's strengths, you might find yourself waiting longer for returns than a Red Sox fan waiting for another World Series.

My contacts in several major VC firms confirm they're already adjusting their 2025 strategies around these regional strengths.

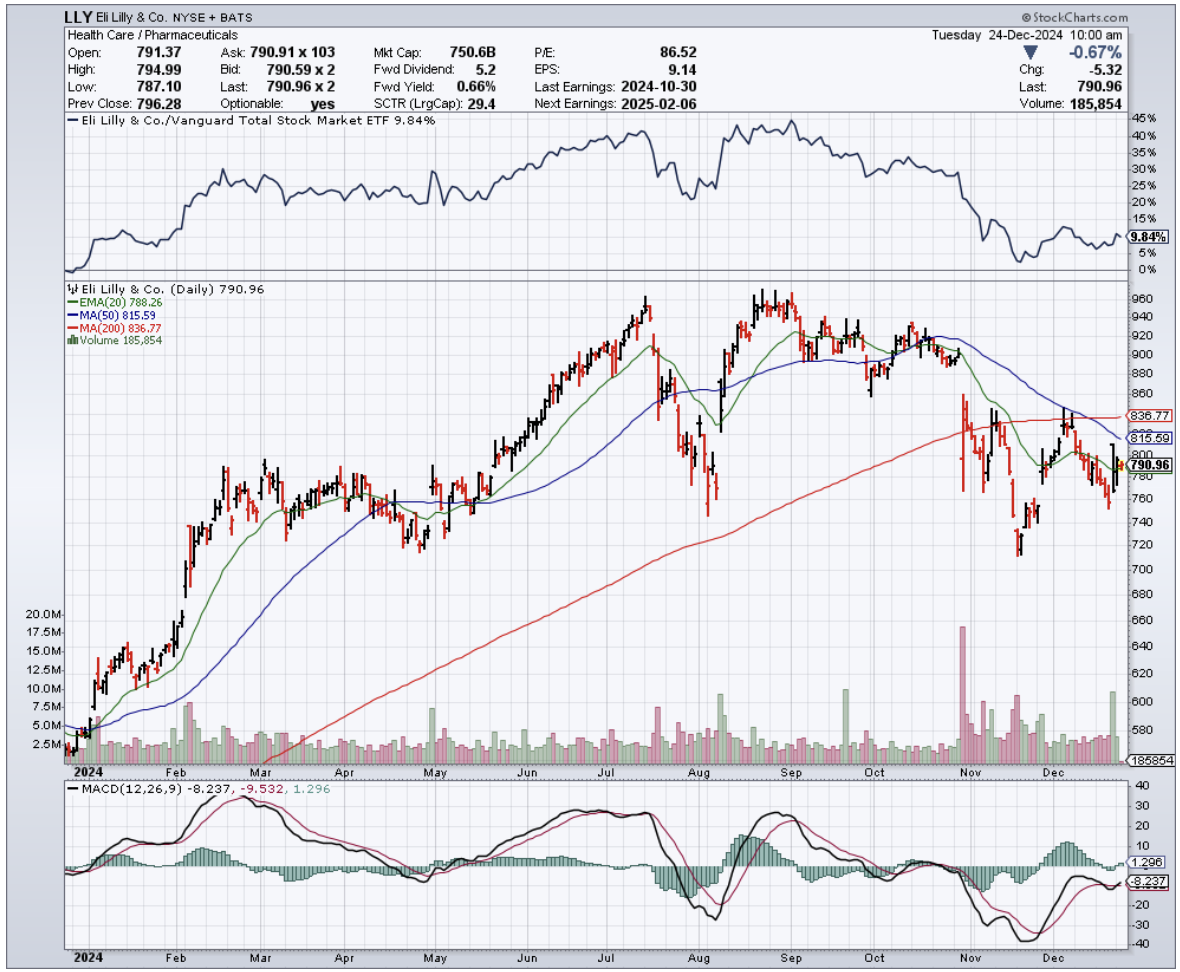

Here's what's really interesting: obesity and GLP-1 drugs are the exception to every rule. After watching Eli Lilly (LLY) and Novo Nordisk's (NVO) recent success, everyone wants a piece of this action.

Even early-stage obesity plays are attracting serious capital, bucking the trend toward late-stage investments.

But remember this about 2025 - being picky about Phase 2 data isn't just smart, it's survival. We're heading into a market where strong clinical validation will matter more than ever.

I've seen enough biotech cycles to know that when the market gets selective, you want to be where the data is solid.

The numbers back this up. Looking at the trends, Phase 2 companies have consistently captured the highest deal sizes, except for that brief period in 2023 when obesity deals sent Phase 1 valuations through the roof.

By 2025, expect this preference for Phase 2 assets to become even more pronounced. Phase 3 investments have been declining - dropping from $4.2 billion in 2021 to $1.7 billion in 2024 - partly because companies with strong Phase 2 data are getting snatched up through partnerships or acquisitions before they even get to Phase 3.

Speaking of partnerships, watch Big Pharma's moves carefully in 2025. They're increasingly hungry for de-risked assets, and strong Phase 2 data is their favorite meal.

I had lunch with a Big Pharma exec last week who told me they've completely restructured their BD team to focus on Phase 2 assets in their regional sweet spots.

As for AI platforms? They'll still get funded - companies like Xaira and Generate:Biomedicines are proving that. But by 2025, they'll need to show more than just fancy algorithms. The market's going to demand real clinical validation.

I recently visited an AI-driven drug discovery company where the CEO proudly showed me their latest neural network. "That's great," I told him, "but show me your clinical data." The silence was deafening.

So, what’s the play here? Well, I'm keeping my own biotech portfolio focused on companies with strong Phase 2 assets heading into 2025, especially in regional sweet spots.

And yes, I've got a position in the obesity space - sometimes a trend is too strong to ignore, even for an old contrarian like me.

One final thought: keep an eye on those time gaps between funding rounds. They're getting longer, and by 2025, companies that don't fit neatly into regional specialties or lack solid clinical data might find themselves in the financial equivalent of a Phase 2 trial that never ends.

Now, if you'll excuse me, I've got a call with a German biotech CEO about their sustainable manufacturing process. These regional specialties aren't going to research themselves.

Mad Hedge Biotech and Healthcare Letter

December 24, 2024

Fiat Lux

Featured Trade:

(THE LAB RESULTS ARE IN)

(GILD), (TSLA), (WVE), (EDIT), (CRSP), (LLY), (NVO), (WMT), (CVS), (CCCC), (RHHBY)

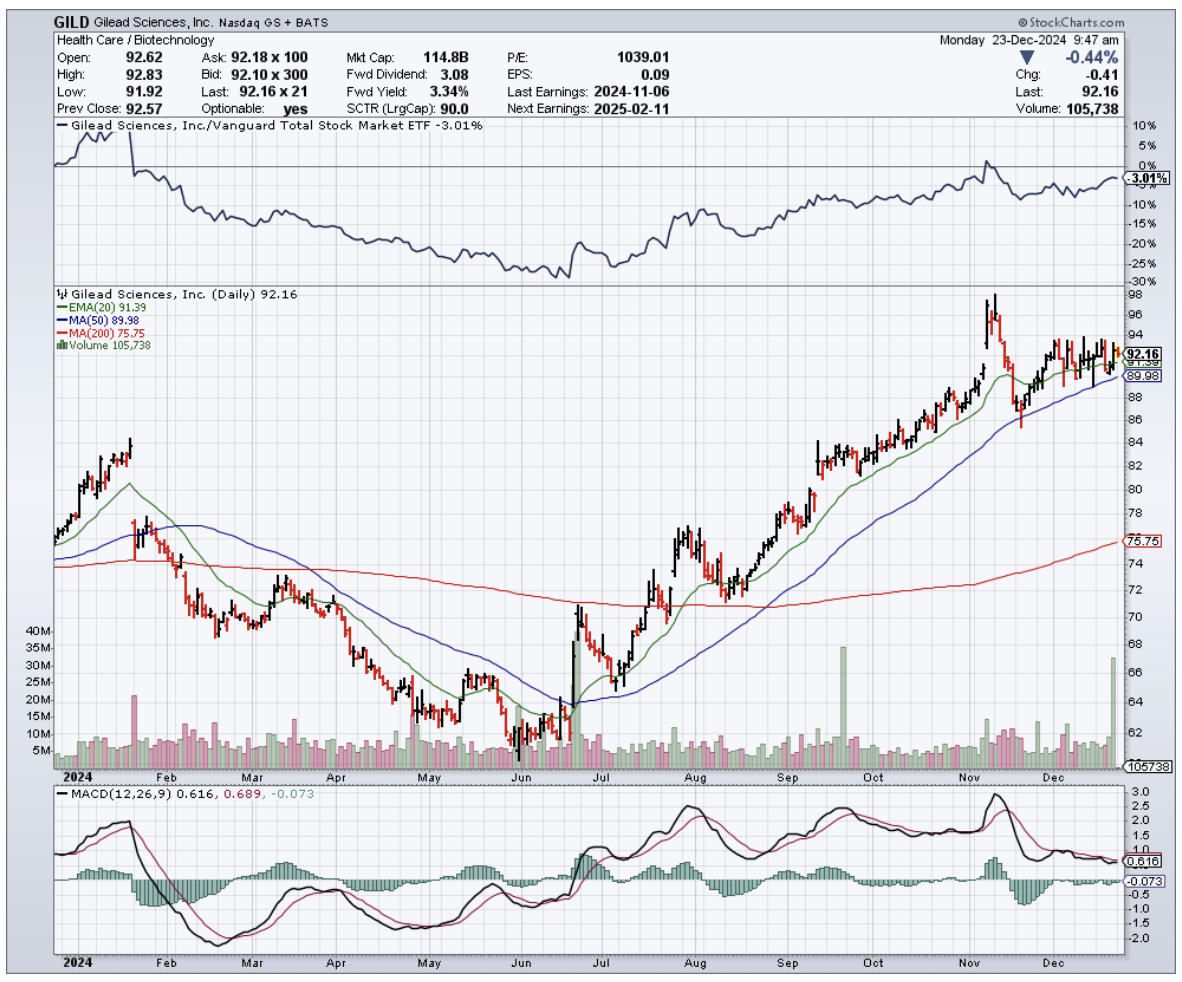

I found myself gridlocked in Bay Area traffic a few days ago, inching past Gilead's (GILD) sprawling Foster City headquarters, when my phone lit up with a call from an old friend at Goldman.

“Alright, tell me—what’s the real story with biotech this year?” she asked, her tone hovering somewhere between curiosity and exasperation. “Half my portfolio feels like a masterstroke, the other half... well, let’s just say it’s testing my patience.”

As I watched a Tesla (TSLA) weave through traffic like it was auditioning for a Fast & Furious reboot, I smiled.

Biotech has always been a bit of a high-stakes chess game—brilliance in one corner, chaos in another, and always a few surprises lurking behind the next move.

“Let me break it down for you,” I said, steering the conversation as carefully as I did my car through the bumper-to-bumper maze.

First, the winners are crushing it, and I mean crushing it. Gilead (GILD) finally cracked the code on HIV treatment, developing what's essentially a vaccine that doesn't require popping pills like they're Tic Tacs.

My contacts in clinical development tell me the Phase 3 data in cisgender women is nothing short of spectacular. With a $6 billion annual market potential by 2028, this isn't just another incremental advance - it's the kind of breakthrough that makes everyone in biotech salivate.

Then there's Wave Life Sciences (WVE) and their RNA editing technology. Remember when we thought CRISPR was the only game in town? Well, Wave just showed us there's more than one way to edit a gene.

Their liver-targeting therapy is the first successful RNA editing in humans - think of it as spell-check for your DNA, but reversible. The market's currently at $1.1 billion, but with 35% CAGR through 2030, this train is just leaving the station.

Speaking of trains leaving stations, molecular glue developers like C4 Therapeutics (CCCC) are watching Big Pharma back up the Brink's truck.

We're talking $8 billion in licensing deals this year alone. After all, when Roche (RHHBY) drops $300 million upfront - not milestone payments, mind you, but cold hard cash - you know they've seen something special in the data room.

But here's where it gets interesting, and I had to pull over at this point in the conversation because my friend wasn't going to like what came next.

CRISPR stocks? Down 20%. Editas (EDIT) and CRISPR Therapeutics (CRSP) are learning that revolutionary science doesn't always translate to revolutionary returns.

My friend Janet at the Fed might be talking about higher rates, but these companies are bleeding cash faster than a Silicon Valley startup's WeWork budget.

The obesity market? Unless your name is Eli Lilly (LLY) or Novo Nordisk (NVO), you're probably not having a great time.

Only three startups cleared $100 million in funding this year. In biotech terms, that's like trying to build a house with pocket change.

The global market's sitting at $4.1 billion, but it's more crowded than a San Francisco coffee shop during a tech conference.

And don't get me started on Walmart (WMT) and CVS (CVS) trying to play doctor. They thought they could disrupt traditional healthcare with their “get your physical next to the garden tools” model.

The result? A combined loss of $250 million and a wave of clinic closures.

The lesson here is clear: just because you can sell lightbulbs and Band-Aids in the same aisle doesn’t mean you should try to diagnose strep throat next to the automotive department.

A kid in a modded Subaru WRX cut me off as I wrapped up the call, but I left my friend with this: In biotech, timing is everything.

Gilead and Wave are showing us that patience pays off when the science is solid. Meanwhile, CRISPR stocks remind us that even the most promising technology needs good timing and deep pockets.

So, watch those clinical trial results like a hawk, and keep an eye on where the venture money's flowing.

But most importantly, remember what my old mentor used to say: "In biotech, you're not just betting on the science - you're betting on the scientist, the CFO, and sometimes, just sometimes, on whether people are ready to get their flu shot next to the garden center."

Now, where's that highway patrol when you need them?

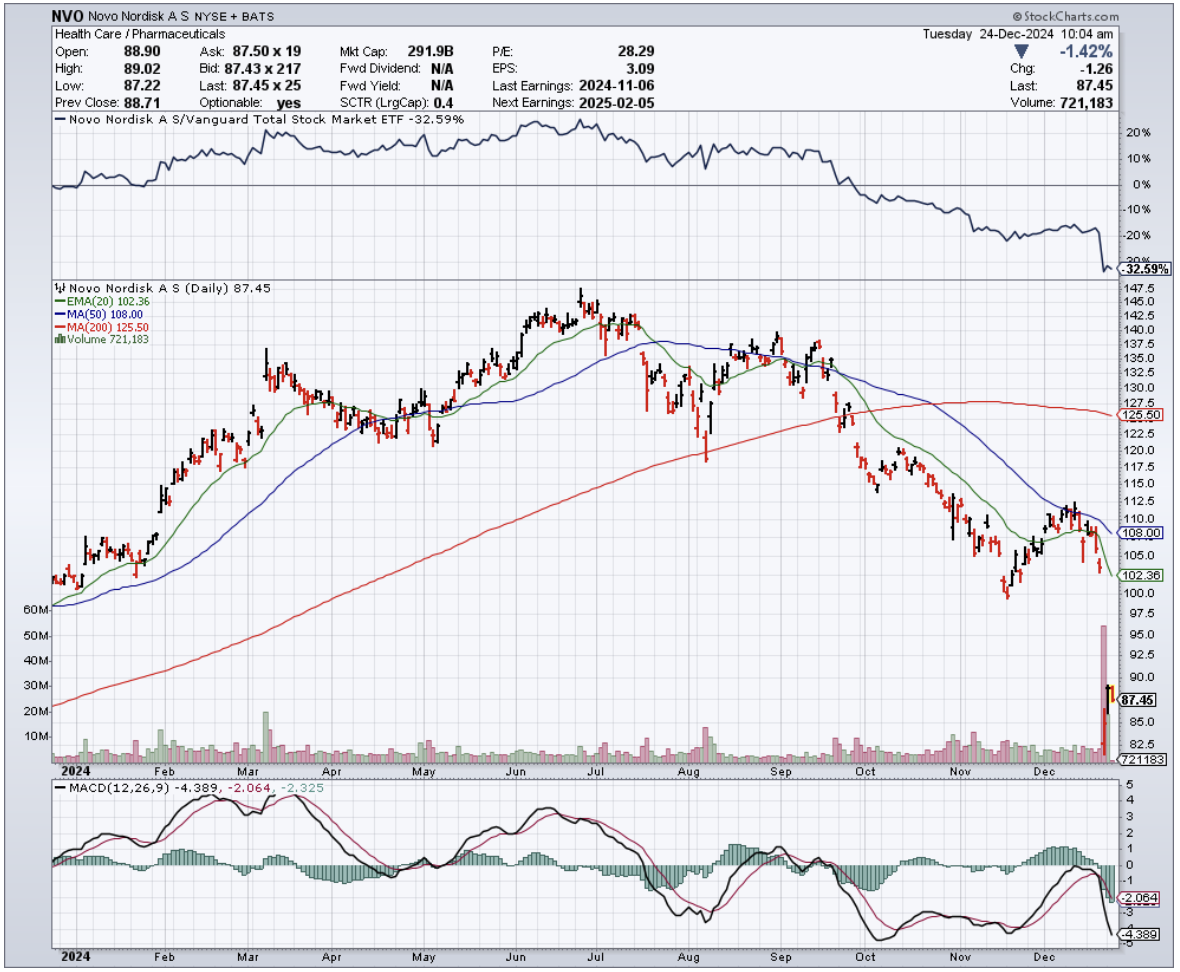

If I had a nickel for every time someone said pharmaceutical manufacturing was boring, I could’ve started bidding against Novo Holdings for Catalent (CTLT) myself.

Sure, I’d still be $16.5 billion short, but you get the point—this deal is huge, and it’s about to make some smart money look even smarter.

Here’s the deal: Novo Holdings is shelling out $16.5 billion to snap up Catalent, a contract development and manufacturing organization (CDMO).

If that acronym sounds like alphabet soup, let me translate: CDMOs are where the real action happens.

These are the guys behind the curtain making sure your miracle drugs and life-saving treatments aren’t just ideas—they’re products hitting the market at scale.

The numbers don’t lie. The CDMO market sits at $146 billion right now.

Fast-forward to next year, and that balloons to $243.3 billion. By 2029, it’s cruising toward a cool $332 billion.

And if you think that’s impressive, just wait: the broader pharmaceutical outsourcing trend is nowhere near slowing down.

In 2014, Big Pharma still clung to in-house production for 66.3% of its output.

Today? That figure’s down to 51%, and dropping fast. Why? Because outsourcing lets the specialists handle the hard stuff—faster, cheaper, and more efficiently.

For investors, Catalent’s immediate upside is a no-brainer. The acquisition premium is pure gravy, but that’s not the whole story.

Rivals like Lonza Group (SWX: LONN) and Samsung Biologics are already feeling the heat.

The biologics CDMO market alone is expected to expand by $10.63 billion between 2024 and 2028, and you better believe those two are scrambling to stay ahead.

If you own shares, keep your seatbelt fastened. If you don’t, well… you might want to rethink that.

And here’s where it gets really interesting: Novo Holdings may be private, but its publicly traded golden child, Novo Nordisk (NVO), is set to ride this wave like a pro surfer.

They’re already a global powerhouse in biologics, and Catalent’s souped-up manufacturing capabilities are going to help them scale production with military-grade efficiency.

Lower costs, tighter operations, bigger margins—it’s like handing a Formula 1 car to an already championship-winning team.

So if you’re not watching Novo Nordisk stock, you’re doing it wrong.

Of course, it’s not just the big CDMO players who stand to win here. Companies like Danaher (DHR), Repligen (RGEN), and Avantor (AVTR) are quietly cashing in on this gold rush.

These firms supply the picks, shovels, and critical bioprocessing tools that CDMOs need to keep production humming.

As Catalent scales under Novo Holdings, demand for these essentials will go through the roof.

Zooming out, the pharma manufacturing landscape is evolving at a breakneck pace.

The CDMO market is expected to hit $530.3 billion by 2033, growing at a steady 7.7% CAGR.

That’s not speculative growth—it’s a structural shift, backed by demand for biologics, gene therapies, and personalized medicine.

In short, we’re entering an era where outsourcing is king, and companies with the infrastructure to capitalize on it are poised to dominate.

Don’t forget about the big dogs in Big Pharma, either.

Pfizer (PFE), Eli Lilly (LLY), and Merck (MRK) aren’t just spectators in this game. They’re snapping up CDMO capacity, investing in biologics, and doubling down on therapies with blockbuster potential.

The Catalent deal is just the latest chess move in a game where the stakes keep getting higher.

So what does this mean for you? If you’re holding Catalent, congratulations—your portfolio is about to get a nice bump.

But the real play here isn’t Catalent alone. It’s understanding that CDMOs, suppliers, and adjacent players are the unsung heroes of this industry transformation.

You want exposure to the companies enabling the next wave of medical innovation? This is where you look.

Novo Holdings just threw down the gauntlet, and the smart money is already moving. The pharmaceutical manufacturing sector isn’t boring—it’s booming.

So, while everyone’s chasing flashy biotech startups and blockbuster drugs, the real smart money is quietly following the companies that make those breakthroughs possible.

Catalent isn’t just a $16.5 billion deal—it’s proof that outsourcing is the new backbone of pharma’s future. Call it “The Big Batch Theory:” scale up, outsource smart, and watch the returns multiply.

Ignore this shift, and you’re leaving money on the table.

Now, if you’ll excuse me, I need to check my CDMO positions. Just like a perfectly run batch, they’re growing fast—and that’s exactly how I like it."

Mad Hedge Biotech and Healthcare Letter

November 26, 2024

Fiat Lux

Featured Trade:

(NO MORE EATING AT YOU)

(PFE), (LLY), (NVO), (AMGN), (RYTM), (ALT)

Who knew the devil could lurk in an Excel spreadsheet? More specifically, in a hidden tab that, until recently, was minding its own business like a shy teenager at a school dance.

That is, until some eagle-eyed analyst at Cantor Fitzgerald decided to right-click their way into a $12 billion nightmare for Amgen.

(If you're wondering how to find these hidden tabs yourself, just right-click on any visible tab in Excel. Though after this debacle, pharmaceutical companies might start password-protecting their spreadsheets like they're nuclear launch codes.)

The data in question concerns MariTide, Amgen's hopeful contestant in the "help-America-lose-weight" sweepstakes.

The hidden tabs revealed what the published paper in Nature Metabolism conspicuously didn't mention: bone density scans that would make an osteoporologist reach for their stress ball.

Patients receiving the 420-milligram dose saw their bone density drop by about 4% over 12 weeks - the kind of number that sends stock traders reaching for their sell buttons faster than you can say "osteoporosis."

Speaking of selling, this discovery sent Amgen's stock tumbling 7%, which in the biotech world is like watching $12 billion vanish faster than free cookies at a Weight Watchers meeting.

Amgen, doing what pharmaceutical companies do best when faced with uncomfortable data, assured everyone that their Phase 1 study doesn't suggest any bone safety concerns. (One imagines their PR team working overtime, possibly sustained by the same stress-eating habits their drug aims to curb.)

Now, let's talk about the increasingly crowded room of companies trying to help elephants become gazelles.

Novo Nordisk (NVO), the current crown prince of weight-loss drugs, is sitting pretty with Wegovy raking in 17.3 billion Danish kroner (about $2.5 billion) in just one quarter.

They're so confident they're throwing $11 billion at Catalent faster than you can say "production scale-up." That's enough kroner to buy every Danish pastry in Copenhagen, though that might defeat the purpose.

Not to be outdone, Eli Lilly's (LLY) Zepbound is showing off with weight loss results that would make Jenny Craig jealous - we're talking 21% body weight reduction.

Together with Novo Nordisk, they're expected to dominate 80% of the market, leaving other companies to fight over the crumbs like desperate dieters at a birthday party.

Still, the supporting cast is equally fascinating.

Pfizer's (PFE) danuglipron and Structure Therapeutics' (GPCR) GSBR-1290 are trying to turn these injectable drugs into pills, because apparently not everyone enjoys playing pin cushion.

Viking Therapeutics (VKTX) is getting creative with VK2735, a dual GLP-1 and glucagon receptor agonist, which is pharmaceutical speak for "two mechanisms of action are better than one."

Meanwhile, AstraZeneca's (AZN) AZD5004 is trying to join the party, though their early Phase I results are about as impressive as a rice cake at a dessert buffet.

Now, let’s take a look at the numbers. The global anti-obesity drugs market is expected to balloon from $6.15 billion in 2024 to an eye-watering $37.94 billion by 2032.

But, that seems to be just the conservative estimate. Some analysts are betting this market could hit $150 billion by the early 2030s.

So, what’s the smart move here?

For those watching this space (while probably patting their own midsections thoughtfully), the message is clear: This market is hotter than a freshman chemistry experiment gone wrong.

But as Amgen's Excel adventure shows, sometimes the devil really is in the details - or in this case, in Tab 9, hidden away like a chocolate bar in a dieter's sock drawer.

And like my old friend Deng Xiaoping used to say, sometimes you have to cross the river by feeling the stones.

Today, those stones are telling me this: hold off on buying Amgen - that bone density data isn't just a minor setback, it's a potential deal-breaker.

If you really want to take part in the action, opt for Novo Nordisk and Eli Lilly for their proven ability to execute and dominate.

And for those of you who, like me, enjoy a bit of calculated risk-taking, consider a speculative position in Structure Therapeutics and Viking Therapeutics.

Before you get too excited, though, I'd suggest limiting these speculative plays to no more than 5% of your portfolio each - promising early-stage biotechs can deliver spectacular returns, but they can also crash faster than a poorly maintained MIG-25.

Mad Hedge Biotech and Healthcare Letter

November 7, 2024

Fiat Lux

Featured Trade:

(COPENHAGEN’S CASH COW)

(NVO), (LLY), (AMGN), (RHHBY), (PFE)

Mad Hedge Biotech and Healthcare Letter

November 5, 2024

Fiat Lux

Featured Trade:

(DANCING WITH SHADOWS)

(RHHBY), (SGMO), (LLY), (BIIB), (ABBV)

In 1906, Dr. Alois Alzheimer first encountered what he called a “mysterious” mental illness, examining the brain of a 55-year-old woman who had died under strange neurological circumstances.

Over a century later, that mystery hasn’t let up. We’re still scratching our heads—and burning through money.

By 2050, Alzheimer’s is projected to cost the U.S. healthcare system $1.3 trillion, more than the entire GDP of Australia.

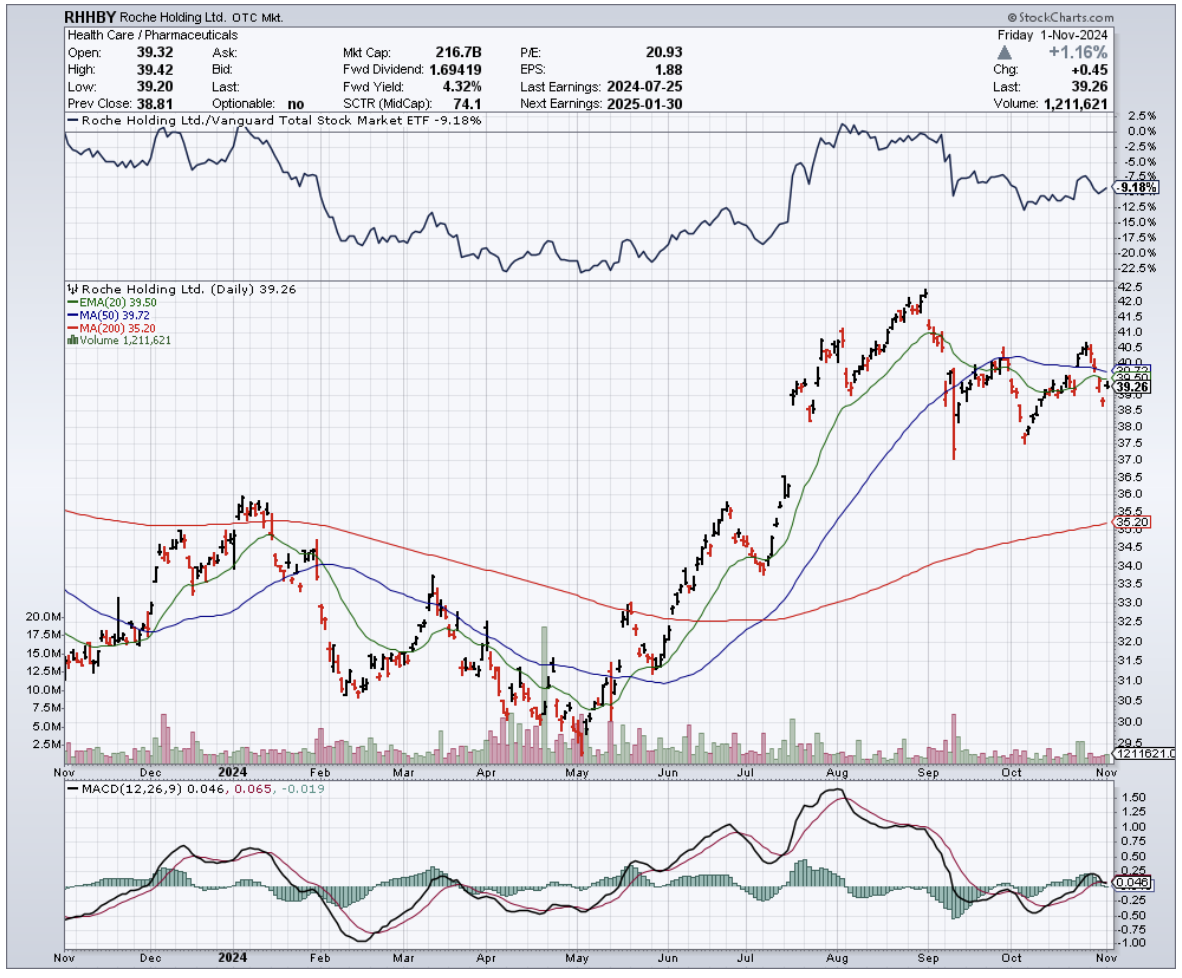

But something’s happening at Roche (RHHBY) that’s got my scientific spidey senses tingling.

Roche has been chasing Alzheimer’s solutions for over two decades, pouring resources into this elusive brain burglar that defies every rule in the book.

And yet, here they are—undaunted, driven by a noble (and, yes, profitable) goal to relieve the massive toll AD takes on patients, families, and entire healthcare systems.

It hasn’t been smooth sailing; setbacks and “whoops, not this time” moments have kept things bumpy. Recently, though, I’ve been seeing hints of a breakthrough that just might bring this long, shadowy dance with Alzheimer’s closer to the light.

For those who've been reading my letter since 2008, you know I rarely get excited about big pharma unless there's real meat on the bone. Well, this time there is, and it's called Brainshuttle technology.

If you’ve never heard of it, think of it as a kind of souped-up delivery service for the brain—no, not that kind. This tech helps Roche’s meds cross the blood-brain barrier, that stubborn security guard that only lets a select few molecules into the brain.

It’s great at keeping out random junk but also frustratingly good at blocking drugs we actually want to get in there.

Brainshuttle could change that, allowing antibodies to cross over more easily and making lower doses (and hopefully fewer nasty side effects) possible.

Enter trontinemab, a drug that’s caught a lot of eyes recently. Armed with Brainshuttle, this amyloid-beta antibody is like the brain’s personal pest control.

Early trials are promising: Roche reported that trontinemab is sweeping out amyloid plaque faster than a Roomba on espresso, and all at lower doses.

Less dose, more punch, and fewer side effects? Sounds like the AD holy grail. They’re even eyeing an accelerated approval path with the FDA.

Now, the FDA isn’t exactly known for sprinting to approval—especially with Alzheimer’s drugs—but trontinemab’s early results make it a strong contender.

But Roche isn’t putting all its eggs in one beta basket. AD research has been dominated by amyloid-beta, but there’s another protein that scientists are pretty excited about: tau.

If amyloid-beta is the ringleader, tau is the muscle, the heavy that clogs up brain cells and wreaks havoc.

To tackle tau, Roche has teamed up with Sangamo Therapeutics (SGMO), a company with tech that sounds like it’s straight out of a sci-fi novel—zinc finger molecules.

These little DNA-grabbers are designed to silence the tau gene, essentially telling it to cool it and stop producing the stuff that clogs up the brain.

The partnership also gives Roche access to something else in Sangamo’s arsenal: an adeno-associated virus capsid. (Translation: a delivery mechanism that gets things across the blood-brain barrier.)

If these tools work as planned, Roche may have a real chance to give AD a one-two punch with both amyloid-beta and tau treatments.

But let's be real here. This is still the Wild West of biotech, and Roche has had its share of setbacks.

They recently walked away from a partnership with UCB, returning the rights to an anti-tau antibody called bepranemab.

Even though UCB called the Phase 2a data "encouraging," it apparently didn't meet Roche's internal bar. That's the thing about Alzheimer's drug development - it's about as predictable as my teenager's mood swings.

The competition isn't sleeping either. Eli Lilly (LLY), Biogen (BIIB), and AbbVie (ABBV) are all throwing everything but the kitchen sink at this disease. But Roche's Brainshuttle technology might just be their secret weapon in this fight.

Here's what keeps me optimistic: Roche’s multi-pronged strategy, combining amyloid-beta and tau, might just give them an edge. It’s not guaranteed—far from it—but having multiple avenues does give them a better shot at success.

This is what I call a "chess not checkers" opportunity. The potential payoff is massive - we're talking about a market that could make crypto's best days look like pocket change. But timing is everything.

So, I'll be watching trontinemab's development like a hawk. The Sangamo collaboration is also on my radar - any breakthrough in tau-targeted therapies could be a game-changer.

As always, don’t bet the farm, folks—not even on a biotech darling like this. But if you’re itching to add a little intellectual flair to your portfolio, Roche’s Alzheimer’s gambit is worth a look. Buy the dip, but set those stop losses. After all, even the best-laid plans of mice and biochemists often go awry.