Mad Hedge Biotech and Healthcare Letter

October 1, 2024

Fiat Lux

Featured Trade:

(SAILING TO BIOTECH VALHALLA)

(VKTX), (NVO), (LLY), (AMGN), (PFE)

Mad Hedge Biotech and Healthcare Letter

October 1, 2024

Fiat Lux

Featured Trade:

(SAILING TO BIOTECH VALHALLA)

(VKTX), (NVO), (LLY), (AMGN), (PFE)

In a market full of duds and darlings, every once in a while, you stumble upon a stock that skyrockets so fast it gives you whiplash. Viking Therapeutics (VKTX) is that stock and boy, am I glad I trusted my gut on this one.

We're talking a journey from $4 to $62 in what feels like a blink of an eye - a voyage straight to biotech Valhalla, if you will. A 1,500% gain? Somebody hand me my horn of mead – and maybe a bigger treasure chest.

See what I did there? Viking stock, sailing to Valhalla – sorry, I couldn't resist. Anyway, if you missed out on this raid, don't worry. This biotech longship is still sailing strong, and it’s only getting started.

Now, I've seen my fair share of biotech booms and busts over the years, from the dizzying heights of the genome sequencing craze to the sobering lows of failed drug trials.

But this obesity drug market? It's shaping up to be the mother of all biotech booms.

At the heart of Viking's meteoric rise is a little molecule called VK-2735, a GLP-1 / GIP receptor agonist.

In layman's terms, it's a weight loss wonder drug that's got Wall Street salivating like Pavlov's dogs at dinnertime.

And why wouldn't they? We're talking about a market that could be worth north of $150 billion annually by the early 2030s.

Let's crunch some numbers, shall we? In the first half of 2024, Novo Nordisk's (NVO) dynamic duo, Ozempic and Wegovy, raked in a cool $11.7 billion.

Not to be outdone, Eli Lilly's (LLY) tag team of Mounjaro and Zepbound pulled in $6.66 billion. That's enough cash to make even a seasoned hedge fund manager's eyes water.

But here's where it gets really interesting. Viking's VK-2735, in its Phase 2 Venture study, showed weight loss results that could make even the most stubborn bathroom scale do a double-take. We're talking up to 14.7% weight loss from baseline in just 13 weeks.

Now, before you start maxing out your credit cards to buy Viking stock, let's pump the brakes a bit. This data is still in its infancy, like a toddler taking its first wobbly steps.

We're talking about a study with just 35 patients. That's barely enough people to fill a small yoga class, let alone stake billions of dollars on.

And let's not forget about safety. While VK-2735 seems to be playing nice overall, there are a few wrinkles to iron out.

The highest dose saw a 20% dropout rate, which is about as concerning as finding a shark in your swimming pool. Most patients experienced some side effects, with nausea, diarrhea, and constipation leading the pack.

Not exactly a walk in the park, but then again, no pain, no gain, right?

Looking ahead, Viking's still got its work cut out. They're aiming to kick off a Phase 3 study by Q1 2025, which means we might not see VK-2735 hit the market until Q1 2027. In biotech years, that's practically an eternity.

But here's the kicker - this delay might actually work in Viking's favor. While they're dotting their i's and crossing their t's, Novo Nordisk and Eli Lilly are out there doing the heavy lifting, expanding the market and greasing the wheels with insurers.

Still, Viking's not resting on its laurels. They're working on a monthly dosing regimen and an oral version of VK-2735.

If they pull that off, it could be a game-changer. After all, who wouldn't prefer popping a pill over jabbing themselves with a needle?

Of course, this isn't a one-horse race. The obesity drug market is starting to look like a biotech version of the Oklahoma Land Rush, with everyone from Amgen (AMGN) to Pfizer (PFE) trying to stake their claim.

But with $935 million in the bank and a net loss of only $50 million for the half-year, Viking's got the financial firepower to go the distance.

So, what's the play here? Well, given the market's current love affair with all things GLP-1, Viking's strong financial position, and the potential of both VK-2735 and their NASH candidate VK2809, I'm cautiously bullish on Viking stock.

It's a high-risk, high-reward proposition, but then again, isn't that what makes this game so damn exciting? Just don't forget to pack your Dramamine - this ride's bound to have some turbulence.

Mad Hedge Biotech and Healthcare Letter

September 24, 2024

Fiat Lux

Featured Trade:

(KNOW WHEN TO HOLD ‘EM)

(LLY), (NVO), (VKTX)

Mad Hedge Biotech and Healthcare Letter

September 19, 2024

Fiat Lux

Featured Trade:

(THE KING’S SPEECH)

(ABT), (DXCM), (LLY), (NVO)

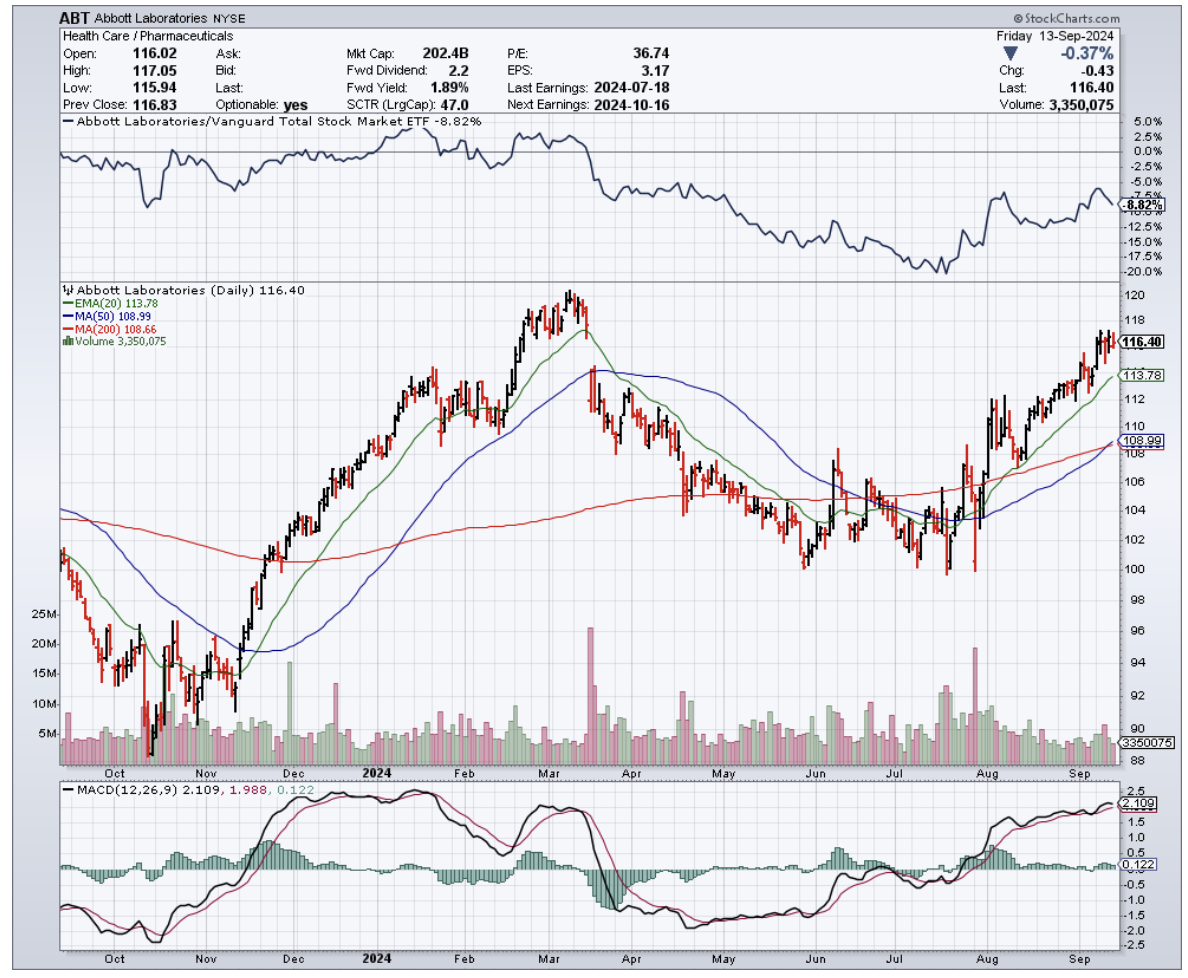

Warren Buffett once said, “Time is the friend of the wonderful company.” If that's true, Abbott Laboratories (ABT) must be Father Time's BFF because this centenarian healthcare heavyweight has been befriending our wallets for longer than most of us have been alive.

First things first: Abbott's not just any dividend stock. It's a bona fide Dividend King, having hiked its payout for over 50 consecutive years. But let's not get too misty-eyed about history.

What's got my attention is Abbott's current form. This isn't your typical sleepy pharma stock. Abbott's been flexing its muscles across multiple segments, showing growth that could very well be a worthy competition against any Silicon Valley startup.

In the first half of this year, Abbott saw positive growth in all but one segment. The laggard? Diagnostics, which took a hit as COVID-19 testing went the way of the dodo. But hey, you can't win 'em all, right?

Now, let's talk dividends. Abbott's currently yielding a respectable 1.9%, outpacing the S&P 500's measly 1.3%. With a payout ratio of 67%, there's still room for this dividend to grow.

But where's the real excitement? Two words: diabetes care.

Abbott's continuous glucose monitoring devices are hotter than a two-dollar pistol, driving 19% organic growth in the first two quarters. With diabetes becoming a bigger epidemic than we anticipated, this could be Abbott's golden goose.

Just look at the skyrocketing stocks of diabetes-focused companies like Eli Lilly (LLY) and Novo Nordisk (NVO). Different products, same lucrative market.

Abbott's FreeStyle Libre CGM system isn't just some gadget. It’s actually a genuine life-changer that's raking in $1.6 billion in quarterly sales and growing 20% year-over-year. In a market where DexCom (DXCM) is nipping at their heels, that's no small feat.

But Abbott's not resting on its laurels. They're expanding into over-the-counter CGM systems like Lingo and Libre Rio, leveraging a decade of international experience to capture more U.S. market share. It's like they're aiming to slap a diabetes monitor on every wrist in America.

And here's the kicker: the number of people living with diabetes is projected to hit 643 million by 2030 and a whopping 783 million by 2045. If that’s not the definition of a growing market, then I don’t know what is.

But Abbott isn't a one-trick pony. While they're busy trying to corner the diabetes market, they're also cooking up a storm in other areas.

Take their cardiac care lineup, for instance. Abbott's dabbling in electrophysiology with their EnSite X EP System, equipped with something called Omnipolar Technology. Sounds like something out of a sci-fi flick, right? Well, it's making cardiac mapping more precise than a Swiss watchmaker, giving arrhythmia patients a fighting chance.

But that’s not where it ends. Abbott's TriClip system is tackling tricuspid valve repair like a pro wrestler pinning an opponent. And don't get me started on their Esprit dissolvable stent. It's like the James Bond of the vascular world - it does its job and then disappears without a trace.

So, while diabetes care might be Abbott's current chart-topper right now, they've got a whole album of potential hits in the works. From glucose monitors to heart repair, Abbott's making moves that could have investors' portfolios beating as steadily as a healthy heart.

And as for you nervous nellies out there, Abbott's beta value of 0.7 suggests it's more stable than a three-legged stool. Perfect for those of you who break out in hives at the mere mention of volatility.

Now, it hasn't all been smooth sailing. Abbott recently faced a trial over claims its preterm infant formula caused a dangerous disease. But don't start panic-selling just yet.

JPMorgan and Barclays reckon the liability is likely to be smaller than a gnat's appetite. Abbott's management is confident, too, probably because the product in question accounts for a whopping... wait for it... $9 million in revenue. That's pocket change for a company like Abbott.

Looking ahead, Abbott's firing on all cylinders. They're seeing 9.3% organic revenue growth (excluding their COVID products), and they're so confident they've raised their full-year guidance.

Meanwhile, valuation-wise, Abbott's looking pretty good. With double-digit earnings growth expected and an AA-credit rating (better than some countries I could name), this stock could easily outperform the market.

So, what's the bottom line? Abbott's got the stability of a Dividend King, the growth potential of a tech startup, and more irons in the fire than a blacksmith's shop.

It's trading at a fair price, and with its track record of innovation and dividend growth, this could be your ticket to a healthier portfolio. After all, in the race for returns, slow and steady often wins more than just participation trophies. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

August 29, 2024

Fiat Lux

Featured Trade:

(ONE TEST TO RULE THEM ALL)

(ILMN), (BAYRY), (LLY), (MRK), (BMY), (AZN), (RHHBY), (NVS), (GH), (TEM), (TMO)

“One test to rule them all, one test to find them, one test to bring them all, and in the lab bind them,” the scientists at Illumina (ILMN) whispered – probably.

Their latest creation just got the FDA nod, and it's set to turn the world of cancer diagnostics on its head. It's as if Gandalf himself handed oncologists a palantír that reveals tumors' deepest secrets.

For those less versed in Middle-earth lore, this is like inventing a universal remote for tumor profiling, and oncologists can't wait to start channel surfing.

Now, you might be thinking, "What's the big deal?" Well, let me break it down for you.

This test, called TruSight Oncology Comprehensive (TSO for short), is the first FDA-approved genomic in vitro diagnostic kit that can make pan-cancer companion diagnostic claims.

In plain English, that means it's a single test that can be used across multiple cancer types. We're talking about a game-changer in precision oncology here.

Let's get into the nitty-gritty. This TSO test is a beast. It screens for a whopping 517 genes and provides comprehensive information on tumor mutational burden (TMB) and microsatellite instability (MSI).

These are crucial biomarkers that help determine how a patient might respond to immunotherapies. The breadth of data this single FDA-approved test can collect is unprecedented.

Now, you might be wondering, "Haven't we had companion diagnostics before?" Sure, but they've typically been limited to specific drugs or cancer types.

This pan-cancer test from Illumina is different. It can be applied to a wider range of solid tumors, and let me tell you, oncologists are loving it.

In fact, about 39% of U.S. oncologists have already said they strongly prefer using multi-gene panels over single-gene tests for guiding treatment decisions. That's a clear signal that there's demand for comprehensive diagnostic solutions like TSO.

Illumina's been busy across the pond, too. A version of this test has been available in Europe since 2022. But the U.S. version's got some new tricks up its sleeve.

It can help identify patients who might benefit from specific immunotherapies, including Bayer's (BAYRY) Vitrakvi and Eli Lilly's (LLY) Retevmo. The latter is a new addition compared to the EU version of the test.

Let's talk about these therapies for a second. Vitrakvi is used for adult and pediatric patients with certain NTRK mutations, regardless of their type of cancer. That's pretty cool, right?

But here's the kicker - these NTRK gene fusions are only found in about 0.1% to 0.3% of solid tumors, and they're tough to detect.

TSO's ability to scan both RNA and DNA means it can find multiple forms of this biomarker. That's a big deal for companies like Bayer, who've sometimes struggled to find eligible patients for this targeted therapy.

But Illumina's not resting on its laurels. They've got a growing pipeline of companion diagnostic claims in development, working hand in hand with drugmakers. They're planning to seek these in future regulatory submissions.

You see, Illumina's been playing the long game, forging partnerships with big pharma to co-develop companion diagnostics that align with targeted therapies.

Take their 2019 partnership with Merck (MRK), for instance. They teamed up to develop and commercialize a companion diagnostic using Illumina's TruSight Oncology 500 assay.

The goal? To identify genetic mutations in cancer patients that would respond to Merck's cancer drugs like Keytruda. This partnership boosted the adoption of Illumina's NGS platform in clinical oncology settings, contributing to both companies' growth.

The market liked what it saw at the time. Illumina's stock got a nice bump following the partnership announcement. And why wouldn't it?

The deal strengthened Illumina's position in the oncology diagnostics market, which is projected to grow at a CAGR of 12.4% from 2023 to 2030.

But Merck's not the only dance partner Illumina's got. They've also teamed up with Bristol-Myers Squibb (BMY) to use their TSO 500 assay as a companion diagnostic for immuno-oncology therapies.

This collaboration expanded Illumina's reach into new oncology applications, allowing BMY to use the TSO platform to identify patients most likely to benefit from its immune checkpoint inhibitors.

And there's more - Illumina's also forged partnerships with AstraZeneca (AZN), Roche (RHHBY), and Novartis (NVS) to develop companion diagnostic tests.

Next, let's talk numbers. Each new FDA-approved indication could potentially add $100 million to $200 million annually to Illumina's revenue. That's no chump change.

Unsurprisingly, Illumina's not the only player in this game.

Companies like Foundation Medicine (a Roche subsidiary), Guardant Health (GH), Tempus (TEM), Caris Life Sciences, Thermo Fisher Scientific (TMO), and GRAIL (another Illumina subsidiary) are all working towards pan-cancer or multi-cancer diagnostics.

Still, Illumina's TSO test is the first to secure FDA approval for pan-cancer companion diagnostic claims. This lead could translate into a significant market advantage.

Actually, Illumina already holds more than 70% market share in the global NGS market as of 2022. This means it’s well-positioned to benefit from this growth, and this latest FDA approval could further consolidate its market dominance.

Speaking of the FDA, they’ve been busy too. They've ramped up their support for precision medicine in recent years, approving a growing number of companion diagnostics and genomic tests.

From 2017 to 2021, they approved over 25 new companion diagnostics, a significant increase from the 5-10 approvals per year in the early 2010s. And a substantial portion of these approvals has been for oncology-related tests.

In 2021 alone, 68% of the FDA's new drug approvals were for cancer treatments.

Now, let's zoom out and look at the bigger picture. According to the World Health Organization, there were an estimated 19.3 million new cancer cases and 10 million cancer deaths worldwide in 2020.

The global cancer burden is expected to rise to 28.4 million cases by 2040, a 47% increase from 2020.

In the U.S., about 1.9 million new cancer cases are expected to be diagnosed in 2023.

The economic impact is also staggering. The economic burden of cancer in the U.S. was estimated at $157 billion in 2020, and it's projected to increase to over $246 billion by 2030.

These numbers stress the growing need for early detection and personalized treatment solutions.

But, unlike other companies, here's where advanced diagnostics like Illumina's TSO can make a difference. By ensuring patients receive the most effective treatments based on their genetic profiles, these tests can reduce unnecessary treatments and improve outcomes.

Studies have shown that using precision diagnostics can lower overall healthcare costs by 15% to 20% by avoiding ineffective therapies and hospitalizations.

Essentially, what we're seeing here is more than just a new test. It's a glimpse into the future of cancer treatment - more precise, more personalized, and potentially more effective.

For patients, it could mean better outcomes. For healthcare systems, it could mean more efficient use of resources. And for us? Well, it could mean significant opportunities in a rapidly growing market.

As Gandalf might say, "All we have to decide is what to do with the time that is given us." Illumina's chosen to use their time crafting this powerful new tool.

The quest to conquer cancer continues, and Illumina’s TSO might just be the ring-bearer we've been waiting for.

Keep your eyes peeled, fellow adventurers. The journey into precision oncology is only just beginning, and it promises to be an epic saga indeed.

Mad Hedge Biotech and Healthcare Letter

August 27, 2024

Fiat Lux

Featured Trade:

(NOT ALL THAT GLITTERS IS LILLY)

(JNJ), (LLY), (CRSP), (ISRG)

I've been so busy chasing after Eli Lilly (LLY) and its trillion-dollar dreams that I nearly overlooked a gem in the making.

While everyone's obsessing over LLY's march towards that coveted $1 trillion market cap, there's another pharma giant that's been quietly chugging along, building value like it has for over a century.

I'm talking about Johnson & Johnson (JNJ). You know, that little company that's only been around for 138 years.

I understand that JNJ isn’t as exciting as the likes of Crispr Therapeutics (CRSP) with their fancy gene editing therapies, or Intuitive Surgical (ISRG) with their robotic surgeons, but, let me tell you, sometimes boring is beautiful – especially when it comes with a 3% dividend yield and a rock-solid business model.

Let's break it down, shall we?

First off, JNJ isn't sitting on its laurels. Just last week, they dropped $1.7 billion to snatch up a private heart-device company. That's not chump change, even for a behemoth like JNJ.

And speaking of big moves, the FDA just gave them the green light for a chemotherapy-free lung cancer treatment.

We're talking about Rybrevant plus Lazcluze, which showed a 30% reduction in the risk of disease progression or death compared to AstraZeneca's (AZN) offering.

That's not just incremental progress – that's potentially life-changing stuff for patients.

But they’re not stopping there. They're also shelling out $600 million upfront (with potential milestone payments up to $1.1 billion) for V-Wave, a company making shunts for heart failure patients.

This deal's expected to close before the year's out, beefing up JNJ's already impressive MedTech division.

Now, let's talk numbers. JNJ's current market cap is sitting pretty at just under $400 billion. Sure, it's not in Lilly's $850 billion stratosphere, but remember – slow and steady wins the race.

And speaking of winning races, JNJ was the global leader in pharmaceutical sales last year, raking in $85 billion. That's a cool 30% higher than their closest competitor, Roche (RHHBY).

But here's where it gets interesting for value hunters. JNJ's currently trading at an enterprise value of 12.8 times forward EBITDA. In English? It's reasonably priced compared to its peers.

Even better, it's trading near the bottom of its five-year range for forward P/E ratio, EV-to-EBITDA, and price-to-free cash flow. Translation: This stock's on sale, folks.

Now, I know what some of you are thinking. "But what about those talcum powder lawsuits?" Fair question.

JNJ's looking at potentially settling around $6.5 billion worth of claims. That's not a small amount, even for these guys.

But here's the kicker – they've got over $25 billion in cash on hand and generated about $19 billion in free cash flow over the last 12 months. They can take the hit and keep on ticking.

Let's talk products. Stelara, Tremfya, Darzalex, Erleada – these aren't just random drug names. They're cash cows for JNJ. And with a diverse portfolio where no single drug accounts for more than 13% of total sales, they're not putting all their eggs in one basket.

Still, I'm not saying JNJ is going to double overnight. This isn't some flashy tech stock riding the AI hype wave.

But for those of us with a long-term horizon and a love for steady income, JNJ looks mighty attractive.

Think about it – they've raised their dividend for over six decades straight. That's longer than some of you reading this have been alive.

And with a 77% payout ratio, they've got room to keep that streak going.

Sure, over the past decade, JNJ's total return of 106% might not set your hair on fire. It lags behind the S&P 500's 234% and even the Health Care Select Sector SPDR Fund ETF's (XLV) 189%.

But remember, past performance doesn't always guarantee future results.

Here's my take: JNJ isn't for the get-rich-quick crowd. It's for investors who appreciate a good night's sleep knowing their money's in a company that's weathered world wars, depressions, and yes, even lawsuits.

Will JNJ hit that trillion-dollar mark? I'd bet my last bottle of Tylenol on it. It might take a decade, but hey, good things come to those who wait.

Mad Hedge Biotech and Healthcare Letter

August 22, 2024

Fiat Lux

Featured Trade:

(BITING OFF MORE THAN THEY CAN CHEW)

(LLY), (NVO), (CTLT), (ZLDPF), (RHHBY), (AMGN), (PFE), (LZAGY), (TMO)